Alex Roll

Alex RollAs the prospect of the end of the rate hiking cycle approaches, concerns are emerging about the upper limits of U.S. yields—particularly real yields— and their impact on equities. Recent upward pressure on Treasury yields has been driven by rising real rates, but concerns now focus on potential risks from rising term premia due to increased Treasury issuance and potentially reduced Chinese support. Whilst the consumer has remained strong, depleting U.S. household savings is another issue on investors’ minds. Following the artificial intelligence catalyst this year, investors seem once again to be favoring U.S. exceptionalism and infrastructure buildout. Looking beyond the U.S., Japanese equities have grown popular, with most adopting long positions, mostly hedged against currency risks.

We have witnessed investors rotating from highly defensive equity positions earlier in the summer to moderately cyclical assets. However, the primary concern remains the potential vulnerability of this shift to rising treasury yields given lower conviction levels. Further, energy security concerns are once again at the forefront with both Russia and Saudi Arabia extending supply cuts, leading to Brent Oil prices of $95/bbl in an environment of a rising Dollar Index (DXY).1 Amid these uncertainties, market breadth remains diverse, further complicating decisions. The current fiscal landscape, however, underscores government spending playing a larger role in corporate profit trends, marking a shift from the previous decade. Given this market backdrop, certain strategies that have strong secular trends and government fiscal backing may be poised to outperform in the near term. We feel similarly about volatility reducing, or less systematic, strategies.

Investment strategies highlighted this month:

- Uranium – In the quest for sustainable and reliable energy generation, uranium is emerging as a key fuel in shaping the future energy mix.

- Defined Outcome Strategies – These strategies could help reduce overall portfolio volatility and lower fixed income duration risk amid market uncertainty.

- Disruptive Materials – International collaboration and strategic investments are playing a crucial role in ensuring reliable and sustainable supply chains for the materials of our future.

