Robots represent the clearest real-world expression of AI. After decades of steady progress and deployment, we believe the technology is approaching growth inflection as AI models become more capable, underlying semiconductors improve, and robotic hardware costs decline. Growth could compound as form factors like Humanoids expand capabilities and, in turn, use cases.

Beyond the technological inflection, there’s also a developing economic case for automation. Robots enable efficient production and delivery of goods and services and are central to the competitiveness of developed countries like the United States. Their role is rising as companies reshore manufacturing, strengthen domestic supply chains, and adapt to a more fragmented global order.

Taken together, technological advances, supportive policy, and the West’s push to rebuild industrial capacity are strengthening the Robotics theme. The Global X Robotics and Artificial Intelligence ETF (BOTZ) targets robotics leaders, innovators, and key value chain participants, seeking to provide targeted thematic exposure to the companies deploying automation across manufacturing, logistics, healthcare, consumer, and a range of other end markets.

Key Takeaways

- Robotics may be approaching a commercial breakthrough as AI enhances real-world automation.

- Governments and companies increasingly view automation as a critical lever to sustain economic competitiveness.

- The Global X Robotics & Artificial Intelligence ETF (BOTZ) seeks to deliver targeted exposure to the robotics value chain.

Robots: Core to Productivity

Automation’s role in economic growth isn’t new. Robots have been used in factories since the 1960s, when the first modern industrial robot, Unimate, was installed on a General Motors assembly line to handle hazardous tasks such as die-casting and spot welding, reducing workers’ exposure to molten metal and heavy parts.1 That history is a useful reminder that robotics began as a productivity lever and a safety upgrade, then scaled because it lifted output per worker while improving precision, uptime, and quality.

