The current investment landscape presents no shortage of challenges for investors, and we expect current levels of market volatility to linger. Following over a decade of low inflation, the U.S. Consumer Price Index (CPI) is now at its highest levels in four decades, and the Federal Reserve (Fed) is aggressively tightening its monetary policy. Despite the angst in the markets, we believe investors have opportunities, outside of traditional defensive approaches. In this piece, we discuss how options-based strategies may help generate income, manage risk, or both, depending on the objective.

Key Takeaways

- In this challenging macroeconomic environment, options-based strategies may provide investors with degrees of insulation. Protective puts used in option strategies can mitigate equity drawdowns by capping the loss of the asset(s) underlying the options, creating alpha compared to just owning the asset(s).

- In a rising rate environment, options-based strategies like covered calls may be able to attract higher option premiums due to greater levels of implied volatility priced into the market.

- For investors looking to diversify, hedge, or generate income, options strategies that use either covered calls and/or protective puts may be useful strategies in anticipation of rates staying elevated for longer.

Investing in a Flattening Yield Curve & Rising-Rate Environment

Investors face a challenging backdrop with multiple factors driving elevated market volatility. Equity and fixed income markets are under pressure due to rising rates and the reversal of longstanding dovish monetary policies amid surging inflation. Currently, markets are pricing the federal funds rate to be 3.50–3.75% by the end of 2022, through a combination of 25 bp, 50 bps and 75 bps hikes and potentially even 100 bps.1

Rate hikes pressured equities through the first half of the year as the Fed, and central banks around the world, tried to rein in inflation with increasingly hawkish stances. However, most of the market decline came from declining price to earnings ratios rather than deteriorating fundamentals. Rising volatility stemming from increasing rates is a challenge for equity and high yield fixed income investors because these assets have negative correlation to volatility.

While the forward 12-month S&P earnings growth was up 6.7%, the forward price-to-earnings ratio dropped from 21.4 at the beginning of the year to 17.5.2

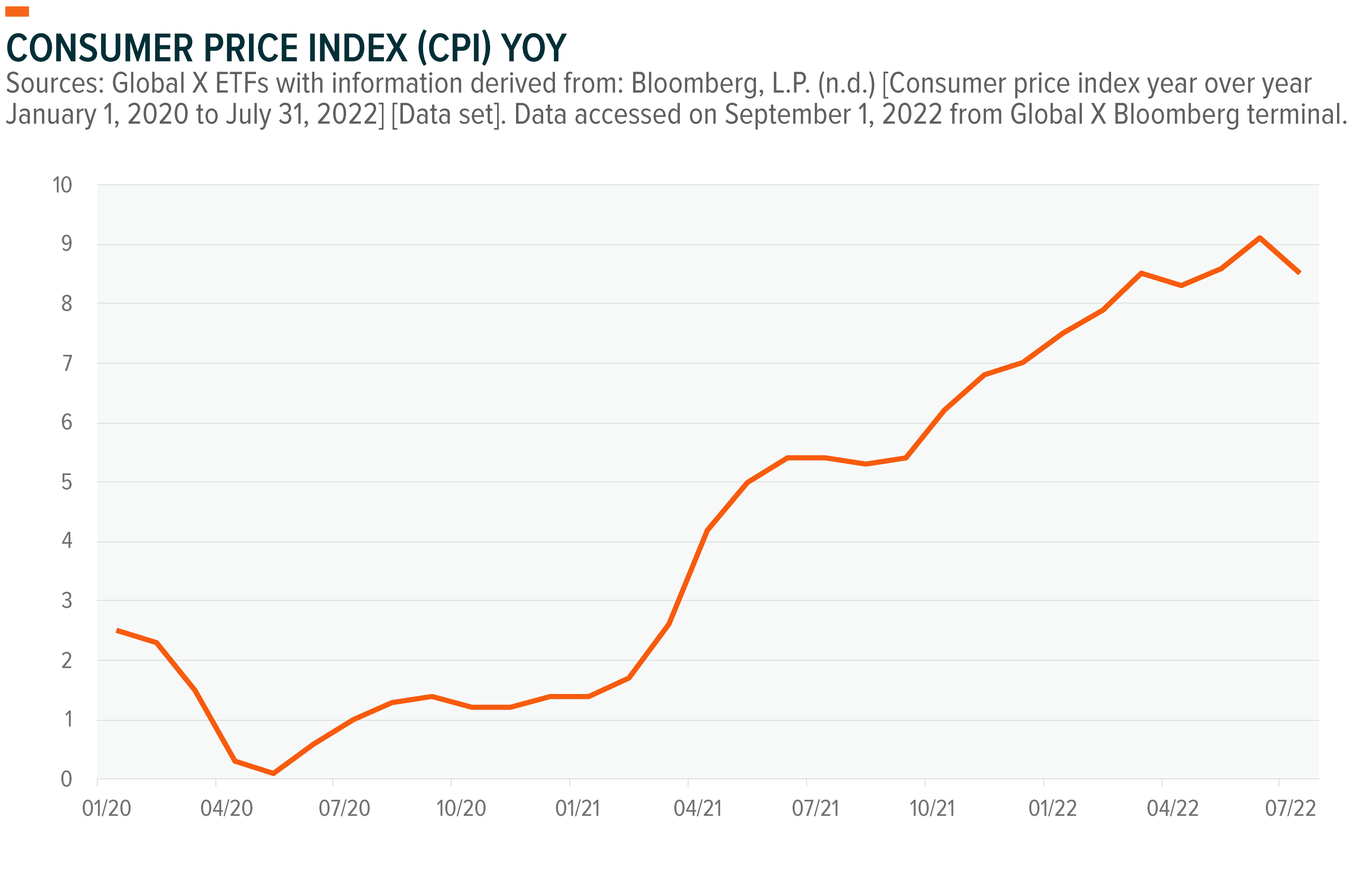

While low following the Global Financial Crisis (GFC), inflation now appears set to be persistently higher for longer. Inflation prints remain elevated, with June’s Consumer Price Index (CPI) numbers coming in at 9.1% year-over year (YoY), its highest reading since December 1981. For investors looking to counter this, a more nuanced approach to this market may be needed.3

In the Current Macro Environment, Options Strategies May Provide Measures of Protection and Income

