Michelle Cluver

Michelle CluverThis piece is part of a larger whitepaper, Investing in Thematics From a PM Perspective.

Paper currency is dying a fast death as technology shifts how people access and interact with their money. Fintech solutions are expanding access and improving the efficiency of financial services. And user interfaces are fast becoming all-digital through online banking, digital wallets, crowdfunding, and buy now, pay later (BNPL) services. But digital disruption remains a work in progress at traditional financial firms. For example, transfers between banks or across borders can still take multiple days to settle. Over time, we expect fintech and blockchain solutions to become more integral across the financial services ecosystem resolving some of these inefficiencies. And as user adoption rises, so too will its prominence in portfolios.

Key Takeaways

- We expect the digital transformation to bring financial services, including mobile payments, online banking, and alternative lending platforms to previously unbanked and underserved populations.

- The pandemic put Fintech’s adoption into overdrive, with digital payments moving into mass adoption. But the Fintech market continues to expand with emerging segments such as BNPL, alternative financing, and blockchain solutions are key avenues for future growth.

- Necessity will likely encourage more traditional financial services companies to incorporate cloud banking and blockchain solutions.

Why Fintech and Blockchain are Such Powerful Forces

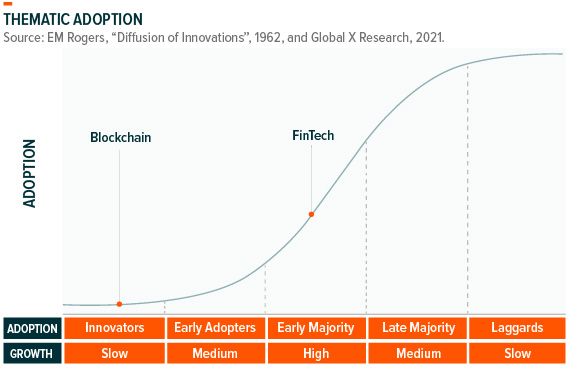

The intersection of financial services and technology, or fintech, is where people go to spend, lend, borrow, invest, and trade. Fintech makes financial services more personal and inclusive. Over the last two years, fintech adoption has increased dramatically, and we expect innovation in the space will continue to increase access to the global financial ecosystem.

Importantly, traditional financial institutions are integrating fintech in their business models. Firms are under pressure to reduce their reliance on legacy infrastructure while strengthening core banking systems to create better consumer experiences. Additionally, the increased focus on data connectivity and analysis to improve corporate decision-making has increased interest in fintech. Global investment activity in fintech, including through venture capital, private equity, and M&A, increased from $124.9 billion in 2020 and $148.6 billion in 2019 to $210 billion in 2021.1

