Michelle Cluver

Michelle Cluver David Beniaminov

David BeniaminovThe pace of Federal Reserve (Fed) balance sheet tapering, that started in November, accelerated in December, bringing forward the timing of the first expected interest rate increase to March 2022 from June 2022. As discussed in our 2022 outlook, we believe that 2022 will be the year of the Fed, with updated guidance and sentiments from the Fed being likely to dominate sentiment in the equities and fixed income markets.

Continuing our focus on the Fed, this month we looked at risk adjusted sector performance in the S&P 500 and analyzed which factors contributed to risk premiums for sector performance during the taper of 2013-2014 and what we can learn for the current period of reducing liquidity.

Key Takeaways

- Liquidity, Momentum, and Size contributed the most to positive performance in 2014.

- The sectors that currently display the highest level of these factors are Consumer Staples, Communication Services, and Real Estate.

- Finally, we discuss differences between economic environments and how those differences could impact the data we analyzed from 2014.

Taper, Hold the Tantrum

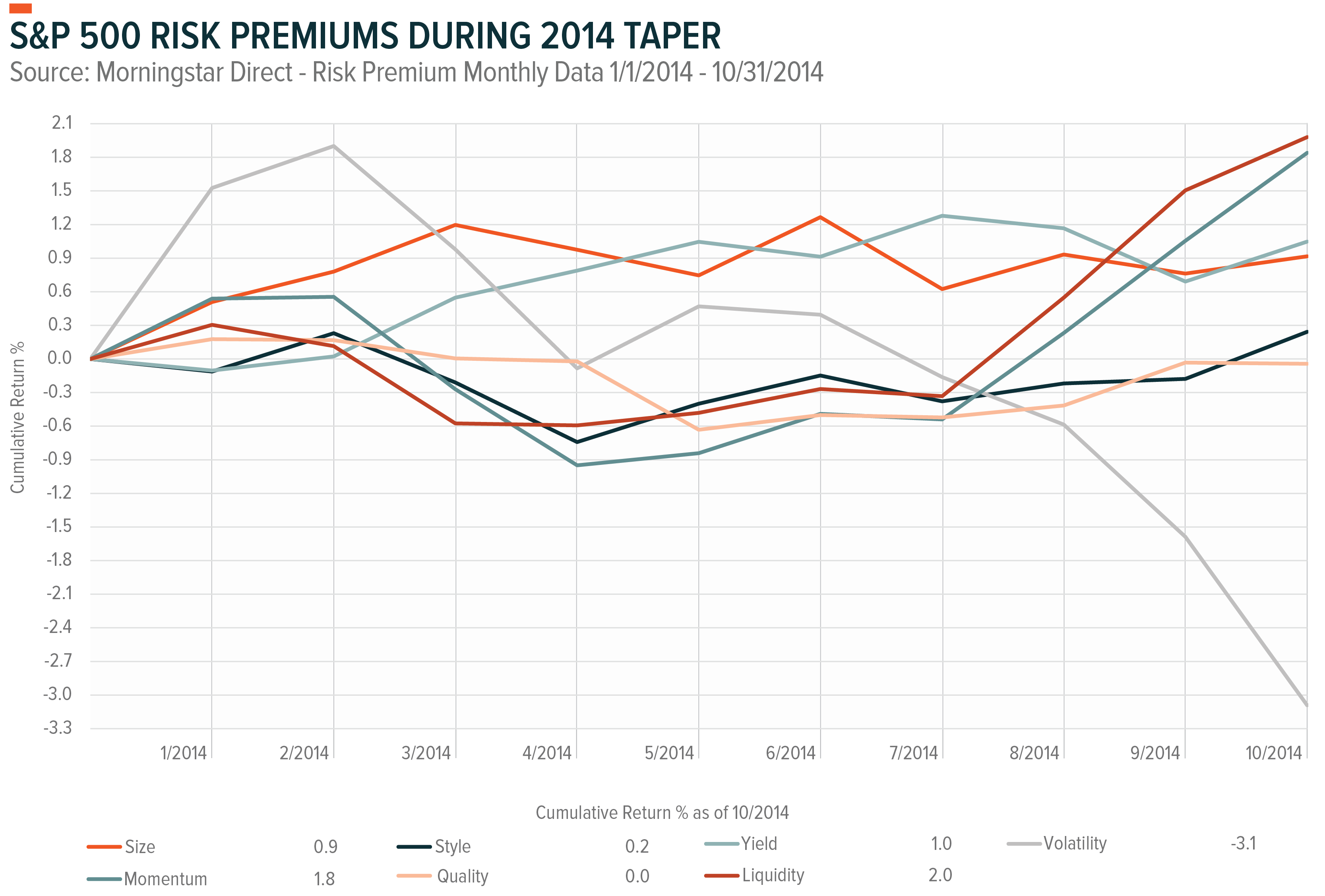

So, what does this mean for equity markets? Not long ago, in 2013, The Fed began a taper by removing liquidity provided to the market after the recession of 2008-2009. The taper began mid-December 2013 and lasted until end of October 2014. Historically similar events tend to rhyme, the economic landscape was quite different in 2013 and 2014 yet with a few similarities. Then, the Federal Funds rate was in the 0.00%-0.25% range, the price of oil was hovering around $100/barrel – not far from WTI Crude’s 2021 high of $84.59, and discouraged workers were leaving the labor market1. The differences are also quite stark: there was no pandemic; inflation was well below the Fed’s 2% target, not strongly above it (2021 Consumer Price Index was up 4.6%2); and valuations were stratified across the sectors. Because sectors and the underlying companies that drive them evolve over time, we do not believe it would be appropriate to compare sector performance from past to present. Instead, we analyzed the factors that contributed to the risk premiums within each sector during the taper of 2014, seeing which factors attributed positively, neutrally, and negatively. Then, we analyzed how those factors’ risk premiums are distributed across the current period sectors, reviewed structural differences between then and now, and considered how this could help positioning in today’s fluid environment. While the past can provide useful information, bear in mind that past performance is not a guarantee of future results.

