Preview

he electric vehicle (EV) supply chain is reaching an inflection point as consumers, original equipment manufacturers (OEMs), and governments accelerate the shift away from internal combustion engines (ICEs) and towards battery-powered vehicles. It’s natural that much of the focus on the emerging EV boom is on the downstream segment, with well-known auto manufacturers receiving outsized attention for unveiling sleek new car models and making bold announcements for electrifying their fleets over the next several years. But we believe that the growth trajectory for EVs will ultimately be determined not by downstream OEMs, but by the upstream lithium miners and battery producers who extract the raw materials and manufacture the batteries for EVs. In recent years, low lithium prices dissuaded miners from increasing production capacity, which is likely to lead to supply bottlenecks in the near future as demand accelerates. Ultimately, more investment in lithium mining and battery production will be necessary to ensure EVs are readily available around the world.

Key Takeaways:

- Major traditional automobile manufacturers like GM and Ford are investing billions to electrify their model ranges over the next 10 to 15 years

- Government policies in major auto markets like the U.S., China, and Europe are further accelerating adoption of EVs through subsidies

- To meet growing EV demand, battery production must expand substantially, causing a global arms-race among major governments, battery producers, and automobile manufacturers

- While lithium markets were previously oversupplied, lagging investment in additional production capacity could result in shortages of the key raw material for batteries as EV demand surges

Traditional OEMs Commit to Electric Vehicles

Globally, EVs accounted for less than 5% of total car sales in 2020, but the segment grew 45% to 3.2 million even amid the pandemic.1,2 EV sales momentum appears to have continued into 2021, with 1.1 million sold in Q1, up 125% from last year.3 Conversely, ICE sales are stalling. They fell 14% 2020 and are up by only an estimated 8% through the first quarter of 2021.4,5

With EV sales growth outpacing ICEs, traditional auto OEMs are increasingly committing to electrifying their fleets. GM is on its way to an all-electric future, with a commitment for 30 new global EV models by 2025 backed by a $27 billion investment on all-electric and autonomous vehicles.6,7 Similarly, Ford recently announced a $29 billion commitment to electric and self-driving cars and unveiled an electric version of the F-150 truck – the bestselling vehicle in the U.S. since 1981.8 Volkswagen Group, too, announced their spending plans on EVs, hybrid powertrains and digital technology over the next five years with a price tag of 73 billion euros ($86 billion).9 The list goes on, with most major OEMs investing heavily in an EV-centric future.

Major commitments by OEMs to retool their production processes to accommodate electric vehicles and to offer a wide range of battery-powered models plays a significant role in furthering the adoption of electrified transport. On the production side, tapping into the vast scale of a GM, Ford, or VW will likely reduce prices for consumers and improve important features like range and charging speeds. And with dozens of models to choose from, spanning a range of sizes, styles, and price points, virtually every car buyer will have a viable EV model to consider.

Government Policies Accelerate EV Demand

Beyond commitments from OEMs to expand their EV lineups, supportive government policies around the world are further driving EV adoption.

In the U.S., President Biden's infrastructure-focused American Jobs Plan commits $174 billion to provide support across the U.S. EV ecosystem. On the demand side, it provides incentives and subsidies for purchasing mass market EV models, heavy duty vehicles & trucks, transit buses, and school buses, while providing funding to electrify the 645,000 vehicle federal fleet. On the supply side, it incentivizes greater investment in domestic EV production capabilities, including tax credits for vehicle manufacturing, cost-sharing grants for battery assembly facilities, low-cost financing for medium and heavy- duty vehicle production, and grants to retool dormant factories. Beyond that, the plan seeks to provide incentives to expand the nation’s electric charging infrastructure by 500,000 stations by 2030.10

Additional proposed legislation, like the Clean Energy for America Act (CEAA) expands on the $7,500 federal tax credit for EVs with a proposed additional $2,500 for new qualified plug-in electric drive motor vehicles for which the final assembly is at a facility in the U.S. before 2026 and other $2,500 if the vehicle is assembled at a facility whose production workers are members of a represented labor organization.11 In total, EVs could be eligible for a maximum credit of $12,500, which in many instances could make them cheaper than their gas-powered alternatives.

Major auto markets outside of the U.S. are offering supportive EV policies as well – though many of them are designed to eventually phase out over the coming years. In China, EV subsidies were extended in April 2020 for two more years. In 2021, the subsidy for EVs with a driving range of 186-249 miles is approximately $2,000 per vehicle, but current plans will taper this subsidy by 30% in 2022.12 Local incentives like free EV license plates and registrations in some major Chinese cities have helped propel hybrid and electric vehicles to already account for one-fifth of new car sales on average in China’s six largest municipalities.13

In Europe, recent initiatives include Germany realigning its tax system to increase taxes on ICEs, France extending financing for EV charging infrastructure, and Spain implementing new tax incentives and aid for EV research and innovation.14 Norway, which exempts fully electric vehicles from taxes and aims to eliminate the sale of petrol and diesel cars by just 2025, ended 2020 with EVs taking a 54% market share.15

Battery Production: A Global Arms Race

While OEMs and governments are signaling strong commitments to EVs, upstream lithium mining and battery production capacity constraints could present bottlenecks.

