Michelle Cluver

Michelle CluverRapid economic recovery coming out of the pandemic created distortions in the labor market – raising questions about economic growth and the future of work. While the disruption of the last few years increased bargaining power, it also heightened concerns about inflation, and consequently real economic growth. But with recession fears rising, the labor market is a key focal point to understanding potential recession severity. Labor participation has risen as COVID-19 concerns diminish and wages and inflation pressures rise.

Key Takeaways

- High demand and the unexpected shift within the economy left a deficit of workers, increasing bargaining power and inflation risks.

- The pandemic seemed like the ideal time to retire, but unretirement is a growing trend as inflation and market volatility diminish purchasing power and savings.

- Weaker earnings and rising economic growth concerns have increased the focus on employment data as the market assesses recession probabilities and potential negative feedback loops.

- Automation remains an area of interest as companies strive to improve efficiency.

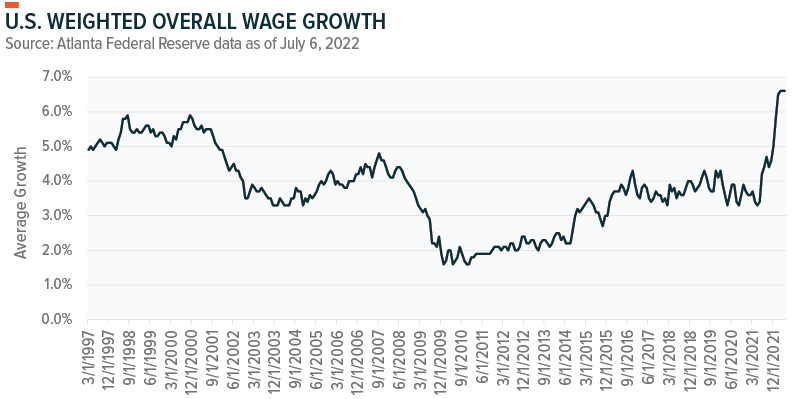

Labor Supply Imbalance

Inflation and the Federal Reserve (Fed) are key focal points for markets in 2022. Rising wages create the potential for a price-wage spiral, escalating inflation fears. But without wages keeping pace with inflation, reduced purchasing power is likely to weigh on consumption. We are starting to see this reflected in weaker consumer spending and sentiment. June’s consumer sentiment dropped to an all-time low of 50.0 on the back of inflation pressures.1

Supply disruptions in the labor market increased wages at their fastest rate in decades. However, as economic uncertainties increased, wage growth plateaued and remains below CPI.2 But the labor market remains tight, with job openings rates well above pre-pandemic levels, reducing the number of unemployed per job opening to historic lows.3 In June, 372,000 jobs were added–adding upwards of 9.1 million jobs since the end of 2020.4

Setting up the Analysis

As discussed in our second half outlook, employment and consumption are currently the key areas of recession risk for the U.S. economy. While job openings data continue to reflect a tight labor market, following a weak earnings season, there may be a developing trend towards staff reduction and right sizing operations. According to Morgan Stanley, the unemployment rate is likely to remain rangebound at about 3.4% until the end of 2022.5 Though, economic data has deteriorated, with retail sales declining 0.3% from May relative to April while manufacturing activity decelerated in June.6 This may portend weakness ahead, increasing the emphasis on monitoring employment data for signs of economic weakness and reduced inflation pressures.

Labor force participation remains below its pre-pandemic levels, but participation has generally been on an improving trend, particularly within the prime age group of 25 – 54. Participation among prime age workers has almost returned to its pre-pandemic levels, while economic participation by those 55 and older has remained low since the start of the pandemic.7

Millions of older Americans retired during the pandemic, but rising inflation, year-to-date market declines, and an abundance of jobs led retired U.S workers back into the labor force. According to analysis based on Census Bureau data, 3.2% of workers that retired a year earlier were back in the labor force by March of 2022.8 This is a more common occurrence than people think, from 2017 to 2019 roughly 3% of retirees returned to work.9 This took a dip in the beginning of the pandemic as the unretirement rate fell from 3.2% in February 2020 to 2.1% by June of 2020. The trend towards unretirement is expected to increase. A recent survey of 1,200 currently employed, 450 individuals who retired during the pandemic, and 400 individuals who are not in the workforce but also not retired, reflects that 68% of workers who retired during the pandemic and 94% of those who left the workforce but didn’t retire, would now consider returning to the workforce.10,11

While the reentry of older workers increases the supply of labor, recession fears may dampen demand for labor. The employment situation is a key area of focus as consumer confidence and spending come under pressure.

Increased Bargaining Power in Key Industries

The pandemic and recent labor shortages altered trends in the workplace. Labor shortages have pushed up wages and contributed to a revival in union membership. The National Labor Relations Board, an agency dedicated to addressing labor rights violations and protecting workers’ right to organize, reported a 57% increase in union petitions from October 2021 to March 2022.12 West Coast ports labor negotiations are likely to be a focal area this summer as unions representing 22,400 dock workers renegotiate a six-year labor contract that expired at the beginning of July.13 This negotiation impacts 29 ports and represents almost half the containers entering and leaving the U.S., and is the main gateway for trade with China.14 While demand for goods has reduced, should talks breakdown, port disruptions could adversely impact supply chains, raising inflation risks while potentially dampening economic growth.

Automation Remains a Solution to Labor Shortages and Higher Wages

Automation has been a key point of contention in the West Coast port labor negotiations. But focusing more broadly, higher wages and increased operating costs are starting to weigh on corporate margins.15 Rising wages shift the cost benefit analysis for automation. Trends in automation remain encouraging, with Taiwanese automation providers seeing a 16-23% year-over-year growth in May.16 Inflation, supply chain disruptions, rising wages, and COVID-19 have one solution in common: automation. Companies are increasingly allocating capital towards improving infrastructure through automating plants and facilities. In recent reports, Honeywell revealed an increase interest in warehouse automation systems focused on capabilities to pick, pack, sort, and carry packages.17

However, higher interest rates and economic growth concerns may delay capital expenditure. When the Fed raises interest rates, borrowing money becomes more expensive, potentially impacting corporate expansion and hiring decisions. According to Bank of America analysis, global profit expectations are at their weakest point since the Global Financial Crisis, increasing the risk of a profits recession.18 Slower sales growth expectations, balance sheet strength, and operating cash flows impact the willingness and ability of companies to invest through this cycle.

Conclusion

Soaring inflation initiated a hawkish shift from the Fed, increasing policy interest rates to a range of 1.5%-1.75% in the first half of 2022. The Fed is expected to raise rates a further 1.5% in the second half, but yield expectations are starting to reduce as markets reassess recession probabilities.19 While the labor market remains tight, trends in employment remain a key consideration for assessing the health of the U.S. economy. Labor participation is likely to increase in the second half as the unretirement trend takes hold and more unemployed individuals actively seek positions. Increased labor supply combined with automation may dampen wage growth. While encouraging from an inflation perspective, slower real wage growth has implications for consumer confidence and spending trends.