Introducing the Global X Emerging Markets Great Consumer (EMC) and Emerging Markets (EMM) ETFs

May 15, 2023

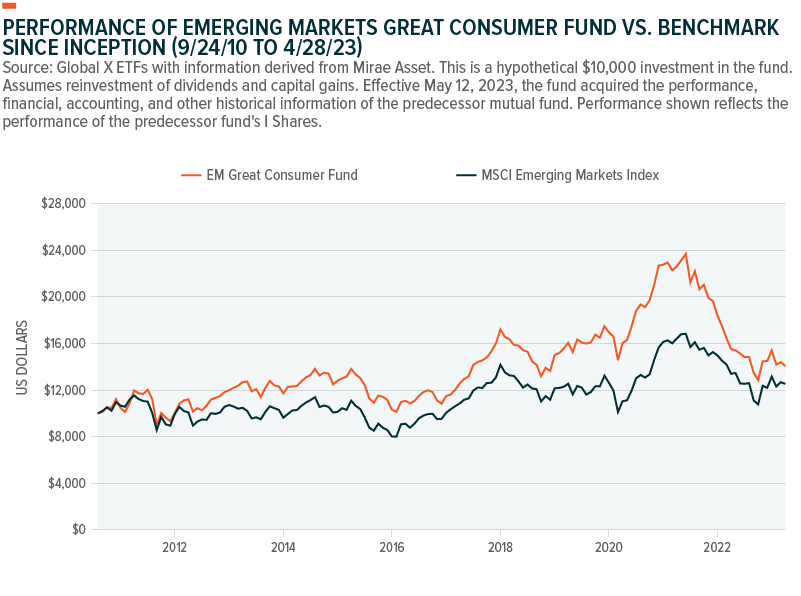

On May 12, 2023, we converted two actively managed emerging markets mutual funds advised by our affiliate, Mirae Asset Global Investments (USA) LLC (Mirae Asset), into two actively managed emerging market exchange traded funds (ETFs). The Emerging Markets Great Consumer ETF (EMC) and the Emerging Markets ETF (EMM) are the latest additions to Global X ETFs’ emerging markets suite. Both strategies carry 12+ year track records of long-term outperformance relative to their benchmark, the MSCI Emerging Markets Index.1,2 The funds have maintained their teams, investment processes, and investment philosophies, but are now offered as ETFs. Both funds seek to achieve long-term capital growth by investing in equity securities in emerging markets (EMs).

Key Takeaways

- We recently converted two actively managed mutual funds from Mirae Asset to active ETFs under the Global X ETFs brand in order to take advantage of the ETF structure, which brings with it lower costs, increased liquidity, greater transparency, and lower minimums.

- Although the asset class can be volatile, exposure to emerging markets has the potential to improve portfolio diversification and, possibly, returns.

- The nuances (being in the right countries, sectors, names, etc.) of emerging markets investments are keys to success, in our view, making active management a compelling strategy in an asset class with such varied cultures, currencies, political systems, and economic backdrops.

Transitioning the Funds From Mutual Fund to Active ETF

- Lower Costs: The expense ratios are dropping. Both funds now carry total expense ratios of 75 basis points (bps).

- Increased Liquidity: In an ETF wrapper, investors can buy and sell in-and-out of the ETFs on an intraday basis on an exchange, whereas mutual funds are only available for purchase or redemption once per day.

- Greater Transparency: Investors will be able to see all holdings within the strategies on a daily basis.

- Lower Minimums: A single share may now be purchased at a time. However, there may be additional costs, such as brokerage fees.

- Maintain Consistency: The funds’ teams, processes, and philosophies all stay the same.

- Potential Tax Efficiency: ETFs are generally more tax efficient than their mutual fund counterparts, as they typically generate fewer capital gains for investors. This is largely due to ETFs’ ability to use an in-kind creation/redemption process with Authorized Participants to limit the amount of taxable events. That said, EMM and EMC may also use a standard cash creation/redemption process, which could make them less tax efficient than ETFs that exclusively use an in-kind creation/redemption process.

Mutual Fund-to-ETF Conversions Demonstrate Confidence in the ETF Structure

In March of 2021, the US ETF industry saw its first mutual fund-to-ETF conversion, providing a road map for others to potentially follow suit.3 Since then, 39 US-listed mutual funds with $56B in total assets converted to the ETF wrapper, all of which were actively managed strategies and do not track an index.4 US and international equity strategies have seen the most assets converted from asset managers.

As per a Brown Brothers Harriman Survey in 2023, investors noted that a fund’s expense ratio was the most important factor when choosing an ETF, while issuer and tax efficiency were 2nd and 3rd.5 This may translate to an investor’s want for an ETF over a mutual fund, too. Typically demonstrating lower net expense ratios than their mutual fund counterparts, EM equity ETFs, and now EMM and EMC, offer investors access to professional portfolio managers within this same asset class.

