This piece is one in a series that delves further into the leading themes emerging from this year’s iteration of our flagship research project, Charting Disruption.

Robotics elevates AI from the digital realm into the operating system of the physical world. As generative AI models grow more capable and associated hardware becomes cheaper and more versatile, we’re rapidly advancing into the era of Physical AI, where networks of machines can think, see, move, and act in real time to augment human workflows.

This shift carries profound implications. Human labor productivity could be supercharged as people increasingly deploy robots for physical tasks. Entirely new use cases will emerge across sectors such as last-mile logistics, self-driving, and robotic manufacturing. Ultimately, this could culminate in Humanoid systems advancing, as general-purpose physical AI brings intelligent automation to everyday businesses and households. In our view, Robotics & Physical AI form a defining theme of the intelligence age.

Key Takeaways

- Robotics could enter a new industrial super cycle as advances in AI, sensors, and hardware fuse digital intelligence with physical capability across industries.

- Parallel cost declines and performance gains are accelerating automation’s adoption, with robots transforming manufacturing, logistics, and healthcare by boosting efficiency and addressing labor shortages.

- Humanoid and general-purpose robots are nearing commercialization, creating a multi-billion-dollar market opportunity as physical AI begins to reshape how humans and machines work together.

Manufacturing’s Automation Shift Is Now an Economic Imperative

Manufacturing has long been central to robotics adoption. Global stock of industrial robots already totals roughly 4.7 million, offering automation a healthy installed base into a core sector of the economy.1 That adoption is expected to further accelerate as new priorities such as reshoring and reindustrialization take shape in strategic industries such as semiconductors and electric vehicle (EV) components.

In 2024, new global industrial robot installations reached 542,000 units, more than doubling over the past decade, and marking the second highest annual installation count of industrial robots in history.2 Asia accounted for 74% of new deployments, compared with 16% in Europe and 9% in the Americas. Annual installations are projected to rise another 6% in 2025 and surpass 700,000 units by 2028, underscoring automation’s steady advance. 3