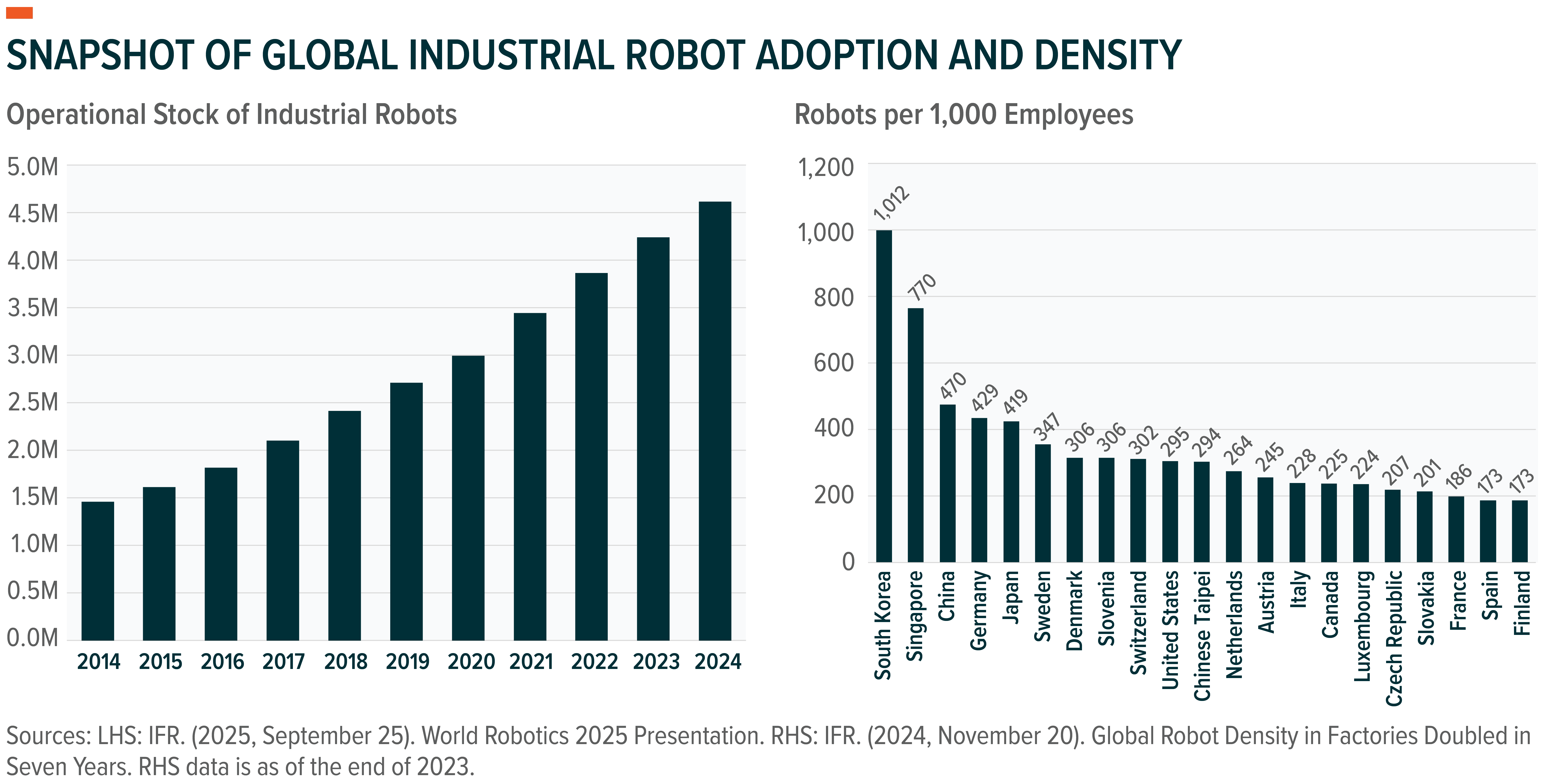

That productivity logic still defines the market today, but on a far larger scale. In 2024, nearly 4.7 million robots operated in factories worldwide – roughly triple the level of a decade ago.2 In industries like automotive, electronics, and metal fabrication, robots have become a core input to competitiveness, where cycle time, quality, and machine utilization directly determine margins. Manufacturing powerhouses like South Korea, China, and Japan have expanded robot adoption alongside human labor to sustain cost and quality advantages at scale, demonstrating how automation can underpin long-term national competitiveness in industrialized economies.3

The U.S. – despite being an early pioneer – did not industrialize robotics to the same extent, leaving meaningful room for other nations to catch-up. Robots account for only about 3% of the U.S. workforce in 2023, compared with more than 10% in South Korea, as decades of offshoring and weak industrial investment reduced urgency to automate at scale.4 That backdrop is now changing as western economies look to rebuild industrial capacity, reshore critical supply chains, and expand production in sectors such as semiconductors and pharmaceuticals. These efforts are also colliding with tight labor markets, rising wages, and complex production processes, which make automation less a choice and more a baseline requirement for competitiveness.5,6

This cycle is more consequential as robotics capabilities improve alongside rising demand for automation. Advances in AI are improving robots’ perception, navigation, and control, enabling them to perform a broader range of tasks than traditional fixed automation. As a result, robots are evolving from a narrow factory tool into a broader platform for physical automation. That shift matters: a 1% increase in industrial robot density has been linked with a 0.8% increase in labor productivity.7 The impact is likely to scale further as newer generations of robots bring more capabilities to market.

Automation’s Next Phase: Smarter, Cheaper, and Policy-Supported Growth

In our view, 2026 is shaping up to be a pivotal year that could cement the role robots play in the economy, as three forces converge to likely accelerate adoption: improving technology, falling costs, and a stronger policy and capital support for domestic industrial capacity.

- Robotic Technology Is Rapidly Improving: In just the past few years, advances in compute and chips have materially expanded robotic intelligence capabilities. For example, Nvidia – a key supplier to the robotics ecosystem – launched its Jetson Thor platform for physical AI in 2025, delivering 7.5x more compute performance than the prior generation while improving energy efficiency by 3.5x.8 At the same time, large language models (LLMs) are expanding robot perception and execution by combining vision, language, and reasoning into task-specific outcomes.9 For years, robotics adoption was constrained less by hardware than by the limits of the digital stack, including compute, sensing, control, and software. Those constraints are now easing. As those constraints ease, the frontier of what robots can do is expanding.

