Implementing options-based strategies have become an increasingly common tool in income-oriented portfolios. Over time, Global X has developed a range of approaches within this space, reflecting different investor objectives, market environments, and preferences for regular distributions versus upside participation.

The Global X Income Edge℠ ETF suite builds on this foundation.

On February 18, 2026, Global X listed the Global X U.S. 500 Income Edge℠ ETF (EDGX) and the Global X Nasdaq-100® Income Edge℠ ETF (EDGQ) on NYSE Arca. These funds maintain exposure to the Solactive GBS United States 500 Index and Nasdaq-100® Index, respectively, and write weekly call options against that exposure in a systematic, actively managed strategy designed to target defined annualized distribution rates – 9% for EDGX and 13% for EDGQ – while retaining the ability to participate in a portion of the respective equity market’s upside.

Key Takeaways

- Options-based strategies have seen a surge in modernization, now offering new features for investors to take advantage of.

- The Income Edge℠ ETFs utilize weekly call option writing and flexible coverage ratios to target defined annualized distribution rates.

- By adjusting option coverage in response to market conditions, the funds seek to balance income generation with continued equity exposure.

Broadening Depth of the Options Market Reflects Demand for Sophisticated Strategies

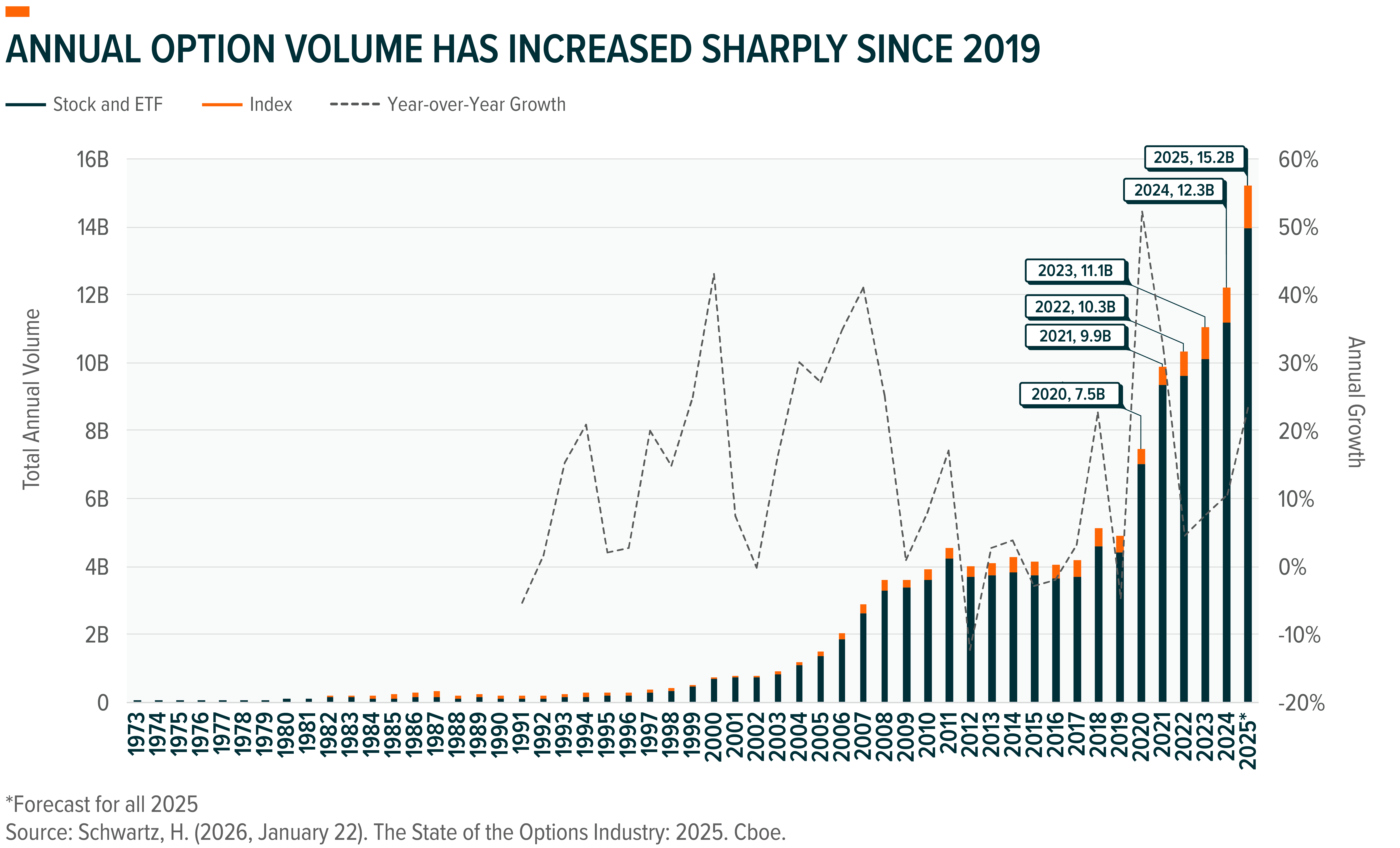

The expansion of the U.S. options market has increased the feasibility of more dynamic, rules-based income strategies within an ETF wrapper. Annual option volumes have increased materially over the past decade, reflecting rising investor demand for instruments to pursue income, hedging, and tactical positioning.

