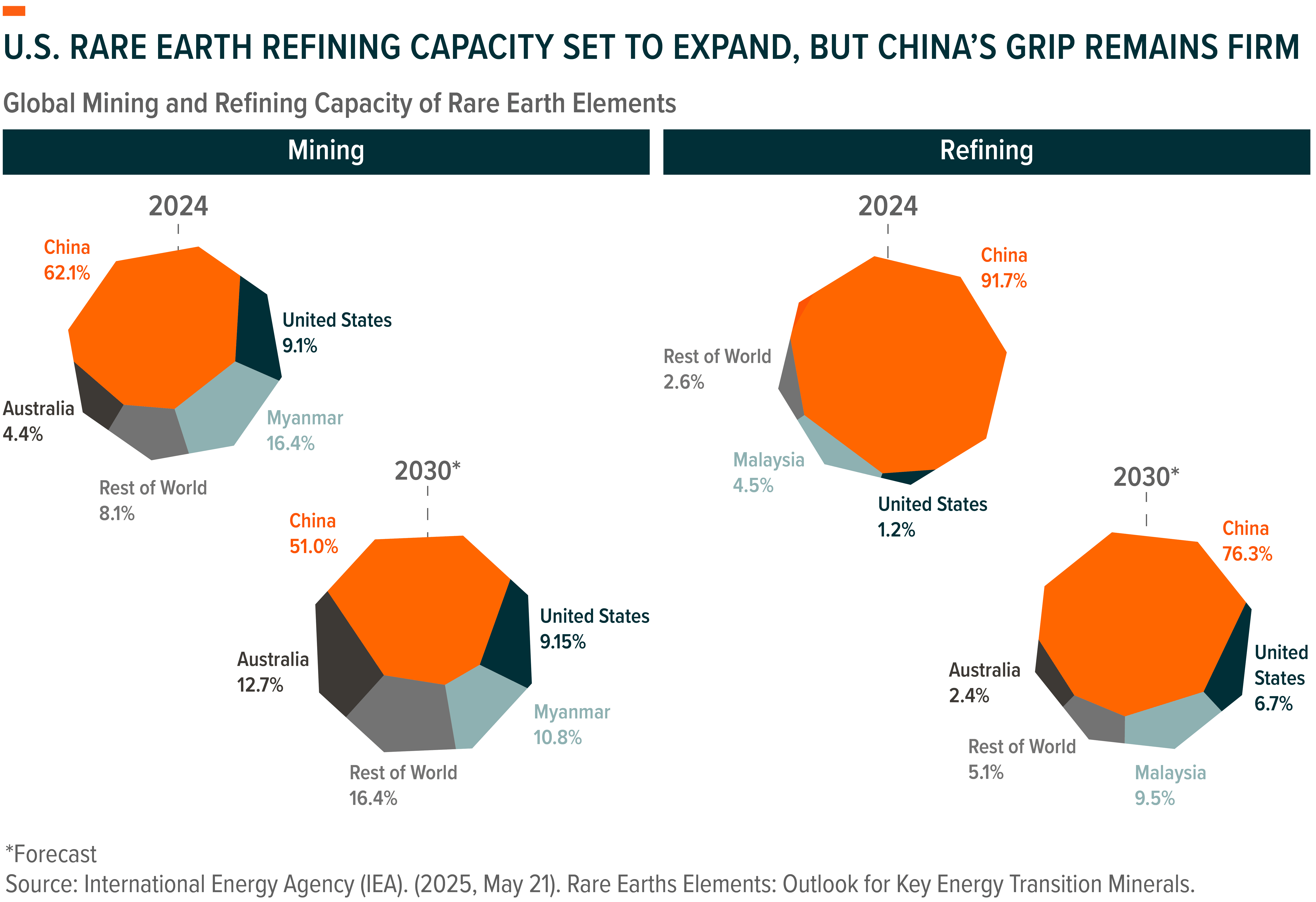

Rare earth elements (REEs) - the 17 metallic elements critical to technologies from AI chips to fighter jets - have become a new front in the global power contest. Currently, China controls nearly 90% of global refining capacity and has repeatedly tightened export restrictions, using its dominance as leverage in a deepening trade and tech rivalry with the West.1 The U.S. and its allies are responding urgently with industrial policy and capital investments to build domestic supply chains.

As geopolitical tailwinds strengthen and structural demand builds, the rare earth value chain is entering an expansion phase. Policy incentives are drawing in private capital, and projects are beginning to scale. Against this backdrop, we view this theme as one with strategic momentum, and increasingly relevant to investors looking for opportunities at the intersection of national security, industrial competitiveness, and tech innovation. The Global X Rare Earth & Critical Materials ETF (EART) seeks to offer investors access to several rare earth miners, in addition to a wide range of other critical materials suppliers.