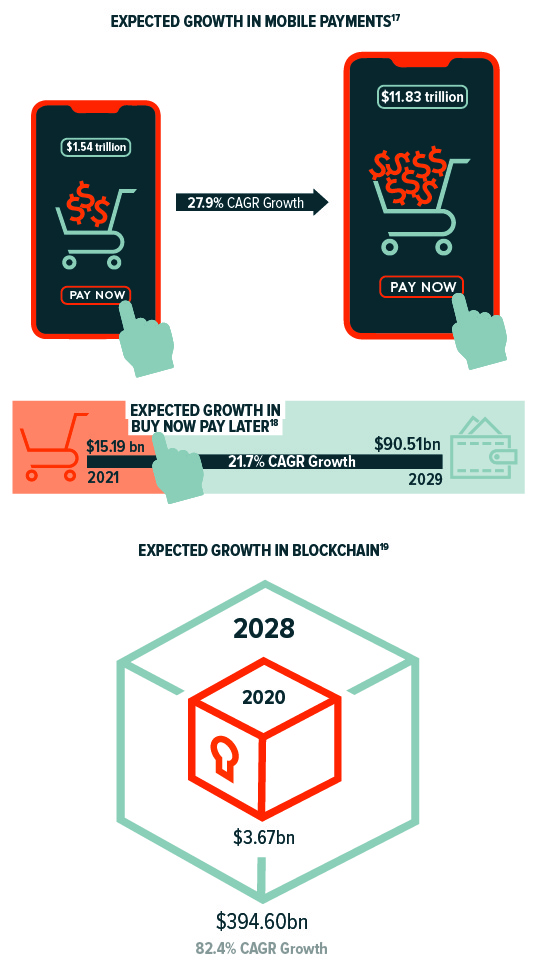

The rise of the digital payments segment illustrates consumer willingness to adopt new technologies and the enormous growth potential for fintech applications. For consumers, the ease and convenience of buying goods or services by tapping a device on a point-of-sale makes digital payments Fintech’s most recognizable segment. For companies, beyond the upfront costs of developing the program and infrastructure to conduct transactions, mobile payment technology is a consumer-friendly way to keep ongoing and variable costs low. With consumers more adept and willing to shop online, more integrated shopping ecosystems are developing.