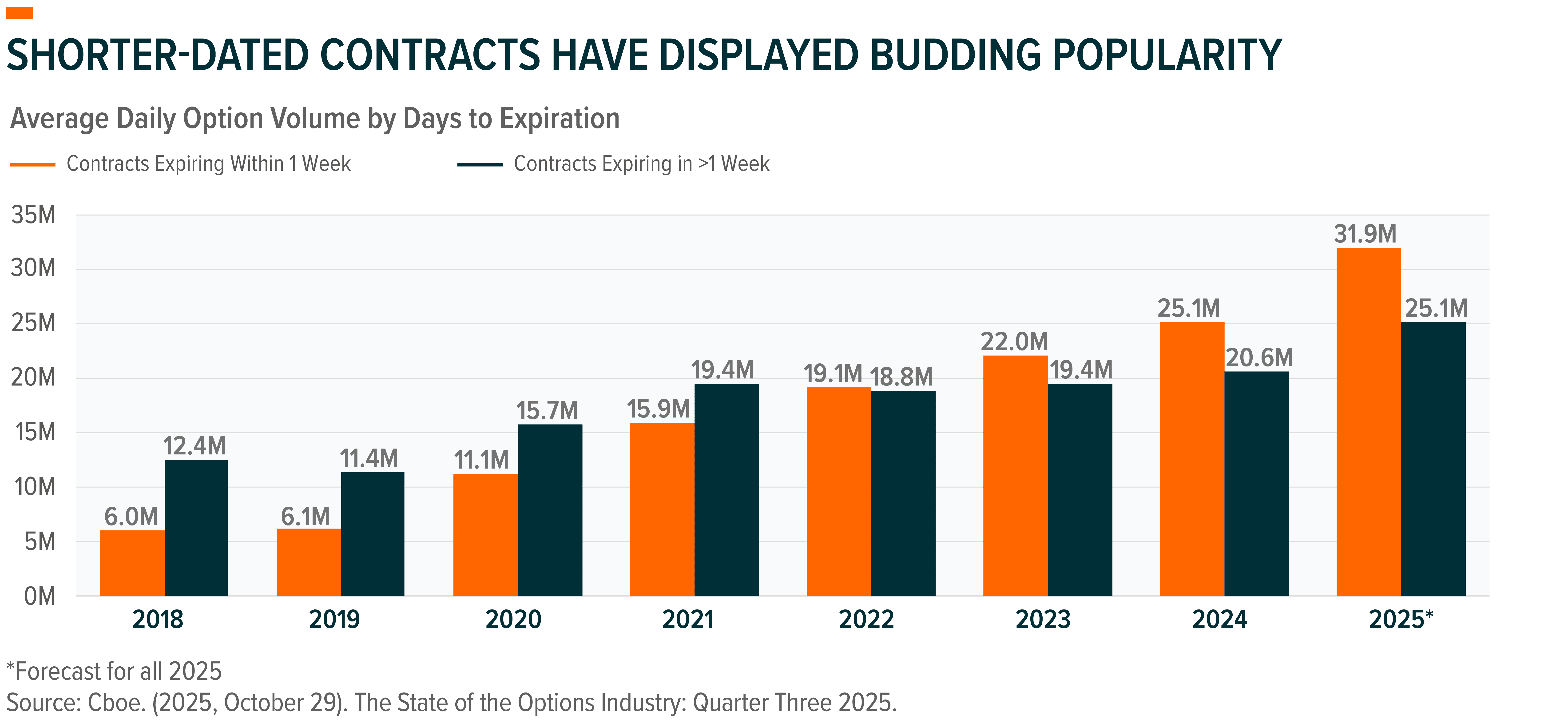

Alongside higher volumes, the composition of the options market has shifted meaningfully toward shorter-dated contracts. Weekly options have become increasingly liquid and widely adopted, providing market participants with more frequent opportunities to adjust exposure.

For investors, these developments increase the feasibility of implementing dynamic options-based income strategies within an ETF structure. Strategies that may otherwise require frequent trading, ongoing monitoring, and operational infrastructure can be delivered through a professionally managed, exchange-traded vehicle.

Systematic Framework for Targeting Defined Distributions

EDGX and EDGQ seek to generate income by maintaining long exposure to their respective reference assets and writing weekly call options in exchange for option premiums. Rather than relying on a fixed or predetermined level of option coverage, the funds employ a systematic process that adjusts the percentage of the portfolio covered each week in pursuit of their distribution rate objectives.

Each week, the funds seek to generate approximately 1/52nd of their stated annual distribution rate target, using option coverage as the primary lever to do so. At the start of each option cycle, the portfolio managers assess prevailing market conditions – including equity volatility, interest rates, and option pricing – to determine the amount of premium required for that week. This premium may be complemented with dividends received from the underlying equity holdings, seeking to achieve the desired weekly distribution.

When volatility is elevated, higher premiums may allow the funds to meet their weekly distribution targets while covering a smaller portion of the portfolio, leaving more exposure uncapped and available to participate in possible equity upside. Conversely, when volatility is lower, option premiums tend to compress, and a greater degree of coverage may be applied to achieve the targeted level of distribution.

By recalibrating coverage on a weekly basis, the Income Edge℠ ETFs seek to internalize what might otherwise be a tactical coverage decision for investors, adjusting exposure as market conditions evolve.

The annualized distribution rate targets of EDGX and EDGQ – 9% and 13%, respectively – reflect the historical volatility profiles of their respective reference assets. The Nasdaq-100 has typically exhibited higher volatility than broader U.S. equity benchmarks, a profile that has historically supported greater option premium potential. As a result, EDGQ is structured with a higher annualized distribution rate target than EDGX, while both funds operate within a consistent investment framework.