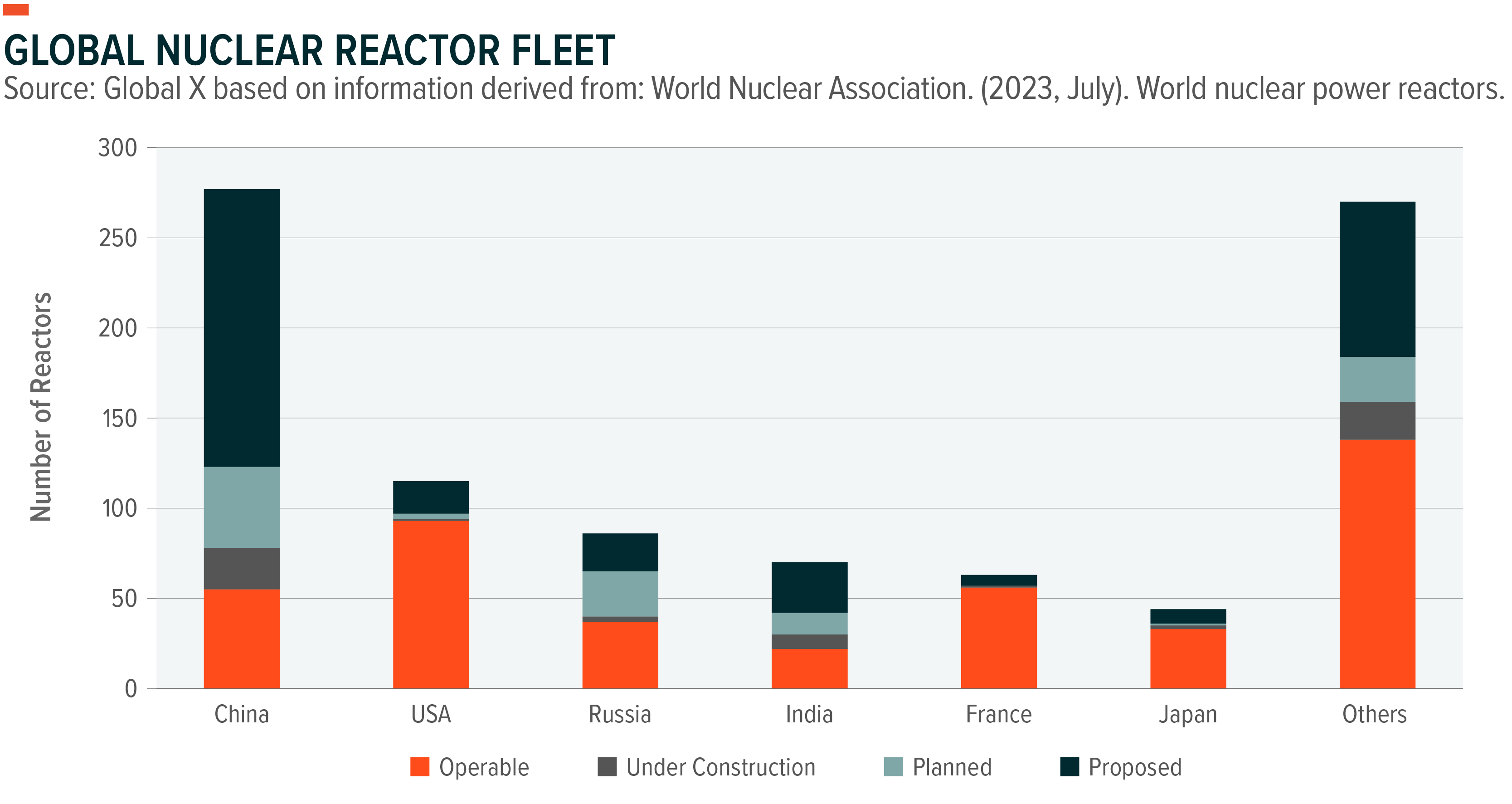

Uranium

In the quest for sustainable and reliable energy generation, uranium stands as a pivotal force in shaping the future of energy security. Governments are increasingly recognizing that nuclear power is a sustainable and low-carbon solution to the world’s growing energy needs and that it is a reliable source of electricity generation. Demand for nuclear power has been increasing in major economies like China, India, Japan, the United States, and various countries within Europe. Another critical factor supporting uranium’s outlook is a geopolitical shift in uranium sourcing. The United States and European utilities are moving away from purchasing uranium from Russia, a move that places additional strain on the limited number of converters and enrichers in the Western world, potentially driving uranium prices even higher. China also plays a pivotal role in the current dynamics of the uranium market, and intends to construct at least 150 new reactors over the next 15 years.2 This surge in growth far surpasses what has been achieved globally in the past three and a half decades.3 In the United States, the Accelerating Deployment of Versatile, Advanced Nuclear for Clean Energy (ADVANCE) Act of 2023 aims to support the development and deployment of nuclear technology.4

Uranium’s price inelasticity is a notable characteristic in the nuclear power sector as fuel buyers prioritize supply security over price. Uranium costs typically account for 4-8% of a nuclear plant’s ongoing expenses, making utilities price agnostic.5 Historical examples, like the 2007 uranium price surge from $23/lb to $143/lb, demonstrate that buyers are willing to pay significantly higher prices, even adjusted for inflation, to avoid nuclear plant shutdowns.6 Rising uranium prices have spurred exploration and mining activity, reversing a period of decline. With 436 operable nuclear reactors worldwide and many more planned, proposed, or under construction, there’s a growing supply deficit, exacerbated by pandemic-related mine closures.7 The industry faces a significant supply deficit extending through 2040, which could be amplified by financial buyers and the emergence of next-generation small modular reactors.8 Recent events, such as a coup in Niger and the U.K.’s creation of a Nuclear Fuel Fund, also highlight the importance of securing uranium supplies and advancing nuclear power globally.

Uranium mining stocks may offer a leveraged play on a material that is more illiquid than other commodities but is likely to have more persistent momentum in its trend. This is due to uranium’s more pronounced fundamental supply and demand imbalance and its longer cycle to reach equilibrium. The rise of Small Modular Reactors further highlights uranium’s essential role in the energy transition and global energy mix.