The factors that encompass a company’s risk premium are based on the Fama-French model: Style, and Size, with Liquidity, Volatility and Momentum included in this analysis.

- Style – A company either displays more value or growth tendencies

- Size – A company’s market capitalization (higher size factor means smaller market capitalization)

- Liquidity – Considers how easily shares are traded and bid-ask spreads

- Volatility- Considers swiftness and range of price changes

- Momentum – Factors in current trends in performance

All these factors create a risk premium for each sector that is added to the 10-Year Treasury Yield and drives forecasted valuations.

First, looking at the Risk/Reward chart based on return and standard deviation relative to the S&P 500 index during the time frame of the 2014 taper we see how each sector fared on a risk-reward basis:

- Real Estate provided above average return with below average risk.

- Health Care, Utilities, and Information Technology sectors provided an above average return for an above average level of risk.

- Consumer Staples provided a below average return for a below average level of risk.

- Financials, Industrials, Materials, Communication Services, Consumer Discretionary and Energy sectors provided below average returns for above average levels of risk.

One goal when choosing an investment is to avoid taking on undue risk, which would have been done in 2014 by avoiding sectors in the bottom right quadrant where investors received a below average return with an above average level of risk. Although these sectors underperformed the broad S&P 500 Index during the 2014 taper doesn’t mean they will do so again this time around.

Factor Focus

At the same time, the risk premium factors that contributed positively were Liquidity (2.0%) and Momentum (1.8%) and negatively was Volatility (-3.1%). What this means is that more liquid companies (liquidity), and short-term sentiment (momentum) had positive contributions to performance and more volatile companies (volatility) had negative contributions to returns. Style skewed slightly towards growth and size premiums rose towards small caps. This data echoes what we mentioned in our Outlook 2022 piece where we said investors will likely put a greater focus on fundamentals next year.