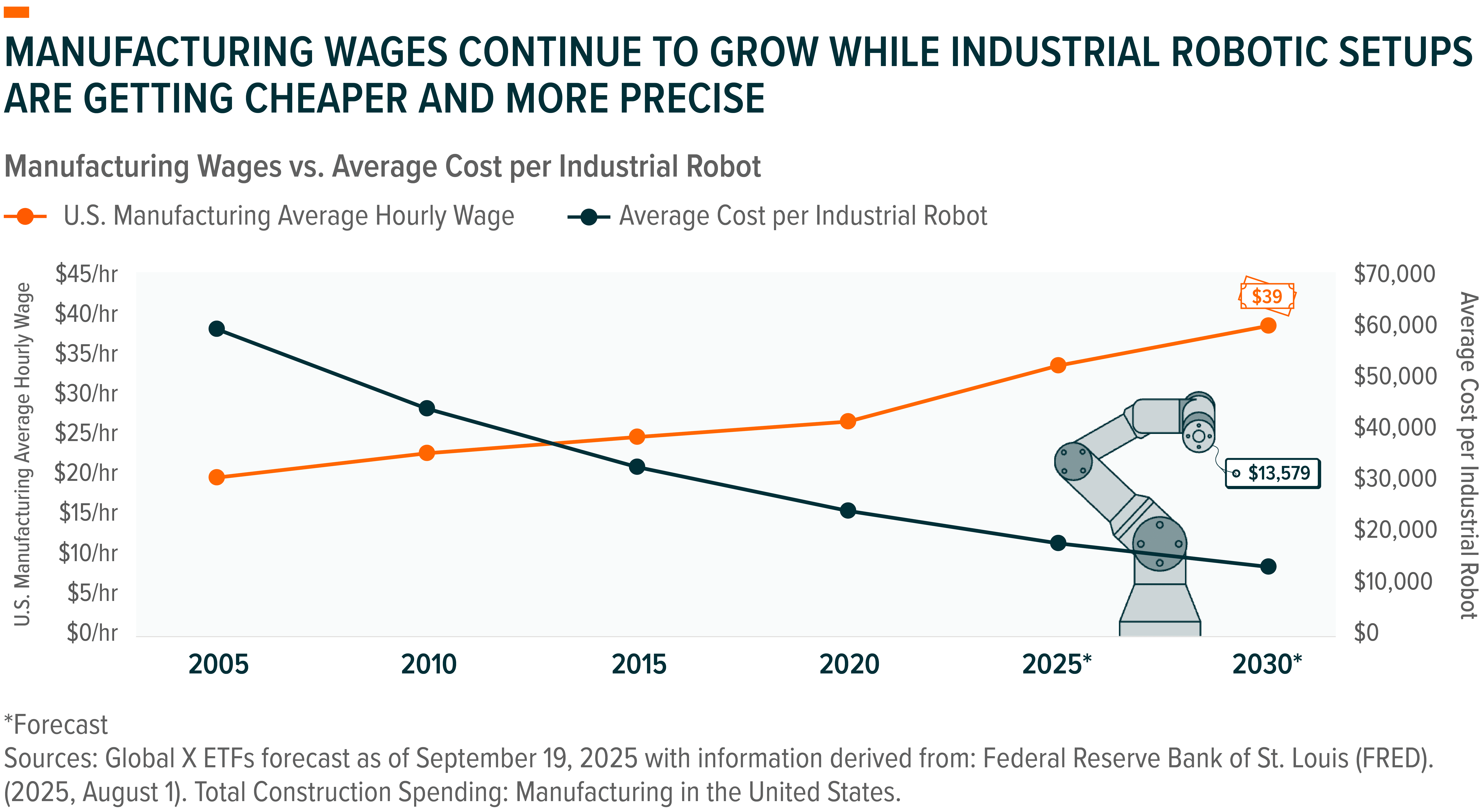

Falling automation costs and rising labor expenses further reinforce the structural global reshoring shift. Average U.S. hourly manufacturing wages reached $34 in 2025, and are expected to rise to $39 by decades end.4 Meanwhile, the average cost of an industrial robot is expected to continue to compress, while functionalities improve.5 These dynamics enable greater quantity and flexibility of robotic systems to operate in a wider range of settings, shifting the economic advantage in favor of automation.

Robots are also getting smarter and more flexible due to AI. Rather than the rigid, fixed setups of the past, software-defined robot platforms with standardized interfaces enable plug-and-play adaptation. This modularization reduces downtime, supports reconfiguration, and lowers integration risk. In effect, companies get the economics of mass customization. Continuous improvements in algorithms, semiconductor efficiency, and power systems are accelerating this shift.

Collaborative robots, or cobots, are also expanding the frontier of industrial automation. Designed to work safely alongside humans, they take on hazardous, repetitive, or precision tasks at a fraction of the cost, allowing workers to focus on higher-value activities such as design, supervision, and decision-making.

Robotics Is Advancing Rapidly Across Services

Improving intelligence is helping Robotics move rapidly beyond factory floors into the everyday economy, such as warehouses, hospitals, delivery networks, and retail spaces. These segments face chronic labor shortages, high turnover, and rising expectations for speed and precision, creating ideal conditions for automation to thrive.

In logistics, autonomous mobile robots now manage everything from pallet movement to last-mile sorting. Amazon alone operates over one million warehouse robots worldwide by using fleets like Proteus and Sparrow to transport and identify packages with minimal human input.6 Walmart, FedEx, and DHL are also integrating robotics to stabilize throughput and protect against labor volatility.

In healthcare, surgical robots are transforming the operating room by enhancing precision, reducing recovery times, and expanding access to complex procedures. In 2025, it’s estimated that roughly 50% of surgeons perform some type of general robotics surgery, up from just 9% in 2012.7 Intuitive Surgical’s da Vinci installed robot base has nearly doubled in the last five years, reaching 10,488 installed units in June 2025.8 Beyond the operating room, hospitals use autonomous systems for medication delivery, sanitation, and patient mobility support, freeing up nurses and technicians to focus on direct care.

In retail, robots increasingly monitor shelf inventory, restocking items, and cleaning aisles. In hospitality, autonomous butlers and delivery bots are increasingly common in hotels across Asia and the U.S., handling room service and concierge logistics. The food industry has begun to implement automated kitchen arms that assemble burgers, brew coffee, and mix drinks with precision and consistency. And in transportation, autonomous robotaxis and delivery pods travel city streets, building toward a future where goods and people move seamlessly through networks of intelligent machines. Since launching its commercial service in 2018, Waymo now handles over 250,000 driverless trips across five major U.S. cities.9

The Evolution of Physical AI Culminates in Humanoid Development

Humanoid robots are emerging as the next major frontier in physical automation, bridging the gap between industrial machinery and intelligent, adaptive assistants designed for human environments. Unlike traditional factory robots, which are fixed and specialized, humanoids walk, see, manipulate objects, and communicate naturally. They’re designed for the spaces people already inhabit, such as warehouses, hospitals, offices, and eventually homes, giving them enormous potential to address global labor shortages, support aging populations, and unlock new forms of productivity.

