Access to clean water remains a critical global challenge, with over two billion people lacking safely managed drinking water.1 At the same time, water demand is increasing while freshwater supplies are being impacted by a multitude of factors, from climate change to inadequate water infrastructure. The Global Commission on the Economics of Water in 2023 estimated that global freshwater demand could outweigh supply by 40% by 2030.2

This imbalance is being further compounded by the rapid expansion of generative AI and other power-intensive computing systems, which require significant volumes of water for cooling. As data center capacity scales globally, these technologies risk adding a new and largely underappreciated source of strain to already constrained water resources and infrastructure.

Solving these challenges throughout the water supply chain will likely require substantial investment in the coming years. Below, we highlight trends that could drive demand within the clean water theme, as well as the Global X Clean Water ETF (AQWA), which seeks to target companies that could benefit from rising demand for clean water provision, water treatment, and sustainable water management technologies.

Key Takeaways

- By 2050, nearly one-third of global GDP could be exposed to high water stress due to increased water demand exceeding supply in many regions.3

- Addressing the growing water crisis will require significant investments into water conservation, purification, and transport. An estimated $6.7 trillion in water infrastructure is needed by 2030, rising to $22.6 trillion by 2050.4

- Companies throughout the clean water value chain could benefit from expected growth in water-reliant industries and an increasingly supportive policy landscape.

