Rohan Reddy

Rohan ReddyCOVID-19 ravaged demand-sensitive sectors like Energy last year when economies around the world came to a standstill. From mid-February to mid-April 2020, energy demand in countries in full lockdown declined 25% on average and 18% in countries in partial lockdown, according to the International Energy Agency (IEA). But by Q4, clouds over the Energy sector began to part as vaccine approvals provided hope, economic activity picked up, and future energy policy in the US came into focus. In our view, these developments along with rising inflation expectations make the sector, particularly midstream companies, attractive as part of an income-oriented investment strategy.

Key Takeaways

- Many macro and political overhangs lifted by the end of Q4, with optimism about the re-opening economy driving Energy sector gains.

- Value sectors like Energy shined as the economy rebounded, and small cap and cyclical sectors became market leaders.

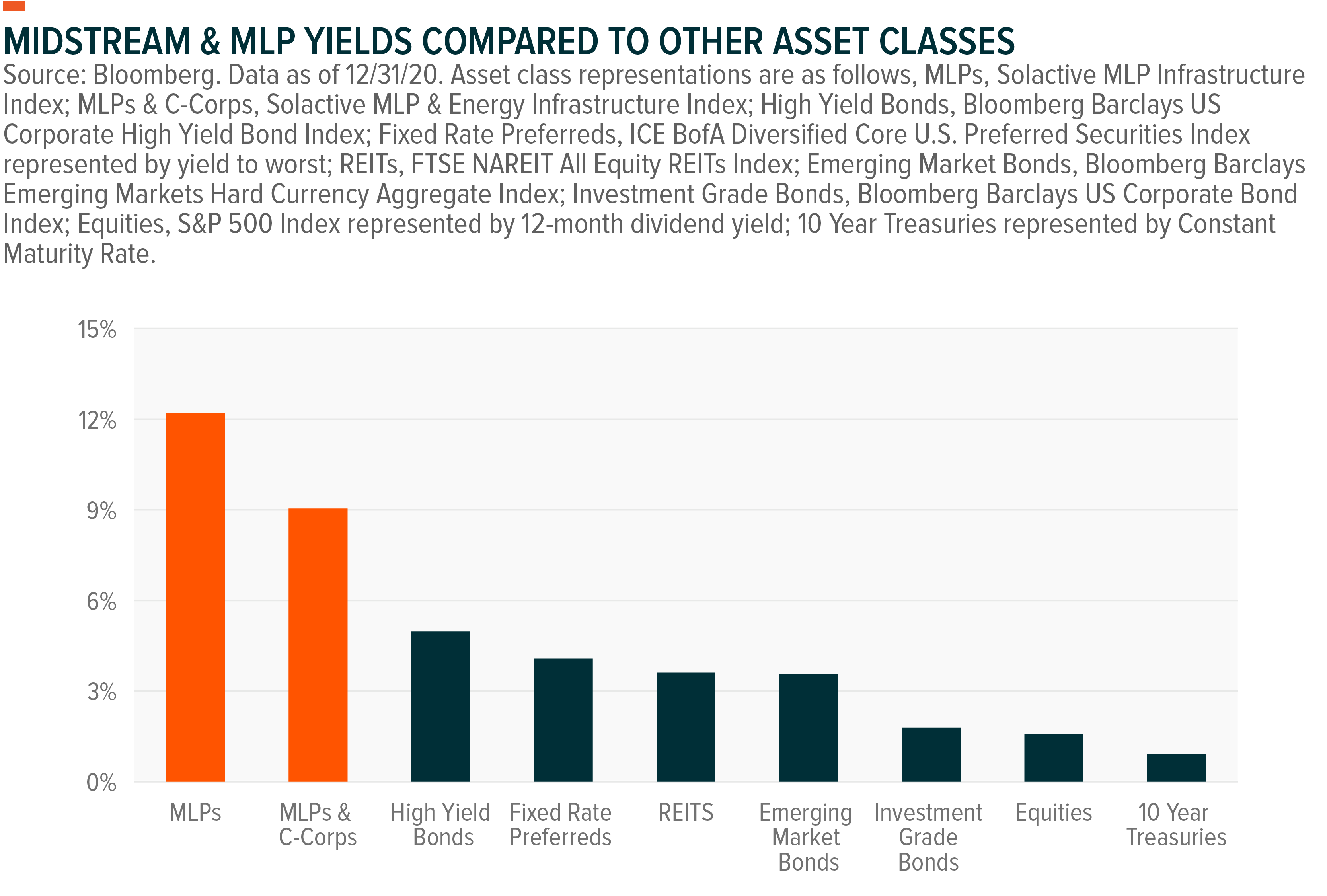

- With rising inflation, midstream equities offer an attractive potential income stream due to high yield spreads compared to most other asset classes.

