As demand for AI computing explodes, the bottleneck is increasingly shifting from chips to powered, ready-to-use data center capacity. New construction is accelerating, but the time, power, permits, equipment, and transmission access required to bring new capacity online make existing powered facilities strategically valuable. That value should rise further in the age of inference, as AI workloads become more distributed and proximity to user and application traffic increasingly matters.

This creates a compelling setup for global data center operators. They sit at the intersection of scarce infrastructure, rising AI demand, and long-duration customer commitments, offering a differentiated way to access the AI buildout, and in our view, with also less direct exposure to the crowded parts of the mega-cap technology trade.

Key Takeaways

- As AI adoption grows, powered and ready-to-use data center capacity could become an increasingly important part of the AI infrastructure stack.

- Computing needs shifting towards inference should make data center demand increasingly recurring and distributed.

- The Global X Data Center & Digital Infrastructure ETF (DTCR) offers a targeted route into the long tail of AI infrastructure.

Supply Constraints Meet Rising AI Demand

AI's economic value depends on infrastructure that can't be built on software timelines. Models train and run inside powered, cooled, networked data centers that take years – not quarters – to bring online. Power contracts, transmission queues, permitting, equipment lead times now determine what gets built and when. For the next phase of AI growth, the binding constraint is physical.

Demand, meanwhile, is changing shape. Training large AI models drove the first wave of compute growth, but inference is driving the next phase and could ultimately represent a larger opportunity. Unlike AI training, which is driven by model development cycles and research spending, inference occurs every time a model is used, allowing demand to scale alongside adoption.

Training workloads can operate in remote hyperscale campuses optimized for low-cost power and raw computing horsepower. Inference workloads, by contrast, are generally more sensitive to latency, proximity to users, interconnection density, and access to cloud and enterprise networks. In our view, that means the next phase of AI infrastructure demand could extend across both hyperscale facilities built for model training and interconnected smaller data centers that support enterprise deployment and inference workloads.

That distinction is increasingly relevant for investors looking to capture the broader AI ecosystem. Hyperscalers should continue to remain central to AI development and deployment, but at the same time, independent operators and colocation providers play a pivotal role within the AI value chain by supporting where enterprises increasingly deploy AI services: close to end users, connected across multiple cloud environments, and integrated with proprietary enterprise data.

Importantly, these operators tend to allocate capital differently from the hyperscalers. Rather than building speculatively and addressing utilization after the fact, colocation businesses generally expand against signed leases and anchor tenants, which has historically translated into more measured asset growth and steadier paths to monetization. That discipline, combined with tangible asset backing, in our view makes the group one of the more attractive ways to gain exposure to potential AI infrastructure upside.