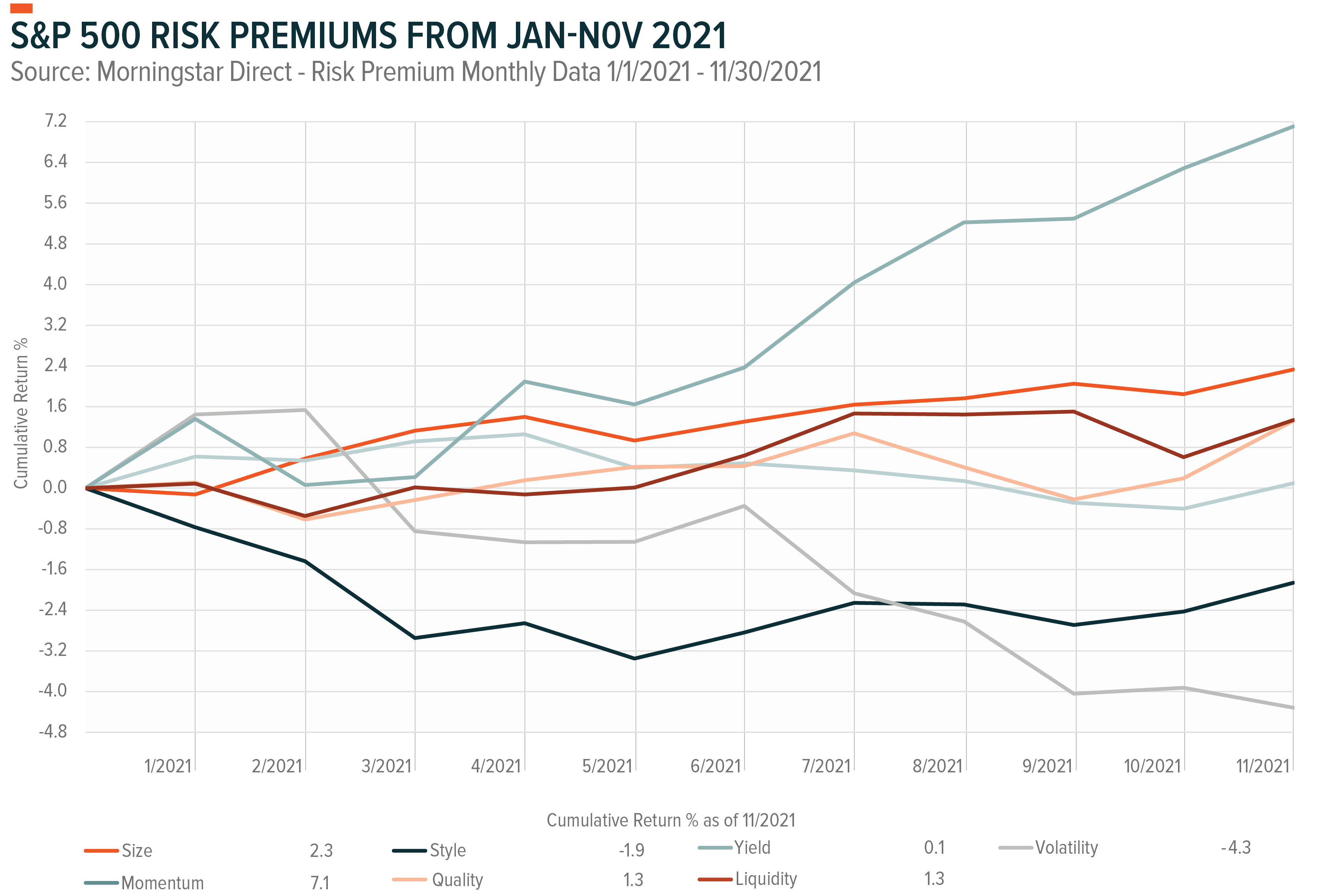

Because markets and companies grow and evolve, the allocation of factor risk premiums change over time across sectors. Looking at the risk factors that impacted returns the most, in 2014 there was Liquidity and Momentum on the positive side and Volatility on the negative side. For the most recent period in 2021, Momentum and Size contributed the most to positive returns and Volatility to negative returns. For the analysis we considered a 1 year period, 3 year period, and a combined data set. The last year provides a reasonable reflection of expectations for higher interest rates while the last three years provide greater historic context. The charts below, in order, reflect 1 year sector factor exposures, 3-year sector factor exposures, and a combination of the two. For the combination of the two, we multiplied the values of the 1-year data by two-thirds, then we multiplied the values of the 3-year data by one-third and added the two values together. This puts a heavier weight on the most recent lookback period while the 3-year is included to normalize the 1-year data.