Increasing Water Stress Is Creating Risks for Many Regions

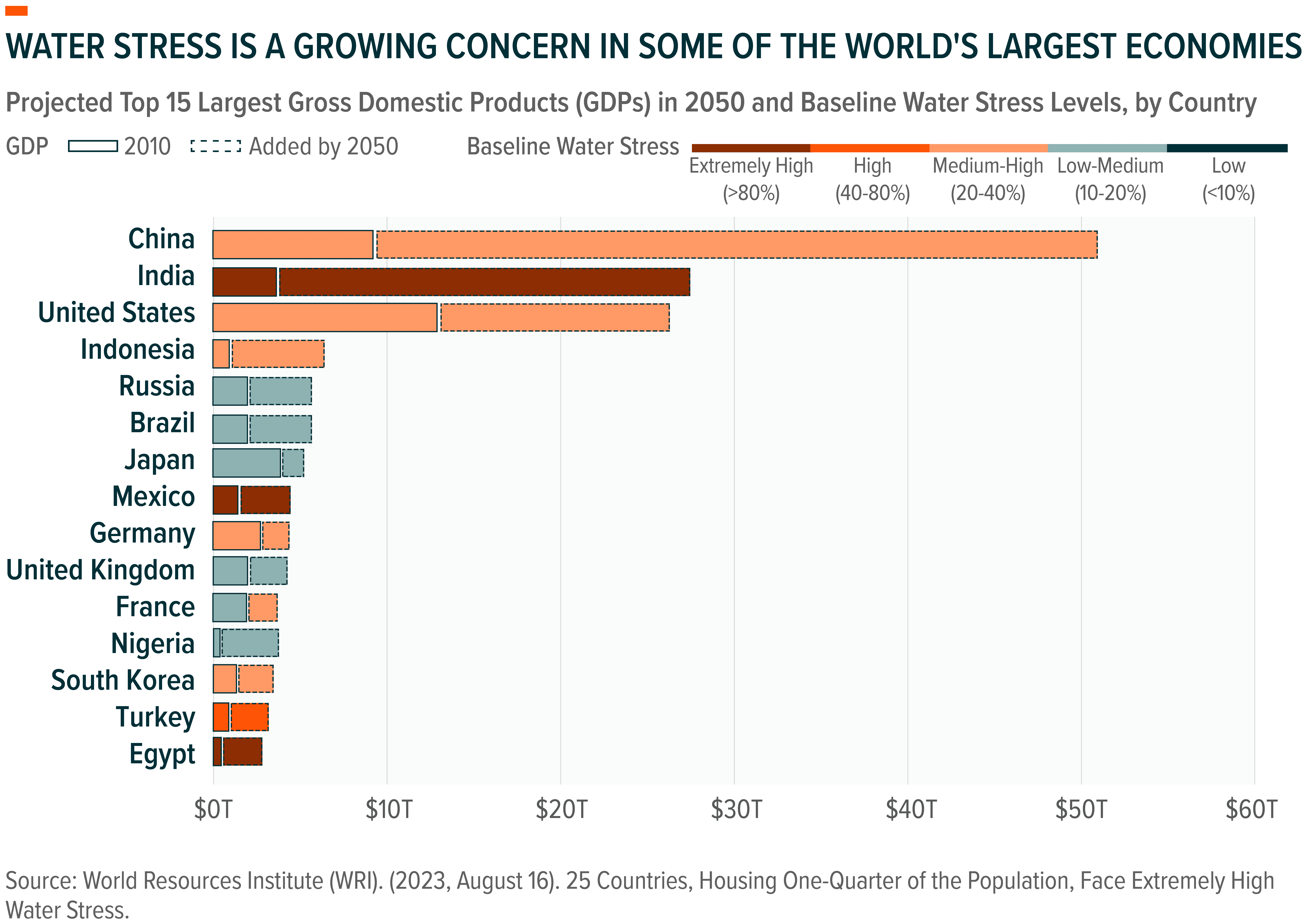

Water stress occurs when water demand is greater than the available supply within a specific area, and it is becoming an increasingly significant global challenge. In 2023, 25 countries accounting for one-fourth of the global population faced extremely high water stress, including India, the United Arab Emirates, and Chile.5 By 2050, countries housing an additional one billion people are expected to face extreme water stress. This could equate to about 31% of global gross domestic product (GDP), or about $70 trillion, becoming exposed to high water stress by the middle of the century.6

Furthermore, dozens more countries that are home to much of the global population are projected to continue experiencing at least medium-high water stress.7

Growing demand for water is one reason for the mounting water stress. Overall, global water demand is projected to increase by as much as 25% by 2050, due to growth in the global population, as well as an expansion of water-reliant industries.8

On the supply side of the equation, water availability in many regions is being affected by unsustainable water use and inadequate water infrastructure. For example, in the 2025 Report Card for America’s Infrastructure, U.S. drinking water infrastructure received a C- overall grade due to aging infrastructure systems, unreliable data, and increasing vulnerability to extreme weather.9 Shifting weather and climate patterns add further uncertainty to the long-term availability of water resources around the world.

The impacts of inadequate water supplies are already becoming apparent for many communities and industries around the world. For example, in June 2025, barges along the Rhine River could carry only 40% to 50% of their typical capacity due to low water levels from persistent drought conditions. This led to surging shipping costs and delays for industrial shipments that rely on the river.10 In 2024, several reservoirs throughout Mexico reached historic deficits due to drought conditions, resulting in unpredictable access to water for citizens and businesses alike.11,12 From 2022 to 2024, severe drought conditions in Panama led to a frequent and severe operational disruptions at the Panama Canal.13

The agriculture, food and beverage, power, and mining industries are some of the other water-intensive industries that could face rising operational risks and impacts from water stress. Around 70% of the world’s freshwater consumption is used for agriculture, so droughts can have significant impacts.14 In 2024, within the United States alone, major weather and fire events resulted in $20.3 billion in total losses to crops and rangeland.15 In the mining sector, 50% of lithium mine production and 52% of copper mine production are located in areas marked as high-risk for water stress.16

AI Is Causing a Boom in Water-Hungry Data Centers

The advancement of AI is expected to increase water consumption from data center operations, creating another complex challenge for both hyperscalers and water utilities. Data centers can require significant amounts of water to cool their processing chips. Large data centers are estimated to use up to 5 million gallons of water per day, which is roughly equivalent to the water use of a town of up to 50,000 people.17 They can also lead to higher water use for power generation, depending on their location. By 2028, global water consumption from cooling and power for AI data centers could total 1.068 trillion liters of water annually, which would be an 11x increase from 2024 estimates.18