Investment Philosophy

We see emerging market economies rapidly moving away from asset heavy, low return business models towards innovative, well-run, profitable sectors. This structural dynamic can create higher paying jobs as employees move up the value chain, which can inherently grow the middle class across emerging market countries. These entrants often spend their newfound discretionary income on education, healthcare, technology, goods, and services – all of which fall into the latter category of business models. This has the potential to create a self-fulfilling cycle of domestic consumer-driven growth.

Investment Process and Philosophy

The management team’s (portfolio managers and analysts) investment process for both funds consists of the following:

Step 1: A proprietary quantitative screening of the emerging market universe is run to arrive at an investable universe (IU).

Step 2: Recommendation lists (RLs) of stocks are compiled by each sector analyst for his/her respective region.

Step 3: A model portfolio (MP) is determined by the investment team.

Step 4: The actual portfolio (AP) construction is done by the portfolio managers.

The process requires each analyst to identify and validate his/her highest conviction ideas, based on fundamental company analysis, and weight them in his/her RL. The investment team utilizes the RLs to determine a model portfolio, which reflects stock weightings to indicate relative conviction levels of ideas. The portfolio manager utilizes the MP to construct an efficient, actual portfolio.

The key pillars of our investment philosophy include: identifying internal and structural tailwinds, while avoiding macroeconomic headwinds; investing in companies that benefit from sustainable competitive advantages; partnering with management teams aligned with minority shareholders; finding visible growth opportunities that could lead to near- and long-term positive earnings revisions; and analyzing intrinsic values based on GAARP (growth at a reasonable price) with multiples balanced by both growth and return profiles. For EMC, the strategy also maintains a key focus on domestic consumption.

Why Invest in Emerging Markets?

Various asset allocation theories, such as the Yale model, advocate for a diversified portfolio that includes investments in both developed and emerging markets.6 These models suggest that investors allocate a portion of their portfolios to EMs in an effort to take advantage of the growth opportunities in these markets, and also to diversify their portfolios and reduce risk.7 When looking at the annualized returns of the MSCI World Index (Net) versus the MSCI Emerging Markets Index (Net), EMs have outperformed developed market equities over the long term (January 01, 2001 through April 28, 2023), though they have also exhibited higher volatility.8 In terms of diversification, research has shown that including emerging market equities in a diversified portfolio can help reduce overall portfolio risk, while potentially improving returns.9

There are also a number of long-term tailwinds that could bolster the case for including active EM exposure in a diversified portfolio. In our view, EMs remain fundamentally attractive based on low penetration rates, catch-up opportunities, and a low base of earnings. The asset class may also benefit from attractive demographics, abundant natural resources, and low hanging fruit in regard to potential investor-friendly economic and political reforms. We also see powerful structural opportunities as economies shift away from asset heavy, low return industries (manufacturing, construction, commodities) and towards services, innovation, and high-return business models.

Why Active Management in Emerging Markets?

With more than 50 different countries, currencies, political systems, and economic backdrops, we believe emerging and frontier markets require a fundamentally different approach to investing than in developed markets.10 The opportunity set is large, but nuanced, which means being in the right names, countries, and sectors, can be vital to performance. Over the past decade, despite mild performance from passive EM strategies (the MSCI Emerging Markets Index delivered an annualized return of 1.80% in the trailing 10 years through April 28, 2023 versus 8.71% for the MSCI World Index), the world’s top performing country by year always came from within emerging or frontier markets (2012-Kenya, 2013-United Arab Emirates, 2014-Kenya, 2015-Hungary, 2016-Brazil, 2017-Argentina, 2018-Qatar, 2019-Russia, 2020-Korea, 2021-Kazakhstan, 2022-Turkey).11,12

From a passive perspective, our experience has been that EM benchmarks tend to lean towards large cap “national champions” and state-owned enterprises (SOEs). SOEs are generally government-owned/influenced companies operating with a broader set of interests, appealing more to their political and socio-economic interests rather than those of minority shareholders.13 By our estimation, these companies represent roughly 25% of the MSCI Emerging Markets Index. Emerging market benchmarks are also typically backward-looking in their methodology, in our view, significantly weighted towards historical drivers of growth, rather than smaller, innovative companies that may have the potential to capture future returns.14 While there is no guarantee an active manager will purchase specific securities or purchase them at an opportunistic time, there is more ability to do so.