Story in Data: The Data Center Opportunity

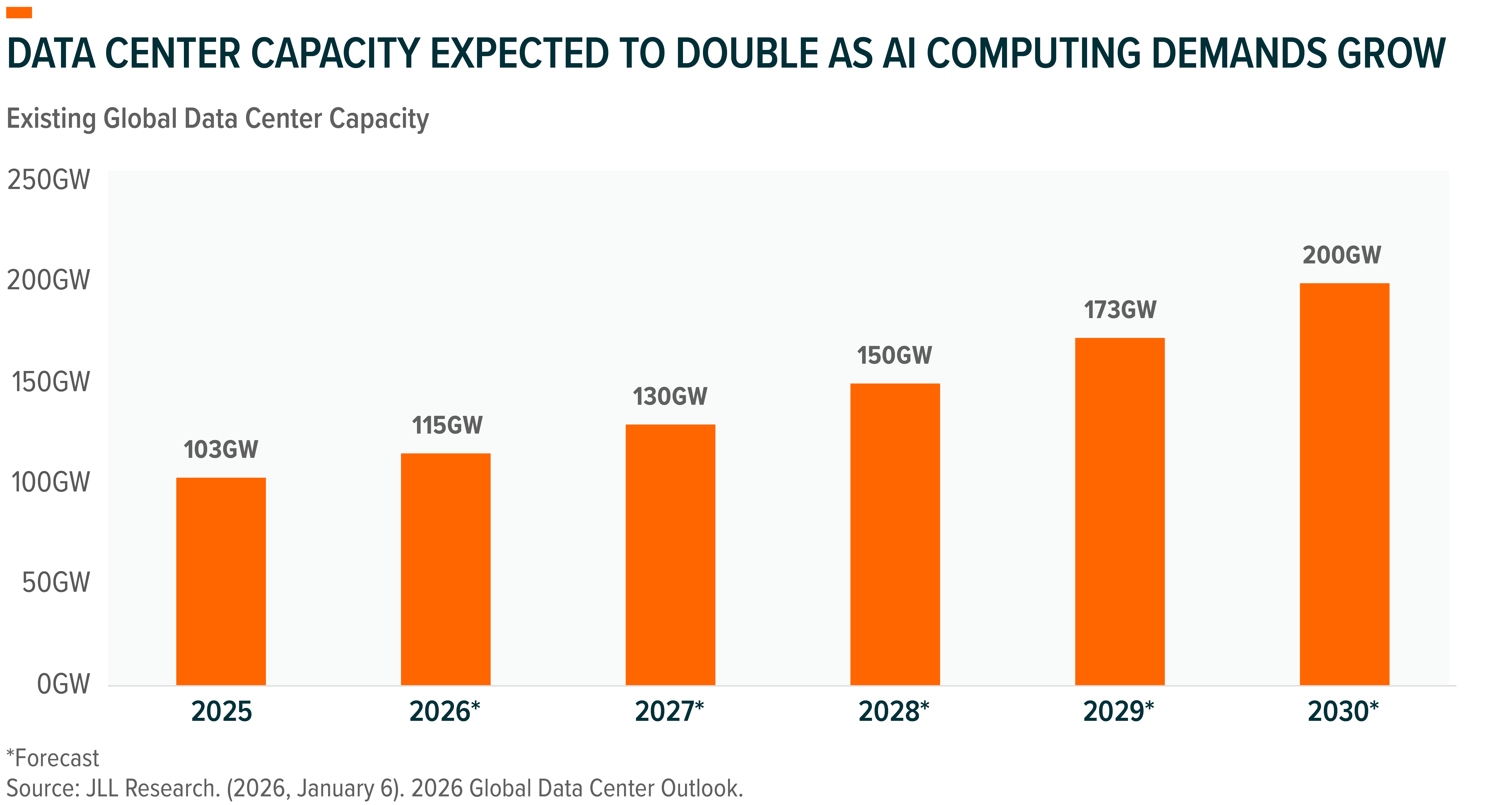

1. Global Capacity Must Roughly Double by 2030 to Meet Demand: Global data center capacity is projected to rise from ~103 GW in 2025 to ~200 GW by 2030 – a 14% compound annualized growth rate (CAGR) and nearly 100 GW of incremental capacity.1 Cloud, AI training, and the accelerating inference wave are converging into a single digital infrastructure supercycle.