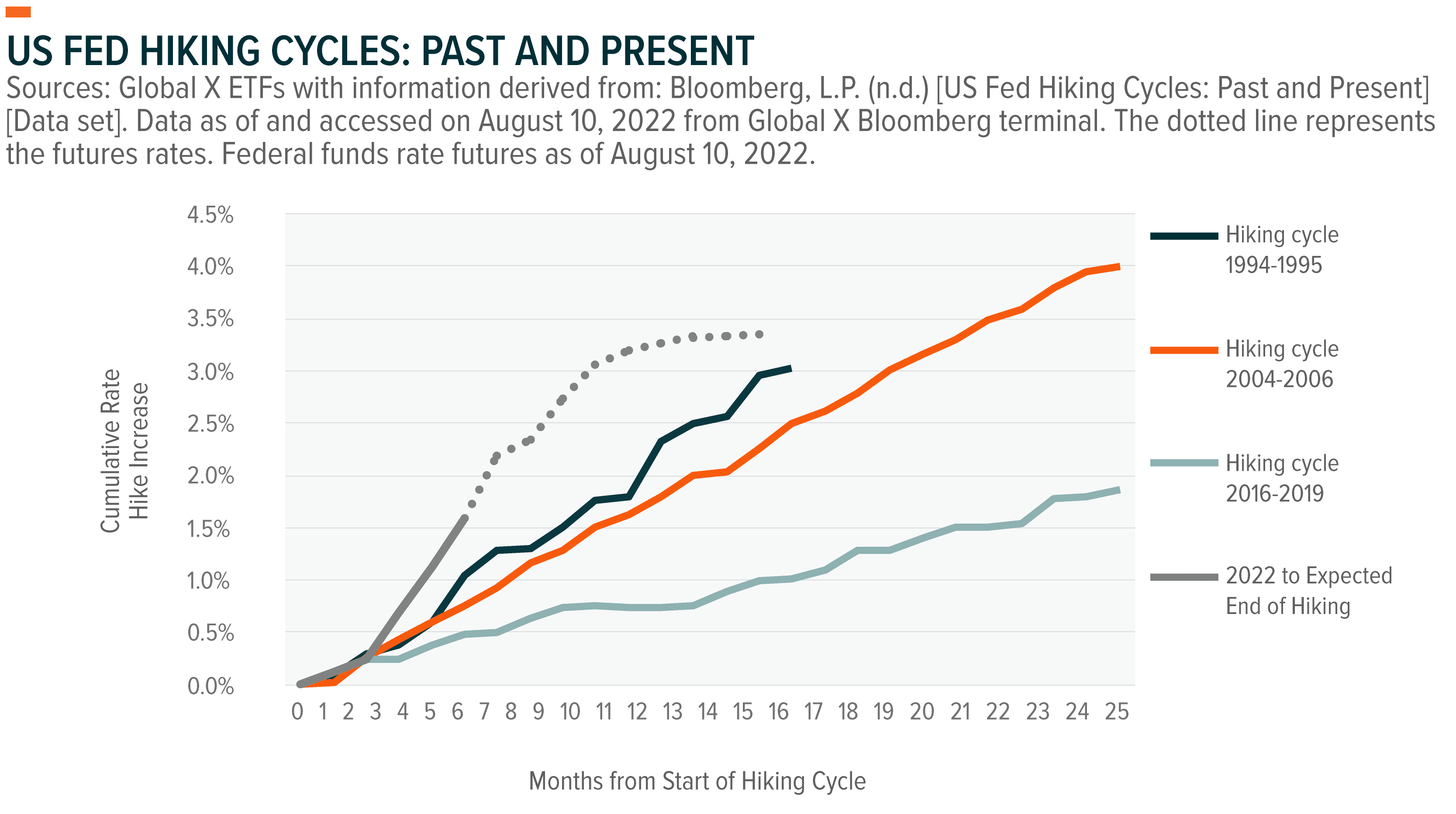

The convergence of multiple headwinds this year is changing the investing landscape. Where investors go for protection against volatility or where they look to generate income may be different compared to the past. However, we believe that options-based strategies, which can be categorized in three main buckets: income, total return and volatility mitigation strategies, may offer compelling opportunities to investors. As we can see below, historically when the Fed engages in a rate hiking cycle, rates tend to rise gradually over time. In the current hiking cycle, we can see the market implied rate increases and end of hiking based on the Federal Funds futures rates in the graph below.

Options Strategies Focused on Income

Covered call strategies may help investors generate diversified income or balance objectives between growth and income, particularly in a rising rate environment like the one we’re seeing today. Covered calls can essentially monetize the volatility inherent in an investor’s equity portfolio depending on the level of equity upside they’re willing to give up. Covered call strategies write call options on an equity or basket of equities while continuing to hold these securities. Covered calls strategies limit upside participation but collect premiums from option-writing. These strategies also diversify an investor’s sources of return from just equities and bonds, which historically struggle in rising rate environments.

Diversification across asset classes is important because simple diversification, such as the 60/40 portfolio split across equities and fixed income, may not meet investors’ specific income and growth needs. While diversification does not ensure a profit or guarantee against a loss, investors may need to consider further sources of diversification through low correlation between asset classes and strategies.

Income-oriented investors tend to look to certain pockets of the market for higher yields. This concentration can lead to an overexposure to a handful of specific sectors, which can help boost distributions but lead to increased sector or company specific risks.

As there is a relative dearth of higher-yielding strategies and asset classes currently, concentration risk within portfolios can also be a concern. Government bond yields increased in the first half of 2022 but yields still remain low across the fixed income landscape, which may force investors to take greater risks to achieve their income objectives. In addition, fixed income assets like government bonds offer higher duration risk, adversely affecting investors as rates rise. Equity-based covered call strategies don’t come with this type of traditional duration risk and allow investors to stay invested in the market. The positive historical correlation of volatility to options premiums also may make it more appealing to income investors, whereas equities and fixed income may see their income potential more at risk in higher volatility environments.

Options Strategies for Potential Total Return and Downside Protection

For many investors, such as retirees or individuals on fixed income levels, protecting principal during market selloffs can be just as important as income generation. Covered call strategies can add potential distribution dynamic to a portfolio, but one drawback for more risk-averse investors is they offer limited downside protection.

Options strategies focused on total return and downside protection can seek to address this issue for risk-sensitive investors through methods like combining selling a covered call with buying a protective put. This helps balance risk, while potentially offsetting the costs of buying the put options. As the put options become further in the money, the delta on the options increases to be closer the value of +1 or -1 (if selling or buying the put, respectively). As the delta moves closer to +1 or -1, the investor should expect a greater change in the option price when the underlying asset moves. Depending on the level of risk an investor is willing to take and their desire for income, these strategies can even be structured in an effort to generate net premiums by having the premium received from the sale of the call option outweigh the cost of the put premium.

Options Strategies That Can Mitigate Volatility

Investors who want to limit volatility within a certain range-bound return profile in their portfolios may want to consider adding options-based collar strategies to their portfolios. When implemented appropriately, these hedging strategies can help to mitigate uncertainty and limit losses without significantly reducing the potential rate of return. For investors focused on extreme events, strategies focused on left tail risk prevention can also help investors mitigate downside risk.

Options Strategies Breakdown

Options strategies offer investors flexibility and the ability to shift market factor exposure, which can be particularly attractive during periods of macroeconomic uncertainty and market volatility. They can also offer a range of potential outcomes for investors, the mechanics of which we break down here.

At-The-Money (ATM) Covered Call Strategies: Premium Potential with Reduced Volatility