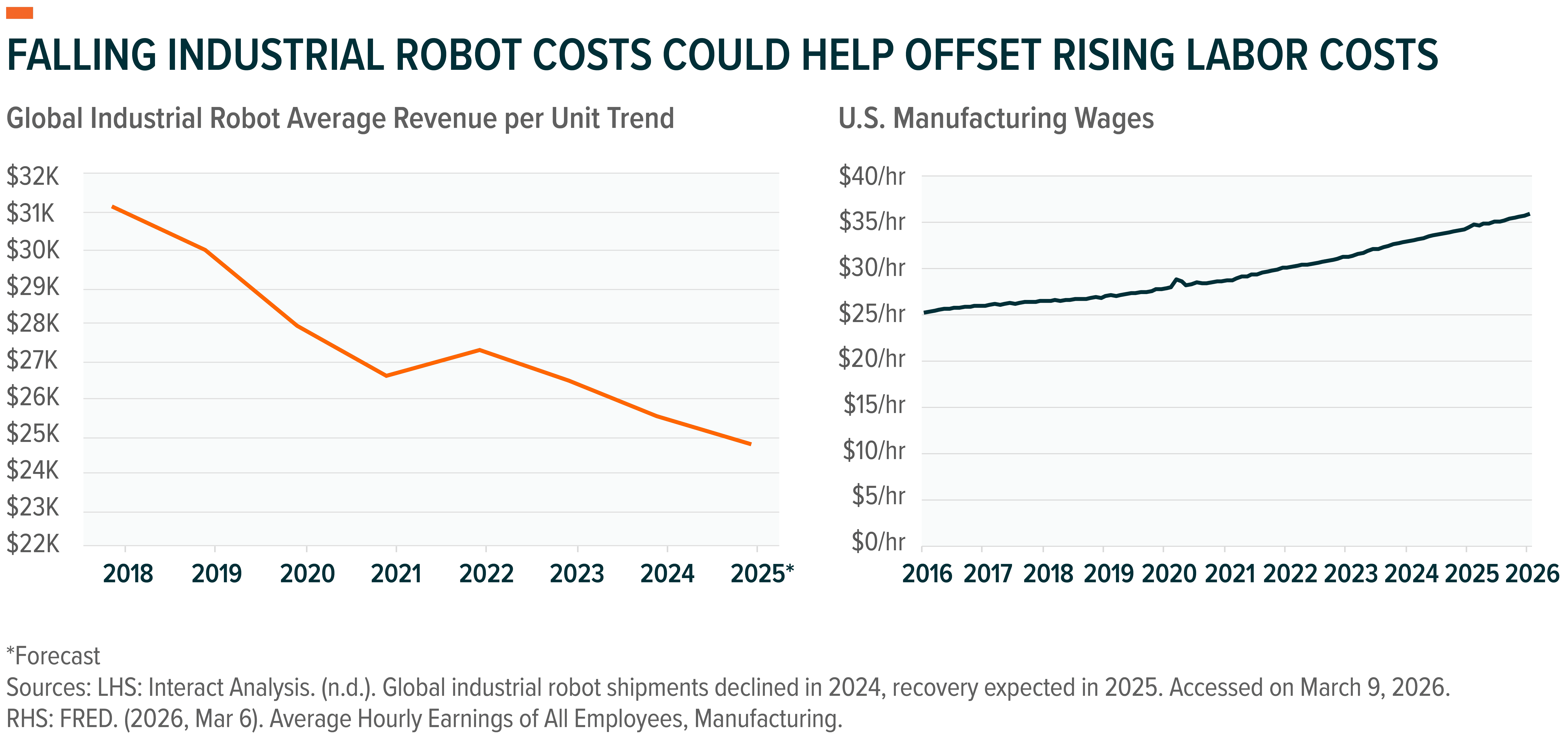

- Economics of Robotics Are Getting Better: Average revenue per industrial robot unit fell from roughly $31,100 in 2018 to about $25,600 in 2024, as higher production volumes and intensifying competition pushed pricing lower.10 Collaborative robots have followed the same direction.11 Simultaneously, the rise of business models like robotics-as-a-service models allows companies to treat automation spending as an operating expense rather than a capital expenditure, expanding adoption across smaller and more resource-constrained businesses. The combination of improving performance, falling costs, and a rapidly advancing software layer is expanding the range of viable applications across industrial and commercial workflows.12