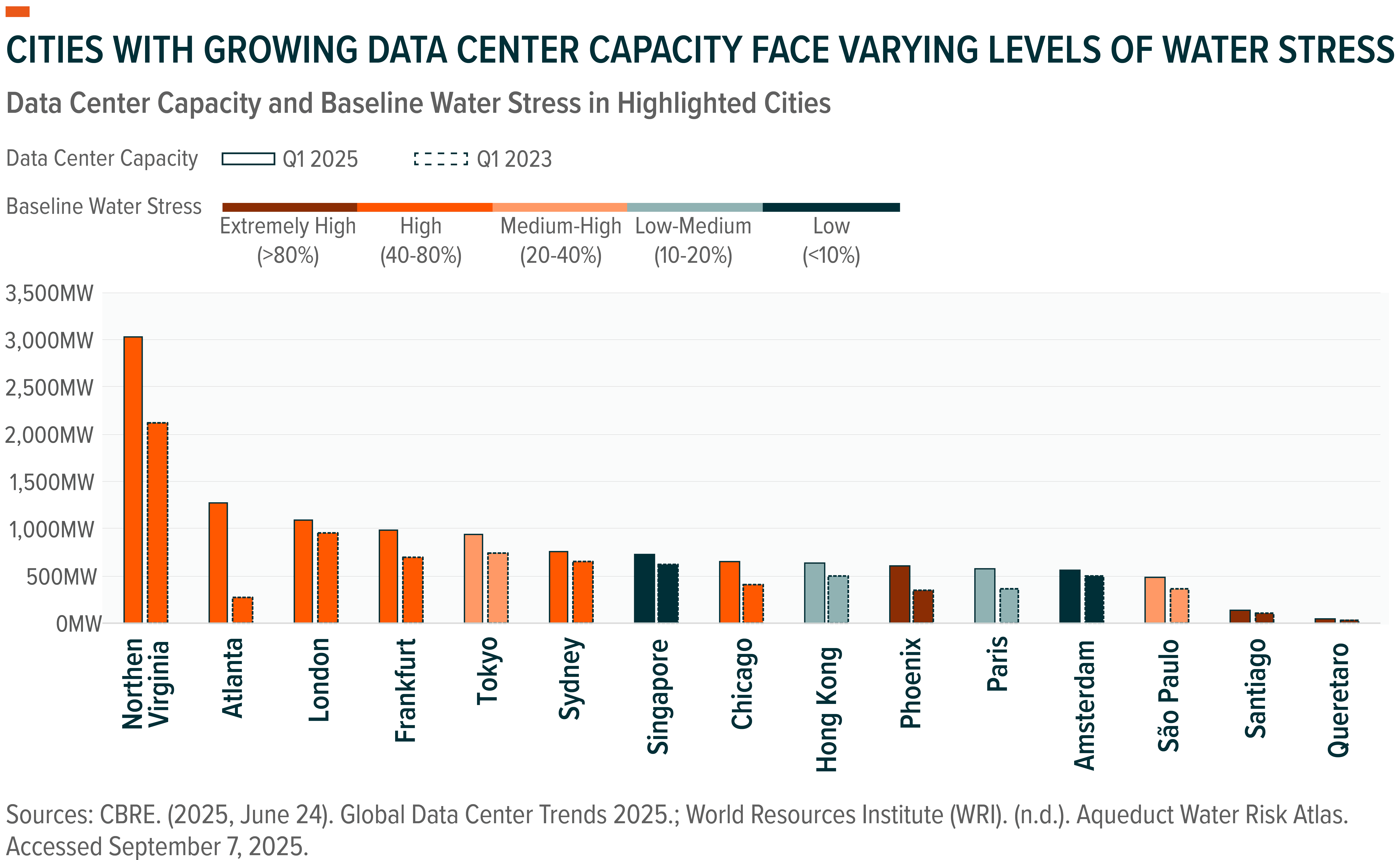

Much of the AI-fueled growth in data centers is taking place in areas already experiencing water-related risks. In the United States, the world’s largest data center market, nearly 66% of data centers built or in development are located in areas with high levels of water stress.19 Other key data center markets such as London and Sydney also face high baseline water stress.20

