On January 7th, 2026, we listed the Global X Zero Coupon Bond ETFs on the New York Stock Exchange ARCA. This is a suite of ETFs that seeks to provide exposure to the FTSE Zero Coupon US Treasury STRIPS index series, which is composed of six individual funds that are each tied to a distinct maturity year from 2030 through 2035. Each ETF holds U.S. Treasury securities that mature in its respective target year, giving investors low-default-risk exposure and the ability to target specific points along the yield curve.

U.S. Treasury exposure is typically viewed as a relatively conventional investment. Backed by high credit ratings from mainstay agencies like Moody’s, Fitch, and Standard & Poors, treasury bonds are frequently referred to as safe-haven assets and an alternative to corporate bonds. What’s less discussed, however, is that the way investors obtain Treasury exposure can materially shape the characteristics of that position.

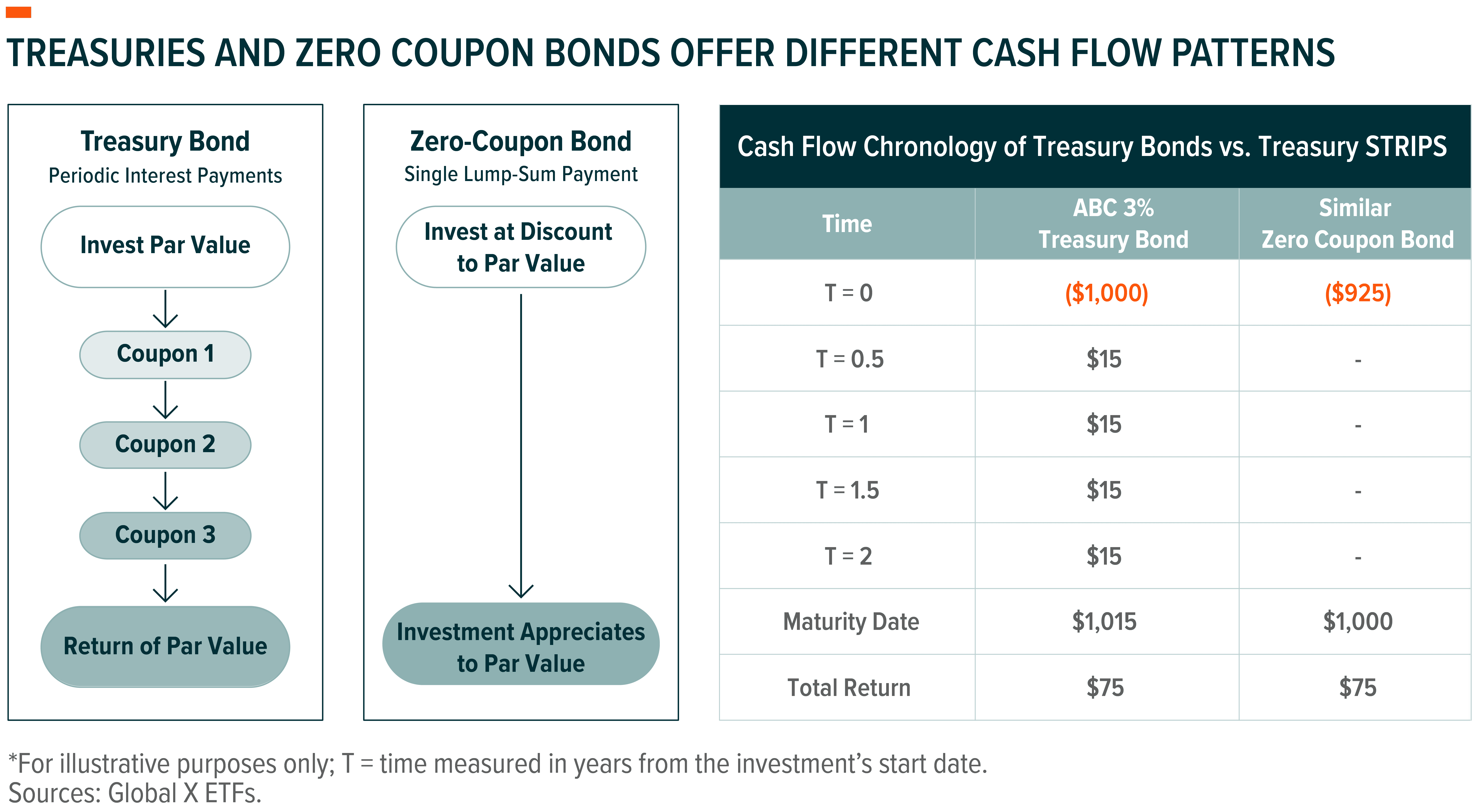

With traditional Treasury bills, notes, and bonds, investors generally know what to expect: periodic coupon payments, sensitivity to interest-rate movements, and a return of principal at maturity. Despite differences in income, duration, and rate exposure, the underlying cash-flow structure is consistent. Zero-coupon securities like STRIPS preserve the credit quality that standard Treasury bonds possess, but they fundamentally alter that cash-flow profile. Instead of receiving coupons, investors buy the bond at a discount and receive the full par value at maturity. This structure offers a distinct form of Treasury exposure that can free up near-term capital and potentially improve financial flexibility. The Global X Zero Coupon Bond ETFs are built to deliver Treasury exposure in this way, promoting capital efficiency, predictable duration metrics, and a seamless fit through the ETF structure into the workflows of modern portfolio construction.

Key Takeaways

- The Global X Zero Coupon Bond Suite of ETFs consists of six funds; each tied to a distinct maturity year from 2030 through 2035. Their relative value proposition centers around capital flexibility and duration management.

- By packaging zero coupon bonds into ETFs, treasury investors have the opportunity to pursue their exposure with less of an initial investment required relative to treasury bonds themselves. They also have the potential to receive periodic distributions.

- A suite of zero-coupon bond ETFs promotes investors’ ability to target specific maturity dates across the yield curve or take an agnostic or laddered approach by allocating them across successive maturity dates.