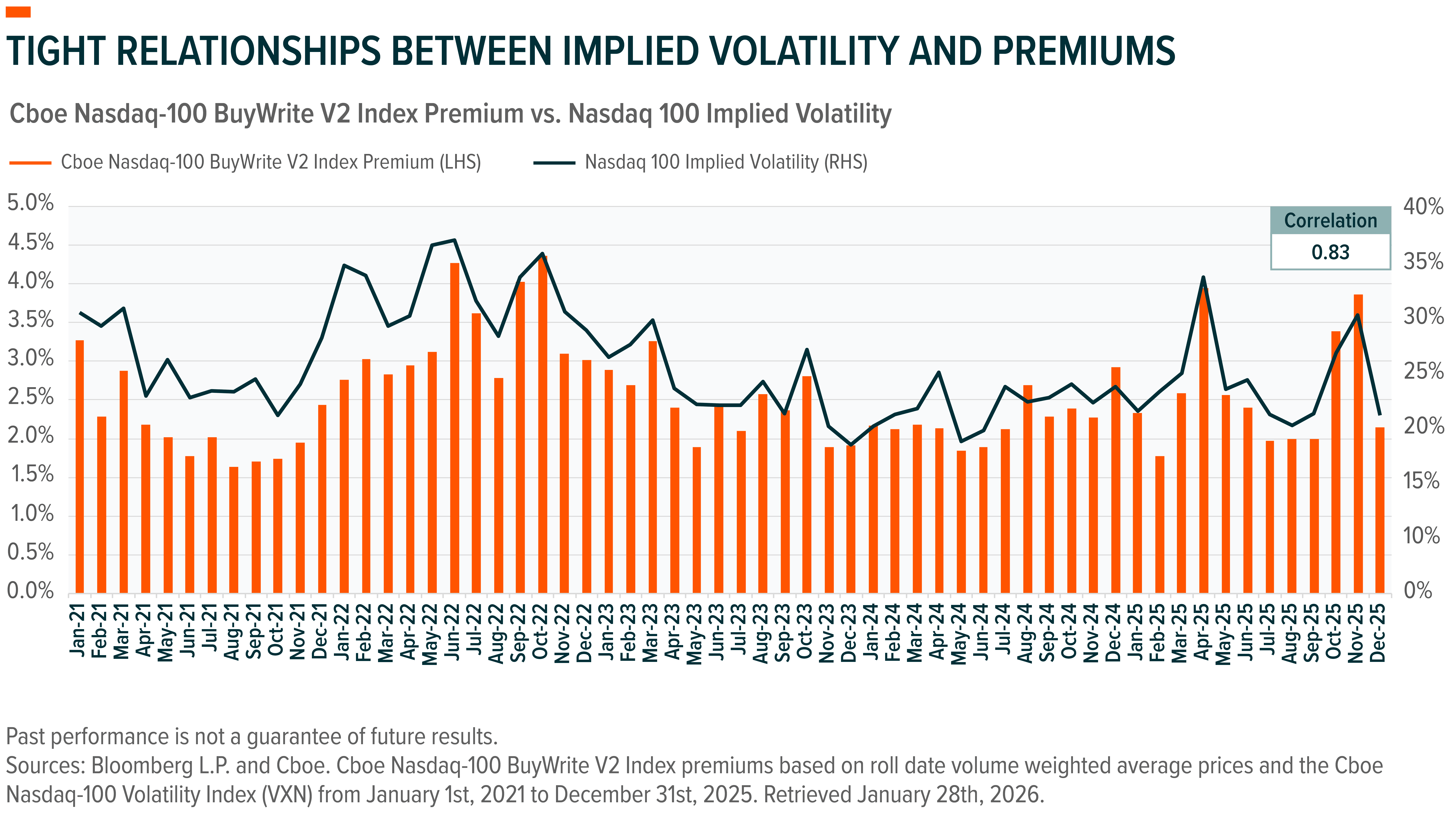

This approach reflects the well-documented relationship between option premiums and market volatility. Historically, periods of elevated volatility have been associated with higher option premiums, while calmer markets have generally produced lower levels of income from option writing.

Variable Option Coverage and Weekly Implementation

In a conventional covered call strategy, an investor typically holds a reference asset and writes call options against that position, generating income in exchange for capping a portion of the reference asset’s upside. The degree to which upside is capped depends largely on how much of the portfolio is covered by call options, with higher coverage generally increasing income potential while limiting participation in rising markets.