Hyperscalers are working with utilities, cities, and water technology providers to help mitigate water-related risks. In September 2025, Xylem partnered with Amazon and two municipalities in Mexico – Monterrey and Mexico City – to deploy technologies that can help reduce water losses and create a more water-resilient future for the two cities.21 Xylem CEO Matthew Pine noted that “this partnership is a model for how hyperscalers and communities can collaborate to ensure water security for both businesses and residents.”22 Also in 2025, Google completed a water sustainability project in partnership with the city of The Dalles, Oregon, to improve water quality and resilience. Google has been operating data centers in the city since 2006 and has plans to upgrade and expand its facilities in the area.23 In January 2026, Microsoft announced its Community-First AI Infrastructure Plan, which includes steps the company can take to reduce water use from data centers.24

Clean Water Supply Chain Stands to Benefit from Converging Tailwinds

In our view, environmental and industrial tailwinds, as well as supportive policies, could lead to new growth opportunities for companies throughout the clean water value chain. This includes manufacturers of water control, storm resilience, and advanced water products such as Mueller Water Products, Badger Meter, Core & Main, Advanced Drainage Systems, and Xylem, as well as utilities such as American Water in the United States and United Utilities in England. Product manufacturers and service providers that can yield more sustainable water use could benefit from an expanding regulatory landscape in Europe and elsewhere. Furthermore, desalination companies could also benefit should more governments and companies turn towards the technology in water-scarce locations.

The positive sentiment has been shared by management teams from several companies. For example, during Xylem’s Q3 2025 earnings call, CEO Matthew Pine stated, “alongside data center buildouts, water demand is growing across key verticals like power generation, chip fabrication, and mining for essential minerals.”25 On Ferguson Enterprises Inc.’s Q1 2026 earnings call, management stated that it continues to see the pipeline for large capital projects, such as data centers, continue to grow, and that it remains bullish on the segment being a continued growth area.26

Mueller Water Products’ September 2025 presentation highlights several challenges facing U.S. utilities that create investment needs, such as aging infrastructure assets, water scarcity, and climate change. The presentation also notes $55 billion in water-related funding from the Infrastructure Investment and Jobs Act, which could lead to new projects for companies throughout the U.S. clean water value chain.27

AQWA Seeks to Capitalize on Rising Water Demands

The Global X Clean Water ETF (AQWA) seeks to invest in companies advancing the provision of clean water through industrial water treatment, storage and distribution infrastructure, as well as purification and efficiency strategies, among other activities. Key fund highlights include:

- Clean Water Sub-Segments: The index that AQWA tracks include companies involved in four sub-themes: 1) Industrial water treatment, recycling, purification and conservation, 2)Water storage, transportation, metering, and distribution infrastructure, 3) Production of household and commercial water purifier and heating products, and 4) Provision of consulting services identifying and implementing water efficiency strategies at the corporate and municipal levels. These sub-themes deliver a combination of companies across the clean water value chain.

- High Thematic Purity: Companies must derive at least 50% of their revenues from one or more of the four sub-segments. In addition, companies must be compliant with the UN Global Compact principles for inclusion. These requirements help ensure that the fund targets companies primarily focused on the provision of clean water.

- Unconstrained Approach: AQWA seeks to capture clean water trends by taking a global approach, as well as investing in companies within the index regardless of sector or industry classification.

In our view, this thematically targeted, geo-agnostic, and high thematic purity focus positions AQWA well to capture rising investment into clean water infrastructure and technologies around the world.

Conclusion: Looming Supply/Demand Imbalance Sparks Action and Creates Opportunities

Many communities and water-intensive industries could see new disruptions to water supplies in the future. Fortunately, there are products, technologies, and services that can help governments and companies begin to mitigate risks associated with water quality and availability. A growing realization of the challenges the world faces regarding clean water is spurring government action and private-sector innovation, creating potential investment opportunities. As clean water becomes increasingly in focus, the equipment producers, utilities, and service providers at the forefront of these solutions stand to potentially benefit.

Related ETFs

AQWA – Global X Clean Water ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.