Zero Coupon Bond Exposures May Enhance Capital Flexibility

Treasury bonds and zero-coupon bonds are similar in that they possess good credit quality, having been issued by the Federal government. They also come with their own measures of duration and convexity risk like any other fixed income instrument. Their meaningful differences emerge elsewhere. For investors managing diversified portfolios, the defining distinction lies in their cash-flow structures, which can materially influence portfolio behavior and outcomes.

A Structural Shift That Frees Capital

When an investor buys a traditional Treasury bond, they pay the full par value upfront, receive semiannual coupon payments until maturity, and then collect their principal at the end of the bond’s term. Zero coupon bonds operate differently. Instead of paying par, investors purchase them at a discount, retaining more cash upfront to deploy elsewhere. The bond then accretes in value over its life, ultimately reaching par at maturity. In effect, the return that would normally be delivered through periodic coupons is realized through price appreciation instead.

The ETF Wrapper Offers Income Potential and a Duration Profile That Supports Precision

The lack of an income incentive represents one of the primary drawbacks associated with traditional zero-coupon bond exposure. However, when held inside an ETF, the experience has the potential to take on a much more investor-friendly shape. As the underlying STRIPS accrete toward par, the fund recognizes taxable income, which creates a basis for it to perform recurring distributions.

For many investors, this is more than a simple convenience. Regular distributions help support cash-flow planning, satisfy required income mandates, and provide a steadier rhythm of portfolio activity than a single lump-sum payout at maturity. In other words, the ETF structure preserves the capital-efficiency benefits of zero-coupon exposure while reintroducing an income profile that aligns with how many fixed income strategies are actually implemented.

Since the securities held within the ETF do not pay coupons, they are expected to continue offering duration profiles that closely match their dates of listed maturity. This differs from traditional Treasury bonds, as well, because they exhibit shorter durations due to the periodic return of coupon income, which faces less interest-rate sensitivity than the final principal payment. As a result, the Global X Zero Coupon Bond suite provides investors with a clear, predictable rate-risk profile that might help those looking to fine-tune duration exposure or position portfolios deliberately across the yield curve.

