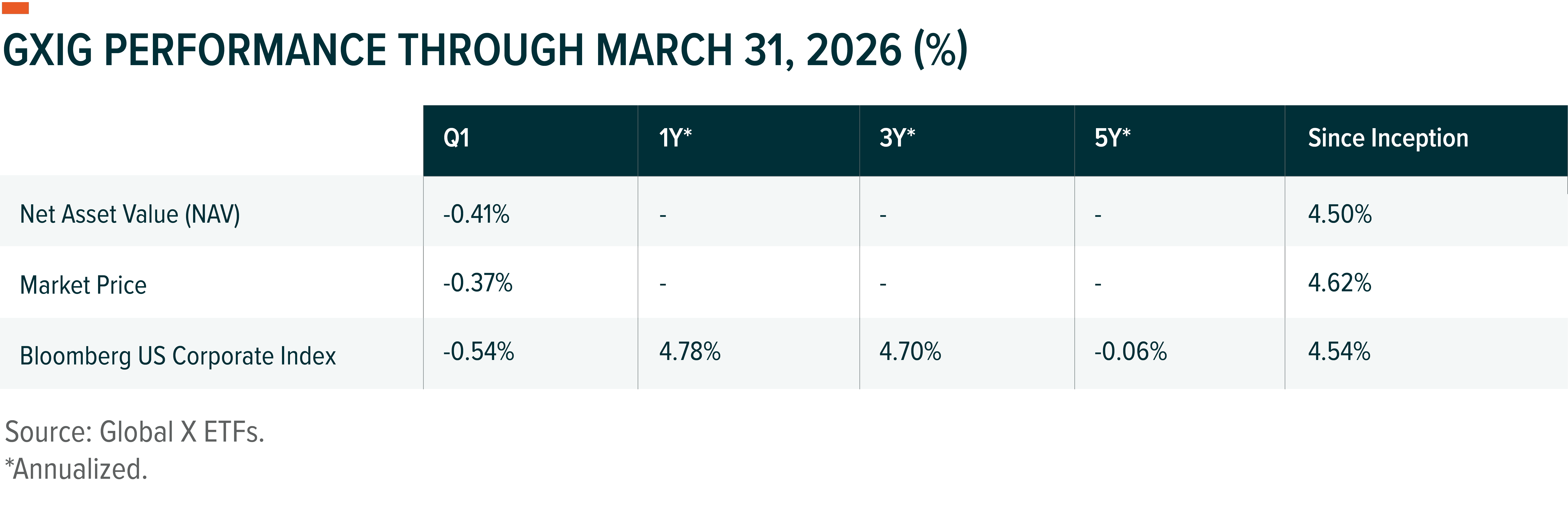

In the first quarter of 2026, despite a challenging environment marked by rising U.S. Treasury yields and widening credit spreads, the Global X Investment Grade Corporate Bond ETF (GXIG) outperformed the benchmark Bloomberg U.S. Corporate Index based on both NAV and market price, largely through favorable security selection.

The performance data quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance data current to the most recent month- or quarter-end, please click here. Total expense ratio: 0.15%. Inception date: 6/16/25.

The performance data quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance data current to the most recent month- or quarter-end, please click here. Total expense ratio: 0.15%. Inception date: 6/16/25.

Market Review

The Bloomberg U.S. Corporate Index recorded a return of -0.54% in the first quarter. An unfavorable environment due to reduced expectations for Federal Reserve (Fed) rate cuts, higher Japanese government bond yields, and the war with Iran negatively impacted performance.

At the beginning of the first quarter, expectations for Fed rate cuts remained elevated. However, as further deterioration in the labor market proved limited and inflation concerns increased, expectations for additional rate cuts declined significantly following the January Federal Open Market Committee meeting. In addition, the sharp rise in Japanese government bond yields exerted upward pressure on U.S. Treasury yields. While Treasury yields declined in February due to a correction in risk asset prices, they rose sharply again in March as oil prices surged following the outbreak of war between the U.S. and Iran.

Over the same period, U.S. Investment Grade (IG) credit spreads widened by 11 basis points (bps), with most of the widening occurring during February and March.1 In February, credit spreads widened as hyperscalers such as Google and Amazon once again announced significant increases in capital spending, reigniting concerns over bond supply, along with rising concerns about credit deterioration in private credit. In March, credit spreads widened further due to the war between the U.S. and Iran.

Fund Performance and Attribution

During the period, the fund outperformed its benchmark by 11 basis points (bps) (based on NAV), with a 6bps underperformance from yield curve positioning offset by outperformance of 4bps from sector allocation and 13bps from security selection.