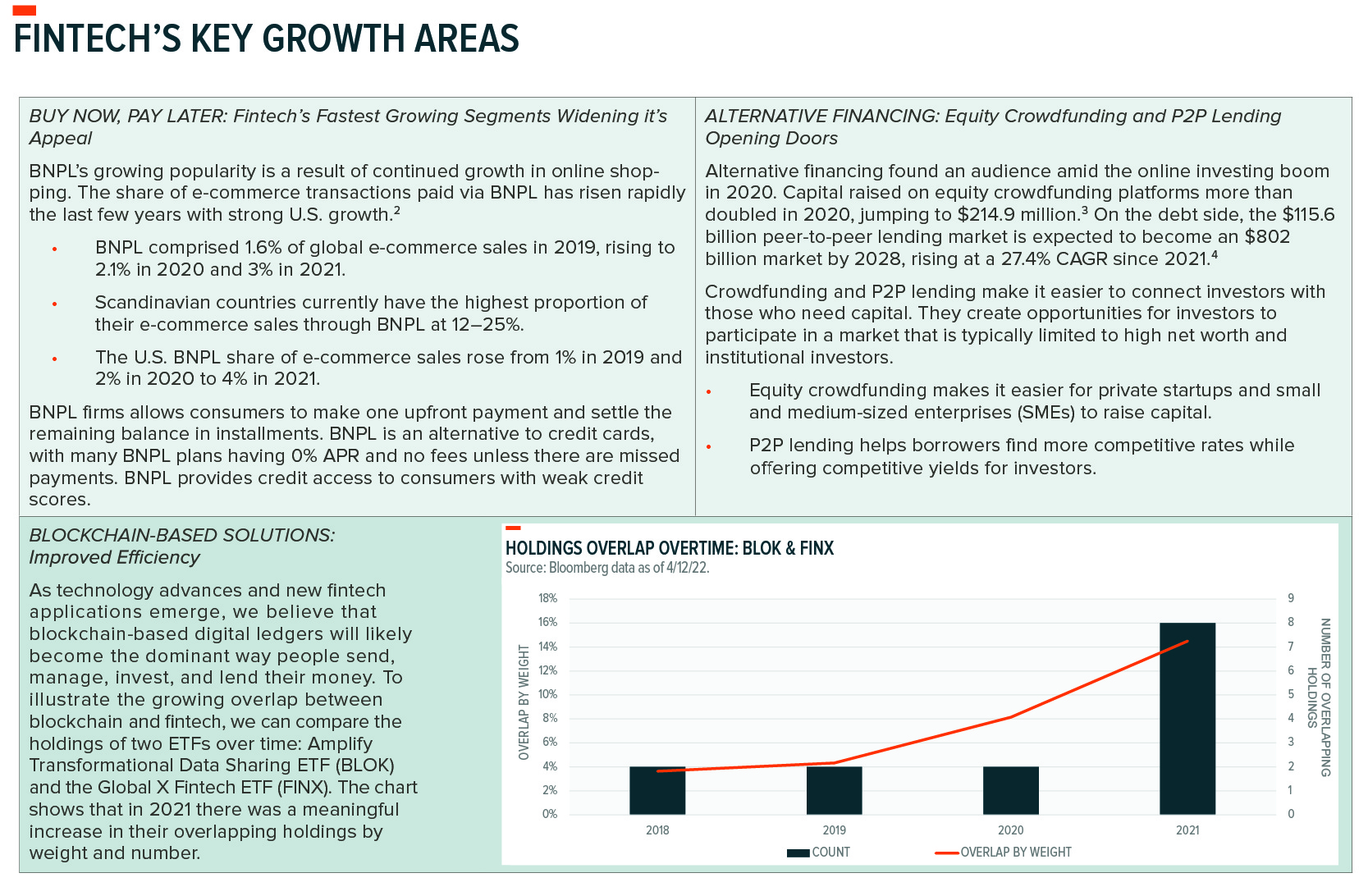

Emerging segments like BNPL, cloud banking, blockchain-based solutions, and alternative financing solutions like equity crowdfunding and peer-to-peer (P2P) lending will likely be part of the next stage of the industry’s evolution.

Fintech: Growing adoption across generations and geographies

Fintech adoption remains most prevalent among younger generations. Ninety-five percent of U.S. millennials say that they use fintech applications. Adoption of new technology typically begins with younger generations, but older generations are increasingly adept with these technologies as well. Baby Boomers are the fastest growing demographic for Fintech, with use among individuals 56 and older doubling year-on-year to 79% in 2021.5

The global adoption rate of fintech solutions reached 64% in 2019.6 Particularly exciting for the industry is its growth potential in emerging markets (EMs) and economies with limited traditional financial infrastructure and unbanked populations. China and India have the widest adoption thus far, reaching 87% in 2019.7 Innovations in mobile payments, online banking, and alternative lending platforms bring financial services to previously unbanked and underserved populations. Without existing infrastructure in place, like traditional bank branches and credit cards, EMs can adopt the latest technology without forcing an old business model into obsolescence.

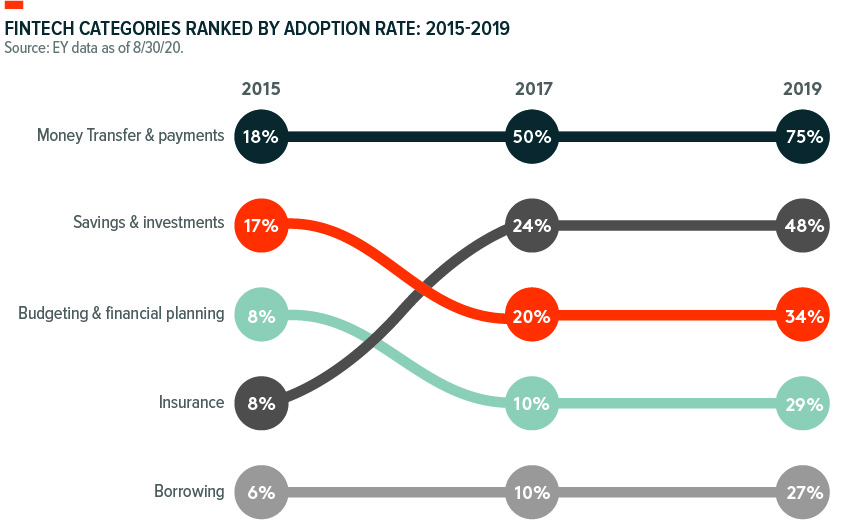

The chart shows the trend in fintech adoption globally across different traditional financial services prior to the pandemic. Since the pandemic, adoption has increased across categories.

Blockchain: A new avenue for growth

In its most basic sense, a blockchain is a type of database focused on recording and maintaining data. Its unique properties stem from its decentralized approach. In a centralized system, a singular authority controls all aspects of transaction verification and documentation. With blockchain’s decentralized approach, data is recorded in “blocks” on a digital ledger. Participants, called nodes, are the computers and devices connected to the network that distribute and validate the ledger on a peer-to-peer (P2P) network. While anyone can create data on public blockchains by creating a new block and chaining it to a previous block, the consensus-based approach to validation means nobody can edit or falsify the data after it’s received a sufficient number of block confirmations. The result is a structure that generates trust without the need for a third party.