- The Energy sector outlook is compelling as macro fundamentals strengthen and an infrastructure bill is discussed.

Macroeconomic and Political Overhangs Lifted

Energy is quite sensitive to economic activity, so economies on pause due to a global pandemic has significant repercussions for the sector. However, vaccine approvals and initial vaccinations rollouts around the world provided a healthy dose of optimism toward the end of 2020. In the US, the Food & Drug Administration (FDA) approved the Moderna and Pfizer-BioNTech COVID-19 vaccines for emergency use in December. With more vaccine approvals on the horizon globally and increasingly efficient vaccination programs, an end date to the COVID-19 ordeal is gradually coming into sight.

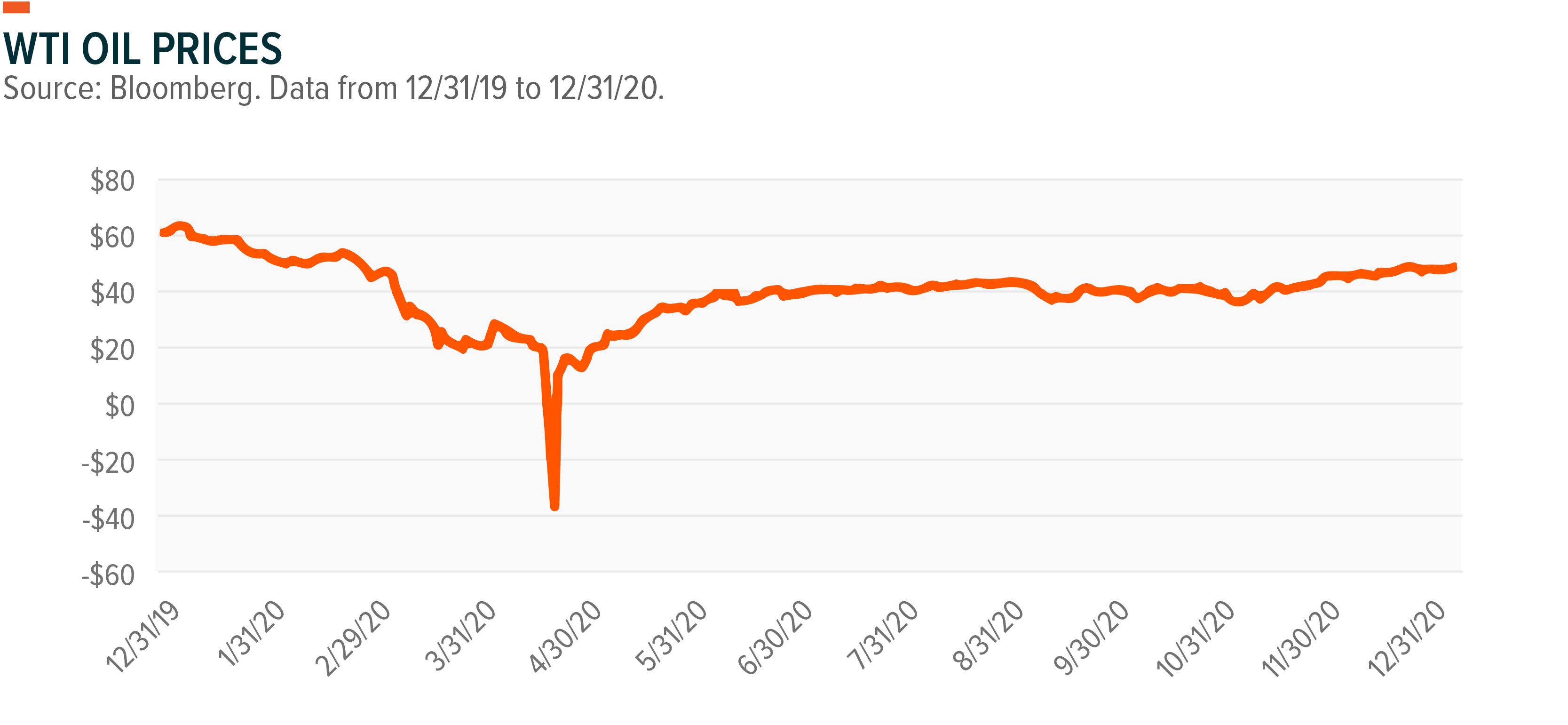

After a long period of malaise, oil prices increased from $40 to $49 in Q4 as global economic activity picked up with restrictions easing. The initial shock of the COVID-19 pandemic caused oil prices to crater, even turning negative for the first time ever in April. A slow recovery took prices to the $40 range, where they middled along for months before starting to climb again mid-Q4.