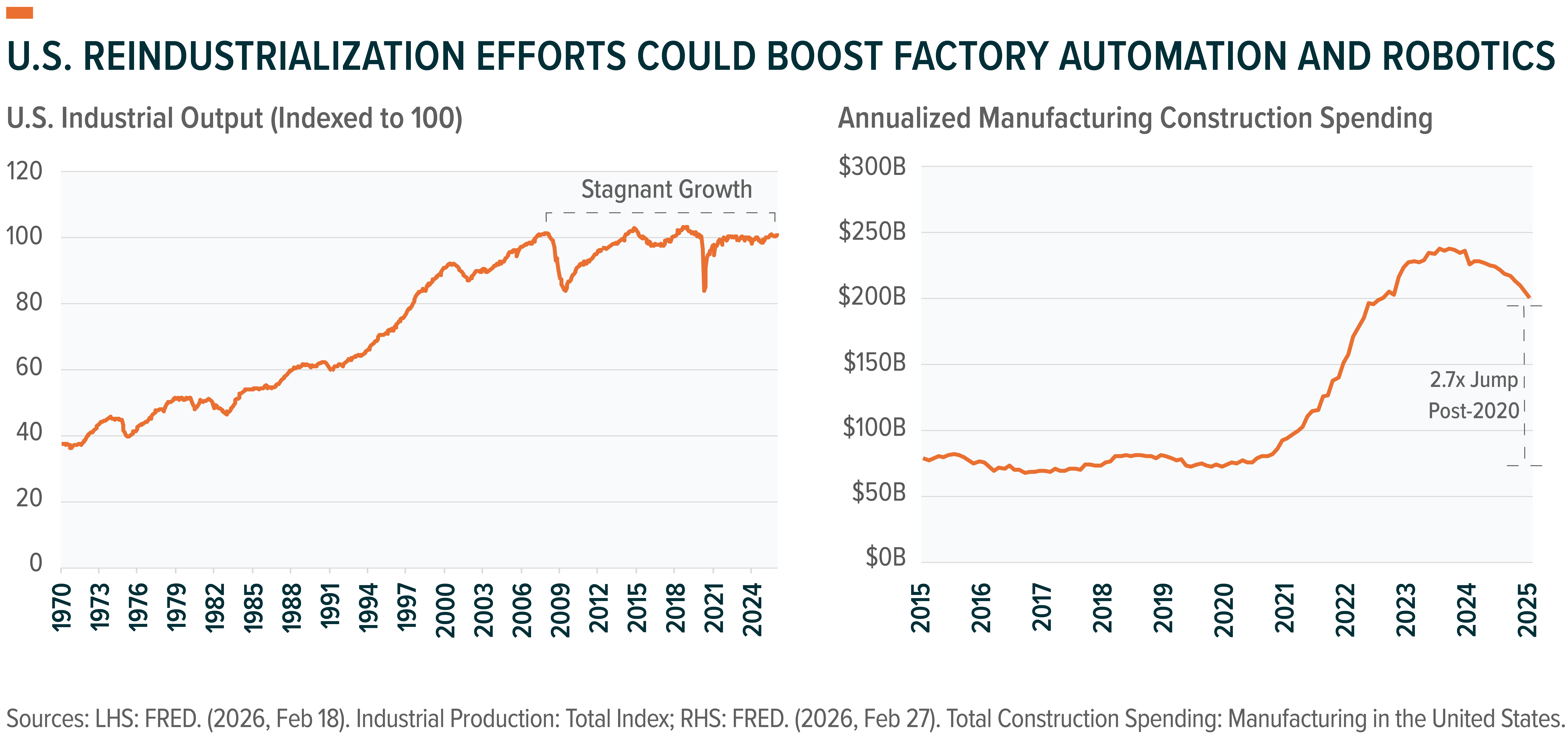

- Industrial Backdrop Is Becoming More Supportive: Governments and companies are increasingly treating manufacturing capacity as a strategic asset pulling forward demand for automation. U.S. Census data show manufacturing construction spending remained above a $200 billion annual rate in 2025, highlighting how elevated the U.S. factory build cycle remains.13 Semiconductors, pharmaceuticals, dominate new builds, which require heavy automation.14 Our analysis suggests that the pipeline of announced investments to expand U.S. manufacturing capacity since January 2025 exceeds $1.2 trillion, which extends runway for growth.15 The current administration is also reported to be working towards a national robotics policy.16

Robots Beyond Factories

As robots become cheaper, smarter, and more capable, adoption is expanding beyond factory floors into other sectors of the economy. Warehousing and logistics, where swarms of smaller robots are commonly deployed, now run on fleets of mobile robots and robotic arms. Amazon alone has deployed more than 1 million robots across its operations.17

Healthcare offers another proof point: Intuitive Surgical, a leader in this space, reported an installed base of 11,106 da Vinci systems as of the end of 2025, underscoring how robotics has become embedded in high-value clinical workflows.18 Its business model is also becoming more service-oriented rather than purely hardware-led, reflecting a broader shift toward robotics-as-a-service.

Autonomous driving represents another frontier of physical automation. Self-driving systems must perceive, predict, plan, and act in real time within dynamic environments, making them one of the most complex forms of physical automation now reaching commercial scale. These systems rely on shared data, large-scale compute, and continuous learning across fleets. The same underlying technologies are increasingly being applied to the movement of goods across factories and warehouses.