It’s conceivable that blockchain networks eventually become embedded in the financial ecosystem because of this key feature: participants don’t need to trust a government to back a currency or to responsibly manage the money supply. For the developed world, the significance of this feature may be difficult to understand, though recent economic crises may facilitate comprehension. Trusted financial institutions operating within strong regulatory frameworks that protect investors is not a privilege enjoyed equally around the globe.

The blockchain network provides a mechanism for financial inclusion for unbanked and underbanked populations, particularly in countries struggling with political instability, corruption, or severe inflation. The onset of the war in Ukraine illustrated the benefits of a decentralized form of currency, as people with cryptocurrency wallets continued to have access to currency.

A February 2021 survey by market and consumer data firm Statista indicated that the top 10 countries with the highest frequency of cryptocurrency usage among their populace were all emerging market countries. Nigeria led the way with 32% of respondents indicating that they use bitcoin or cryptocurrency more broadly, followed by Vietnam at 21% and the Philippines at 20%.8 The U.S. reported an estimated 16% of adults own cryptocurrency.9 The average age of these potential buyers is 44, which suggests digital assets continue to gain acceptance in the mass market.10

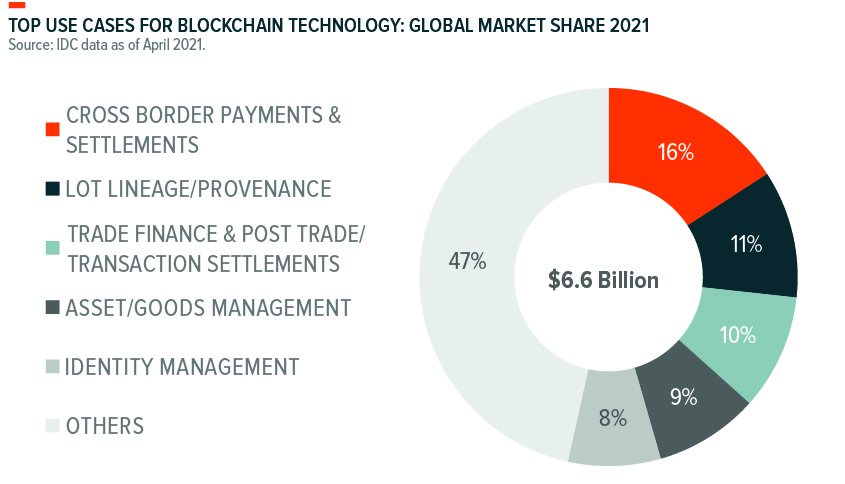

Broad use cases for blockchain

In the short term, blockchain use cases will likely cluster in the banking industry, where financial institutions use the technology to facilitate cross-border payments and transaction settlement. Banking-related use cases accounted for nearly 30% of global blockchain spending in 2021.11 Beyond financial institutions, applications of blockchain technology are vast, touching supply chains, healthcare tracking, and smart contracts.

Blockchain’s secure ledger creates efficiencies for firms keeping tabs on their international supply chains. For example, firms can easily identify and track tainted or tampered products. Health records can be stored in a blockchain by using a unique patient identifier, allowing patients to access their own records and authorize health service providers to access their information in real time. Smart contracts can increase the efficiency of transactions because there is no paperwork involved and no time spent reconciling errors. Secured by encryption mechanisms, participants can trust smart contracts because they’re decentralized and transparent.

Visualizing the Market

Risk to the Fintech Theme

Consumer risks: Unsuitable products, scams, and market declines

Fintech platforms commonly remove the middlemen from transactions, democratizing finance. However, there are downsides. In traditional finance, industry employees are commonly held to a fiduciary standard, bound to act in the best interests of their clients. Before they make recommendations, they screen investment opportunities and products for individual customer suitability. Fintech platforms automate much of this work, simplifying suitability and risk tolerance conversations to questionnaires and prescreening options for a wide range of clients before allowing users to make their own decisions. Easy access to risky or complex financial products can lead to harm if investors lack the knowledge or experience to assess them properly.

