The MSCI Brazil Index (Net) continued to show momentum and advanced over 19% in the first quarter,1 as allocators appeared to see value in single-digit valuation multiples, commodity exposure, easing monetary policy, and a meaningful political calendar.

Market Review

Brazilian equities posted strong gains in the first quarter of 2026, supported by higher commodity prices, resilient domestic demand, and improving fiscal expectations. Energy names led the rally, first driven by investors looking for value, cyclical, and asset heavy business models, and then eventually from the price spike resulting from geopolitical turmoil in the Middle East.

Brazil’s central bank also began a potentially impactful interest rate cutting cycle March 18. Looking at the past seven completed rate cutting cycles in Brazil, the average MSCI Brazil Index (Net) rally stood at roughly +95% (cumulative), where the average drawdown was around -15% (cumulative).2 While past performance is not a guarantee of future results, this historical context supports a potentially constructive return profile.

Last, Brazil faces an important Presidential Election later this year, and the market may be incorporating improving polling numbers from the opposition, as President Lula’s popularity continued to sink last quarter.3

Fund Review

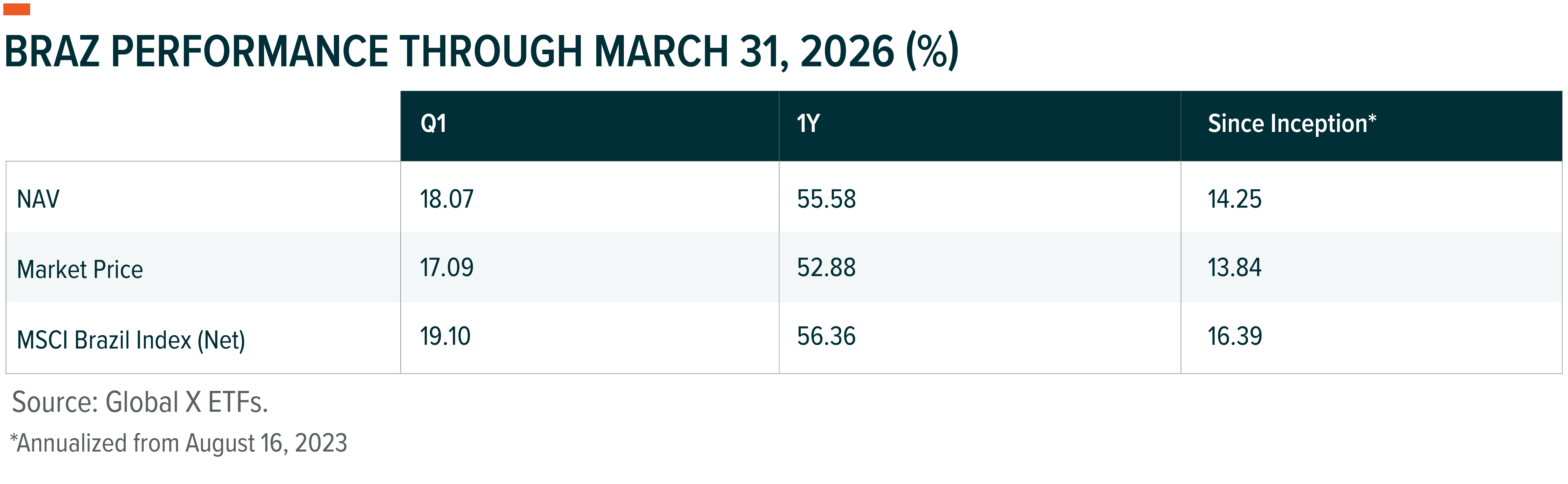

The Global X Brazil Active ETF gained 18.07% (NAV return) in the first quarter, taking 12-month returns up to 55.58%. The high teen performance slightly underperformed the 19.10% return for the MSCI Brazil Index (Net). While the fund slightly lagged, it captured most of the market’s upside, consistent with its focus on higher-quality compounders.

Sector positioning and stock selection within energy and financials drove positive attribution. Energy contributed 1.29%, supported by both Petrobras exposure and positioning in smaller peer, Petro Rio.4 Financials added 0.72%, led by positions in Itau, Banco Bradesco, and capital markets names that benefitted from expectations of coming rate cuts.5

Detractors came from consumer discretionary (-0.85%), communication services (-0.67%), and information technology (-0.49%).6 Stock-specific weakness drove most of the downside, particularly in names exposed to domestic consumption.