In a rising Treasury yield environment during the first quarter, the fund’s duration overweight detracted 6bps from performance through yield curve positioning. However, in a widening credit spread environment, holding some U.S. Treasuries contributed 4bps of outperformance from a sector allocation perspective, while holdings in technology sector bonds added 13bps through security selection.

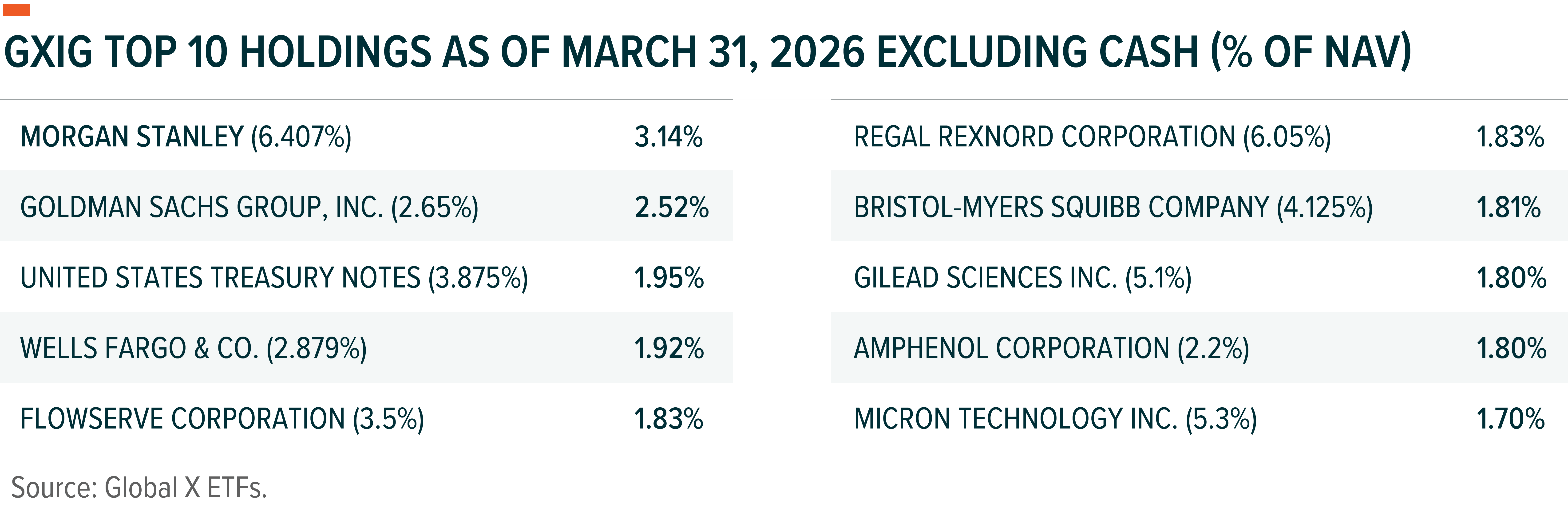

Specifically, technology companies such as Micron Technology and Google were key contributors to outperformance in security selection. On the other hand, issuers such as AT&T, General Motors, and Arthur J. Gallagher & Co. detracted from performance due to weak earnings, merger and acquisition announcements, and concerns about disruption from AI models.

During the first quarter, the fund reduced exposure to certain financial sector issuers in an attempt to avoid private credit-related risks. It also trimmed exposure to technology companies facing risks from heavy issuance or potential disruption from AI.

Holdings are subject to change.

Outlook

Despite a ceasefire, the outcome in the war between the U.S. and Iran remains uncertain. If a peace agreement is concluded and transit through the Strait of Hormuz resumes, we would expect to see lower oil prices, a weaker U.S. dollar, declining Treasury yields, and stronger performance in risk assets.

However, U.S. IG credit spreads are already tight by historical standards, and concerns over large-scale bond issuance by hyperscalers have intensified. As a result, we expect further spread tightening to be limited. In particular, certain issuers in the technology and communications sectors may be significantly affected by bond issuance, warranting caution.

Issues related to private credit are expected to persist, so we plan to continue avoiding companies with high exposure to private credit. Meanwhile, we feel the recent spread widening in some software companies appears to have been excessive and may present short-term trading opportunities.

The fund plans to maintain an overweight duration position in anticipation of declining Treasury yields and tightening credit spreads, while keeping a higher allocation to high-beta securities that tend to benefit in a spread-tightening environment. However, the fund will selectively avoid issuers where credit spreads are expected to widen due to bond issuance or idiosyncratic risks. The fund’s investment strategy and models will be monitored in an effort to flexibly adapt to changes in macroeconomic conditions and market dynamics, and positioning can be adjusted quickly if needed.

Related ETFs

GXIG – Global X Investment Grade Corporate Bond ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.