Looking at the data strictly for a one year look back period, for liquidity – Consumer Staples, Communication Services, and Financials scored highest. For momentum – Utilities, Consumer Staples, Industrials and Health Care scored highest. Since the style risk premium referenced in the ‘S&P 500 Risk Premiums During 2014 Taper’ skewed positive that meant growth just slightly outperformed value, so we look at which sectors have the lowest style factor (meaning more growth tendencies) – Communication Services, Technology, and Consumer Discretionary.

On an aggregate basis the Consumer Staples, Utilities, and Communication Services were the highest scorers across the analyzed metrics. Finally, for the growth over value component, Communications Services scored higher than the other sectors. This data also ties in with our Outlook 2022 piece as we discussed the importance of having a balance of both growth-oriented and value-oriented companies. From the data, the liquidity factor was the biggest contributor to return, which was prevalent in both value and growth focused names.

When combining both time frames of data and weighing the 3-year historical at 1/3 and 1-year at 2/3 the results are below:

Highlighted cells are where we see notable differences between the two time periods of data on their own and when combined.

- As expected, we didn’t see any material changes in Style or Size.

- We noted a rise in momentum for Communication Services and drops for Consumer Discretionary and Information Technology.

- Volatility dropped the most for Information Technology and Health Care and rose the most for Financials. Although these were the standouts, almost every other sector also experienced change in volatility. This is likely due to the impact of the “covid era”, some sectors were positively impacted by COVID-19, while others benefitted from reopening plays. As surges and new variants arise, we expect leadership shifts.

- Liquidity, which accounted for the highest contribution to return from risk premium during the previous taper, rose strongly for Communication Services, Energy, and Industrials and dropped for Information Technology.

All in all, given the adjustment and based on the factor data from the previous taper Consumer Staples, Communication Services and Real Estate exhibit the highest levels of the liquidity factor. Utilities, Consumer Staples, and Industrials exhibit highest levels of the momentum factor. Communication Services, Information Technology, and Consumer Discretionary display highest levels of the size factor. Finally, Utilities, Real Estate, and Consumer Discretionary show highest levels of earnings and debt quality. When using the factor data from the previous taper and relating it to the current environment Consumer Staples, Communication Services, and Real Estate all seem to benefit the most.

What’s Different Now?

No period is the same so this data must be contextualized given the current economic environment. For example, the economy of 2014 wasn’t grappling with a supply chain crunch impacting profit margins of sectors like Consumer Staples, Consumer Discretionary, and Materials which is expected to persist through at least mid-year.3 Or the extraordinary inflation the current U.S. economy is grappling with which has elevated prices for both producers and consumers across all sectors. Of course, another COVID-19 strain surge is always possible that would dampen economic growth and cause investors to rotate out of certain sectors into others, or worse, into cash.

Another consideration is composition. From a structural perspective the Communication Services sector prior to September 2018 was the Telecommunications Sector which had a stronger focus on value. Given this and taking into consideration the current environment where some of the larger growth focused Communication Services sector names are more immune to supply chain issues, we would expect this sector to provide different risk adjusted returns during today’s taper.

Also, the high inflation environment we are currently in is plainly different from the inflation levels seen in the 2014 taper. This directly affects the forward-looking expected growth of the Financials sector. Because The Fed is readying itself to begin raising rates next year and because companies in the Financials sector benefit from rising rates by borrowing short term and lending long term this sector would also be expected to provide a different risk adjusted return during the current taper.

This brings to the final point that diversification across factors and sectors is increasingly important. Investors will likely place a higher focus on fundamentals as the Fed takes the necessary steps to complete its taper and begin raising rates to combat inflation. We believe investors should also have a balance between value and growth names which would provide them with the potential to weather stylistic pullbacks. For our current views please reference the sector table below.