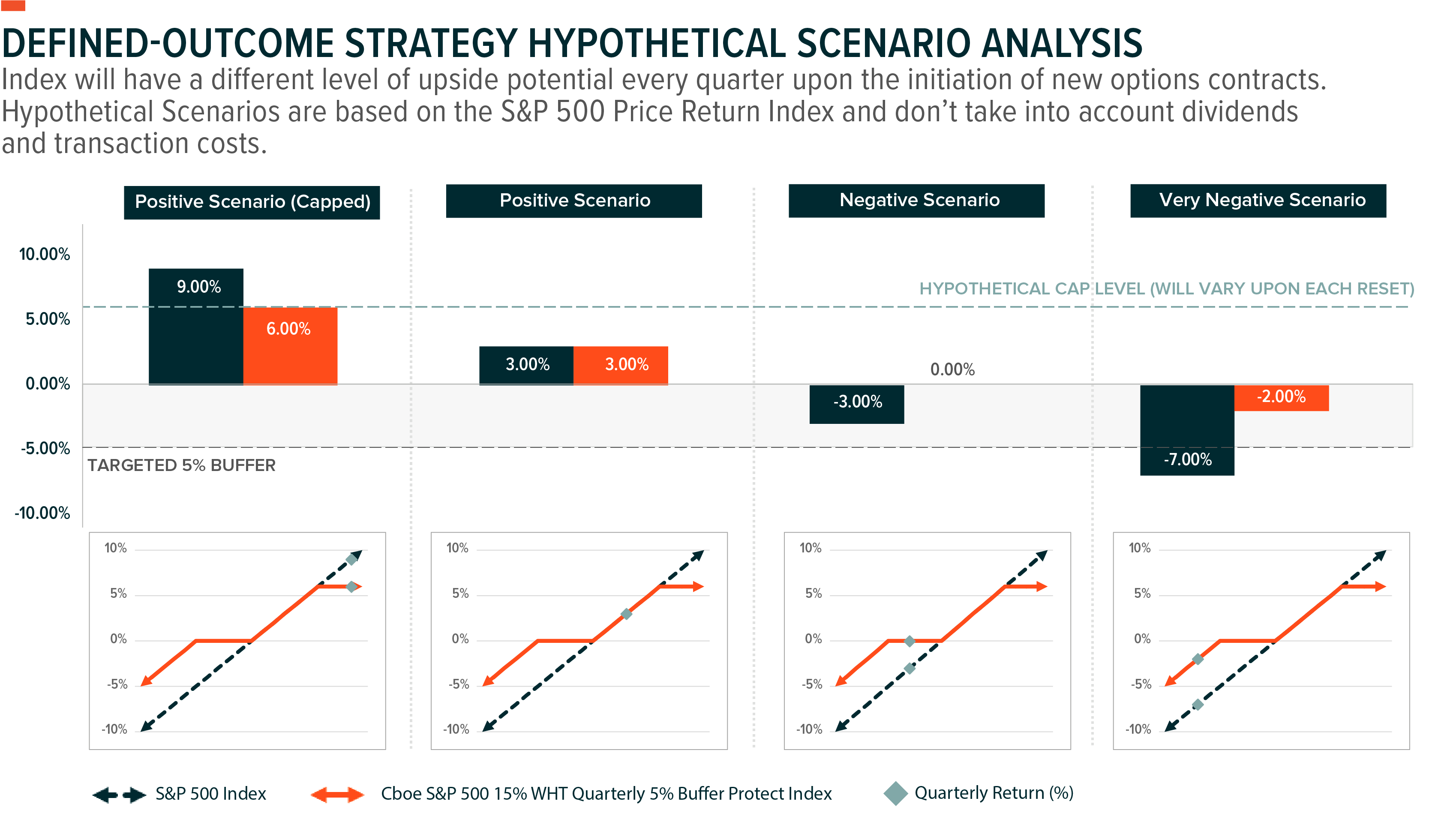

Defined Outcome Strategies

Defined outcome strategies can offer both portfolio volatility reduction and lower fixed income duration risk versus bonds. Prioritisation of risk reduction over capital gains could apply where there is uncertainty about market direction in the near term or an expectation of heightened volatility in equity markets. A defined outcome strategy could potentially help achieve this objective. If markets were to fall, these strategies would buffer some downside provided by a specified level, while participation in the potential upside up to a certain cap is still possible. It’s important to note that these strategies appear to be most effective when investors commit to a predetermined holding period. Implementing a defined-outcome strategy on a broad index such as the S&P 500 may serve as another option to offset sector risks of low volatility factor strategies. Furthermore, a defined-outcome strategy could potentially complement a traditional 60/40 equity/fixed income portfolio by reducing overall portfolio beta, as well as reduce duration risk on long-term fixed income.

Considering the predefined level of downside protection embedded in a defined-outcome strategy, a “defined outcome” could be expected in terms of returns from the underlying asset, as long as the strategy is maintained from the initiation of the contract until its expiration. As an illustration, take the Cboe S&P 500 15% WHT Quarterly 5% Buffer Protect Index, which serves as a representation of a quarterly defined-outcome strategy. This index incorporates a 5% buffer that resets at the start of each calendar quarter. To achieve this, the index constructs a put spread that combines a long “at-the-money” put option with a short 5% “out-of-the-money” put option. During bearish market conditions, the investor will only incur losses over a quarterly period if the S&P 500 experiences losses surpassing the 5% buffer. Conversely, in a bullish market trend, the investor could enjoy full participation in the upside of the S&P 500 up to a predetermined cap, which is determined by the strike price of the covered call for the specific outcome period.

It is important to note that the defined outcome is specific to each fund’s holding period. Liquidating early or buying midway into an outcome period results in varying degrees of downside protection and upside caps. Defined outcome strategies may be most appealing when seeking to retain long exposure in the market but also reducing overall beta and volatility risk.