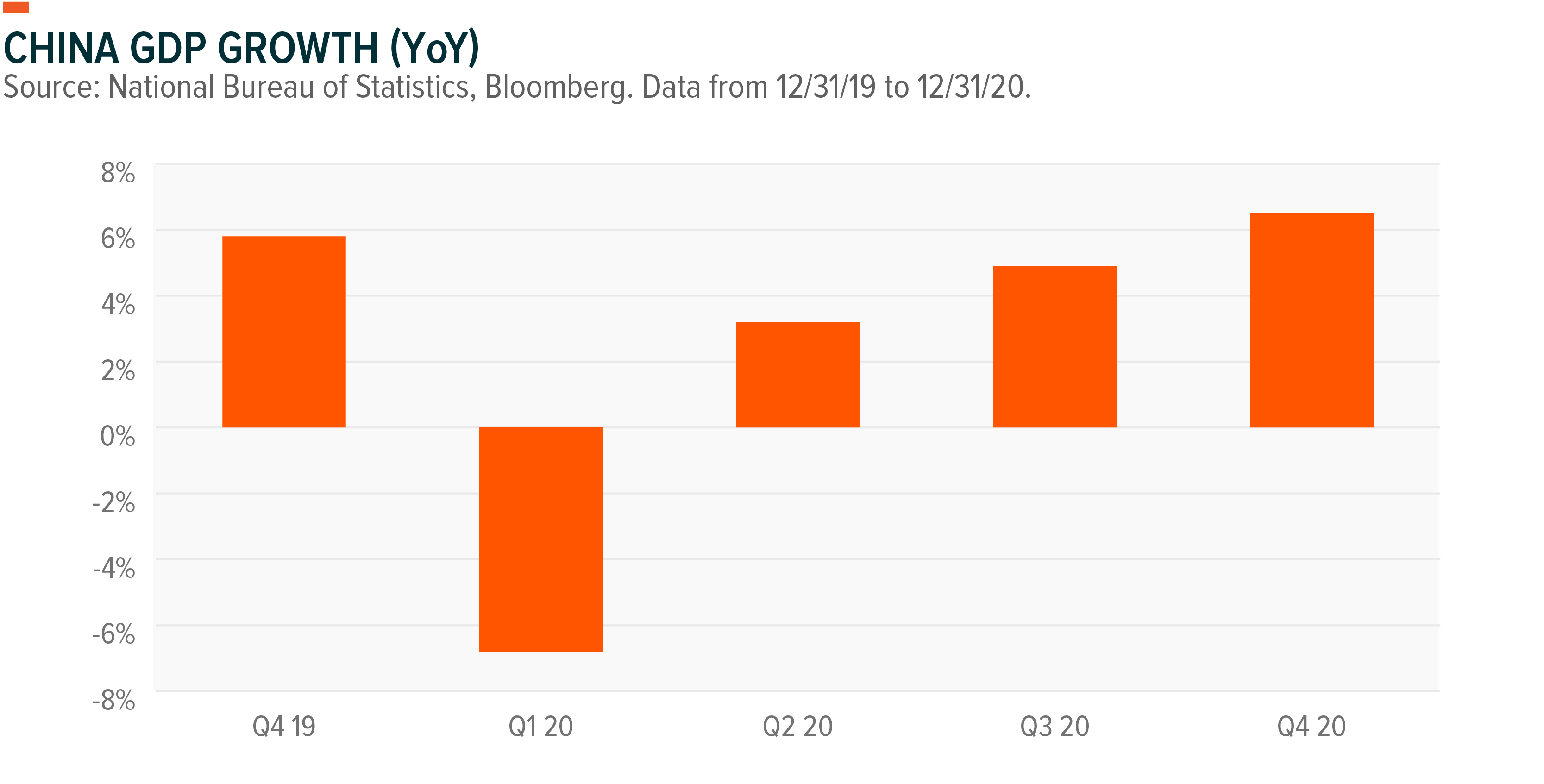

Economic growth in the US and China, the world’s largest economies, turned for the better in Q4, and growth expectations are continuing to rise. As a region, Asia handled the pandemic response particularly well and data there gradually returned to normalcy throughout the second half of the year. China’s manufacturing data was a standout, with its Purchasing Managers’ Index (PMI) increasing from 50.9 in June to 51.9 in December. That result helped China’s GDP growth rise from 3.2% year-over-year in Q2 to 6.5% in Q4.1