On the battery front, the ability to efficiently, reliably, and inexpensively mass-produce lithium-ion cells is essential for growing the EV market. Yet limited battery manufacturing capacity, particularly in major developed markets, presents supply chain risks. For example, President Biden’s plans to electrify the federal vehicle fleet would require 69 GWh of battery capacity.16 Yet total battery production in the U.S. was only about 40 GWh in 2020.17 Factoring in fast-growing demand for EV passenger vehicles, buses, and trucks, and U.S. automakers will likely have to depend on overseas battery supply chains for the foreseeable future.

But given the strategic importance of EVs as an advanced technology, a method to thwart climate change, and a potential major employer in manufacturing, governments, OEMs, and suppliers do not want to outsource major components of this industry. At present, there are 211 announced lithium-ion battery factories capable of producing over 1 GWh of battery cells per year. 156 are in China, followed by 22 in Europe and only 12 in the U.S.18 Today, battery capacity in the U.S. largely comes from Tesla-Panasonic’s Gigafactory 1 in California, LG Chem’s Michigan plant supplying GM, and AESC Envision’s factory in Tennessee.

A few battery producers are ramping up production capabilities in the U.S. LG Energy Solution plans to invest $4.5 billion to expand its EV battery manufacturing footprint in the U.S. with an additional 70 GWh of capacity starting in 2025.19 Panasonic also plans to add a new production line at the Nevada factory it co-owns with Tesla.

But the battery arms race isn’t just limited to the U.S. Suppliers are investing around the world in expanding battery production facilities in major markets. For example, Panasonic is looking at building a lithium-ion battery business in Norway in a bid to supply European carmakers.20 In China, leading battery manufacturer CATL recently announced its plans to invest $4.5 billion to increase its lithium-ion battery capacity.21

Some car manufacturers are taking battery production into their own hands. At its Battery Day in September 2020, Tesla announced a goal to generate 100 GWh of battery production by 2022.22 During its Power Day this March, Volkswagen outlined a roadmap to have six 40 GWh cell manufacturing plants with a total of 240 GWh of capacity by 2030.23 China’s Geely was another carmaker to jump into the battery production fray in March. It aims to build a 42 GWh cell base in Ganzhou, Jiangxi Province.24

For perspective, in 2020, global battery capacity totaled 755 GWh.25 Yet, total battery capacity in the global pipeline for 2030 is 3,792 GWh (or 3.8 TWh), a robust 402% increase from 2020.26