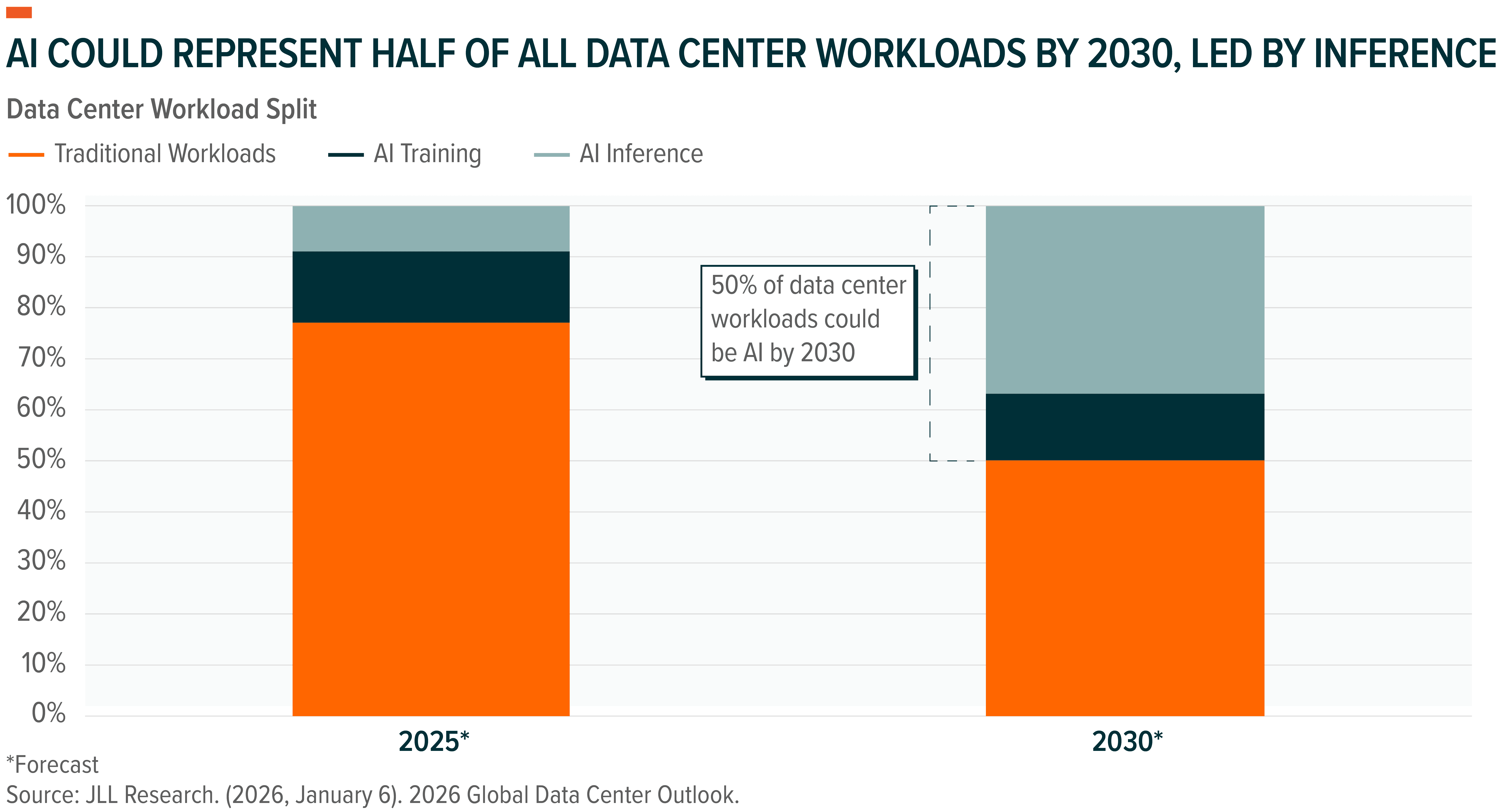

2. Demand Mix Shifts Toward Inference: Inference could overtake training around 2027, with AI representing ~50% of all data center workloads by 2030.2 Training can sit in remote campuses, but inference depends on latency, connectivity, and proximity to users. As AI deployment expands, demand may increasingly extend beyond hyperscale campuses toward interconnected colocation and metro-area infrastructure, bringing a broader range of digital infrastructure providers into focus.