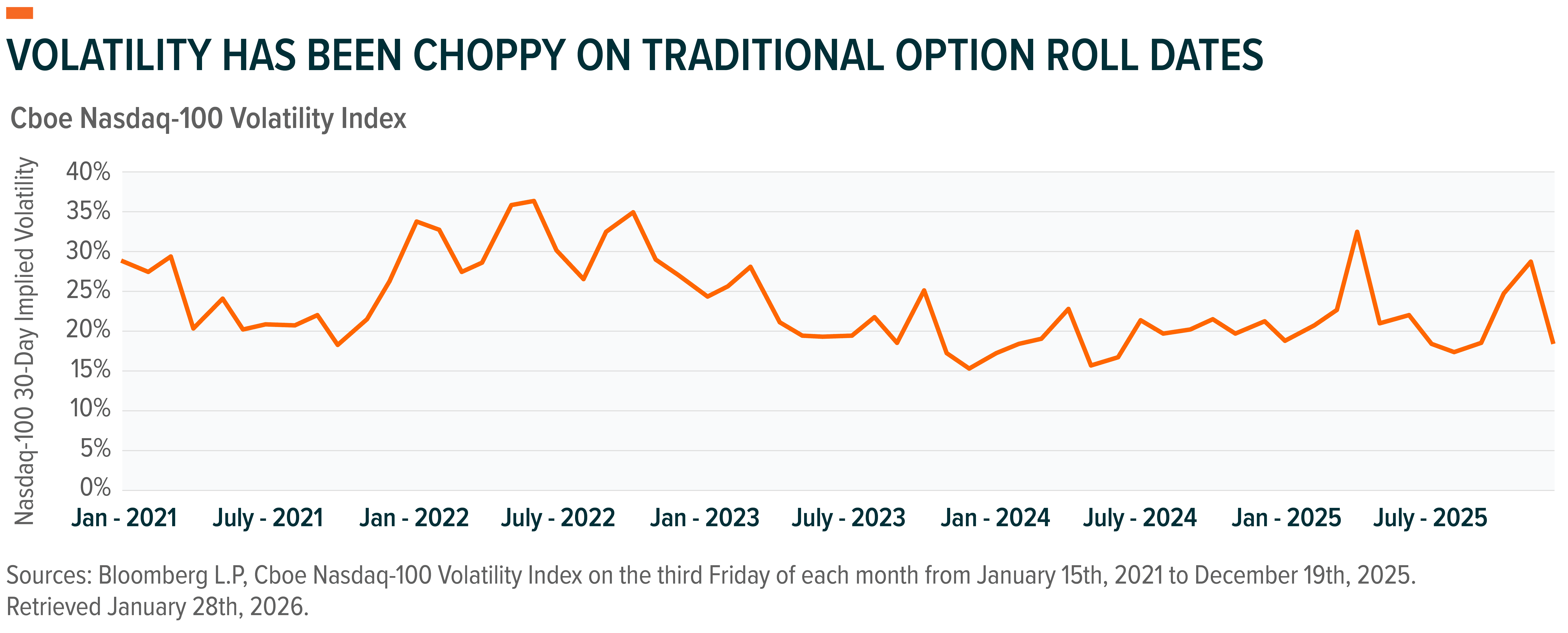

Beyond the coverage ratio, volatility is a key driver of option premiums, but it does not evolve smoothly over time. As shown below, volatility levels observed on traditional monthly option roll dates have historically been uneven, often fluctuating meaningfully from one expiration to the next.

The level of volatility present on that specific date can have an outsized influence on option premiums and portfolio positioning for the weeks that follow. In environments where volatility changes rapidly, this dynamic can leave premium generation more dependent on the timing of the roll itself.

The Income Edge℠ ETFs are designed to manage this trade-off. Rather than maintaining a fixed level of option coverage, the funds may dynamically adjust coverage levels in response to market conditions. This structure is intended to support income generation while maintaining exposure to equity price movements across varying volatility regimes. We expect the fund’s coverage ratio to average approximately 25% over the long term, though actual coverage may fluctuate meaningfully from week to week and is not fixed, targeted, or guaranteed. In periods of elevated volatility, option coverage may compress well below 25%, while in lower-volatility environments, coverage may expand well above 25%.

A key enabler of this approach is the use of weekly call options. Shorter-dated contracts allow the portfolio managers to reassess market conditions and recalibrate coverage more frequently, reducing reliance on any single option roll date.