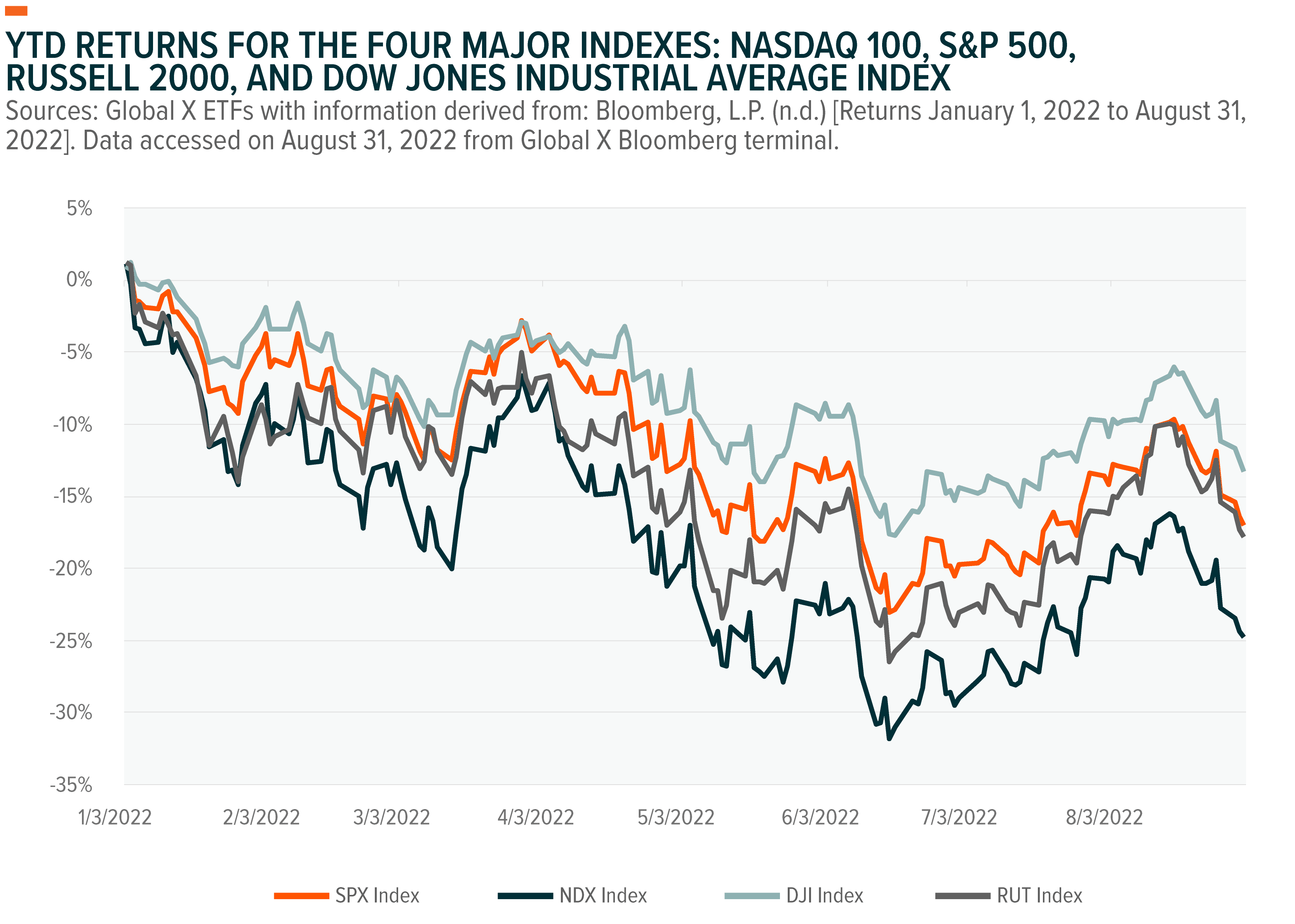

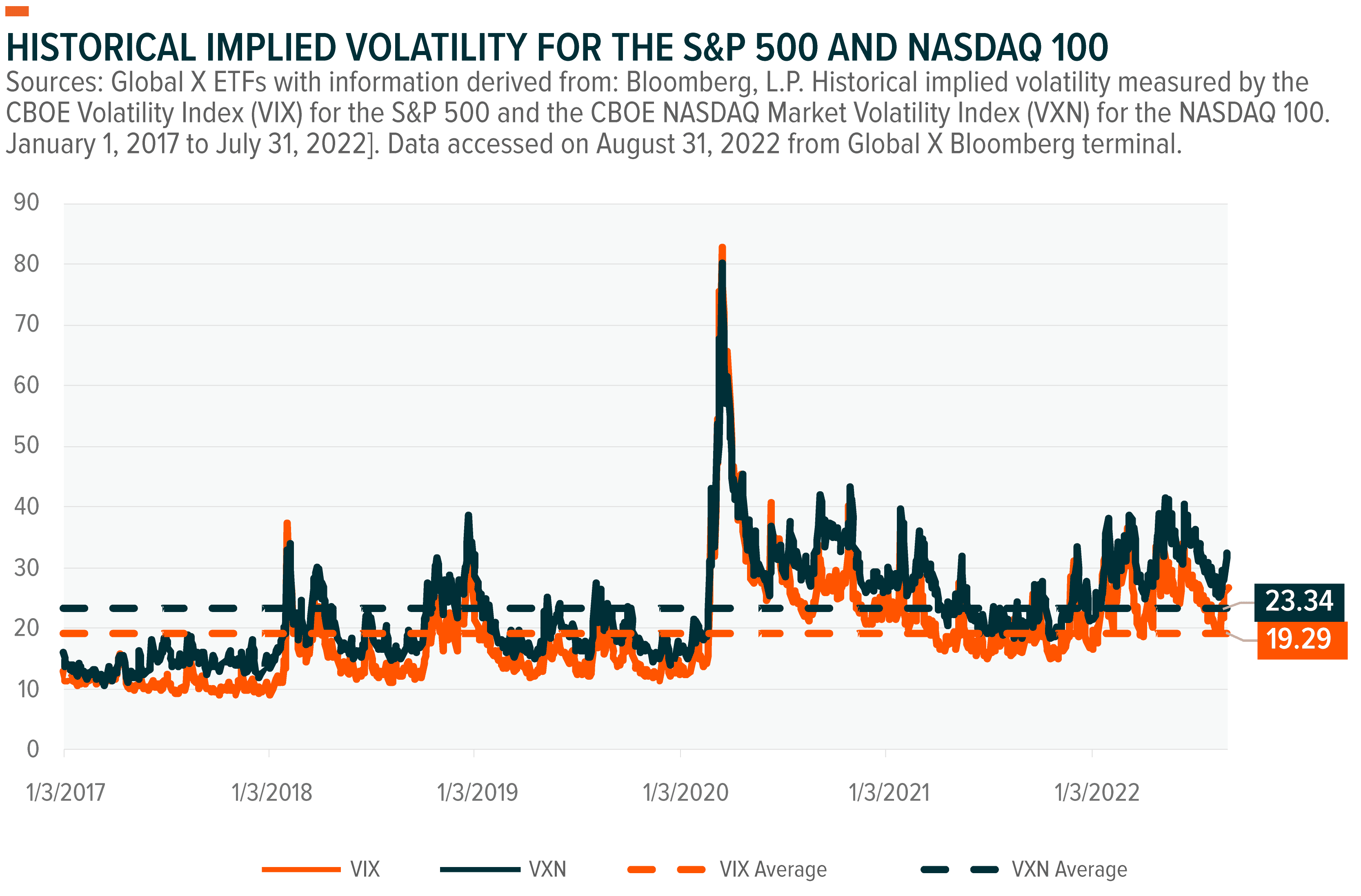

Covered call strategies can be a complement to equity and fixed income exposures. Covered calls written ATM can be appealing to investors seeking income with the potential for reduced volatility in their equity exposure. For example, historically the Nasdaq 100 is more volatile than the S&P 500 due to overweight exposure to growth sectors like Technology and Communication Services, but the S&P 500 recently has been getting more volatile. The ability to collect premiums can potentially mitigate volatility in down markets.