At the stock level, key contributions to returns came from CIA Paranaense de Energia (+1.03%), Petrobras ADR (+0.77%), and Banco Bradesco ADR (+0.62%).7 The largest detractors included the fund’s underweights in Vale (-0.91%), Sabesp (-0.74%), and Ambev (-0.47%).8

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. High short-term performance, when observed, is unusual and investors should not expect such performance to be repeated. Performance current to the most recent quarter- and month-end is available at https://www.globalxetfs.com/funds/braz/. Expense Ratio: 0.75%.

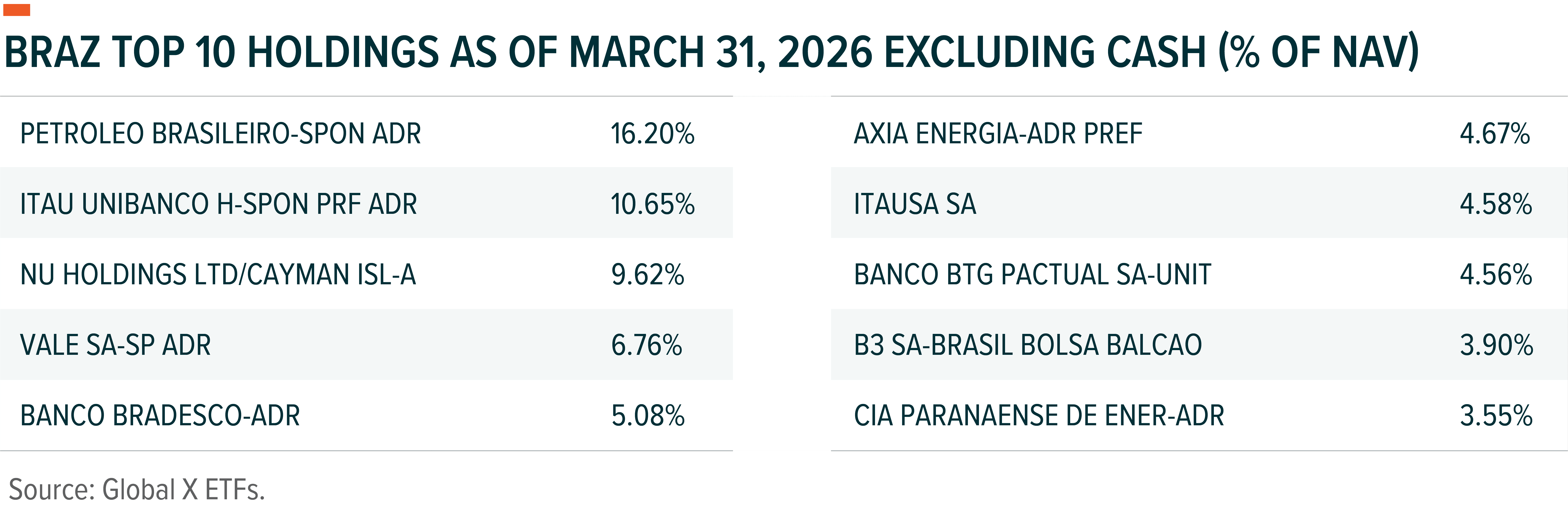

Holdings are subject to change.

Outlook

In our view, Brazil offers a constructive setup with geopolitical neutrality, attractive valuations, and leverage to global commodity demand. We believe Brazil could benefit from three key tailwinds.

- The central bank cutting rates could improve appetite for borrowing and spending, while also improving asset quality. Lower rates should also improve overall balance sheet strength.

- If the U.S. dollar returns to its weaker downtrend, this should help Brazilian companies levered in U.S. dollar debt and commodity producers as a whole.

- Last, Brazil faces an important election cycle and the market could reward incremental signs of political change and economic reform.

Recent global volatility leads us to believe that markets should reward balance sheet strength, capital discipline, and consistent cash generation. Our focus remains on a select group of high-quality companies we believe can compound return profiles above their cost of capital through different parts of the investment cycle. The fund targets high-quality Brazilian companies with superior returns on capital, disciplined leverage, and durable prospects for growth. BRAZ delivers bottom-up fundamental analysis with the fee structure, liquidity, and transparency of its ETF wrapper.

Related ETF

BRAZ – Global X Brazil Active ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.