Lithium: Price Dynamics Favorable

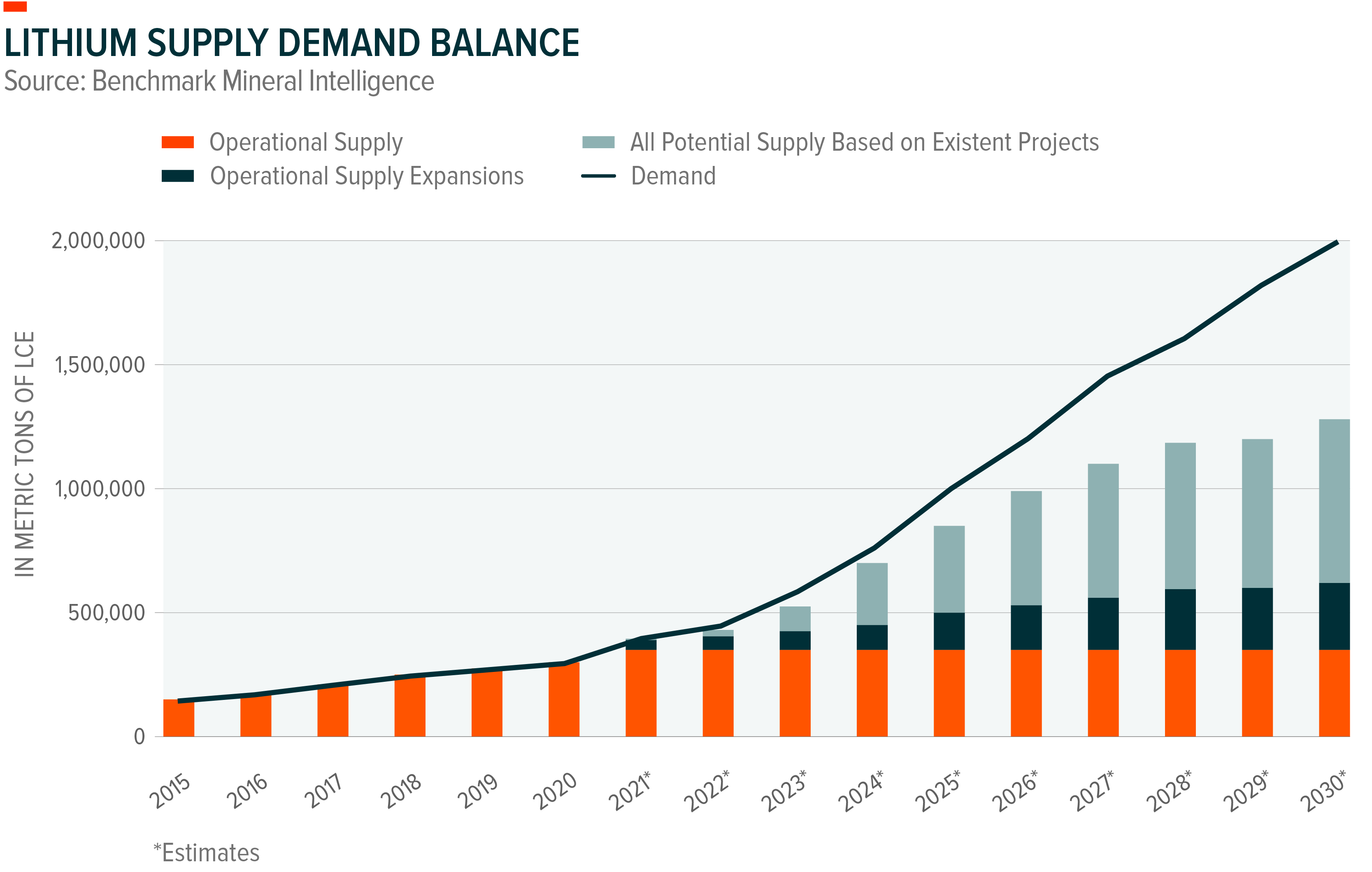

Lithium prices have risen rapidly, up 69% this year as of May 2021.27 This is a stark contrast from the last three years when prices declined from over $20,000 per metric ton (mt) of lithium carbonate equivalent (LCE) in Q4 2017 to less than $8,000 in Q4 2020 because the market tipped into a temporary oversupply. Falling prices resulted in delayed and cancelled capacity expansions as lithium miners saw little incentive to increase capacity. Yet as lithium demand surges again, concerns of a future supply crunch is raising an important question: Can Lithium Keep Up with the EV Boom?

As lithium prices rise this year, expansion plans are being revived. The world’s largest lithium producer, Albemarle, is set to double its production capacity to 175,000 mt by year-end.28 The second largest producer, Chile’s SQM, is on track to expand production of lithium carbonate by 71% to 120,000 mts by December.29 And several other lithium miners are making progress on their capacity expansions. Yet, given how much lithium is needed to keep up with the rapidly growing EV market, supply may fall into a deficit as early as this year.30

Lithium demand is expected to increase by over 200% during the next five years, rising from 300,000 mt in 2020 to 1 million mt by 2025. By 2030, demand could reach 2 million mt. But it takes time to bring on additional lithium supply. Depending on the method of extraction, bringing new capacity online can take 3–5 years or more of studies, permitting, capital raising, and capital expenditure before any lithium is produced. Therefore, rapid demand growth for EVs could be limited by supply-side upstream lithium mining capacity conditions.

Governments and companies around the world are starting to pay attention to the potential lithium supply-demand gap and evaluate actions to prevent this from happening. Chile and Australia are the world’s two largest producers of lithium, which then ship most of the raw material to China for processing into battery cathodes. The U.S. is seeking to become an important player, with companies like Lithium Americas developing lithium projects in northern Nevada, for example. The project, known as Thacker Pass, is the largest known lithium resource in the U.S., and aims to produce the first carbon neutral lithium products in the industry.31 Large OEMs such as Daimler and VW, too, have intensified their scrutiny of lithium miners to prevent uninterrupted lithium supply.

Conclusion

EV growth is surging as customers demonstrate a growing interest in the latest automobile features and climate change-mitigating technologies. Governments are helping to make EVs more affordable to the masses through subsidies and incentivizing domestic production. And OEMs are meeting customer demands by offering wider EV product ranges than ever before. But less focus has been given to the upstream segments of the EV supply chain. Battery production must grow substantially to meet expected EV demand, and governments and OEMs may be wise to repatriate this critical piece of the supply chain. Beyond batteries, the raw materials necessary for EVs must also be secured, but a recent history of cancelling capacity expansions could come back to hurt the industry unless it is addressed quickly. Factoring in rising geopolitical tensions and general supply chain uncertainty, and we could see a new arms race forming with major economies seeking to build out fully domestic supply chains, spanning mining, battery production, and auto manufacturing.

LIT: The Global X Lithium & Battery Tech ETF (LIT) invests in the full lithium cycle, from mining and refining the metal, through battery production.

DRIV: The Global X Autonomous & Electric Vehicles ETF (DRIV) seeks to invest in companies involved in the development of autonomous vehicle technology, electric vehicles (“EVs”), and EV components and materials. This includes companies involved in the development of autonomous vehicle software and hardware, as well as companies that produce EVs, EV components such as lithium batteries, and critical EV materials such as lithium and cobalt.

Click the fund name above to view the fund’s current holdings. Holdings subject to change. Current and future holdings subject to risk.