Like in China, the US’s PMI increased from 52.2 in June to 60.5 in December. The December improvement helped drive the US’ Q4 GDP growth to 4%, following abnormal readings of +33.4% in Q3 and -31.4% in Q2. With this result, the Congressional Budget Office estimates the US economy will grow 4.6% in 2021.2

The US election also provided much-needed clarity for the Energy sector. In the run-up to November 3, the market feared that a Democrat-controlled House, Senate, and White House could bring legislative risks to the traditional oil and gas industry. But the risks are more centralized, reflective of a society that increasingly favors a coordinated approach to cleaner energy sources. President Biden’s energy agenda focuses on putting a lid on widespread Energy sector growth, rather than trying to systematically eliminate the sector’s presence in the economy.

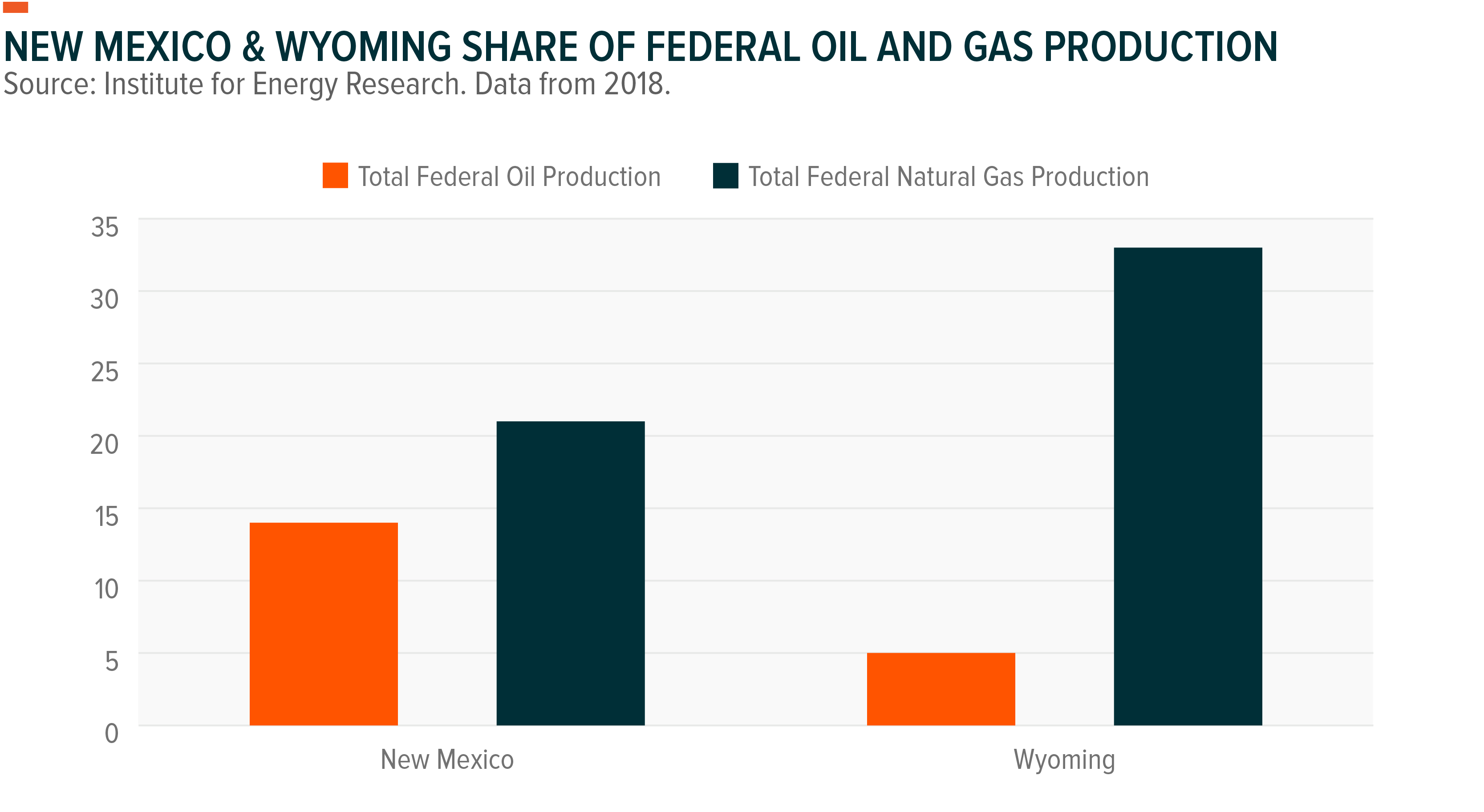

For example, as promised during the campaign, Biden halted new oil and gas leases on federal lands, but he still allowed existing leases on federal land to continue. This move may limit downside to specific companies and geographies with at-risk assets, rather than impact the broader industry. For context, 22% of total oil production and 12% of total natural gas production in the US is on federal lands.3 The states most affected by these measures are New Mexico and Wyoming, as they have the most federal acres under lease.4