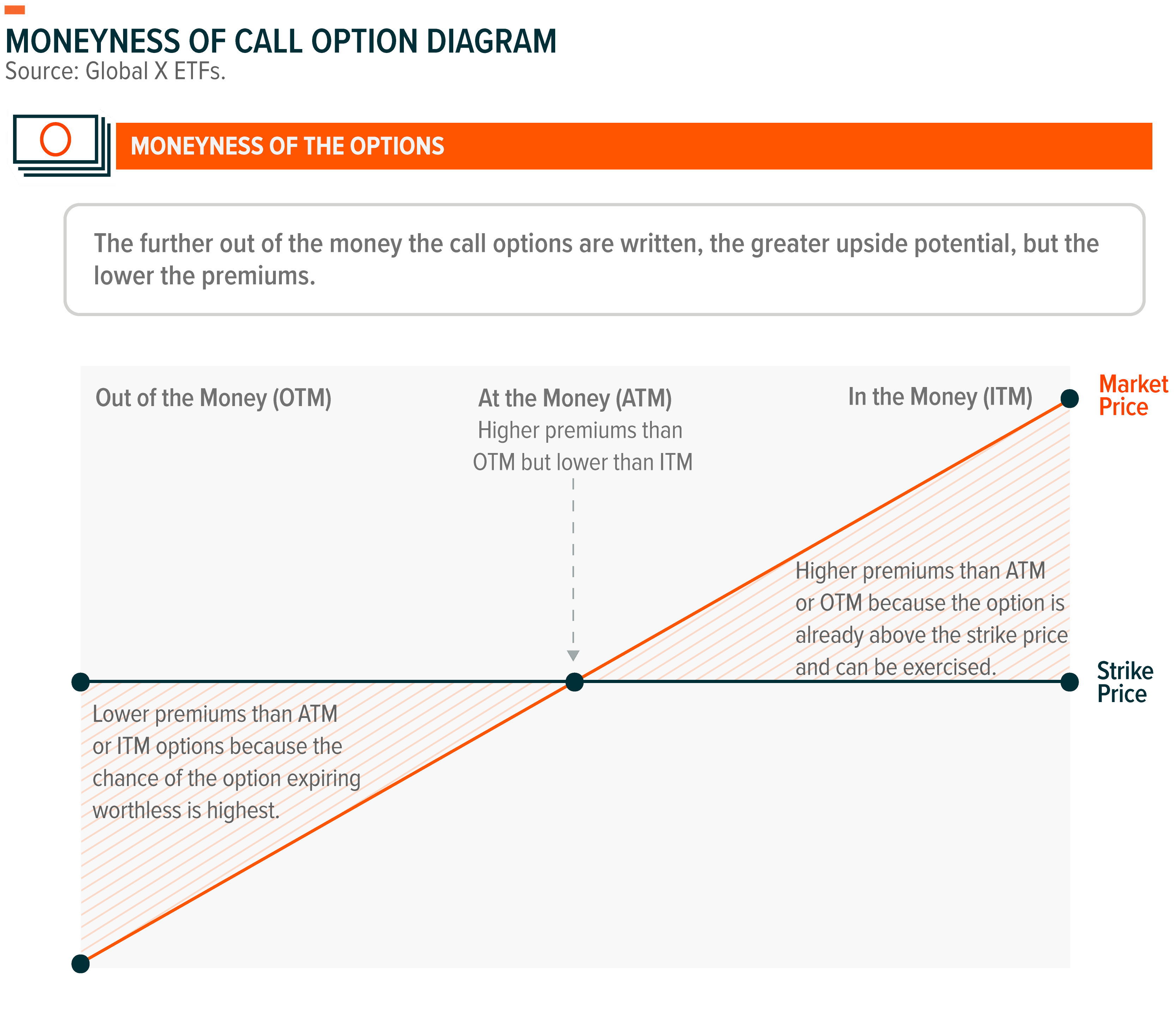

Covered call strategies consist of owning one or more stocks and selling a call option on that same stock or stocks. Covered call strategies can be 100% covered which means that the strategy is writing calls on 100% of the portfolio. A strategy could be implemented with less coverage. For example, a strategy can write calls on 50% on the portfolio. Such a strategy would receive half of the premium but participate in half the upside of the underlying securities.

What the investor can expect in terms of premiums received depends on how much notional exposure the call option is written, and the moneyness of where it’s written—at the money (ATM), out of the money (OTM), or in the money (ITM). With a covered call strategy, an investor can get a mix of premiums from the call option written and equity market participation for the underlying securities.

Covered call strategies written ATM forfeit the upside potential in exchange for the premiums received from writing the call option. As option premiums tend to rise in volatile markets, covered call strategies tend to perform better in such markets than in major bull or bear markets. For example, with a call option written ATM to fully cover the underlying securities exposure, we would expect it to outperform the underlying exposure in flat- and down-market scenarios, but underperform in up markets.

In periods of higher volatility, options strategies like covered calls tend to be better positioned because options premiums received are positively correlated to market volatility. Global X manages four covered call funds: Global X Nasdaq 100 Covered Call ETF (QYLD), Global X S&P 500 Covered Call ETF (XYLD), Global X Russell 2000 Covered Call ETF (RYLD), and Global X Dow 30 Covered Call ETF (DJIA). These funds write one-month call options that are rolled monthly. The covered calls encompass 100% of the notional value of the portfolio and the funds look to prioritize the premium component by writing the call options at-the-money (ATM) rather than out-of-the-money (OTM). These funds look to perform distributions on a monthly basis.

RYLD, which is writing covered calls on the small cap Russell 2000 Index, is a case study for when ATM covered call strategies may make sense for investors. After the COVID-19 pandemic, there have been larger drawdowns and a faster recovery for the Russell 2000 compared to the other reference indices, largely due to the volatility present in that index. In the one-year period from September 30, 2021 through September 30, 2022, RYLD was down only 24.48% compared to -25.95% on the Russell 2000 Index.4