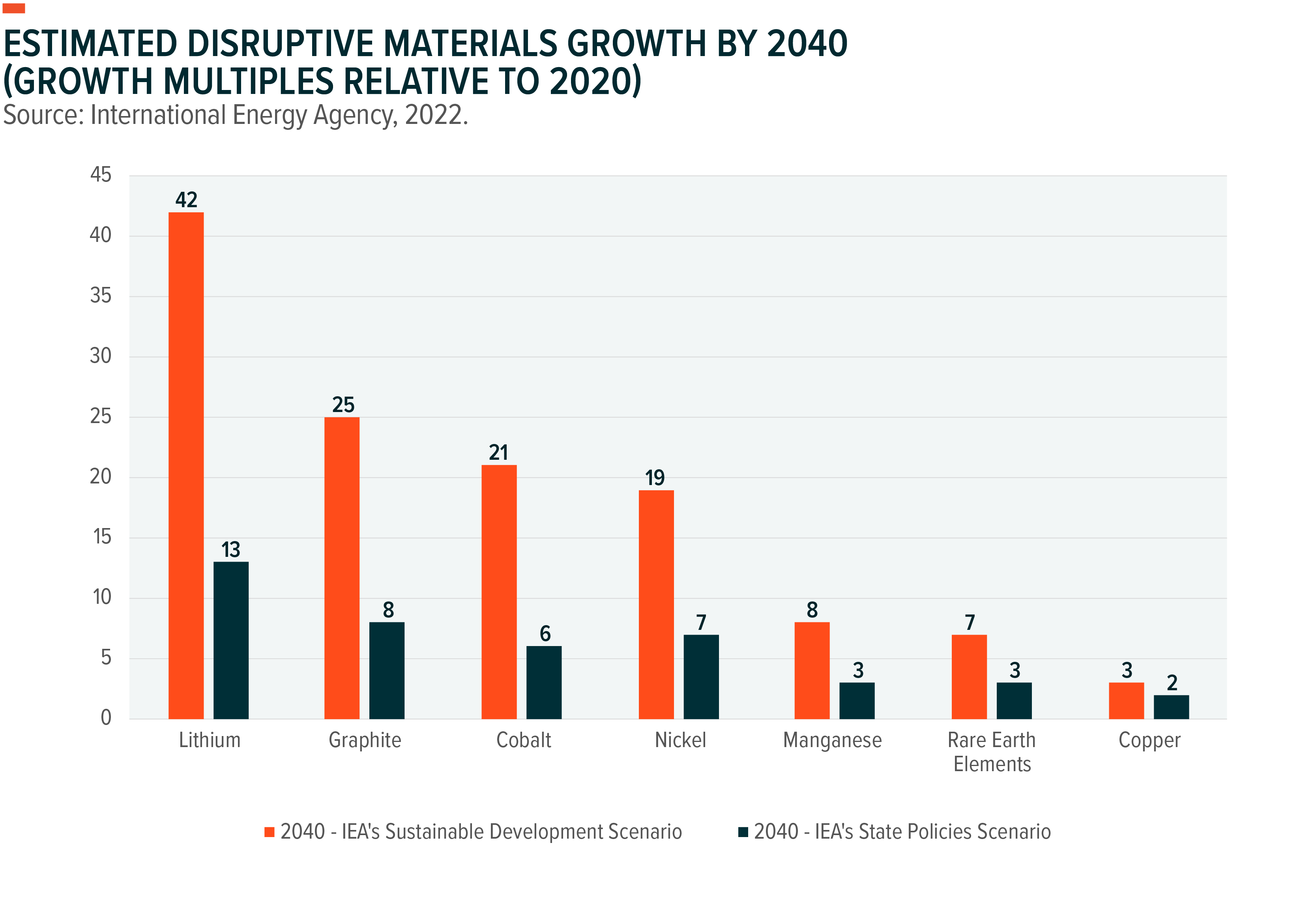

Disruptive Materials

International collaboration and strategic investments are playing a crucial role in ensuring reliable and sustainable supply chains for the materials of our future. The rapid growth in clean energy demands has created new opportunities for disruptive materials, but it has also presented a complex landscape characterized by volatile prices, supply chain bottlenecks, and geopolitical concerns. Consequently, international cooperation has emerged as a key strategy for ensuring reliable mineral supplies, including the Mineral Security Partnership, which aims to facilitate investments in diversified mining regions.9 Further, to address supply and diversification concerns, numerous countries have introduced policies and initiatives. These include but are not limited to the European Union’s Critical Raw Materials Act and the United States’ Inflation Reduction Act. These policies aim to ensure sustainable and adequate mineral supplies by incentivizing exploration and refining activities.

The surge in electric vehicle (EV) sales, which increased by 60% in 2022, has substantially contributed to the demand for disruptive materials—particularly lithium, a key component in EVs.10 Between 2017 to 2022, demand from the energy sector tripled for lithium, increased by 70% for cobalt, and rose by 40% for nickel.11 As part of this, we witnessed record-breaking installations of solar photovoltaic systems, while wind power also boosted demand. Investment in disruptive materials development has seen significant growth, with a 30% increase in 2022. Companies specializing in lithium development have recorded a 50% increase in spending, followed by those focusing on copper and nickel. Companies based in China nearly doubled their investment spending in 2022, reflecting the global importance of these materials. In the business sector, EV manufacturers, battery cell makers, and equipment manufacturers are increasingly investing in critical mineral value chains, from mining to refining. Long-term offtake agreements have become standard procurement strategies, further strengthening supply chains. Automakers like Tesla, General Motors, and BMW have secured long-term agreements for disruptive materials.12

Many countries, including Indonesia and China, have imposed restrictions on certain materials exports. Australia stands out as a potential solution to meet the growing global demand for disruptive materials, thanks to its supportive sector strategies and international collaboration. For example, Australia’s Lynas Rare Earths Ltd. is expanding its rare earth processing facility and mining operations.13

In the International Energy Association’s Announced Pledges Scenario (APS), projected demand for disruptive materials is poised to more than double by 2030. In the Net Zero Emissions by 2050 (NZE) Scenario, demand for disruptive materials grows by three and a half times by 2030. Disruptive materials are indispensable in a growing number of modern applications, with everything from electronics and clean energy tech to the defense industry contributing to their soaring demand trajectory.