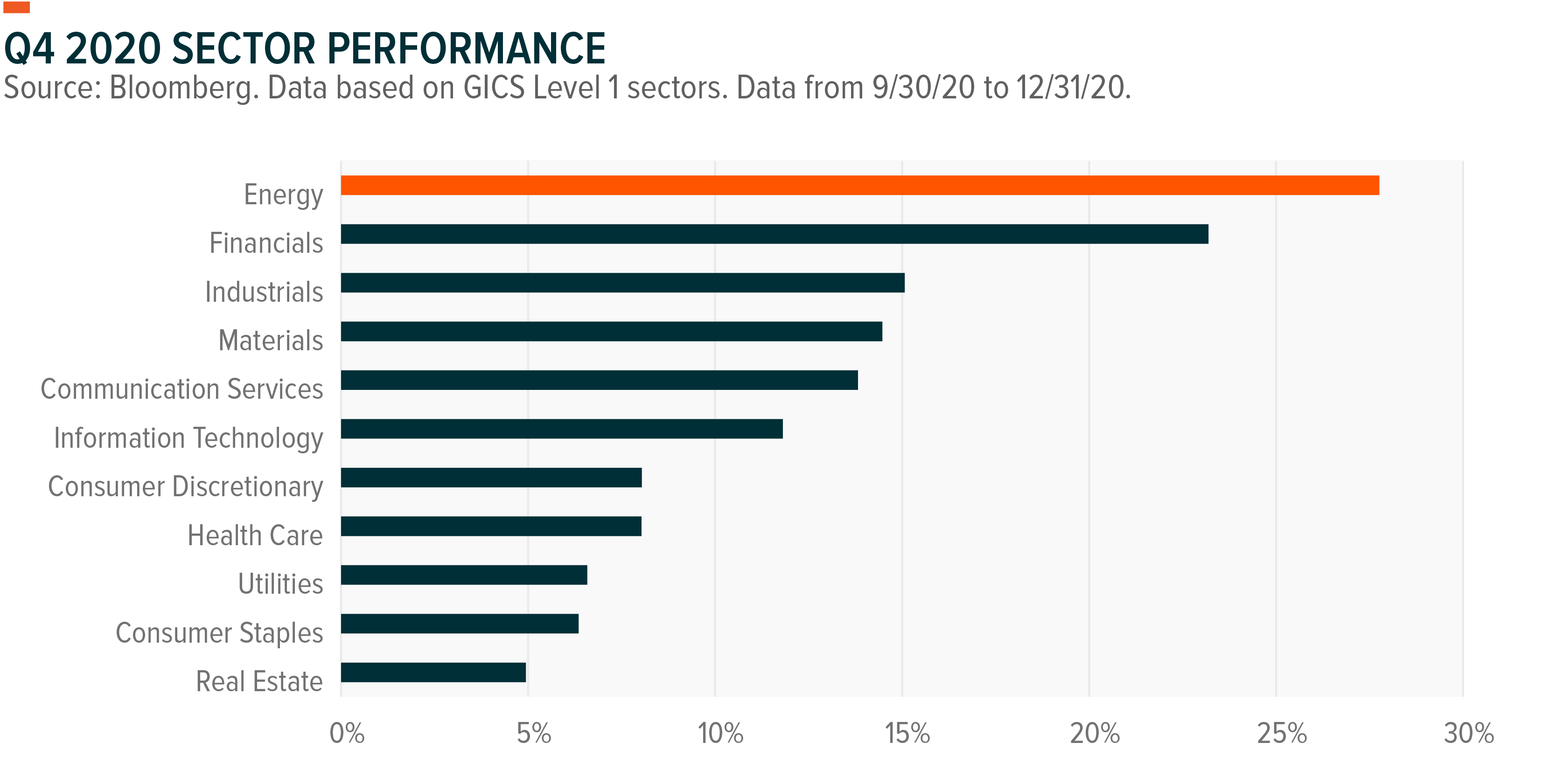

Q4 Performance: Value Sectors Shine As Demand Rebounds

In response to Q4’s positive news flow, growth-oriented sectors like Technology took a backseat to value sectors like Energy. In another sign of cyclical strength, small caps vastly outperformed the broader market and high growth indexes. The Russell 2000 returned 31.36% versus just 13.09% for the Nasdaq 100 and 12.14% for the S&P 500 during the quarter.5 The Energy sector rallied 27.76% in this time frame and midstream MLPs returned 25.51%.6 A resurgence of value and small caps often is a sign the market believes economic conditions are improving. The domestic economy is often strong in these periods, meaning services sector demand and the consumer are operating at higher than average levels. This signals greater demand for energy consumption.