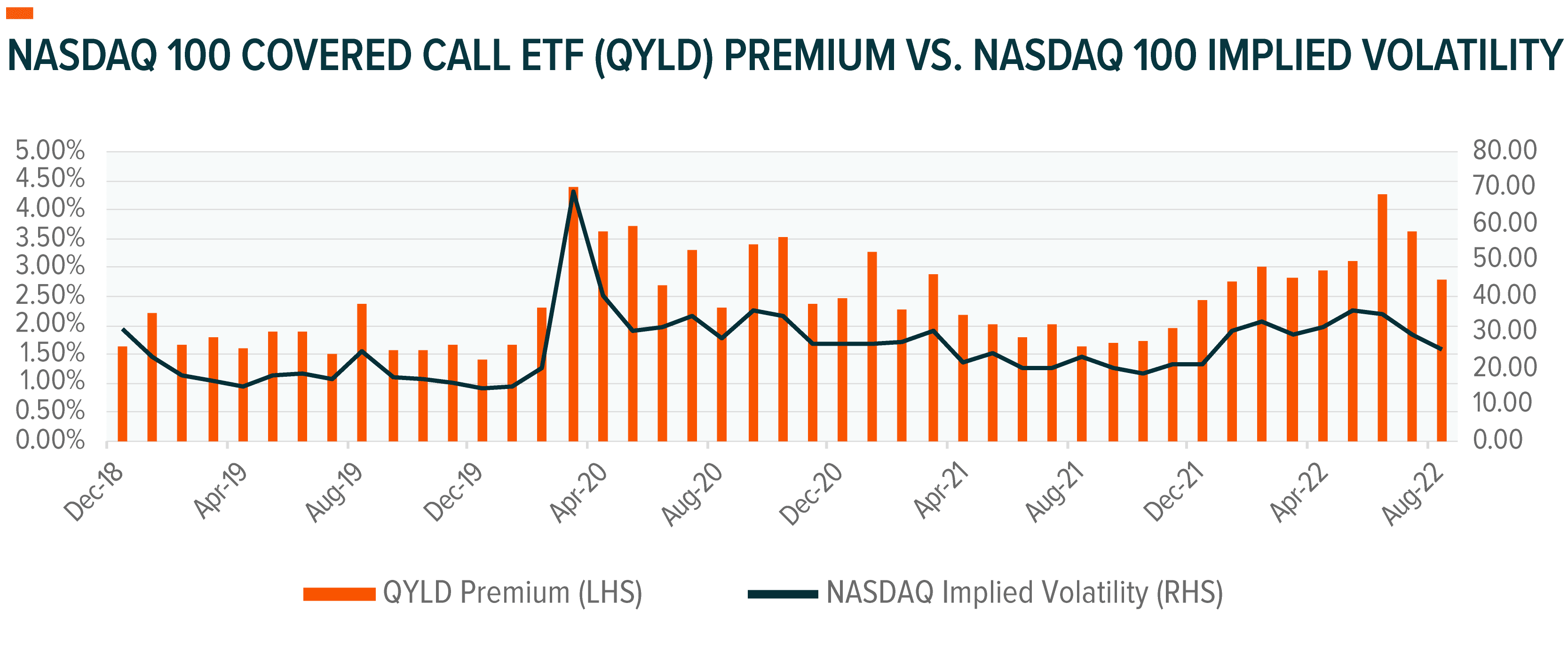

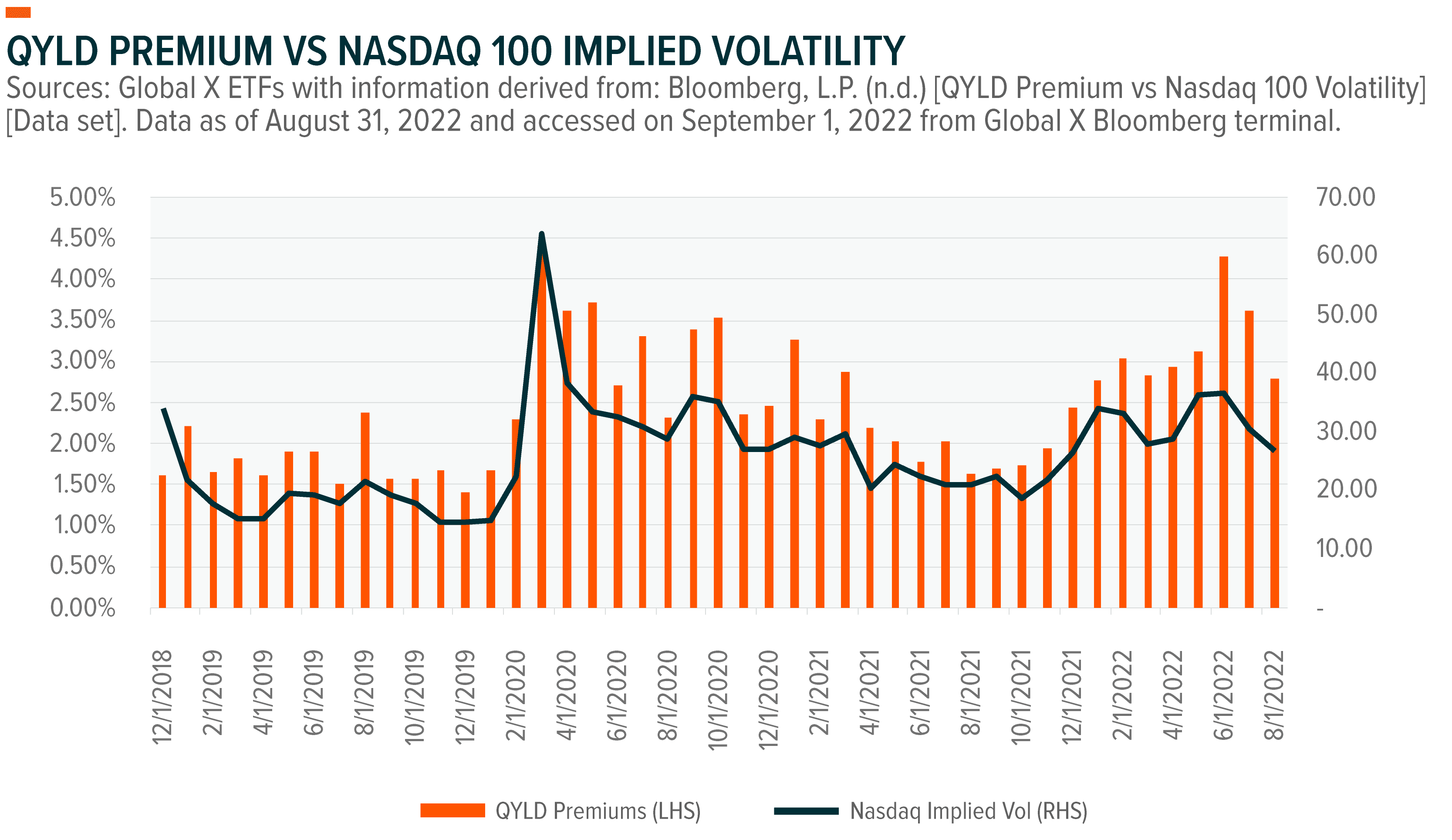

In addition to the Russell 2000, the higher volatility experienced by the NASDAQ and S&P 500 indexes has been supportive of the premiums earned by the Global X ETFs deploying covered call strategies on those indexes. We can also see with QYLD for example, that premiums received have been highly correlated to levels of implied volatility.

Covered calls can be used both strategically and tactically. These strategies may be helpful in market environments where income is hard to find. For example, traditional income-generating investments like bonds are falling short of many investor’s needs this year as they face increased duration risk with rising yields in the market from the actions of the Federal Reserve. The Bloomberg Global Investment Grade Corporate Bond Index price is down about 10.75% year to date as of 8/31/2022. But covered call strategies such as QYLD and XYLD may produce a premium component while diversifying the source of risk in a portfolio as the calls are written on diversified indices such as the Nasdaq 100 or the S&P 500 as opposed to single company securities.

Covered call strategies can be appropriate for tactical portfolios as well. In an up market, a covered call strategy will likely underperform the underlying because it keeps the option premium but forfeits the upside. In a flat market, the strategy will likely outperform as the strategy keeps the premium from selling the call option. In a down market, the strategy may also outperform because it keeps the premium received from selling the call option, which may offset some or all of the underlying market’s decline.

Covered Call and Growth Strategies: For Income and Upside Potential

A covered call and growth strategy can be an equity sleeve replacement or complement for bullish investors seeking a balance between income and upside potential. The main differences with these strategies compared to the ones described above is the level of equity upside retained and amount of premium received. Covered call and growth strategies can be utilized by allowing for equity upside to be retained by only writing call options on a partial amount of the portfolio, for example 50%.

In the current rising rate environment, covered call and growth strategies seek to pursue option premiums while still allowing for growth potential in the uncovered 50% of the portfolio. This strategy may appeal to investors who want to live off their savings for 20–30 years and may want current income and growth to combat inflation. More tactically, an investor may have a more bullish view of the markets and shift from a fully covered strategy to a 50% covered strategy in an effort to capture more upside potential in the near term. QYLD and XYLD are 100% covered whereas the Global X Nasdaq 100 Covered Call & Growth ETF (QYLG) and Global X S&P 500 Covered Call & Growth ETF (XYLG) are 50% Covered.