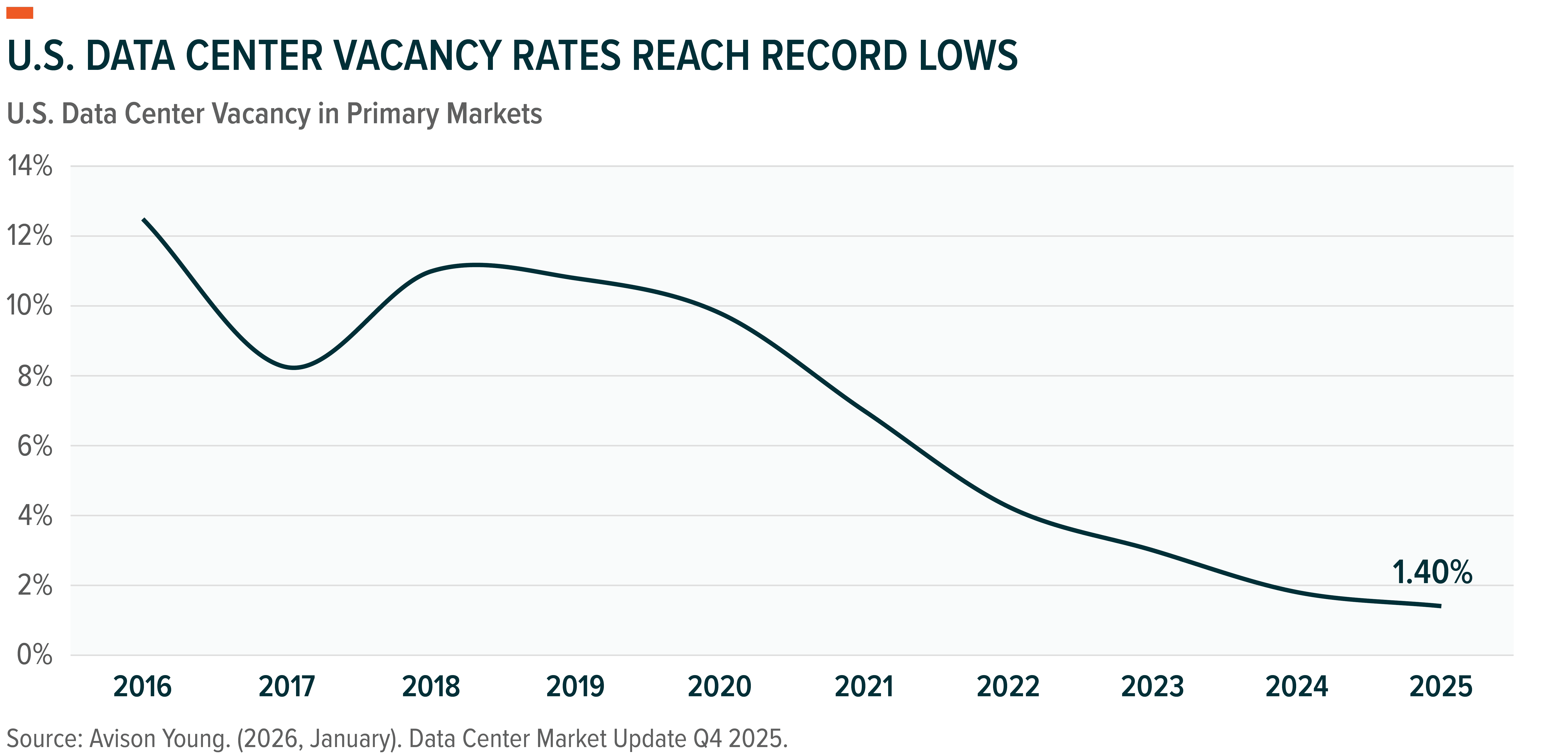

3. Vacancy Is Already Near Record Lows: North American data center vacancy across primary data center markets fell to 1.4% by year-end 2025 – even as new supply came online.3 Demand is absorbing capacity faster than it can be delivered, which could continue to support favorable pricing and leasing dynamics for existing facilities.

