Emerging Markets (“EM”) equities showed resilience during a volatile quarter, highlighting the potential benefits of diversification and creating a potential entry point into international assets.

Market Review

Emerging Markets equities, measured by the MSCI Emerging Markets Index (Net) (“the benchmark”), declined 0.17% in the first quarter, compared to a 4.35% decline in the S&P 5001. Despite Middle East led geopolitical volatility, EM assets proved relatively resilient, supported by their diversified composition and allocators’ search for value. Oil prices (measure by Generic 1st ‘CO’ Future) surged 76.49% during the quarter, driving outperformance in commodity producing countries, particularly energy exporters (outside of the Middle East), while energy importing countries lagged2. Colombia, Peru, and Brazil were among the strongest performers, while Indonesia, India, and the Czech Republic lagged. Mid-quarter pullbacks in Korea, Taiwan, and India were also notable.

Despite the geopolitical conflict, the U.S. Dollar Index (DXY) strengthened only 1.66%, leaving investors constructive on EM prospects3. A potentially dovish Federal Reserve System (Fed), elevated U.S. fiscal spending, and rising political uncertainty could pressure the dollar, which has historically supported EM performance by easing financial conditions, lowering foreign debt burdens, and supporting commodity prices. Attractive valuations, commodity exposure, structural reforms, and ongoing technology demand continued to keep the asset class in focus for allocators.

Fund Performance & Attribution

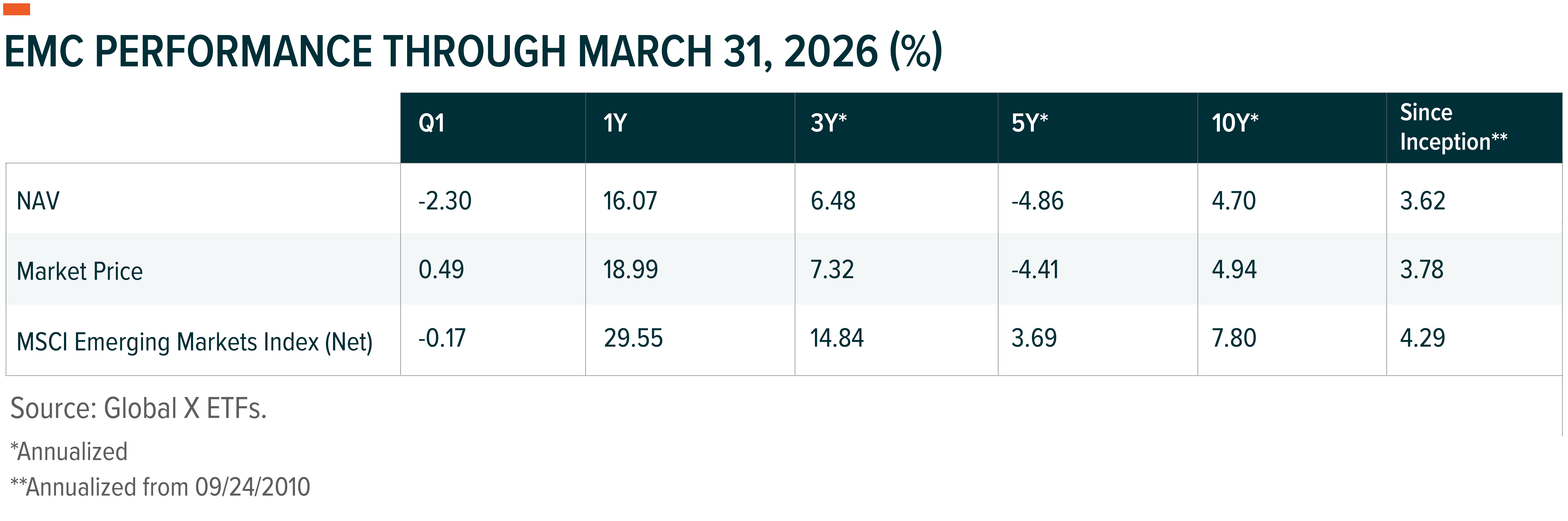

EMC returned -2.30% (NAV return) in 1Q 2026 versus -0.17% for its benchmark, for -2.14% of relative underperformance. EMC outperformed broader EM consumer segments, as the MSCI Emerging Markets Consumer Discretionary (Net) and Emerging Markets Consumer Staples (Net) indices declined 11.63% and 4.17%, respectively5. On a market price return basis, EMC closed the quarter up 0.49%6.

At the country level, the most notable contributions to returns came from stock selection in South Korea (0.85%) and Mexico (0.30%), along with an underweight to Indonesia (0.21%)7. The main detractors from returns came from stock selection in Taiwan (-0.94%) and China (-0.81%), along with an overweight position in India (-0.74%)8.