China’s Robotics Leadership Enters a New Age

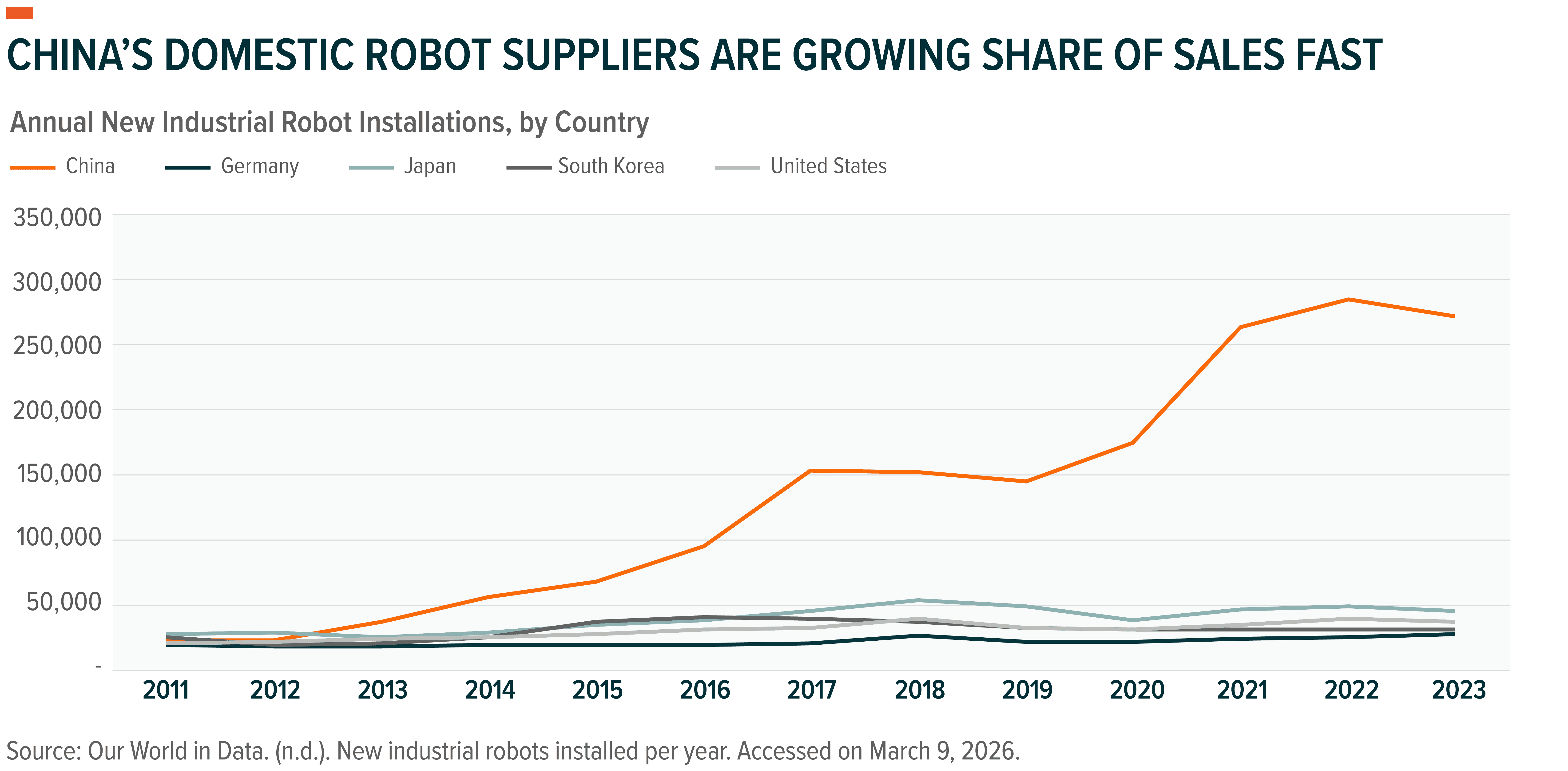

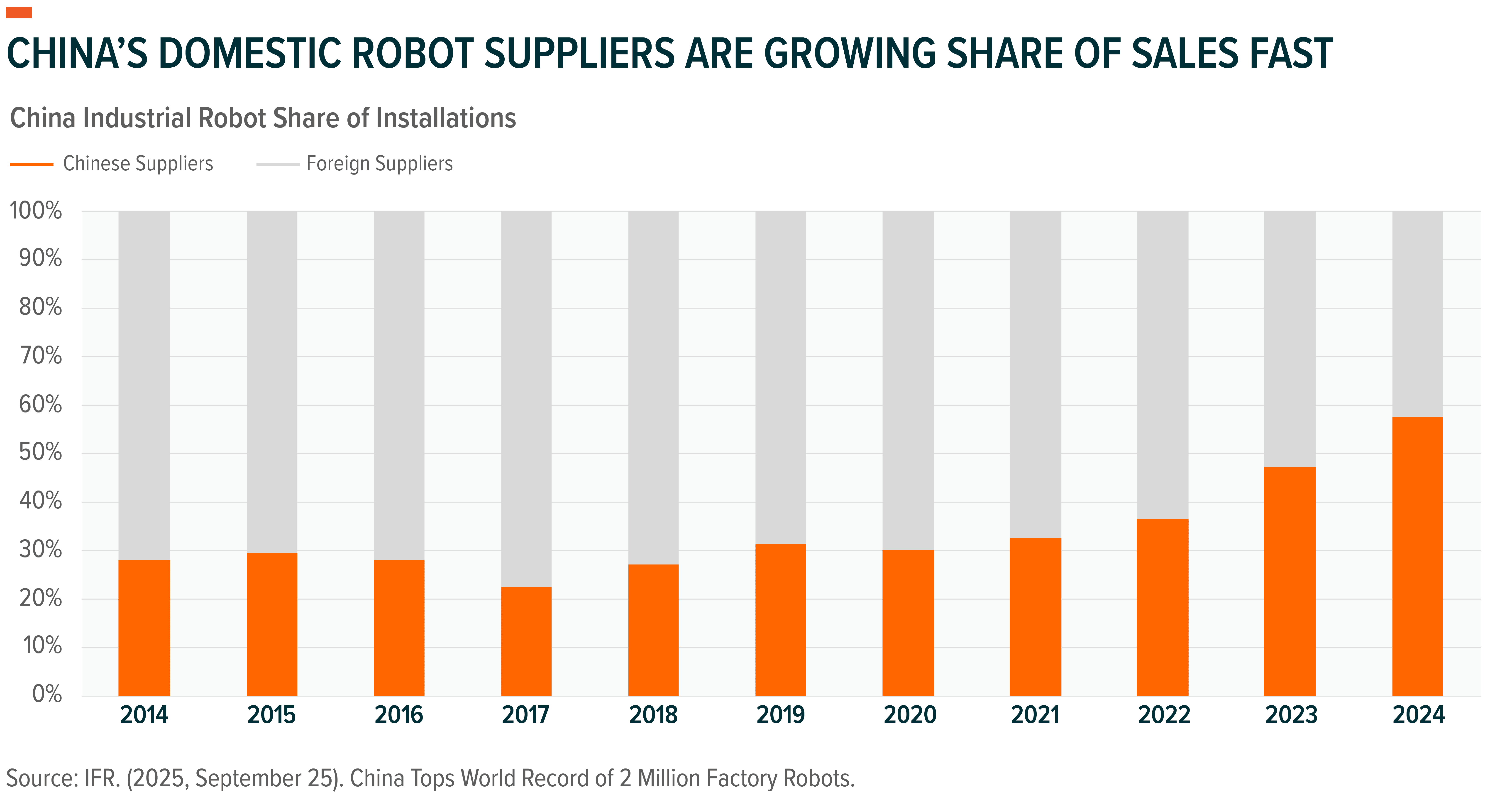

For years, China’s robotics leadership was defined by demand, as it was the world’s largest buyer of industrial robots – most of which were imported into the country. Chinese factories installed 54% of all global industrial robots sold globally in 2024 and operated an installed base of over 2 million.19 This scale is also reflected in China’s automation intensity: robot density reached 470 robots per 10,000 manufacturing employees in 2023, ranking third globally behind South Korea and Singapore, and twice the U.S.20

Now the story is broadening from consumption to domestic capability. In 2024, Chinese robot manufacturers supplied 57% of all industrial robots purchased in China, surpassing foreign suppliers for the first time and up from 47% in 2023.21 Local firms are expanding beyond legacy strongholds such as autos and electronics manufacturing into sectors like food processing, textiles, and wood products, which suggests market broadening for Chinese suppliers rather than simple replacement of legacy segments.

In our view, this gives the regional ecosystem disproportionate influence over the future of the robotics industry. Scale accelerates learning curves, deepens supplier networks, and speeds iteration. Chinese factories also become the real-world proving ground for modern automation, allowing unparalleled iterative testing. We believe the skill, data, and cost curve compression created by this ecosystem will play a defining role in global robotics commercialization in the years ahead.

Lastly, Chinese policy is a major factor in catalyzing the domestic robotics ecosystem. Regulators have long treated automation as a strategic lever to move up the value chain, reduce dependence on foreign technology, and defend manufacturing leadership as labor costs rise.22 That translates into aggressive adoption targets, incentives, and coordinated investment, that started with a focus on components (motors, sensors) and factory automation, and increasingly focuses on humanoid and service robotics.