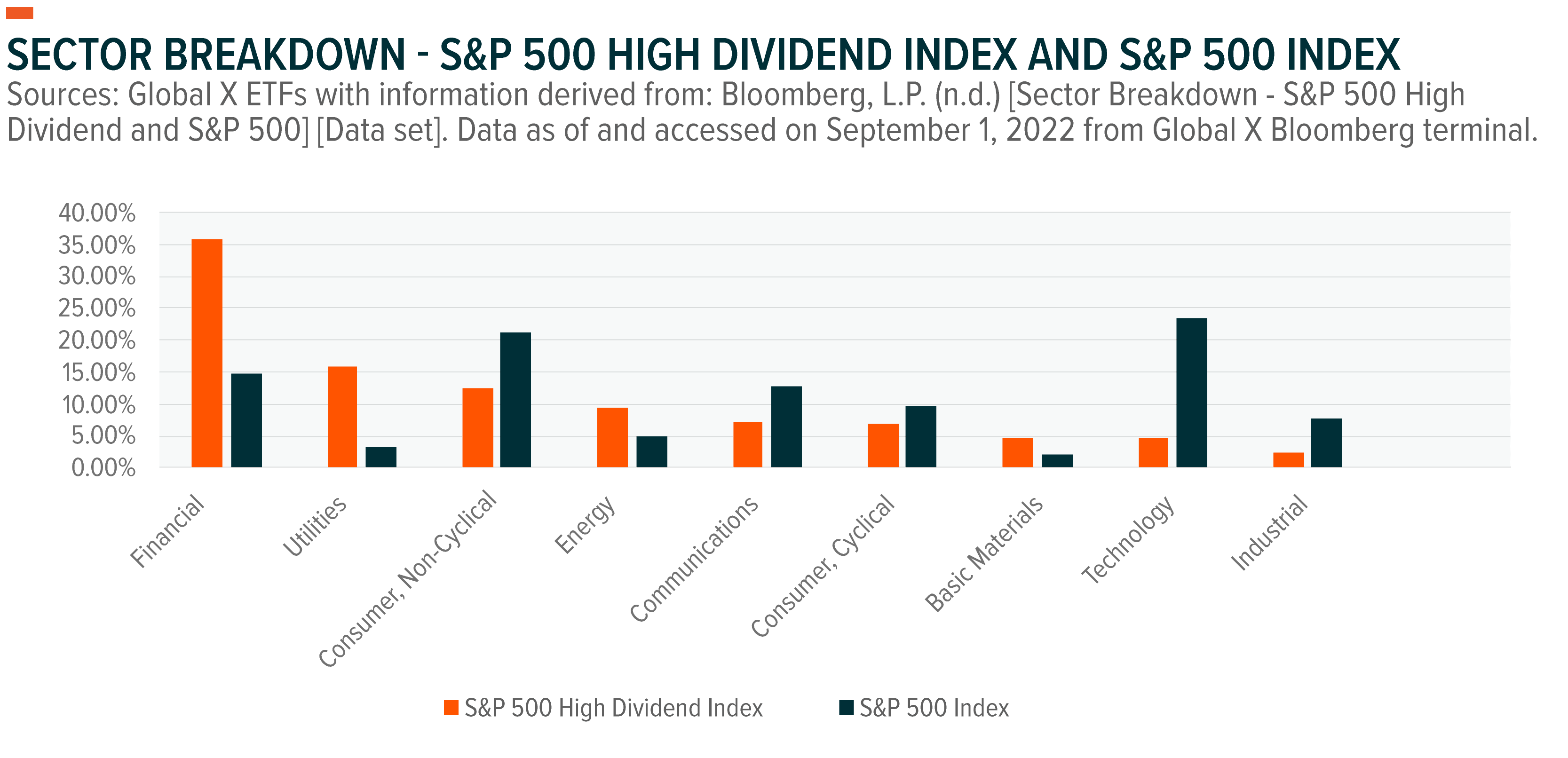

Some investors may find that they already have substantial exposure to specific sectors and want to diversify their portfolio. For example, typical income-oriented portfolios tend to have greater weightings to dividend-paying sectors like Financials, Utilities, and Real Estate while being underweight Information growth-oriented sectors like Technology, Communications Services, and Health Care.

Today’s environment appears particularly well-suited for the 50% covered call approach. Income is challenging to find across most asset classes, and rates are still relatively low compared to historical levels. Allocating half of an investor’s exposure to upside potential while seeking to generate income from the other half could be an attractive proposition for addressing this environment.