Key Takeaways

- Rare earth elements are becoming increasingly critical to the development and deployment of next-generation technologies.

- Limited refining capacity and concentrated supply chains threaten innovation scalability. With most refining capacity located in China, the sector’s dependence on a single source has become a structural vulnerability.

- The U.S. and Europe have responded aggressively to China’s dominance with industrial policy and new investments.

Growing Strategic Vulnerability Brings Rare Earths into Focus

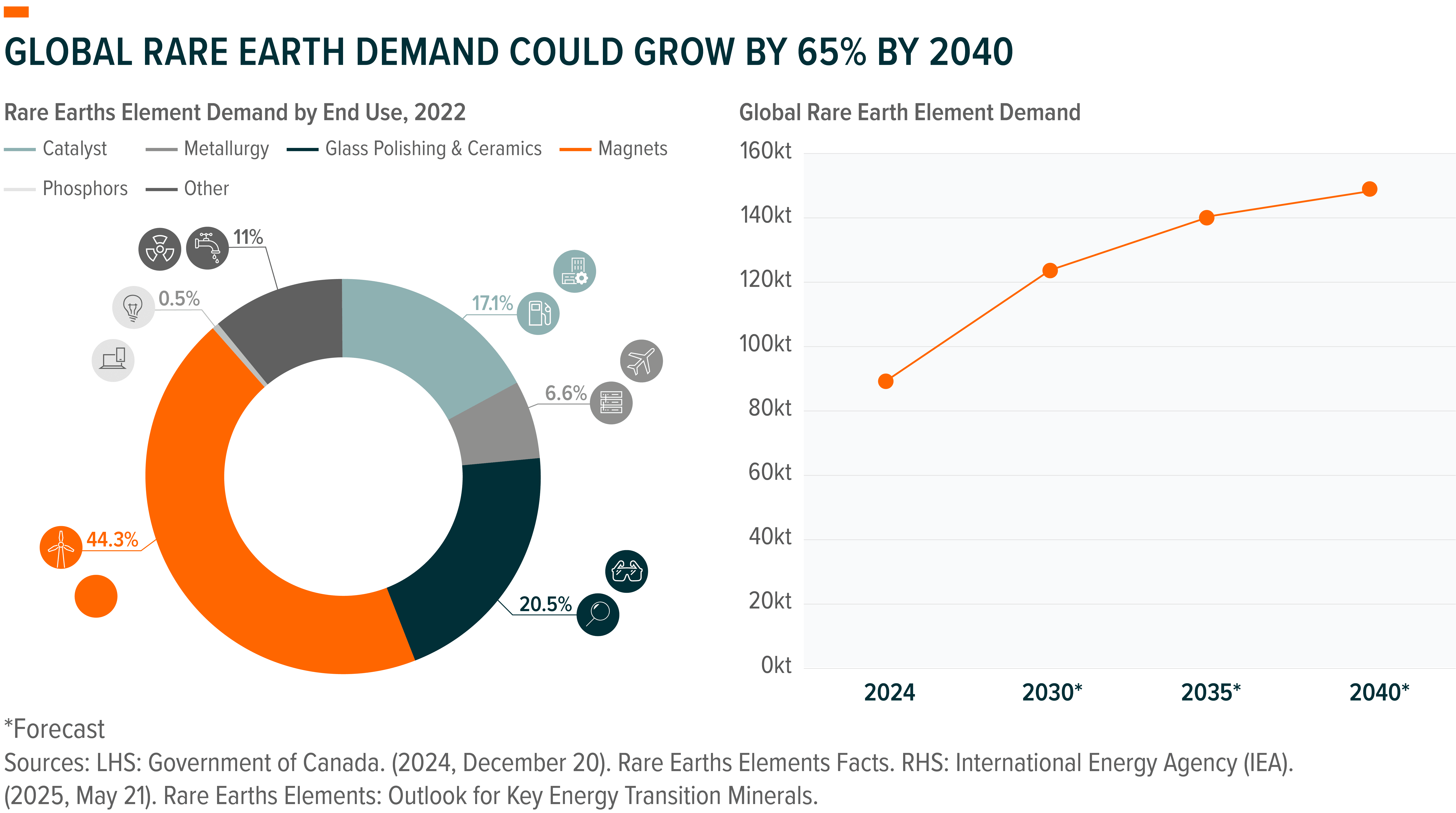

Rare Earth Elements (REEs) are a group of 17 metallic elements that are essential to smartphones, electric vehicles, wind turbines, and military equipment as they enhance magnetic, battery, and electronic efficiency. Rare earth elements demand could surprise to the upside as adoption scales across key sectors, including:

- Artificial Intelligence: AI chips require rare earth dopants such as neodymium, praseodymium, terbium, and dysprosium, which improve magnetic, optical and conductive properties in advanced semiconductors. Over the next five years, trillions in AI chips could be shipped worldwide, driving exponential growth in demand for rare-earth-enhanced chip materials.2

- Defense Technology: Each U.S. F-35 fighter contains roughly 418 kgs of rare earth materials integrated in targeting systems, stealth coatings, radar, actuators, and power amplifiers. U.S. Navy submarines require nearly 4,600 kgs of rare earth materials.3

- Battery Storage and Electric Vehicles: Grid-scale batteries and EVs rely on REEs for high-performance magnets used in inverters and motors. For example, roughly 90% of EVs today use permanent-magnet motors, with a single motor containing as much as 2 kg of neodymium and dysprosium.4 With global EV sales projected to surpass 45 million by 2030, securing reliable REE supply chains will be critical to electrification momentum.5

Moreover, the rise of unmanned systems, drones, quantum computing, and AI-enabled sensors adds new layers of demand for REEs in precision motors, actuators, and optical systems. All of this is expected to drive REE demand up by 65% by 2040, and limited access could derail U.S. leadership in advanced technologies like AI, defense, and electrification.6

Broadly speaking, the physical cost of innovation is only now coming into focus and the buildout of a wide range of these critical mineral supply chains could prove to be a generational industrial event.