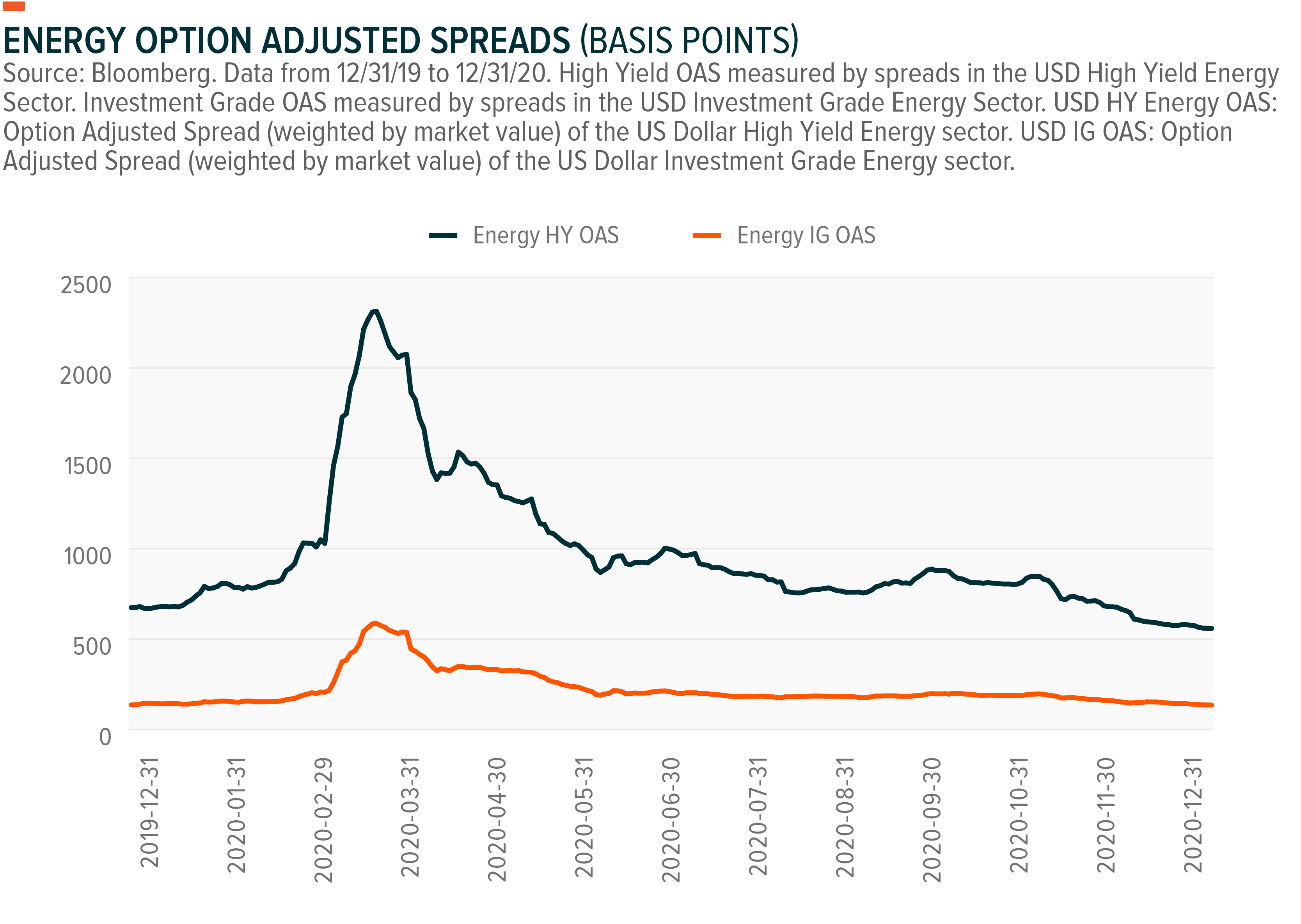

Initially, the shock of COVID-19’s spread led to black swan-like fears in the energy market. Financing conditions proved challenging. A bond yield blowout in the sector made credit issuance extremely challenging, and a longer-term shift away from equity issuance left energy companies in an uncertain position. But two factors kept the sector afloat.

First, the Federal Reserve stabilized the credit markets. The Fed slashing interest rates to zero gave energy debt investors a lower yield spread. Second, the market came to believe that it overestimated credit riskiness in the energy patch. High yield credit markets rallied after the initial yield blowout when it was clear energy demand wouldn’t be entirely shut down and OPEC+ support – via production cuts – would be extended for months to come. Fed actions and the government’s emergency stimulus measures also helped to assuage fears and reset energy asset prices when the economy began laying the normalization groundwork in Q4.

