Emerging Market (EM) debt, as measured by the JPMorgan EMBI Global Core Index, declined in a volatile first quarter of 2026, as an oil-driven geopolitical shock helped lifted U.S. Treasury yields and the dollar, widened credit spreads, and overturned the supportive macro backdrop that had prevailed early in the quarter.

Market Review

Emerging sovereign credit declined in the first quarter of 2026, with the JPMorgan EMBI Global Core Index falling 1.93%, as a supportive start to the year gave way to a sharp risk-off move following the U.S.-Israel attack on Iran and the subsequent jump in oil prices.1 This geopolitical event shifted market focus toward the inflationary consequences of higher energy prices, pushing U.S. Treasury yields higher and strengthening the dollar as investors priced in a slower path for global rate cuts. As major central banks moved into a wait-and-see stance, the risk of a prolonged closure of the Strait of Hormuz drove sharper differentiation within the EM debt universe, with energy exporting countries proving more resilient than more vulnerable importers. This produced clear dispersion within the asset class, with energy exporters such as Brazil and Trinidad and Tobago proving relatively resilient, while issuers more directly exposed to the regional conflict, including Bahrain, the United Arab Emirates, and Saudi Arabia lagged. The most notable underperformer was Ukraine, due to fading prospects for a near-term ceasefire, delays to external funding linked to Hungary’s blockage of an EU package, and early implementation risks around financial assistance from the International Monetary Fund Extended Fund Facility.

Fund Performance and Attribution

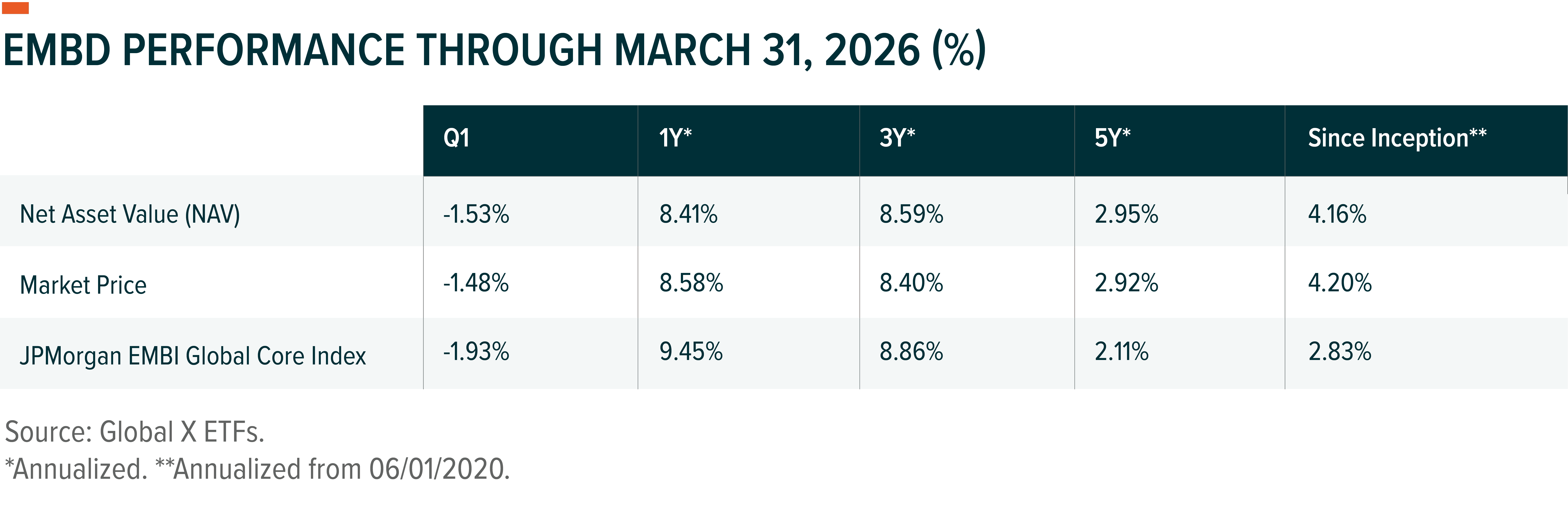

EMBD returned -1.53% (NAV) in 1Q26 versus -1.93% for its benchmark, resulting in 40 basis points (bps) of relative outperformance. On a price basis, the fund returned -1.48% (Market Price), outperforming by 45 bps. Relative performance was driven mainly by country allocation and security selection, with a smaller positive contribution from yield-curve positioning. The positive contributors were an underweight in Bahrain (8 bps), security selection in Egypt (8 bps), and an overweight in Brazil (6 bps), while higher cash and U.S. Treasury exposure also helped during the March risk-off move. These gains reflected positioning in credits less exposed to the direct fallout of the Middle East conflict and in selected energy-linked issuers. The main detractors were an underweight in China (-6 bps) and security selection in Saudi Arabia (-5 bps) and Poland (-2 bps). Overall, relative performance reflected differentiated country exposure to higher energy prices, geopolitical risk, and the fund’s conservative positioning.