For example, China’s 14th Five-Year Plan for the Robotics Industry, released in 2021, targeted robot revenue growth of more than 20% annually through 2025 while expanding adoption across sectors including agriculture, construction, mining, healthcare, and eldercare. The plan also promoted a shift toward system-level automation rather than standalone robots. In 2023, the “Robot+” action plan reinforced this push by targeting a doubling of manufacturing robot density by 2025 relative to 2020 levels. Meanwhile, guidance from China’s Ministry of Industry and Information Technology’s (MIIT) on humanoid robotics called for breakthroughs in perception, control, and manipulation, alongside mass production by 2025 and the development of an internationally competitive ecosystem by 2027.23

In our view, this combination of focused policy boost and rapid iteration – enabled by proximity to a domestic ecosystem spanning batteries, electric vehicle (EV) supply chains, power electronics, sensors, and AI hardware – closely resembles the conditions that drove China’s rise in EVs, suggesting robotics may be approaching a similar inflection point.

Humanoids: The Next Big Platform in Robotics

Humanoids represent a key evolution in general-purpose robotics because they’re designed to function in a world designed for people. Our surroundings – which include doors, stairs, shelves, tools, carts, and safety procedures – all assume a human-sized agent with hands. Industrial automation has historically required rebuilding the environment to fit the machine: fixed cells, guards, conveyors, and specialized tooling. Humanoids flip that dynamic. Robots capable of learnings tasks and operating safely around humans can automate work within existing infrastructure.

Improvements in processing platforms, falling AI computing costs, and expanding data availability are accelerating humanoid development. The progress is also drawing well-capitalized entrants who see commercial promise. Incumbents such as Tesla are entering laterally, bringing hardware expertise, proprietary data, and integrated ecosystem advantages. Tesla expects to begin selling its Optimus humanoid robot to the public by the end of 2027.24 Hyundai plans to begin mass production of Atlas robots developed by Boston Dynamics by 2028 and is reportedly targeting production of 30,000 units annually.25 At the same time challengers including Figure AI, Agility Robotics, Unitree, UBTECH, and Shenzhen Dobot are scaling rapidly through innovation and industry partnerships.

Our estimates indicate that the global humanoid sales could approach a million units sold by 2030 and then steeply inflect to reach a cumulative 400 million units sold by 2040, assuming the current trajectory of innovation and cost compression holds.26