Consumer risk is also rife within the cryptocurrency market. Scams, defunct coins, and volatility are common, making the space a metaphorical minefield for investors. In 2021 alone, $7.8 billion in value was scammed, typically via rug pulls, where “developers” build what appear to be legitimate cryptocurrency projects before taking investors’ money and disappearing.20

Even legitimate tokens bear risk. Data from token tracking website Coinopsy shows that 2,399 coins are now dead.22 Investors need to be cautious in the crypto space, as regulation remains light and illicit activity common.

Cryptocurrency bans, regulation, and federal centralization

China and eight other nations curbed their crypto markets considerably.23 China enforced crypto restrictions in stages, first prohibiting financial institutions from engaging in any crypto transactions, then banning all domestic crypto mining activity, and finally declaring all financial transactions involving cryptocurrencies illegal. Previously, China was the undisputed world leader in bitcoin-related activities. The country’s three largest exchanges accounted for over 45% of global market transactions, and Chinese miners controlled about 65% of the Bitcoin network’s collective hash rate.24,25 Market reactions to each successive restriction were initially negative, indicating the risk to investors should other nations implement similar policies.

A maximum regulation scenario would likely entail governments co-opting cryptocurrencies, as central banks will be hard pressed to relinquish the centralized control they currently have over currencies. Instead, they would issue Central Bank Digital Currencies (CBDC) that modernize fiat for the digital age. China implemented a digital yuan, which as of this writing has been used to settle over $13.78 billion in transactions.26

Currently, the Federal Reserve (“Fed”) has no concrete plans to implement a CBDC, but it has studied the feasibility of such a currency. Partnering with MIT, the Fed worked to “build and test a hypothetical digital currency oriented to central bank uses.”27 These tokens would be backed by real dollars, which would clearly define their value. Crypto enthusiasts would view this hybrid model as blasphemy because it splits trust between governments and cryptographic proofs, but it would likely view the concept more approachable to the average consumer. A successful CBDC implementation would likely draw demand away from traditional crypto assets, decreasing their value.

Digital asset blockchains require significant energy

The majority of today’s blockchains, including Bitcoin’s, use Proof of Work (PoW) cryptographic proofs to integrate new information and transactions into the chain. This approach relies on competing miners expending significant amounts of energy to solve computationally-intensive math problems. Miners that guess correctly are compensated for their time, processing power, and energy spent with a block reward and transaction fee. Currently, the Bitcoin network consumes an estimated 204.5 terawatt hours (TWh) of electricity a year to function, comparable to the annual power consumption of Thailand. In the process, the Bitcoin network releases 114.06 million tons of CO2 in the environment, comparable to the average annual greenhouse emissions of more than 20 million gas powered passenger vehicles.28,29

We expect governments to eventually place limitations on mining as part of the global effort to reduce carbon emissions. Such a change would likely force cryptocurrencies to adapt, or risk declining adoption. An alternative cryptographic proof gaining favor is Proof of Stake (PoS), which allows blockchain participants to validate new blocks based on their ownership stake in the network. With a validator selected at random and no proof to solve, energy consumption plumets.

Thematic Intersection with Fintech and Blockchain

Fintech and Blockchain

A key advantage of fintech platforms compared to their more classically minded financial competitors is their ability and willingness to integrate new approaches at scale. Fintech platforms can shift their business models over time as new technologies are adopted. The fusion of blockchain and fintech to form decentralized finance (DeFi) is a perfect example.

Together fintech and blockchain leapfrog middleman and bring much needed competition to the banking and finance space. Blockchain implementations can produce substantial savings, up to a 70% cost reduction on financial reporting, and up to 50% across compliance, onboarding, and operations.31

Fintech and Internet of Things (IoT)

Fintech platforms and Internet of Things technologies can transform everyday services. For example, insurance underwriters typically operate with incomplete information, which increases the cost of property and casualty insurance policies. Historically, driving record, demographics, and vehicle information determine the price of their auto insurance. While these data points provide a reasonably accurate estimation of future insurance risk, they rely on risk bucketing and generalizations.