The performance data quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Investors should not expect high short-term performance to be repeated. For performance data current to the most recent month or quarter-end, please click here. Total expense ratio: 0.39%.

The index tracks liquid, U.S. dollar Emerging Market (EM) fixed- and floating-rate debt instruments issued by sovereign and quasi-sovereign entities.

Outlook

We believe the outlook for EM debt has become more challenging, with risks tilted to the downside as the path to resolving the Middle East conflict appears difficult and a return to pre-war conditions in the Strait of Hormuz remains uncertain. For EM, this likely means a tougher backdrop of higher oil prices, tighter financing conditions, and weaker global demand expectations. Even so, many EM nations entered this period with stronger reserve buffers, healthier external accounts, and reduced near-term refinancing needs following substantial front-loaded issuance and liability management, which should help the asset class absorb volatility better than in prior energy shocks and may create selective opportunities if spreads adjust. In our view, the main risks are a more persistent energy shock, renewed U.S. dollar strength, and higher real yields, which could further tighten financial conditions and weigh most heavily on oil importers and lower-rated issuers with weaker policy flexibility. At the same time, further volatility could create more attractive entry points in issuers with stronger external buffers, as well as in higher-rated sovereign and corporate credits, particularly in Latin America.

We intend to remain positioned for a more selective and challenging environment, with an emphasis on country differentiation, valuation discipline, and downside resilience. In a market where higher oil prices, tighter financing conditions, and geopolitical risk are likely to keep dispersion elevated, we believe active country and security selection matter more than broad beta exposure.