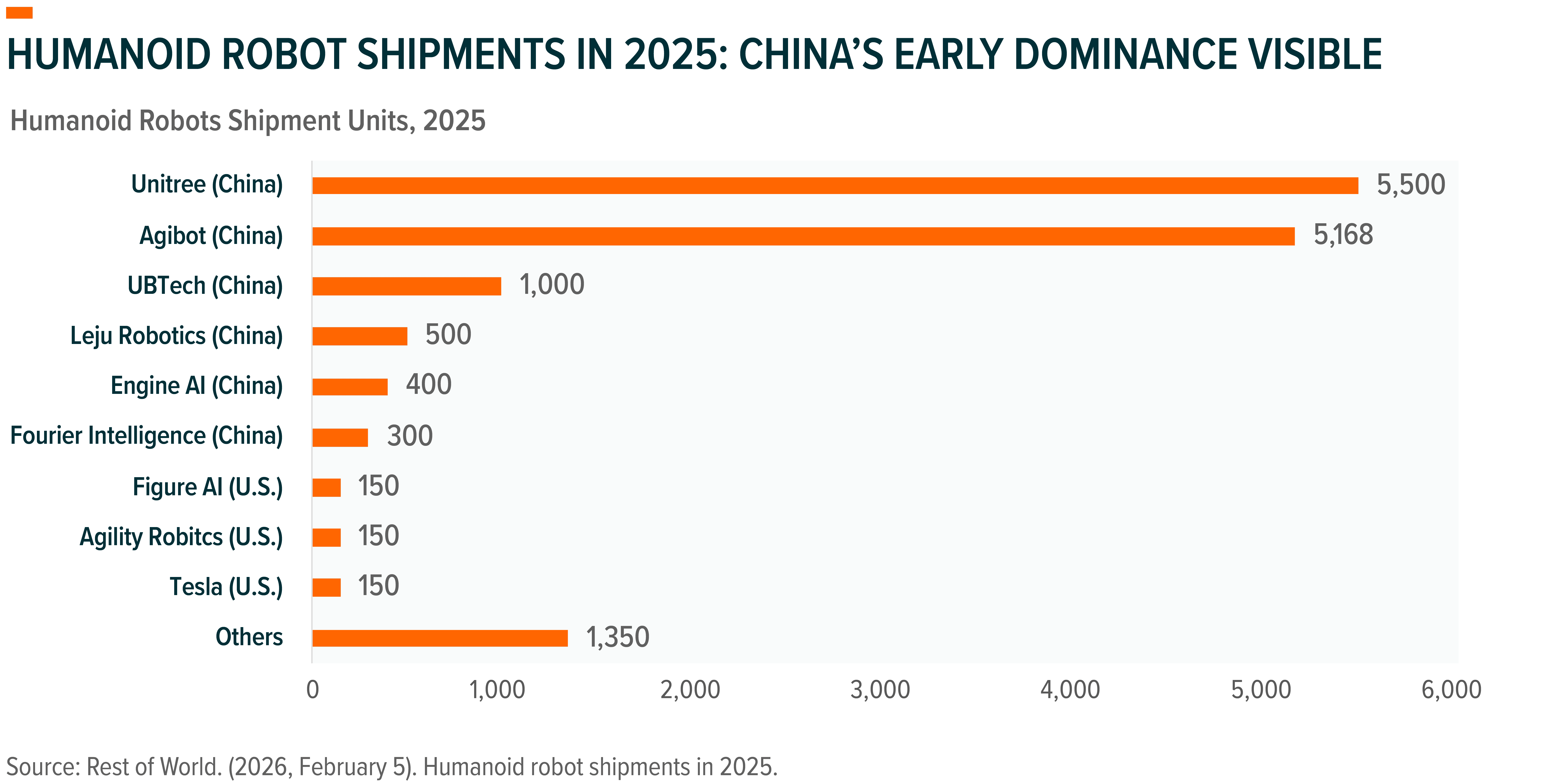

China’s role in this market also cannot be understated. Recent reporting highlights a bustling ecosystem of Chinese humanoid companies, with Unitree cited as pricing its G1 humanoid around $13,500, illustrating how aggressively Chinese firms are driving down costs.27 Our research team witnessed the ecosystem’s leadership firsthand at CES 2026 earlier this year.

BOTZ: Targeting Full Stack Innovation in the Robotics Ecosystem

The Global X Robotics & Artificial Intelligence ETF (BOTZ) is designed to provide targeted exposure to the companies advancing the global robotics and automation-linked artificial intelligence markets. The fund seeks to track the Indxx Global Robotics & Artificial Intelligence Thematic Index, which is built to capture both the breadth and depth of the theme.

- Targeted Value Chain: BOTZ is designed to capture companies across a broad span of the robotics and automation-linked artificial intelligence value chain. The fund targets companies in industrial robotics and automation, unmanned vehicles and drones, non-industrial robotics, humanoid technology, and artificial intelligence.

- Balancing Pure-Plays with Diversified-Revenue Companies: In addition to pure-players and pre-revenue companies, BOTZ also allocates to diversified-revenue companies, capped at 10% in aggregate and 2% per individual company. This structure helps preserve the portfolio’s pure-play core while broadening exposure across the ecosystem.

- Exposure to Key Markets: BOTZ’s index is comprised of robotics companies across developed markets such as the U.S. and Europe, along with China, while capping China at 10% of total index weight. This approach provides exposure to the companies advancing and commercializing robotics globally, while limiting innovation risk from emerging markets.

- Modified Market Cap Weighting: Using a modified market-cap weighting approach, BOTZ’s index allows companies to gain representation as they scale. The index caps individual pure-play and pre-revenue companies at 8%, while diversified-revenue companies are subject to a tighter 2% per company cap.

The index’s tight revenue filters and thematic construction create distinct exposure to both pure-play innovators and diversified revenue companies across the robotics ecosystem. For investors, with its tilt toward industrials, BOTZ can also help diversify away from mega-cap and technology-heavy portfolio concentration while still capturing the core tailwinds underpinning the AI opportunity.

Conclusion: We Believe The Commercial Inflection Point for Robotics Is Here

Robotics is moving to a near-term commercial inflection, supported by improving AI capabilities, falling hardware costs, and a more urgent global push to automate production and logistics. Just as importantly, the theme is no longer confined to factory floors, as adoption broadens into warehousing, healthcare, autonomous systems, and – increasingly – humanoids, expanding the addressable market for the companies building the robotics stack. For investors, BOTZ offers a targeted way to access this shift through exposure to the global leaders, enablers, and innovators driving robotics toward broader commercialization.

Related ETFs

BOTZ – Global X Robotics & Artificial Intelligence ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.