However, by using telematic sensors to track GPS and onboard diagnostic information such as speed, acceleration, and breaking behaviors, insurers can form true-to-life risk models based on individualized driver behavior. Privacy focused individuals may view such tracking as invasive, but telematic data collection gives consumers the ability to control their premium costs by incentivizing the adoption of safer driving habits. This integration can increase affordability for lower-risk drivers and coach more aggressive drivers to reduce their incidence of risky behaviors. Such incentives have resulted in accident rate reductions of 10–40%.32

Sensor data can also assist in fault determination, demonstrating directly whether a driver caused an accident or was the victim of one. For underwriters, that means fewer claims, lower administrative costs, and faster resolutions.

Fintech and Cloud Computing

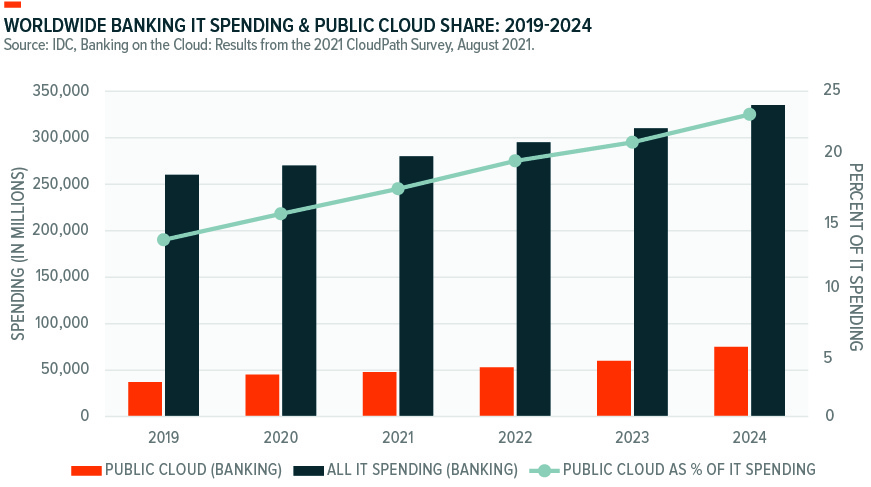

Fintech is viewed as a disruptor of traditional financial services, a well-deserved reputation, but one that doesn’t tell the whole story. Fintech firms also offer technologies that help traditional financial services companies enhance their services. Cloud banking is one such growing vertical. Globally, banking industry IT cloud spending is forecast to increase at a CAGR of 16.2% between 2019 and 2024, increasing to roughly 25% of IT budgets.33

Cloud technology can streamline previously cumbersome processes for banks, such as onboarding new clients, opening accounts, and managing regulatory compliance. Commercial bankers using cloud solutions can see reductions in underwriting times by as much as 81%.34 Other cloud-based approaches can help banks respond to shifting market trends and bring new products to the market up to 16 times faster than the average.35 Importantly, these solutions aren’t just more efficient operationally, they also shift expenditures away from significant upfront investments in IT infrastructure to lower-cost, subscription-based software-as-a-service (SaaS) models.

Capital One Bank is a leader in cloud adoption, having shuttered all their internally operated data centers in 2020 to run exclusively on the AWS cloud. Over 80% of their 2,000 applications and software tools were rebuilt to run on the cloud from the ground up, and the migration is already paying dividends. Application updates are much more frequent, improving from a quarterly or monthly cadence to multiple times a day. Disaster recovery tests show downtime falling by up to 70%. These efficiencies and performance improvements from the cloud environment can differentiate the bank from its peers and serve as a model for the advantages of a cloud banking transformation.36

Blockchain and Video Games

Play-to-earn is a new frontier for gaming and non-fungible tokens (NFTs). According to a report on NFT tracking site DappRadar, more than 1 million digital wallets connected to decentralized gaming apps per day in October 2021, representing 55% of the blockchain industry’s overall activity.37 Players can earn NFTs from a variety of blockchain games. In Q3 2021, game NFTs accounted for more than 20% of the $10.6 billion in NFT volumes.38 A key differentiator between blockchain games and other traditional games is the ownership of playable items, and therefore the ability to sell, trade, use, and lend these tokens.