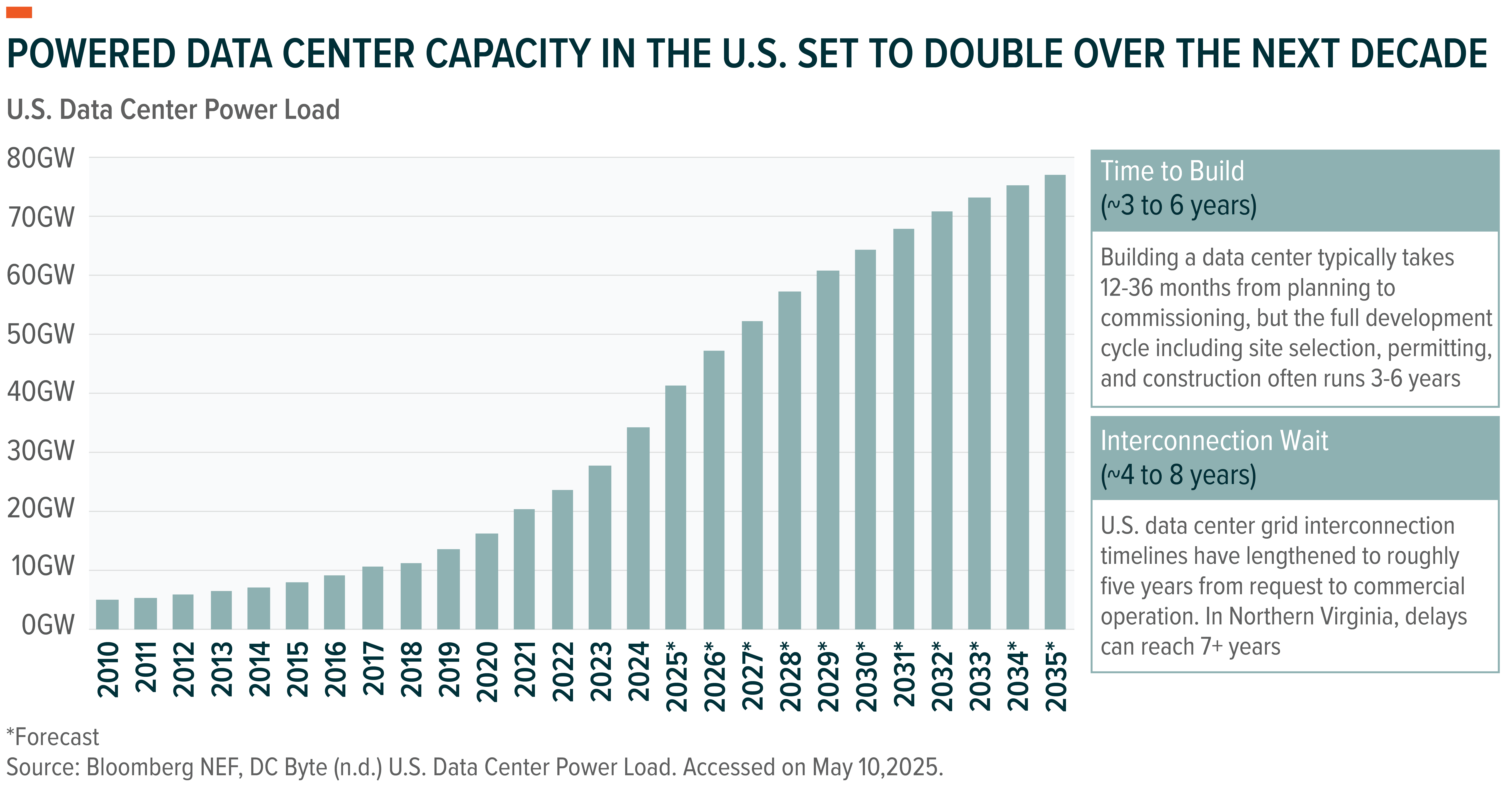

4. Power Is the Real Bottleneck: In major markets like the U.S., new data center supply is becoming harder to deliver. Traditional 12-to-18-month timelines no longer apply for large AI campuses, with projects requiring multiple substations and interconnection timelines stretching to 24, 36, or 48-plus months when new high-voltage transmission or incremental generation is needed.4 As a result, existing powered and operational capacity may become increasingly valuable, particularly in markets where access to power and transmission infrastructure is limited.