China Has a Lock on Global Rare Earth Supply

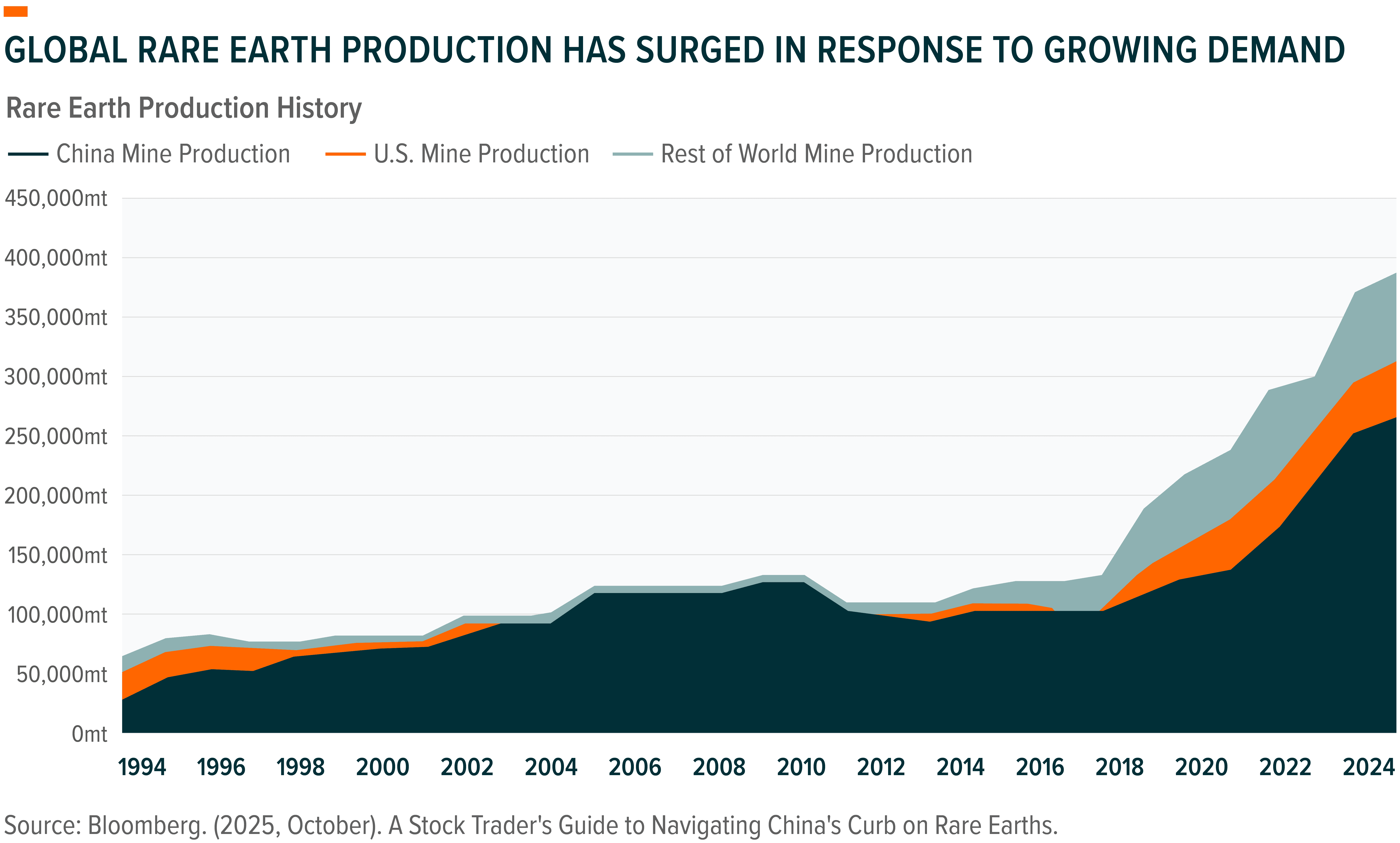

Despite their name, rare earths are relatively abundant in the Earth’s crust. What’s scarce is refining capacity. China controls over 60% of the world’s mining and nearly 90% of the world’s refining capacity for REEs, giving it decisive leverage in the global supply chain.7

And China is not shy to leverage this dominance as a geopolitical tool against the West. In April 2025, China moved to impose export controls on seven of the 17 rare earth elements, specifically samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium, in likely response to U.S. tariffs.8 Shortly thereafter, China tightened exports of additional rare earths as well as high-purity magnets.9 This was likely in response to the Trump administration’s ongoing tariff negotiations and actions.

As trade tensions escalated through the year, the Chinese government further expanded its restrictions. Most recently, in October 2025, Beijing introduced additional controls on rare earth technology exports tied to defense and semiconductors.10

China’s dominance was achieved via decades of subsidized programs boosting the domestic ecosystem. However, its lock on refining capacity - and the ability to leverage it strategically - now threatens key sectors of the Western innovation economy. Potential progress on a U.S.–China trade deal around Xi–Trump summit eases near-term pressure but is unlikely to diminish urgency of diversification.11

Government Support and Capital Aligns to Boost Domestic Production

U.S. response to this vulnerability has been urgent. Earlier this year, President Trump signed an executive order that launched an investigation into potential national security risks from reliance on imports of processed critical minerals. Before that, the Inflation Reduction Act (IRA) in 2022 earmarked over $40 billion for domestic EV and battery supply chains, including rare earths.12 As part of that, the U.S. Department of Energy has already extended grants and loan guarantees to rare earth processors and recyclers.

Actions have extended beyond policy alone. In an uncommon move, the Department of Defense took a stake in MP Materials, the only company running a rare earth mine in the U.S.13 Soon thereafter, Apple committed to buying nearly $500 million worth of recycled magnets from the company, produced in the U.S.14 Additionally, the Pentagon also committed to buying magnets from domestic producers over the next decade, bolstering demand certainty.

Private capital shows similar vigor in capitalizing on the sector’s momentum, which builds our confidence in the theme. JP Morgan reportedly announced a multi-trillion-dollar initiative to back clean-tech and materials infrastructure in the U.S., including rare-earth mining and refining.15 Miners are also responding. Australian producer Lynas is expanding refining capacity in Texas, supported by U.S. Department of Defense funding.16 MP Materials is vertically integrating from mine-to-magnet with a facility in Fort Worth.17

Efforts to diversify away from Chinese supply are coming from other major industrialized regions as well. Europe has pushed the Critical Raw Materials Act, targeting 10%+ domestic rare earth production by 2030 - a material jump from near-zero today.18

We expect support to strengthen in the coming months, potentially adding more urgency, momentum, and capital to this shift, making this a key theme for investors.

Conclusion: Disruptive Materials Form the Core of the Innovation Economy

Geopolitical tailwinds, structural demand growth, and rising strategic urgency position rare earths as a cornerstone of the technologies of tomorrow. As China continues to leverage its dominant position in rare earth supply, we expect manufacturers and governments to increasingly secure direct offtake agreements with Western miners, potentially locking in multi-year supply contracts. We believe the backdrop makes the rare earth and disruptive materials theme a strong candidate for consideration for investors looking for secular opportunities.

Related ETFs

EART – Global X Rare Earth & Critical Materials ETF

Click the fund name above to view holdings. Holdings are subject to change. Current and future holdings are subject to risk.