Fintech and Blockchain in a Portfolio Context

Fintech will continue to make financial services more digital and scalable. This transformation is well underway, but it’s one that still has significant room to run globally, particularly in EM, where demand for broader access to financial services is generations in the making. In the U.S., consumers increasingly want and expect digital banking experiences, encouraging traditional financial services firms to pivot to keep up with Fintech trailblazers.

Fintech’s digital payment revolution has reached the point where GICS sector changes are being reviewed. Transaction and payment processing companies are currently classified as a part of the Information Technology sector. In the proposed GICS classification, which is due to be implemented in Q1 2023, these companies will be reclassified as Financials Services.39 Based on current market capitalization, should this sector change occur, the largest payment processing companies will be among the largest companies in the Financial Services sector.40

For investors, a risk is not having exposure to the continued adoption and integration of this innovative sector. Gaining exposure through an ETF provides access to a group of companies that continue to disrupt how people interact with their finances.

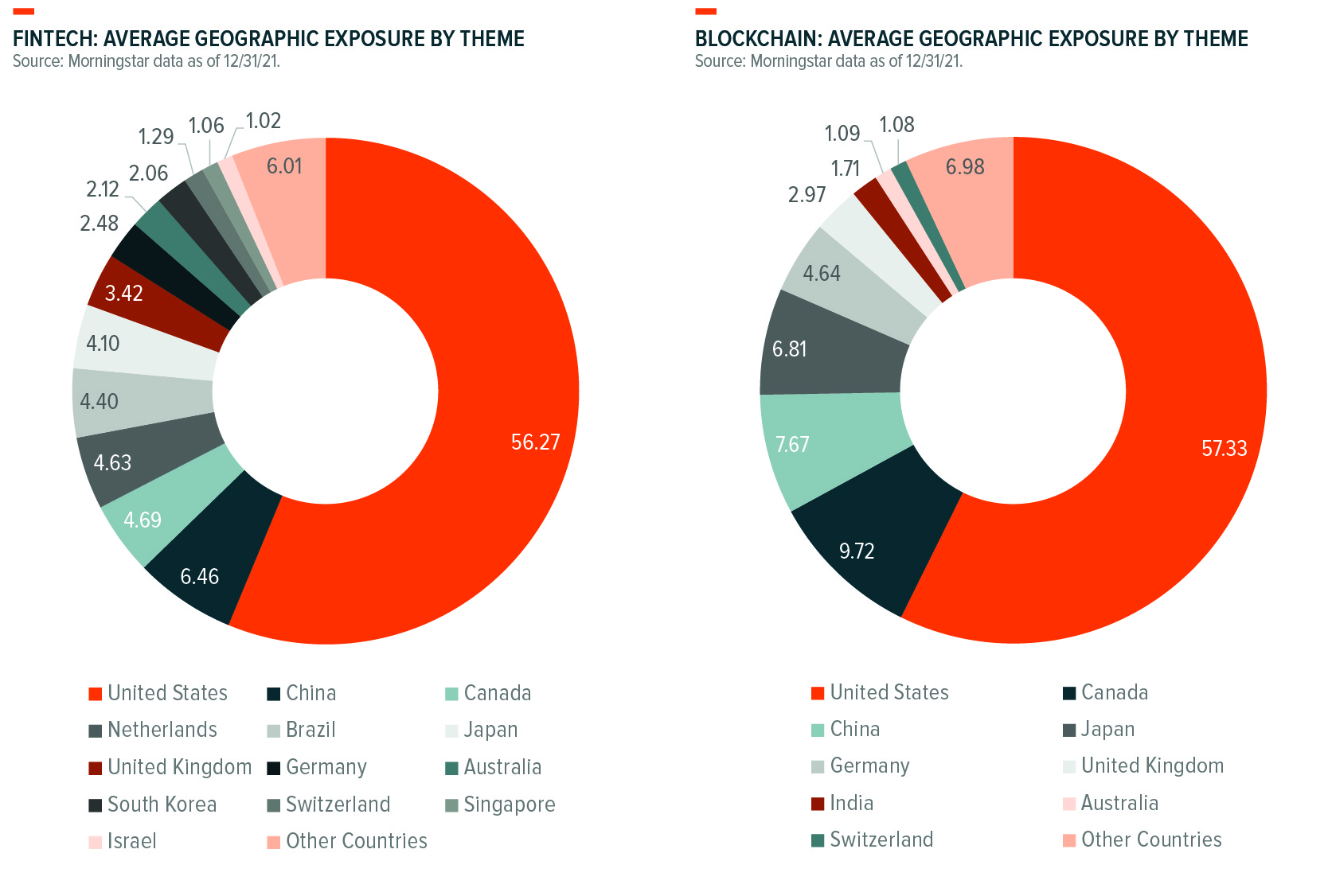

The companies operating in the Fintech space are global and positioned to benefit as thematic adoption increases across the world. The charts, to the right, break down the geographic exposure of the largest Fintech thematic ETF products. We believe that there is ample innovation occurring outside of the U.S. and that limiting exposure to the U.S. may exclude key players, to the detriment of investors over the long term.

Note: Includes the five broad Fintech ETFs and the largest five blockchain ETFs according to our thematic classification. All Thematic ETFs weighted the same.

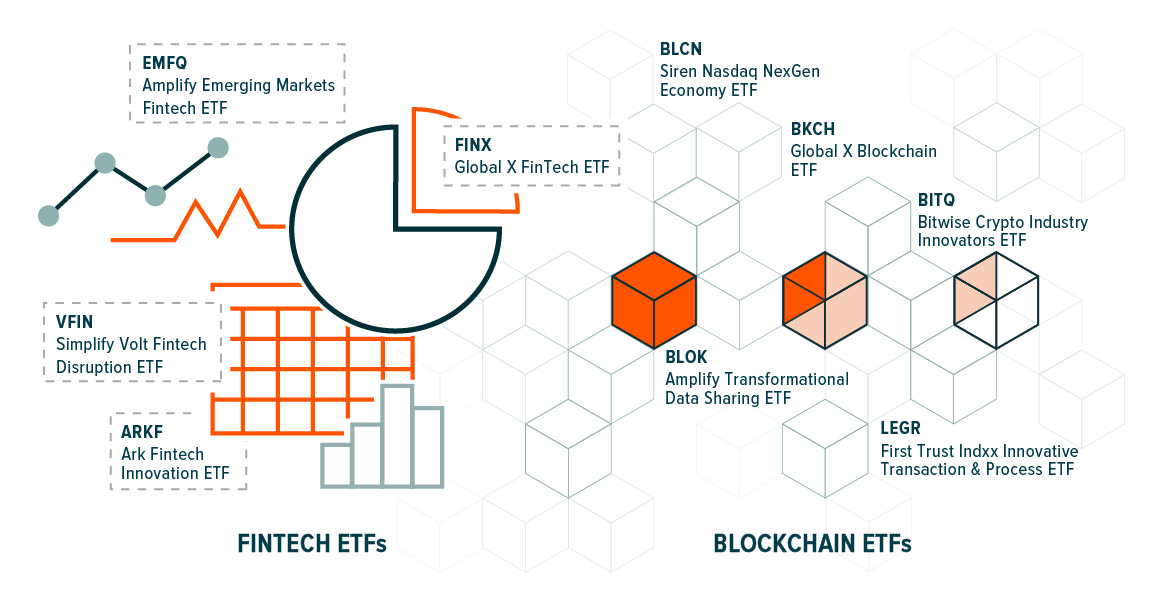

How To Access Fintech

The graphic below identifies the largest U.S. listed ETFs that provide direct exposure to the Fintech theme through FinTech and Blockchain technology.

Read the next section of the Thematic Investing Whitepaper on the Climate Change theme.