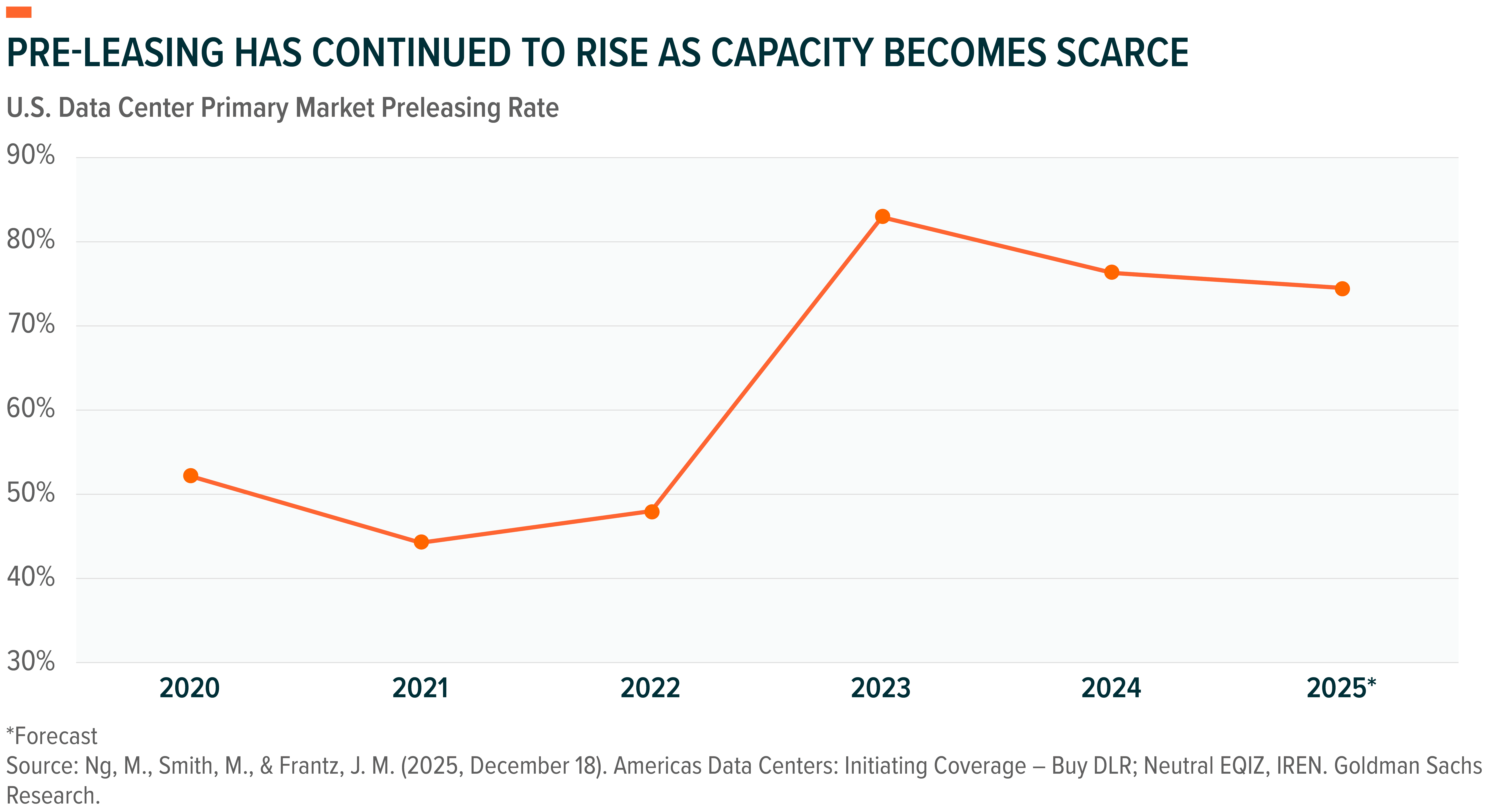

5. Pre-Leasing Turns Scarcity into Revenue Visibility: Preleasing is expected to remain in the mid-70% range, compared with the historical 40% to 50% norm.5 That suggests operators are able to secure demand years before capacity is delivered and are not merely building speculative capacity into an AI hype cycle.