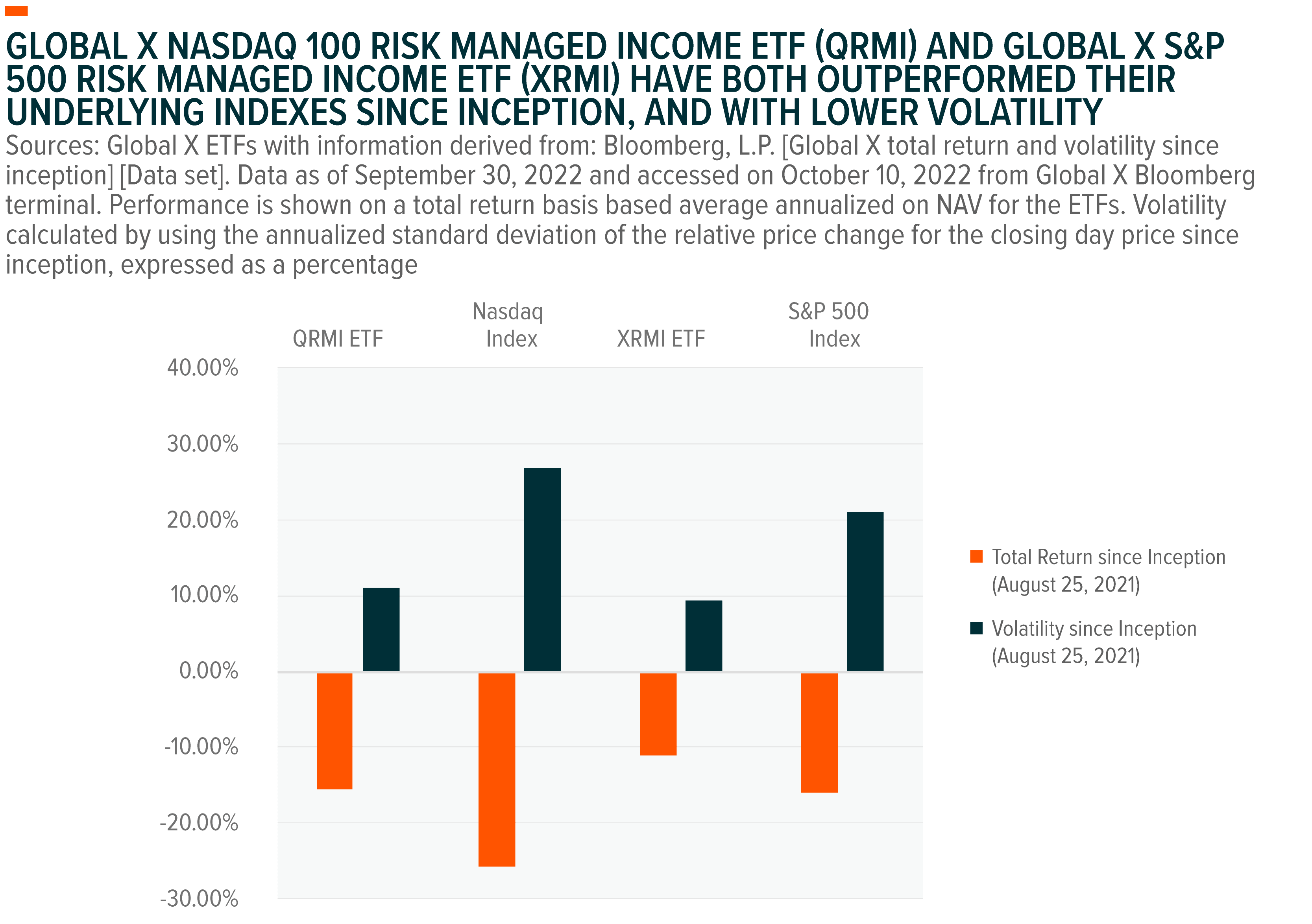

Risk Managed Income Strategies: May Produce Income And Mitigate Risk

Risk managed income strategies essentially combine a covered call with a protective put. The goal is to seek the option premiums that are typically pursued in a covered call strategy while also mitigating the risks of a major market selloff with a protective put. A risk managed income strategy may be an attractive source of return and can even serve as a complement to fixed income holdings given the different factor exposures through the use of call writing and put buying.

This strategy is a net credit collar strategy, meaning it intends to generate positive net option premiums while protecting against a portion of market downside. These can even serve as a replacement for or complement to covered call strategies, if the investor is willing to sacrifice some distributions for a degree of downside protection. In order to generate net premiums, risk managed income strategies typically own the securities in an equity index while also selling an ATM call option on that index and buying an OTM protective put. An example of this could be writing an ATM covered call and purchasing a 5% OTM protective put.

These strategies are considered net credit collars where the premiums received from selling the call option exceeds the cost of purchasing the put. This is compared to net debit which means that the strategy costs money to implement.

Performance data quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month- or quarter-end, please click on the fund names below.

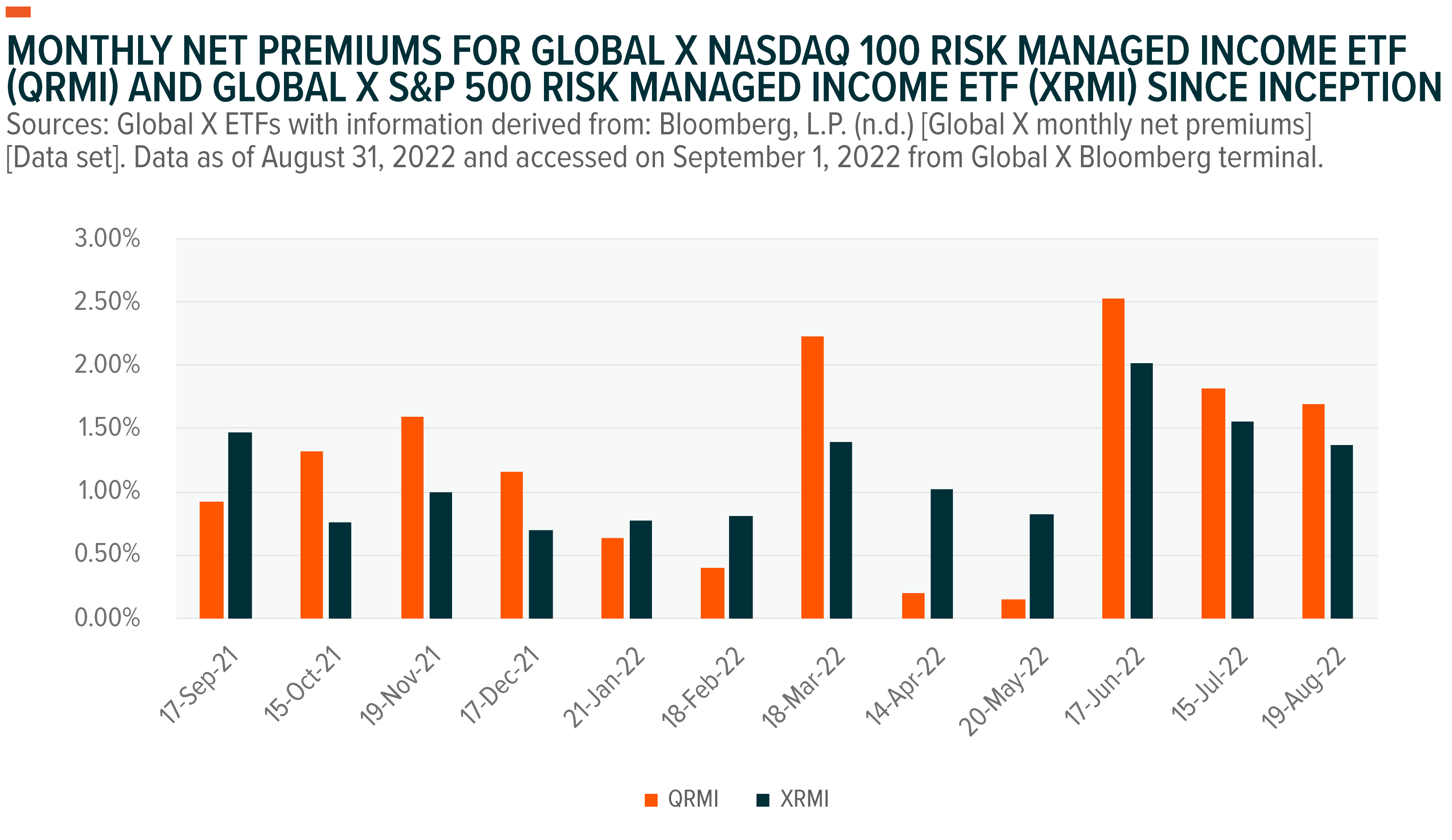

Risk managed income strategies can serve as a diversifier in an income portfolio, either in an alternatives bucket or by reducing exposure to equities. They are typically used as long-term strategic allocations, given that they have negligible inflation risk and seek to provide a diversified income. Below are the premiums generated from the Global X Nasdaq 100 Risk Managed Income ETF (QRMI) and the Global X S&P 500 Risk Managed Income ETF (XRMI). These funds intend to make distributions on a monthly basis.

QRMI and XRMI expect to settle their previous month’s options on their expiration dates and distribute a portion of the net income from their options premiums. Portfolio managers then enter into new one month options positions and the process repeats monthly.

Tail Risk Strategies: Defensive Positioning for a Drawdown Event

For those extraordinary events that upend markets and their returns, tail risk strategies can replace or complement existing exposures for a degree of protection. Tail risk strategies typically own the securities in an equity index while also buying an OTM protective put on that index. This allows for participation in the upside potential, minus the put premiums paid, while mitigating the impacts of significant downside moves.

The recurring purchases of protective puts in addition to fund management fees mean that these strategies come with costs. In an upward trending market, tail risk strategies will likely underperform because of the cost of the premiums paid to purchase the put options. In a sideways market, underperformance is possible because of the put option costs.

Severe downward markets is where tail risk strategies are designed to outperform. These strategies can be used strategically or tactically to achieve defensive positioning. They can make sense for investors looking for the growth characteristics of equities in their portfolio yet want to potentially avoid major drawdowns. Tactically, tail risk strategies can be helpful if an investor expects a major drawdown event but wants to remain invested in case upside continues. For example, implementing a tail risk strategy may be appropriate in a strong bull market where an investor believes a bubble may be forming.