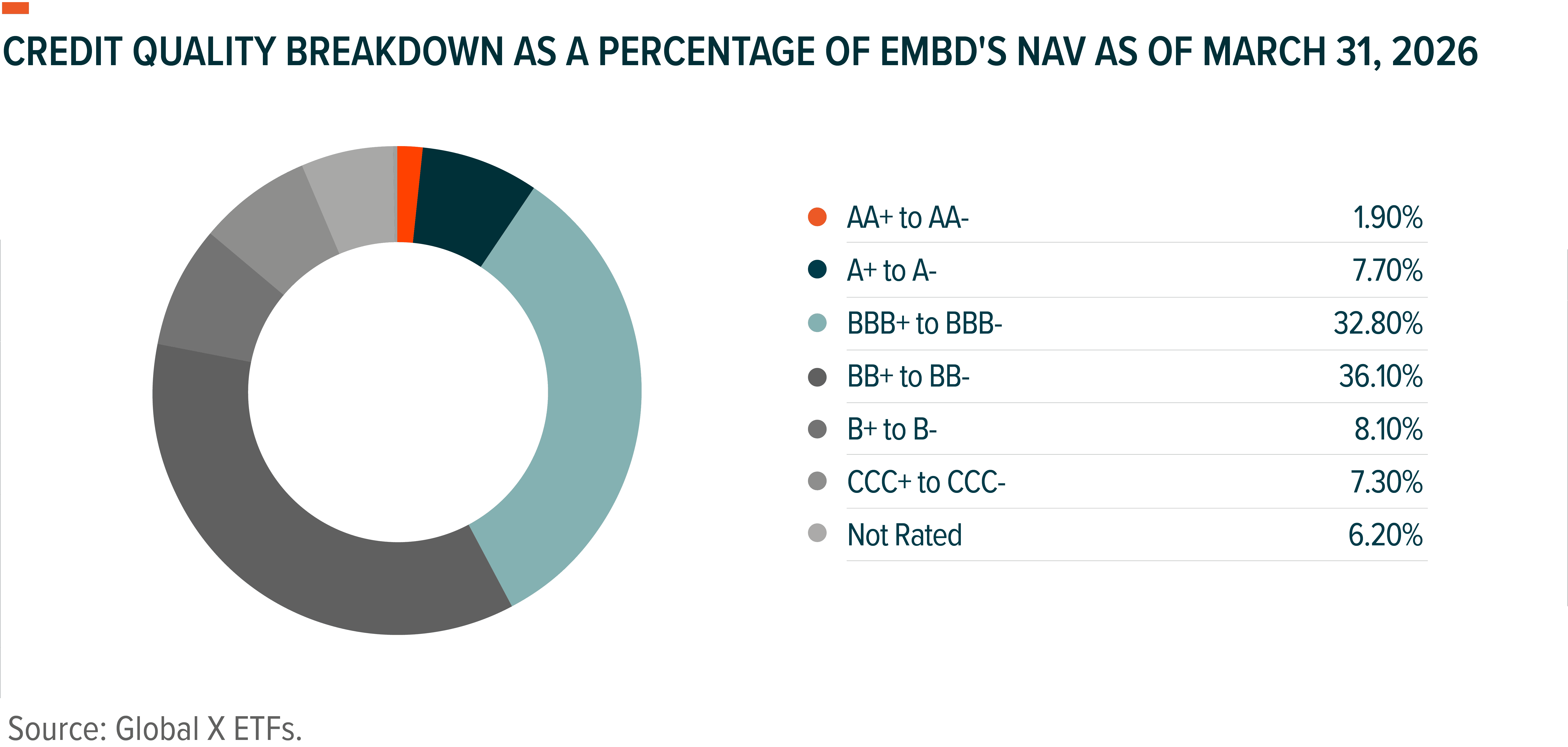

Credit Quality Methodology: All rated securities are rated by at least one of the three major rating agencies (Moody's, S&P, & Fitch). If more than one of these rating agencies rated the security, then an average of the ratings was taken to decide the security's rating. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest). Quality ratings are subject to change.

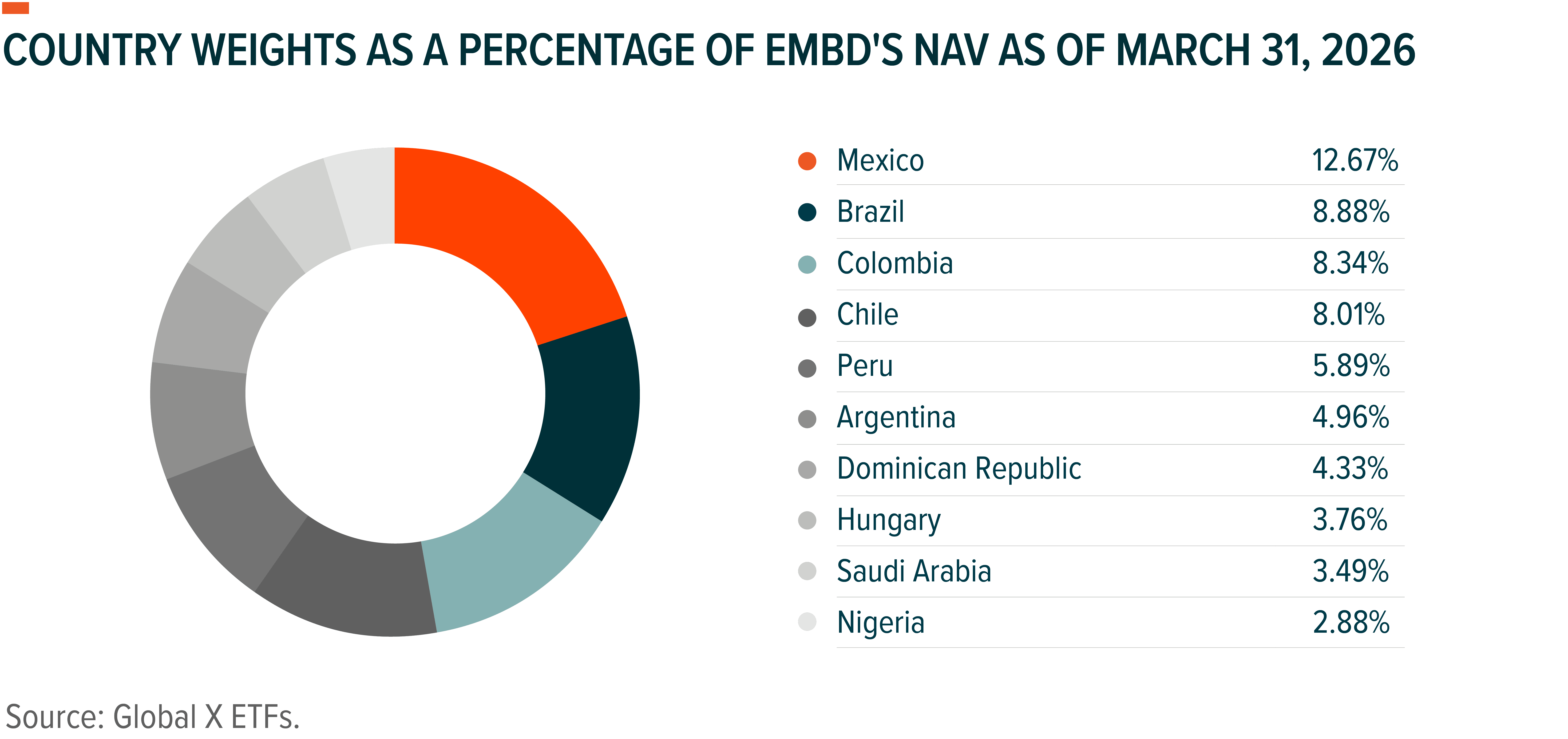

Geographic breakdowns are based on equity positions held by the ETF and exclude cash, currencies, and other holdings. Subject to change.

Related ETFs

EMBD – Global X Emerging Markets Bond ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.