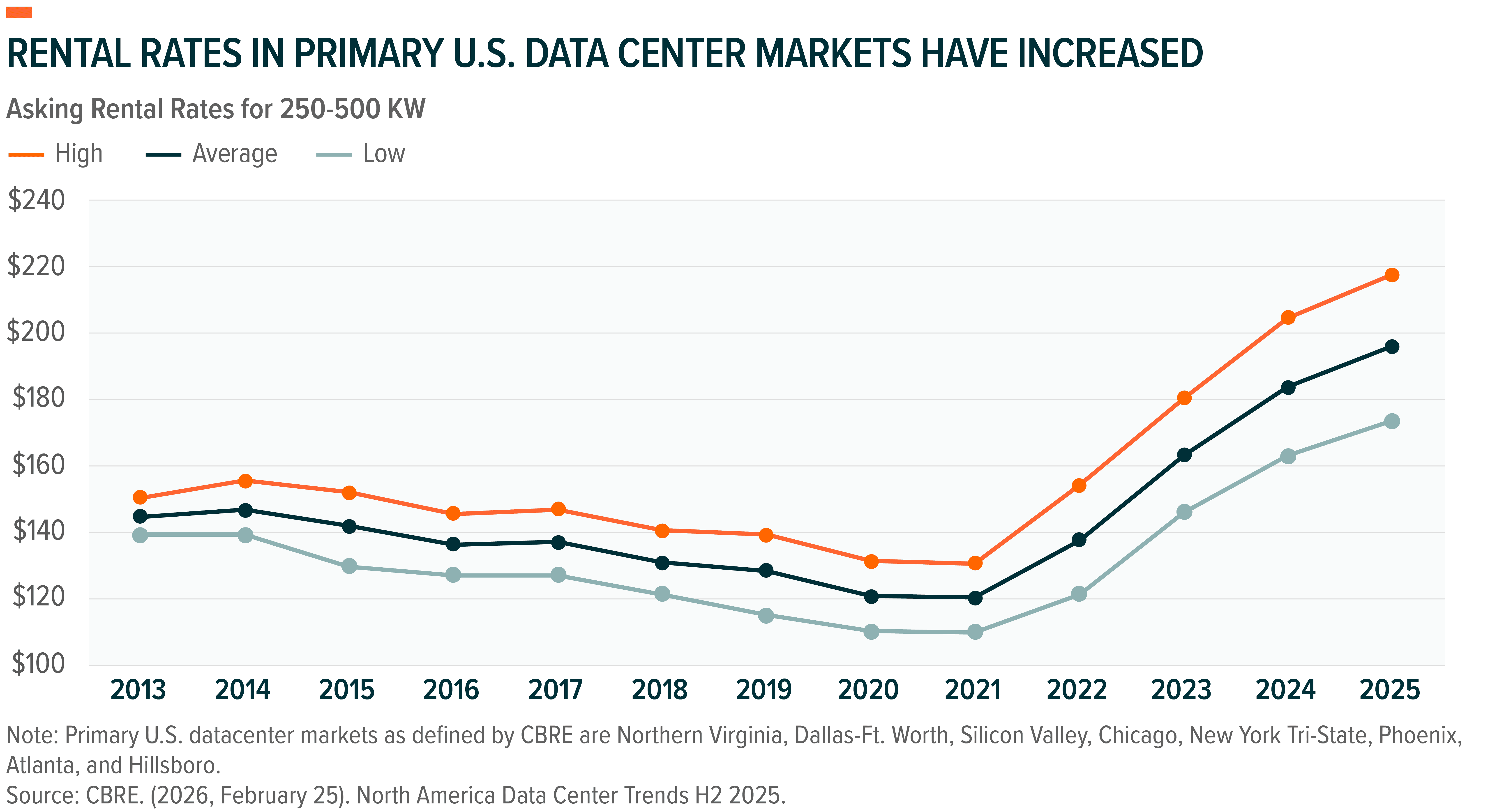

6. Rents Have Increased Because Capacity Is Scarce: North American lease rates rose +6.5% year-over-year (YoY) to $194.95/kW/month in 2025, the fourth consecutive annual increase.6 Growth has moderated from prior years’ spikes but remained well above historical averages – a clear signal of pricing power against record-low vacancy.