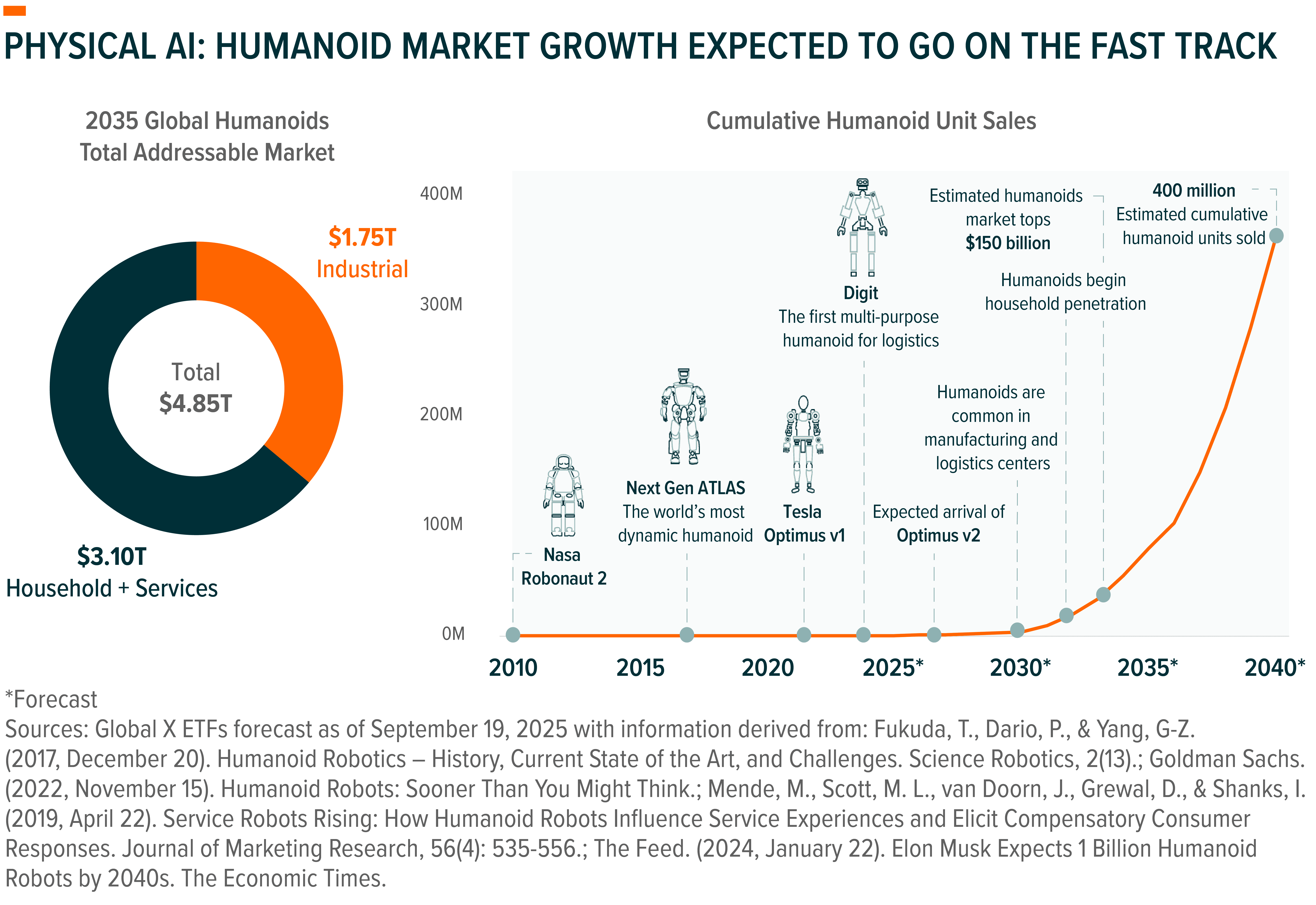

The market opportunity is vast. Humanoid adoption could touch roughly one-third of industrial labor roles and up to 15% of global households by the mid-2030s, translating to nearly $5 trillion in total economic potential.10 Pilots for early prototypes, such as Agility Robotics’ Digit and Figure’s humanoid models, are already underway in logistics and manufacturing.

By 2030, it’s estimated that global annual humanoid sales could reach 1 million, just 17 years after commercial humanoid sales began. By 2040, cumulative humanoid unit sales could potentially reach 400 million.11 Such a trajectory would closely parallel the early expansion of the automobile industry, which similarly took about 17 years to progress from initial commercialization to 1 million units sold.12

Conclusion: Physical Intelligence Starts to Make Its Mark

The rise of Robotics and Physical AI marks a structural transformation in the global economy, as intelligence extends from the digital realm into the physical world. Automation that once centered on manufacturing is now advancing across a wide range of industries, improving productivity, precision, and scalability. As humanoid and autonomous systems evolve, they will increasingly bridge the gap between industrial capability and human adaptability. Collectively, these developments position Robotics and Physical AI as a defining investment theme of the intelligence age – one with the potential to reshape productivity, open new markets, and drive long-term economic growth.

For additional insights, please view our full report, Charting Disruption: Outlook for 2026 and Beyond.