Locking in Rates Matters When Zero Coupon Bond ETFs Can Still Perform Distributions

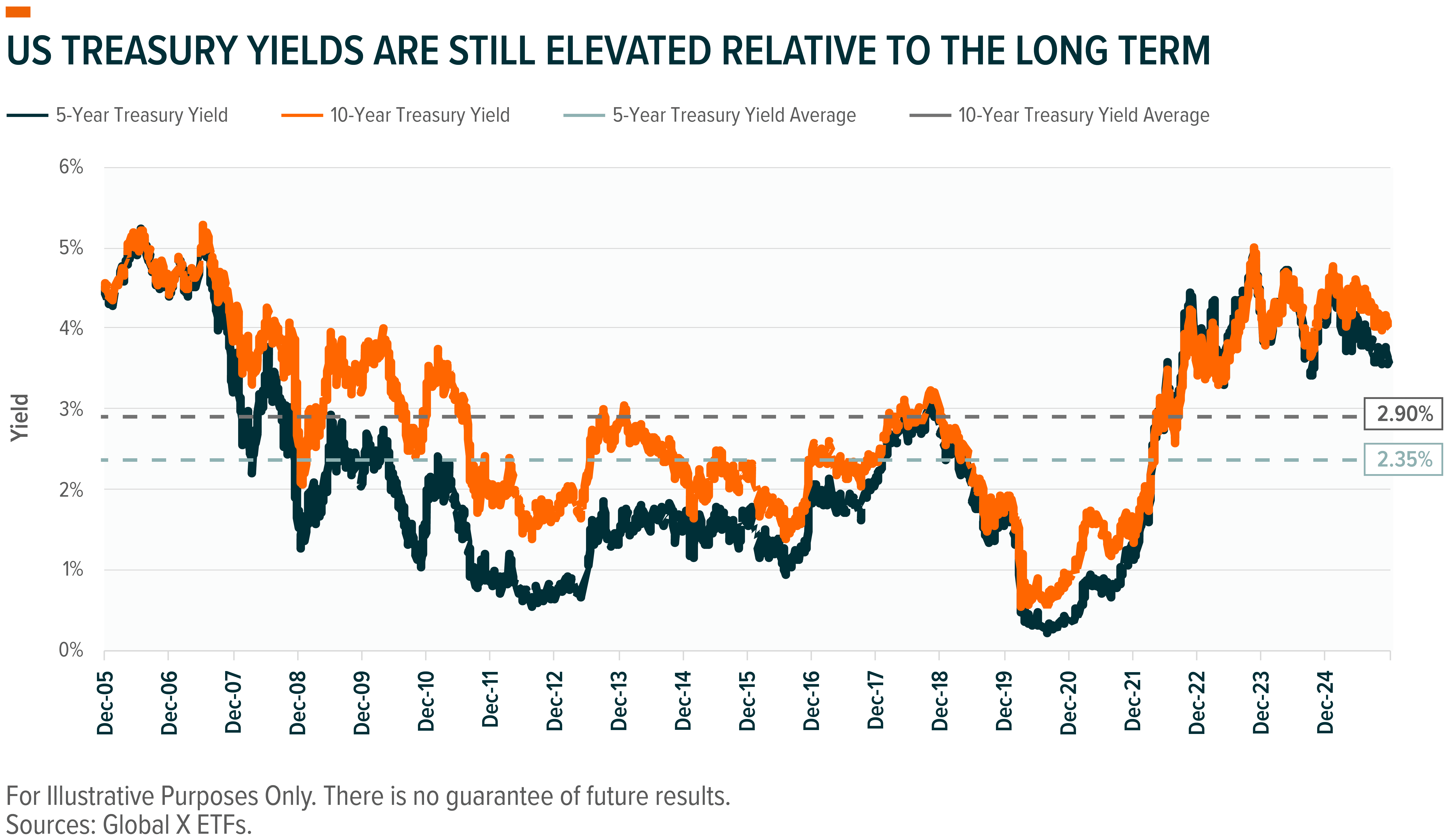

Over much of the last fifteen years, fixed income investors have had limited opportunities to capture meaningful yield. After the post-2008 recovery began to raise rates modestly in the late 2010s, the COVID-19 pandemic abruptly reversed that progress, pushing yields back to historic lows. Only after the Fed’s aggressive tightening cycle in 2022/2023 did Treasury markets reestablish yield levels that resembled long-term historical norms. These higher rates have reshaped conversations around income, inflation, and duration positioning, and they’ve renewed investor interest in strategies that can efficiently lock in yield at favorable points on the curve.