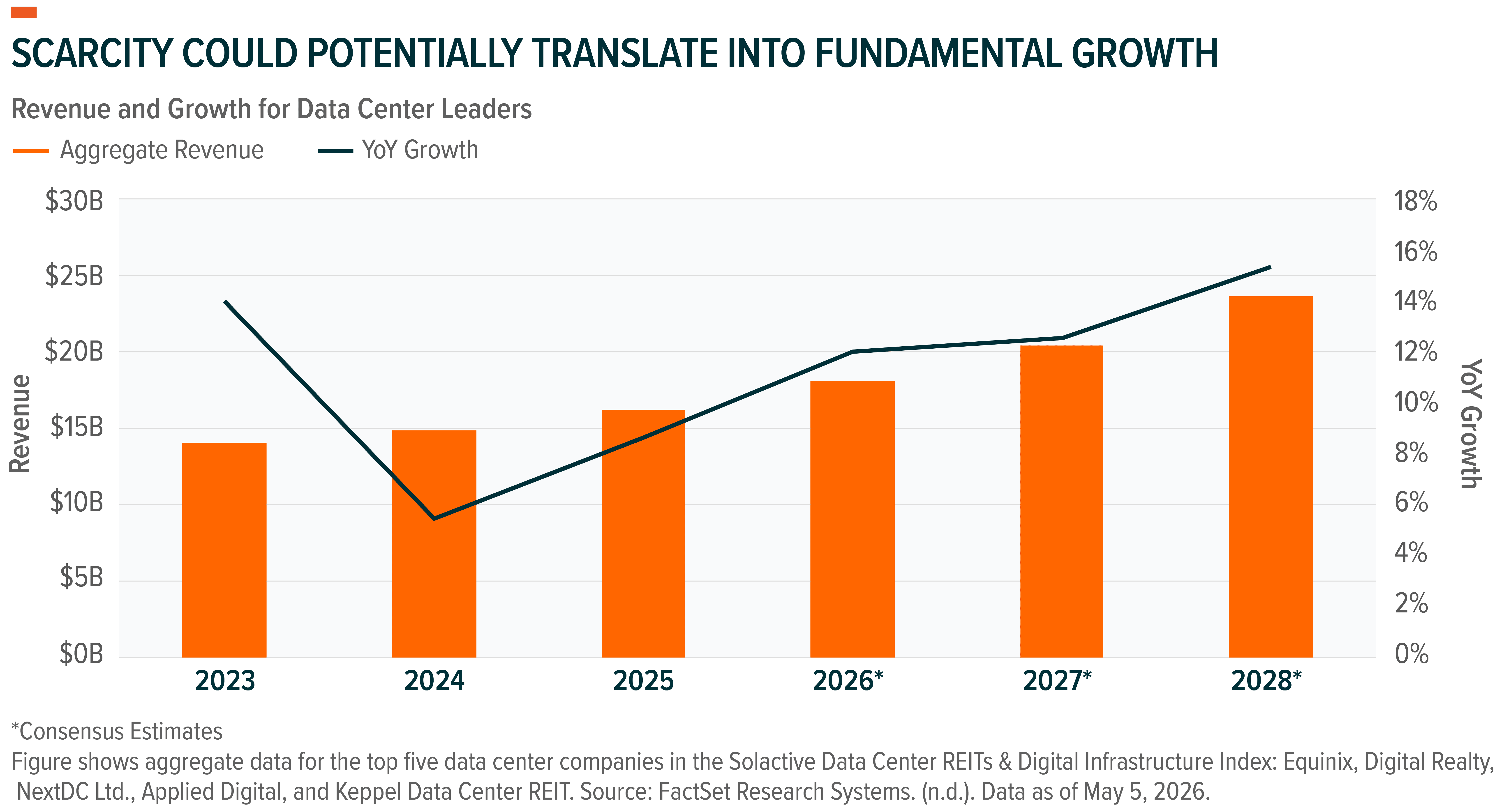

7. Data Center Fundamentals Set for Growth: The combination of rising rental rates (+6.5% YoY), mid-70% pre-leasing, and 1.4% vacancy produces what is, in our view, a contracted, multi-year revenue and earnings runway for scaled data center and digital infrastructure companies. In our view, that is what makes the group distinct, with AI-linked top-line growth supported by real estate investment trust (REIT)-style cash flows and asset backing.

Conclusion: Data Centers Are the Toll Booths of the AI Age

AI runs on infrastructure that is hard to replicate, slow to build, and increasingly pre-leased. As inference scales and AI moves deeper into the enterprise and consumer lives, operators that own powered, permitted, well-connected capacity are positioned to monetize one of the innovation cycle’s most important bottlenecks. In our view, data center operators offer investors a differentiated way to access the AI buildout – asset-backed, contractually supported, and structurally scarce.

Related ETFs

DTCR – Global X Data Centers & Digital Infrastructure ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.