Global X Research Team

Global X Research TeamOn November 25th, the Global X Guru suite of ETFs, which track the equity investments of major hedge funds, underwent their quarterly rebalances. This suite includes the Global X Guru Index ETF (GURU), the Global X Guru Activist Index ETF (ACTX), and the Global X Guru International Index ETF (GURI). The November 2016 GURU Report can be found here.

Below is a summary of this report as well as additional information on the performance and trends within the US hedge fund industry.

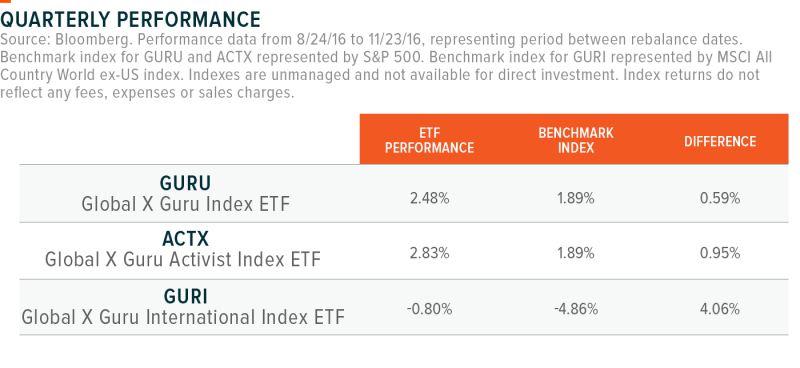

- Between the most recent quarterly rebalances (August 24th to November 23rd), all three funds, GURU, ACTX, & GURI, outperformed their benchmarks by an average of 187 bps

- Low quarterly turnover numbers across the Global X funds indicate perhaps stronger conviction among hedge funds in their major positions, with an average of just 16% turnover in GURU, ACTX, & GURI over the last two rebalances

Quarterly Performance

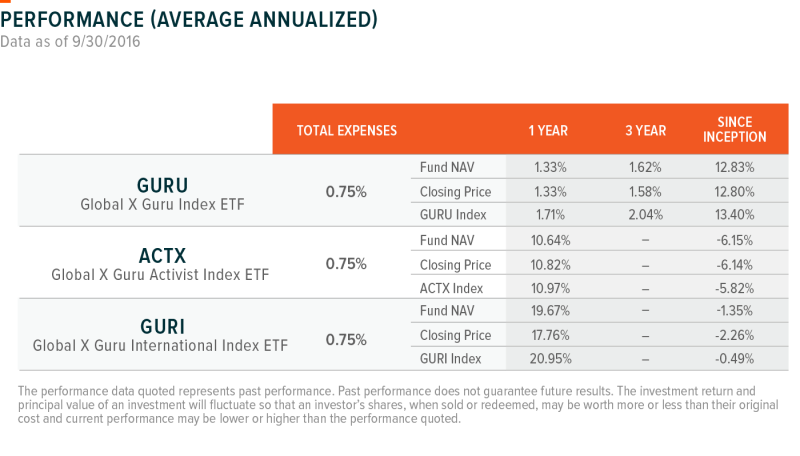

Performance data current to the most recent month- and quarter-end can be found at the following links: GURU, GURI, ACTX.

High conviction hedge fund picks in the health care sector, particularly in biotech, had been battered over a heightened likelihood of increased regulatory controls on drug prices. Many hedge funds remained confident that the market was mispricing these stocks, and held steady on their biotech holdings. This resolve was ultimately rewarded as GURU’s health care stocks have rallied 18% since GURU’s May rebalance, while the S&P 500’s health care sector has been down -1.4% during this period.1

Among activist hedge funds, we observed overweights in the Energy and Materials sectors as activists identified these companies as ripe for disruption. These bets have paid off handily with ACTX’s Energy and Materials picks up 22% and 17%, respectively, since ACTX’s May rebalance, compared to the S&P 500’s Energy and Materials sectors up only 8% and 5%, respectively.1

On the international side, markets experienced greater ranges of performance dispersion as major Western European markets sold off while commodity exposed Developed and Emerging markets led the way. GURI’s overweight positions to Canada and Brazil, nations with higher than average commodity exposure, proved beneficial, as these positions generated nearly 80% of the fund’s outperformance.1 A stronger global macro backdrop, improving commodities outlook, and constructive monetary policy drove returns in these markets after a prolonged slump.

Looking Forward

While the industry has faced challenges ranging from fee pressures to periods of underperformance, hedge funds still remain uniquely positioned to potentially generate alpha due to their deep talent pool and ability to make high conviction investments. Direct investments into hedge funds, however, often requires paying high fees and entering into lock-up periods that reduce liquidity. We believe that a more liquid, tax-efficient, and cost-effective vehicle like an ETF can be preferable exposure to high conviction hedge fund investments.