Over the last year or so, economic growth and accompanying inflation has led the Federal Reserve (Fed) to tighten monetary policy, and it has had a direct impact on these recently generous rates. That said, relative to long-term averages, investors are still able to fetch yields on U.S. Treasuries that are materially higher than much of the last twenty years. For investors looking to preserve today’s yield levels, zero-coupon exposure can be an effective tool.

Within the ETF wrapper, not only are the Global X Zero Coupon Bond ETFs able to benefit from these higher interest rates, while they retain the structural benefits of zero-coupon exposure. They also operate within a regulated fund framework that can support recurring distributions. Indeed, under the Investment Company Act of 1940, funds must distribute substantially all of their taxable income. So, while owning a zero-coupon bond might result in no physical cash flow to the ETF until the bond reaches maturity, the fund should experience an unrealized capital gain from the bond appreciating en route to its par value. This results in a periodic distribution from the ETF and, in fact, those distributions may come more frequently than that which would have been received had an investor owned a treasury bond outright. The Global X Zero Coupon Bond ETFs expect to perform distributions on a monthly basis. This might be considered preferable to certain investors to the semi-annual coupons that are offered by treasuries. It can help investors recognize a consistent source of income and meet spending goals or tax obligations.

A Laddered Bond Exposure May Promote a Smoother Return Profile

The capital flexibility offered by zero-coupon bonds can be compelling, but investors must balance that against the higher duration sensitivity inherent in their structure. For those seeking a defined cash flow at a specific future date, accepting that added rate sensitivity may be worthwhile, particularly within a target-maturity framework where outcomes are clearly scheduled.