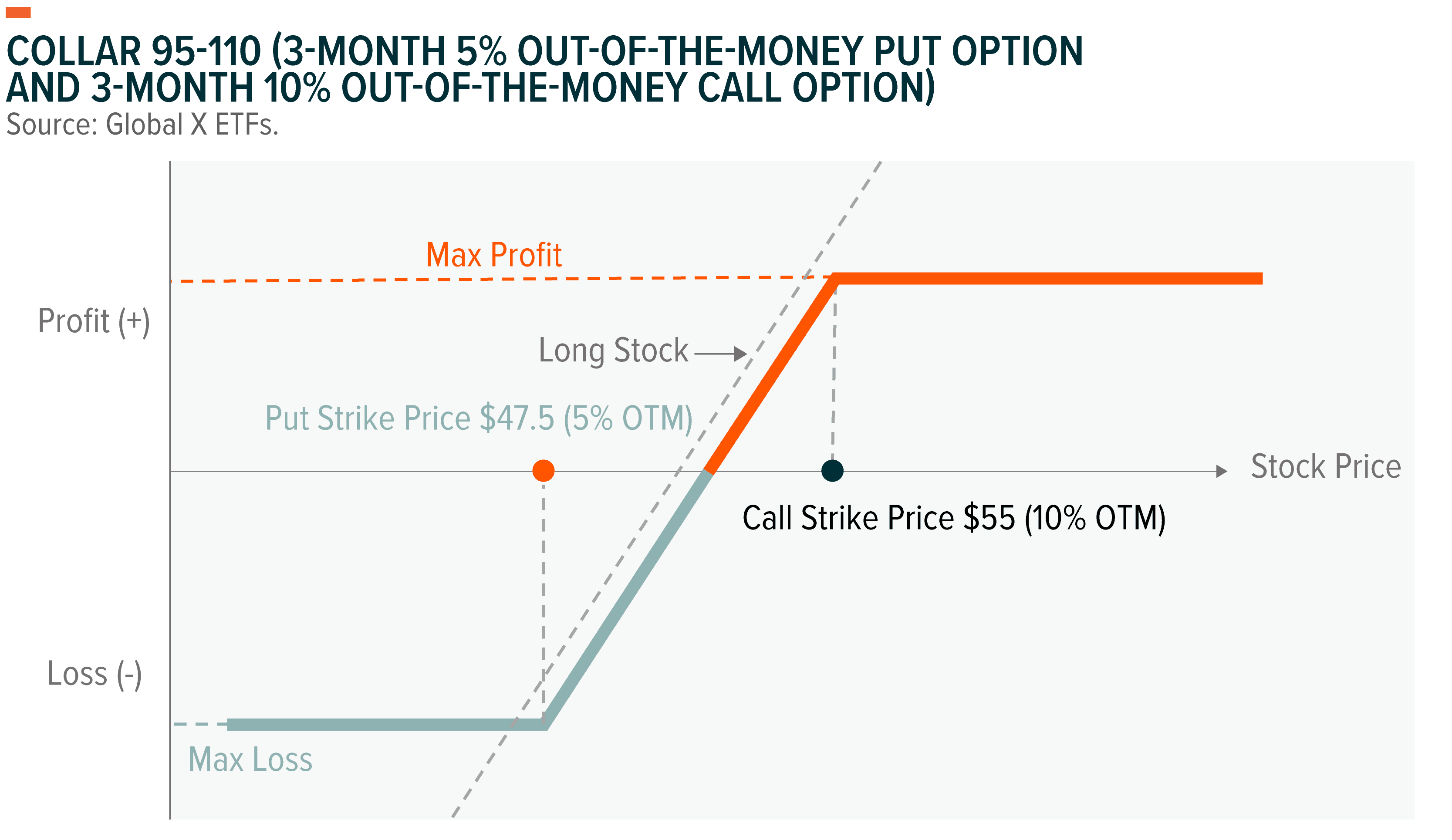

Collar Strategies: Limited Upside, but Limited Downside

Options strategies focused on mitigating volatility can help investors set expectations for a range of possible outcomes. Collar strategies can help temper downside risk through the purchase of a protective put. Risk managed income (RMI) strategies are a type of collar strategy. The key difference between these two is that RMI strategies still seek to generate net positive premiums whereas not all collar strategies are designed to generate net positive premiums.

Collar strategies typically combine owning equity securities with buying an OTM put option and selling an OTM call option on those same securities. As the name implies, a collar restricts performance between a specific range through the options’ expiration date. A collar strategy combines a long stock position, long put and a short call, which allows investors to create a range-bound level of returns at a relatively low cost while leaving some upside profit potential when the short-term forecast is bearish but the long-term forecast is bullish. For example, in a collar 95–110 strategy, an investor is buying a 5% OTM put and selling a 10% OTM call. The put option that is purchased will be 5% higher than the current price of the stock and then will be selling a put option that is 10% below the current price of the stock.

This can be a complement or replacement to existing exposures for investors who expect the market to move slightly upwards or sideways. In other words, these strategies are designed for more risk sensitive investors that may be expecting muted equity returns going forward.

Depending on the collar design, the options contracts can be net debit, meaning they cost money to implement; net credit, meaning they generate a positive net premium; or zero cost. Collar strategies can also mitigate downside risks through the purchase of a protective put. But by selling a covered call, these strategies can help limit the cost of the put in exchange for limiting upside potential.

Global X’s Options Strategy ETFs

Global X’s suite of option strategy ETFs can help investors maintain their preferred upside and downside exposures, as well as offering different levels of distribution potential. When selecting an options strategy, we believe investors should consider which underlying indices and underlying percentage of coverage or exposure the strategies use within the context of the portfolios, and how they align with their overall investment goals.

Based on an investor’s view of the macroeconomic landscape and their objectives, they may select either an options strategy that provides a certain level of desired hedged protection, or they can look to options strategies designed to potentially offer higher premium distributions.

For example, using an option strategy with monthly distributions may help to smooth out volatility compared to broad market indices. Accordingly, the covered call suite, the covered call and growth suite, and risk managed income suite have monthly distributions with one month options contract lengths rolled over each month.

The tail risk and collar 95–110 strategies are not necessarily designed to generate income but offer investors risk mitigation potential through the use of put options or collared return ranges with multiple options, respectively. These strategies offered by Global X utilize three-month option contract lengths in an effort to balance the cost of the put option protection and the frequency of equity market returns breaking through those levels or ranges.

Conclusion

Options-based strategies can help investors navigate various market conditions, including the type of elevated rising interest rate, inflation-driven volatility in the market currently. These strategies can help investors achieve certain objectives like seeking to generate income or managing downside risk. Markets are variable, but certain options strategies, including some of those offered by Global X, can help provide investors some stability amid uncertainty.

Related ETFs

XRMI - Global X S&P 500 Risk Managed Income ETF

QRMI - Nasdaq 100 Risk Managed Income ETF

QYLD - Global X NASDAQ 100 Covered Call ETF

XYLD - Global X S&P 500 Covered Call ETF

RYLD - Global X Russell 2000 Covered Call ETF

XTR - Global X S&P 500 Tail Risk ETF

QTR - Global X Nasdaq 100 Tail Risk ETF

XCLR - Global X S&P 500 Collar 95-110 ETF

QCLR - Global X Nasdaq 100 Collar 95-110 ETF

QYLG - Global X Nasdaq 100 Covered Call & Growth ETF

XYLG - Global X S&P 500 Covered Call & Growth ETF

DJIA - Global X Dow 30 Covered Call ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.