At the sector level, positioning in materials (0.13%), consumer staples (0.13%), and health care (0.09%) added value, while selection in communication services (-0.96%) and consumer discretionary (-0.62%), along with an underweight in energy (-0.44%), detracted9.

At the stock level, the fund’s positions in Samsung Electronics (2.12%) and SK Hynix (0.59%) in Korea along with Franco-Nevada in Canada (0.29%), added the most to performance10. The largest detractors included Xiaomi (-0.53%), Prestige Estates (-0.38%), and HDFC Bank (-0.33%)11.

Effective May 12, 2023, the fund acquired the performance, financial, accounting, and other historical information of the Mirae Asset Emerging Markets Great Consumer Fund. Performance shown prior to May 15, 2023 reflects the return of the Mirae Asset Emerging Markets Great Consumer Fund's I shares with a NAV conversion ratio of 0.47 applied in connection with the acquisition. Market price returns prior to that date reflect the predecessor fund’s NAV return.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent quarter- and month-end, please visit globalxetfs.com/emc. Expense Ratio: 0.65%.

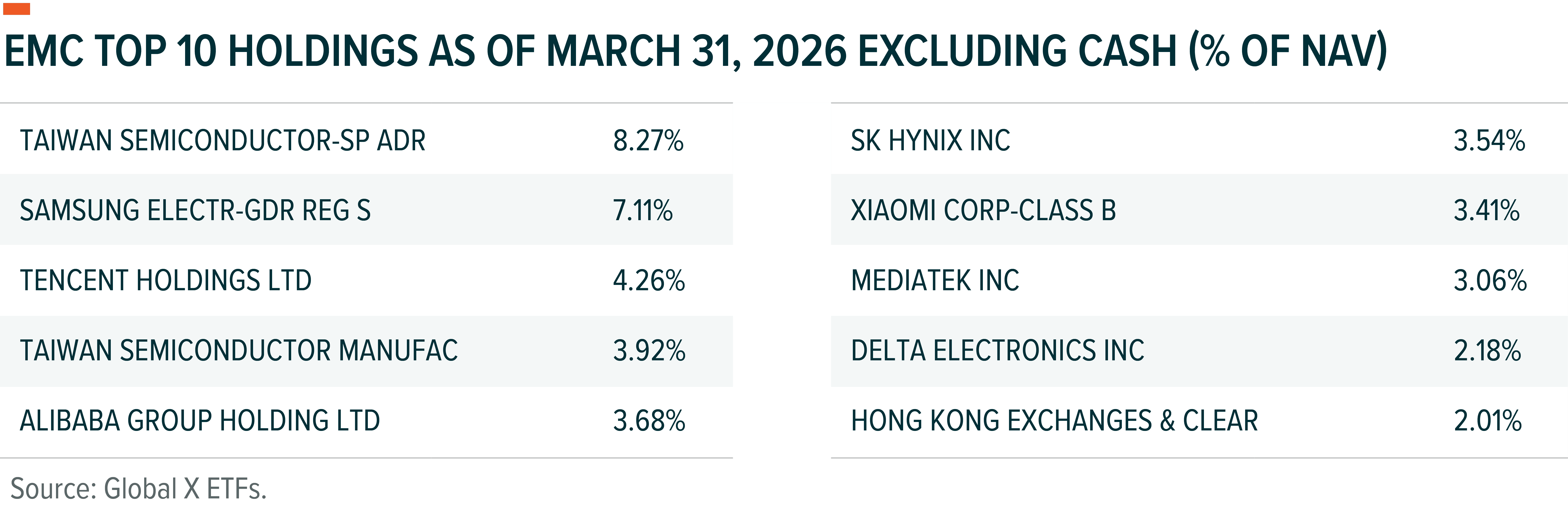

Holdings are subject to change.

Outlook

In our experience, three factors tend to drive emerging market performance: the U.S. dollar, U.S. interest rates, and China. These forces shaped prior cycles, including the 2001–2010 period when EM equities materially outperformed developed markets12. Today, elements of that backdrop appear to be re-emerging. A forthcoming new Fed Governor, a dollar trending toward mean reversion, and early signs of renewed stimulus in China suggest a more supportive setup. We also remain constructive on the technology cycle in North Asia, commodity exposure, political reform and monetary policy in Latin America, and the long-term structural growth story in India.

We believe active management remains critical, as potential outcomes across EM can vary. Companies that generate returns above their cost of capital, supported by strong management and disciplined balance sheets, should outperform. The strategy focuses on actively identifying businesses positioned to benefit from long-term secular growth in domestic consumption, while maintaining limited exposure to more cyclical commodity segments. EMC delivers bottom-up fundamental analysis with the fee structure, liquidity, transparency, and potential tax efficiency of its ETF wrapper, now with a lower expense ratio of 65 basis points.

Related ETF

EMC – Global X Emerging Markets Great Consumer ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.