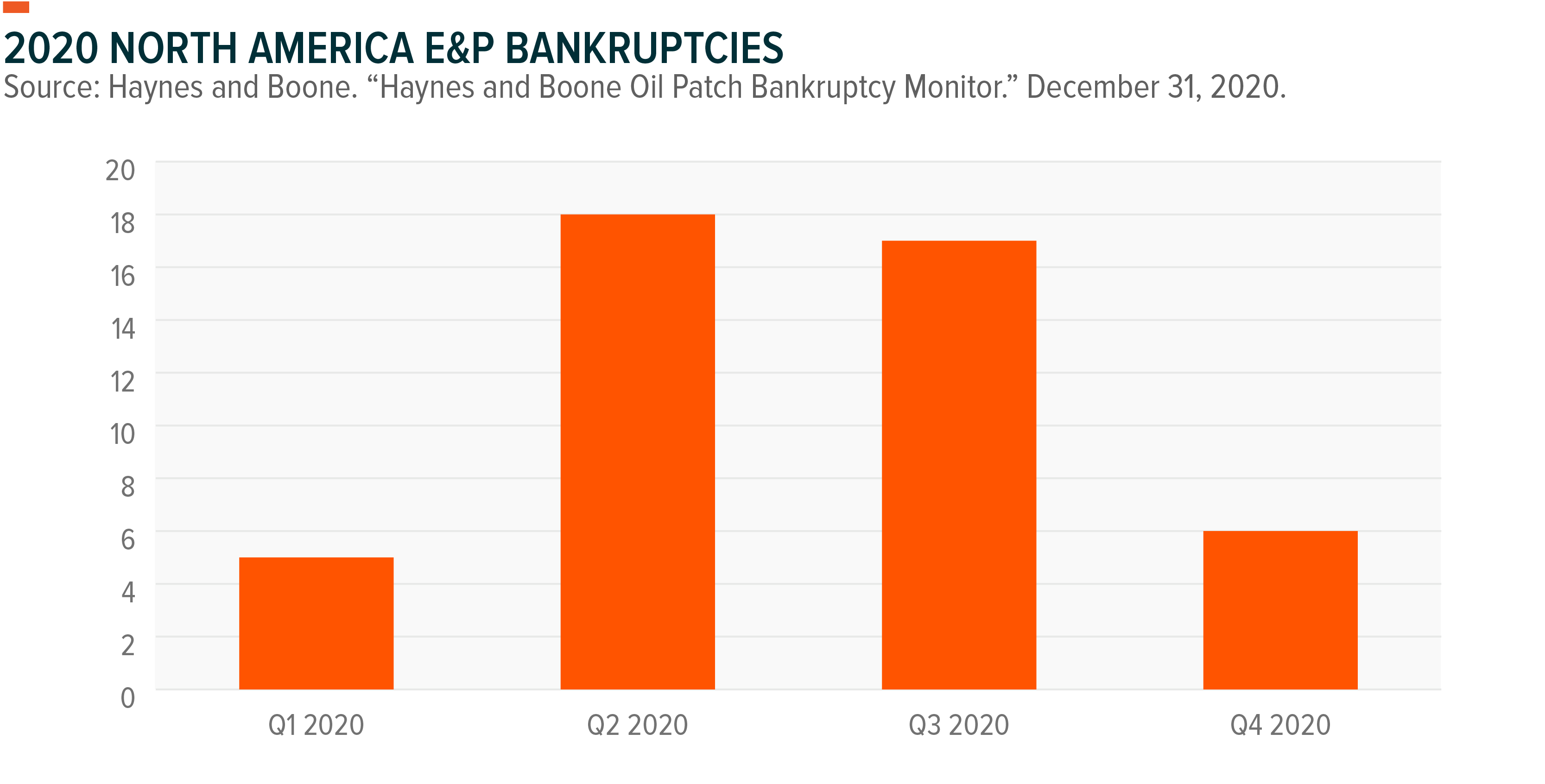

Energy also benefitted from some clarity on midstream contracts in Q4 as bankruptcies were settled. Bankruptcies spiked after the oil price collapse last March, but the pace slowed considerably throughout 2020 as fundamentals improved. Midstream companies have a vested interest in recovering as much as they can from Exploration & Production (E&P)’s during the bankruptcy process. Bankruptcy court is fraught with uncertainty, but these settlements indicate distressed upstream E&Ps are willing to work with their midstream counterparts in this environment.

- Extraction Oil & Gas, which declared bankruptcy last year, settled with Elevation Midstream to provide the firm with approximately 60% of what it claimed it was owed.7

- Extraction entered a new supply agreement with NGL Energy Partners (NGL), retaining Extraction’s crude volumes on NGL’s Grand Mesa Pipeline.8

- Chesapeake Energy settled with Williams Cos (WMB) for $112 million and WMB entered into a new gas supply commitment with Chesapeake.

With Rising Inflation, Midstream Equities Become A Key Potential Income Strategy

In Q4, the 10-year US breakeven rate, a measure of inflation, rose from 1.63% to 1.99% and oil prices went from $40 to $49. In the 10-year period through 2020, the 10-year breakeven rate had a 55% correlation to monthly oil prices in the US.9 It’s not necessarily a 1-to-1 move, but higher oil prices are typically associated with inflation. Oil’s rise in Q4 could be a directional indicator of inflation to come. For more thoughts on the inflation outlook, see our latest Income Monitor.

Inflation historically pushes up bond yields, but often the rise is only in nominal terms, as real yields, which account for inflation, remain relatively flat. To maintain high real yields, investors may want to consider asset classes with high yield spreads to US treasuries. Currently, yield spreads on midstream are some of the most attractive in the market, finishing the year at 8.13%.10 At the same time, there were no distribution cuts to major midstream companies in Q4 and coverage ratios for distributions are strong at 2.2x on average for the Q4 period, indicating that the high yields appear sustainable.11 Further, midstream