From a geographic perspective, Asia represents more than 78% of the MSCI EM Index.15 So, if the average global equity investor has a 5% allocation to EM passively tracking this benchmark, then he/she would have just over 100bps dedicated to all of Latin America, all of Emerging Europe, all of the Middle East, and all of Africa combined, which means many opportunities within these deep markets could be overlooked. Moreover, in roughly a third of the markets classified as EMs by MSCI, more than half the market cap is in a single stock.16 In countries like Colombia, the UAE, Indonesia, Chile, Greece, and Saudi Arabia to name a few, 50% of index market cap is concentrated in fewer than five stocks.17 Consequently, investors may not benefit significantly from the diversification that is generally associated with broad market passive strategies. Active managers have more leeway to look beyond a country’s largest players and potentially invest in a wider swath of the investable universe, which could increase diversification.

A Management Team with Extensive Experience in EM Equities

EMM and EMC boast robust and responsible portfolio management team structures. As an asset class, emerging and frontier markets now contain more than 50 different countries, economies, currencies, political systems, and other factors.18 At the same time, investment management is moving in the opposite direction. Fees are declining, team numbers are diminishing, and it’s proving more difficult for EM managers to carry out their active mandates. This is especially true when one considers the concentration risks within global benchmarks. The EM team is positioned to take advantage of this opportunity. The team structure consists of a New York-based adviser (Global X Management Company LLC) and a Hong Kong-based sub-adviser (Mirae Asset Global Investments (Hong Kong) Limited) with portfolio managers hyper-focused on their respective regions of Asia and LatEMEA (Latin America, Europe, the Middle East, and Africa). With a 12-person research team between the adviser and sub-adviser, the group aims to analyze the smaller regions of the asset class with as much rigor as the large. The team also boasts personal, academic, and professional EM experience. The group speaks 11 unique languages and, for the most part, has grown up within EM cultures, using local products and understanding local consumption trends.

From a style perspective, the funds’ characteristics align with growth at a reasonable price (“GAARP”). The strategies aim to find quality business models that can offer sustainable compounding returns, trading below intrinsic value. We believe that growth only creates value when the business model boasts a difference between its economic returns and its cost of capital. The larger the spread, the more sensitive to changes in expected growth rates. Therefore, the team aims to balance valuation multiples with a company’s prospects for both earnings growth and reinvestment rates.

Both funds carry successful 12+ year track records of benchmark outperformance using a strict investment process and philosophy since inception. These are high conviction strategies offering portfolios of 50-65 names (60-65 in EMM and 50-55 in EMC), and they generally have had a 6-8% tracking error. Given this level of off-benchmark exposure, the team places an emphasis on downside mitigation via stress tests and sensitivity analyses.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance current to the most recent month- and quarter-end, please click on the fund names below.

The Global X Emerging Markets ETF Strategy

This EM fund presents an opportunity to invest in an active, tactical EM strategy focused on quality EM leaders within their respective sectors and regions. This is a well-rounded, core strategy focused on bottom-up fundamental analysis. This is a broad market fund that takes a tactical and opportunistic approach to investing in the world’s fastest growing economies. The professionals primarily responsible for the management of the fund are W. Malcolm Dorson for the adviser and Rahul Chadha and Phil Lee for the sub-adviser.

The Global X ETFs Emerging Markets Great Consumer ETF Strategy

The EM Great Consumer ETF presents an opportunity to invest in an active EM strategy with a responsible investment team, a proven process, and a differentiated focus on, arguably, the most attractive business models within emerging markets. The professionals primarily responsible for the management of the fund are W. Malcolm Dorson for the adviser and Joohee An and Sol Ahn for the sub-adviser.

The strategy aims to capture a structural shift across developing markets, as GDP profiles move away from exports and towards domestic consumption-driven growth. Though the fund may invest across all sectors, it is expected to consistently remain underweight in energy and materials relative to its benchmark, which also makes it an attractive compliment to portfolios tilted towards cyclicality and value.

With an underweight in exporters and commodities, the strategy seeks to reduce its exposure to the unknowns of foreign currency swings, commodity moves, and trade rhetoric. We believe this can help reduce volatility and improve risk-adjusted returns.

Conclusion

Emerging markets are some of the most dynamic in the world, offering potential for vast growth. Common themes of favorable demographics, abundant natural resources, and the possibility of investor-friendly political/economic reforms can make for compelling investment opportunities. Yet, many investors avoid the space for a variety of reasons, including its penchant for volatility. However, used as part of a diversified portfolio, exposure to the asset class has the potential to reduce volatility and increase returns.19 Due in part to the construction of emerging market benchmarks, as well as the diverse nature of the asset class, nuance is key, making this an area that is well suited to active management, in our view.

Related ETFs

EMM – Global X Emerging Markets ETF

EMC - Global X Emerging Markets Great Consumer ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.