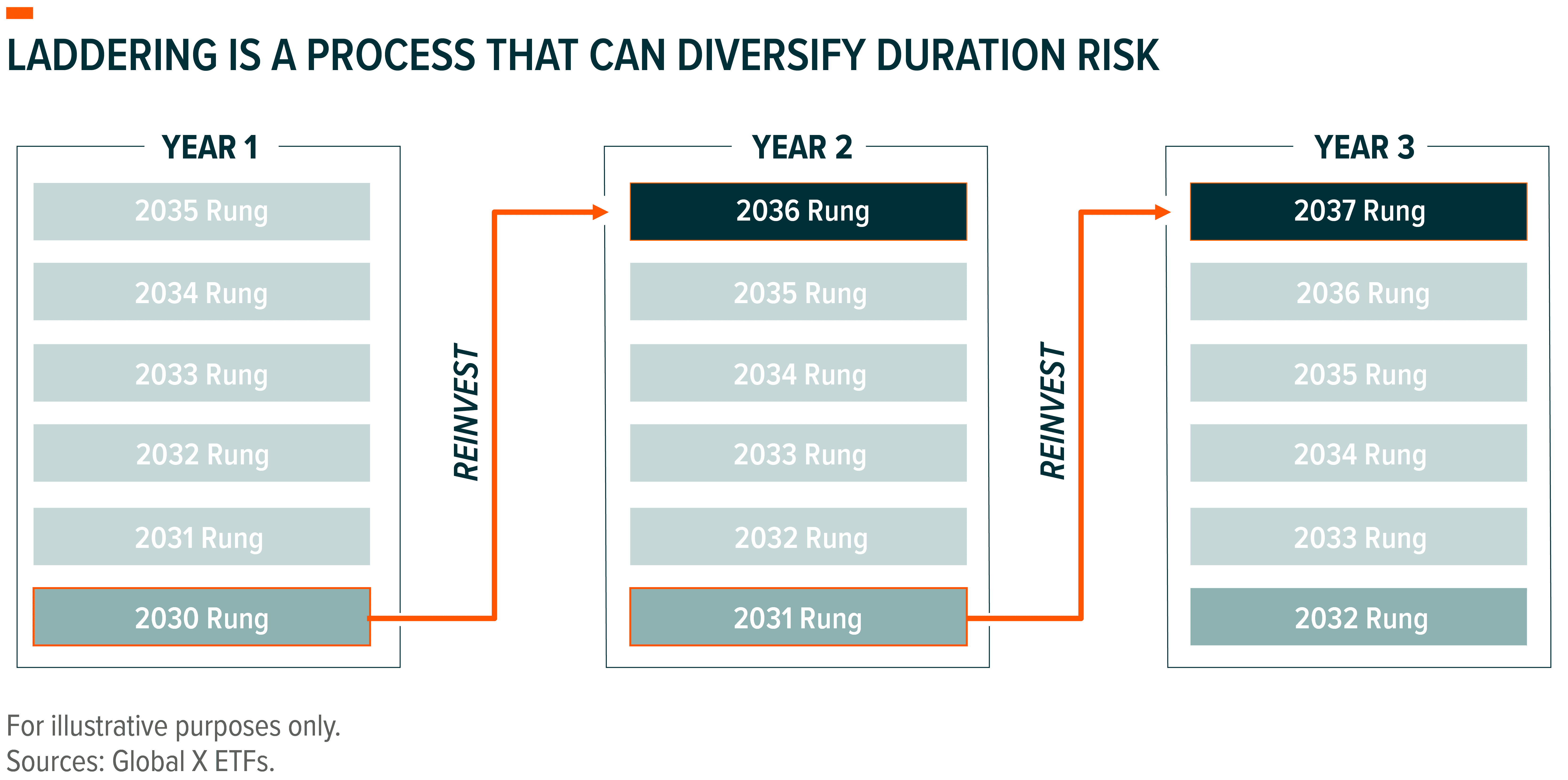

For investors using zeroes primarily for capital efficiency, however, concentrating exposure in a single maturity year may introduce more volatility than desired. Allocating across multiple maturity dates, like that which takes place in a laddering strategy, can help moderate this effect. Laddering is the practice of holding bonds with staggered maturities. As each rung of the ladder matures, the investor needs only reinvest a portion of their total portfolio. The diversified allocations work in that way to mitigate reinvestment risk. They also add an element of diversification by spanning exposures across various points across the yield curve, which interact differently with changes in interest rates and economic news.

With the Global X Zero Coupon Bond suite, investors can choose to target a specific maturity year or allocate across multiple maturities to build a laddered profile. This flexibility allows them to pursue capital efficiency while also mitigating some of the typical drawbacks associated with concentrating exposure in a single zero-coupon bond fund.

Laddering isn’t the only opportunity that these funds offer to help mitigate reinvestment risk. At their core, zero coupon bonds address this influence by accreting to par value rather than paying coupons. These coupons differ from the distributions that a zero-coupon bond ETF might perform, as it is necessary to reinvest the coupons at the treasury bond’s original rate of return to achieve the yield at which it is listed. The distributions ETFs perform as a function of zero-coupon bond unrealized income is reflective of the compounding that has already occurred inside the bond, where any additional growth that could be realized by reinvesting the distribution would likely be considered additional upside potential.

Conclusion: Global X’s Zero Coupon Bond ETFs Offer a Capital-Efficient Path to Treasury Exposure

Investors often turn to treasuries as means of generating a low-default-risk return or as an opportunity to mitigate broader portfolio volatility. Zero coupon bonds share these core attributes, but their structure adds an additional layer of potential value. The Global X Zero Coupon Bond ETFs offer investors target maturity exposure, and they can be implemented into a portfolio individually or be combined to form a broader strategy. By reducing upfront capital requirements, these ETFs may free up resources for managers to pursue other opportunities while still aligning with defined goals and cash-flow needs. They also offer tools to help address reinvestment risk and support more deliberate financial planning.

Related ETFs

ZCBA – Global X Zero Coupon Bond 2030 ETF

ZCBB – Global X Zero Coupon Bond 2031 ETF

ZCBC – Global X Zero Coupon Bond 2032 ETF

ZCBE – Global X Zero Coupon Bond 2033 ETF

ZCBF – Global X Zero Coupon Bond 2034 ETF

ZCBG – Global X Zero Coupon Bond 2035 ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.