entities have established certain contractual escalators on tariff rates to mitigate the cash flow risks associated with higher interest rates. After the multi-year transition to the self-funding model, many midstream companies paid down debt and reduced leverage ratios to the 4.5x range in an effort to limit refinancing risks. In addition, FERC regulated pipeline tariff rates are tied to the Producer Price Index for oil pipelines, so pipelines can pass through inflation to customers.

Energy Outlook Compelling with Improving Fundamentals, Infrastructure a Priority

COVID-19 wreaked havoc on energy production in the US last year. Oil production peaked at 13 million barrels per day (mbpd) last March and then began its slide to a low of 9.7 in August. But production stabilized in the 11 mbpd range towards the end of 2020 and appears set to trend higher as an increasingly vaccinated economy ramps back up. How to get that production from Point A to Point B is part of a broader strategic prioritization by federal and even state governments, most visibly through a potential infrastructure bill at the federal level. Investors looking to capitalize on energy infrastructure opportunities may see government focus as a point of interest. The recent cold weather crisis in Texas and middle America showed that the case for, and discussions about, improved energy infrastructure isn’t going away anytime soon. The latest Infrastructure Report Card from the American Society of Civil Engineers gave the US a C- grade.12

Higher-yielding income assets like midstream equities may look more attractive to investors in 2021 with rate expectations increasing. Midstream’s 8.13% yield spread to the 10-year treasury is well above other income-oriented asset classes like REITs & Utilities, at 3.95% and 2.52%.13 Midstream’s income profile is an upgrade too. MLPs for example often distribute Return of Capital (ROC), potentially providing greater after-tax income. For investors concerned about idiosyncratic risks in midstream, eschewing active management for a broad-based passive offering like the Global X MLP & Energy Infrastructure ETF (MLPX) could be an efficient and low-cost way to gain exposure to a space well-positioned for a re-opening economy.