The potential relevance of this structure was evident in 2025, when the Nasdaq-100 experienced sharp, event-driven moves. In early April following Liberation Day, the Nasdaq-100 declined 12.71% from April 2 to April 8, 2025, before rebounding 14.53% on a total return basis through the end of the month.1 In such environments, strategies that reset option exposure more frequently may be better able from a portfolio management perspective to respond to rapidly changing conditions, rather than remaining tied to a monthly roll established prior to the event.

By combining weekly option writing with variable coverage, the Income Edge℠ ETFs seek to internalize what might otherwise require ongoing tactical decision-making by the investor, adjusting option coverage as volatility and market conditions evolve within a disciplined, rules-based framework.

Conclusion: Defined Annualized Distribution Rate Targets Within a Systematic Covered Call Strategy

The Global X Income Edge℠ ETFs build on Global X’s lineup of covered call funds by introducing a weekly option strategy designed to target defined annualized distribution rates. By pairing systematic call writing with a flexible coverage approach, EDGX and EDGQ aim to deliver distributions while maintaining exposure to equity market movements. In doing so, the Income Edge℠ ETFs offer investors an additional way to pursue equity income within the Global X covered call framework.

Related ETFs

EDGX – Global X U.S. 500 Income Edge℠ ETF

EDGQ – Global X Nasdaq-100® Income Edge℠ ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.