In the classic 1980s comedy Trading Places, Louis Winthorpe III and Billy Ray Valentine thwart the infamous Duke brothers, who had stolen a government crop report and attempted to use it to corner the frozen orange juice market. Compared to their OJ hijinks, today’s commodity markets are no laughing matter. Given continued supply-side challenges and the rise of trade barriers, these markets seem to more closely resemble the dystopian futures reflected in a Stanley Kubrick film.

By traditional definition, a commodity can be an economic good that is mass-produced or unspecialized, such as an agricultural or mining product.1 It can also be a good or service whose wide availability typically leads to smaller profit margins. In the increasingly automated world of rapid technological change and improved productivity, however, neither definition sounds particularly convincing nor representative of the opportunity.

We believe some definitional reframing is in order, as commodities will play a vital role in sustaining the ongoing automation and AI innovation boom central to today’s global economy. With supply chains tightening, investors may want to hone their understanding of these assets, the players involved in their production, and their structural impact within a portfolio.

Key Takeaways

- Commodity access and supply chain security are increasingly important to economic growth around the world, which should be reflected in the value of commodity assets over time.

- Growing uncertainty around resource security may prompt governments to replicate structures like the U.S. Strategic Petroleum Reserve to hold a broader array of resources.

- Commodities are underrepresented in investor portfolios, potentially making the current backdrop a compelling opportunity to consider strategic, long-term allocations.

Just Clockwork Oranges No More

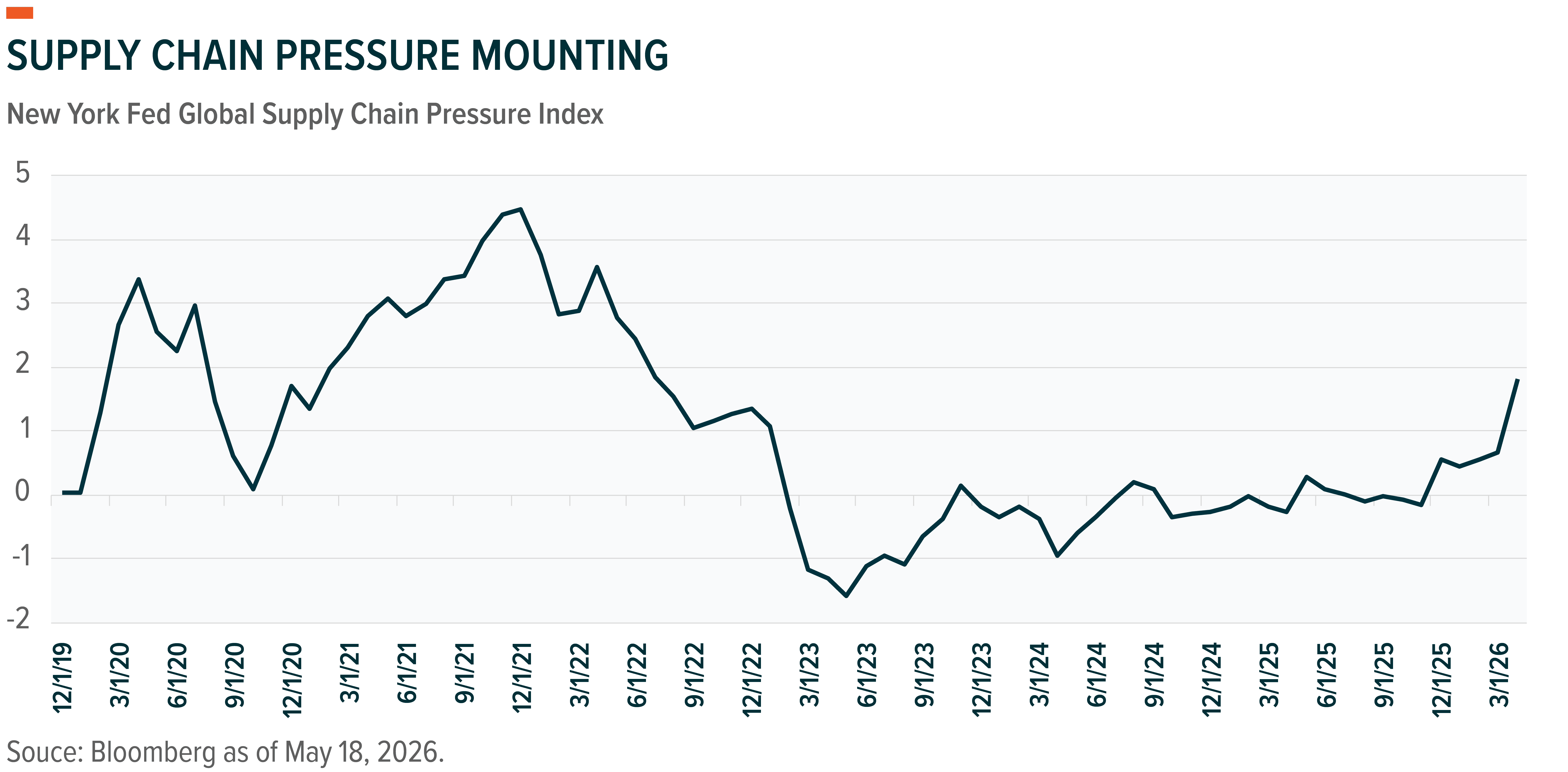

Based on any number of metrics, supply chains are under pressure. The World Bank’s Global Supply Chain Stress Index is close to the pandemic peak, and the Federal Reserve Bank of New York’s Global Supply Chain Pressure Index has risen in recent months.2 Some of these pressures can be linked to the conflict in Iran, but that is only the latest development in an increasingly complex trade environment.

After decades of increased economic integration, global interdependence is stalling out. Protectionist measures are becoming endemic to the modern economy, marked by tariffs, mercantilism, export restrictions, and investment barriers.3 Alongside these policy shifts are the concentrated production of certain industrial inputs, slower supplier delivery times, and threatened access to critical minerals and rare earths.

Recent months have been particularly disruptive. Natural disasters have taken production of critical industrial resources like copper offline.4 Low enriched uranium is in a structural shortage because national security concerns that have left a refining capacity shortfall.5 Costs of inputs like aluminum and lithium ion are higher due to tariffs.6 The closure of the Strait has affected resources beyond oil, including fertilizer and helium.

The treatment of commodities as a strategic priority is another emerging trend.7 The role they play in national defense is not necessarily a new issue, but growing defense budgets combined with the integration of AI into military capabilities mean that more raw and intermediate goods must be sourced.

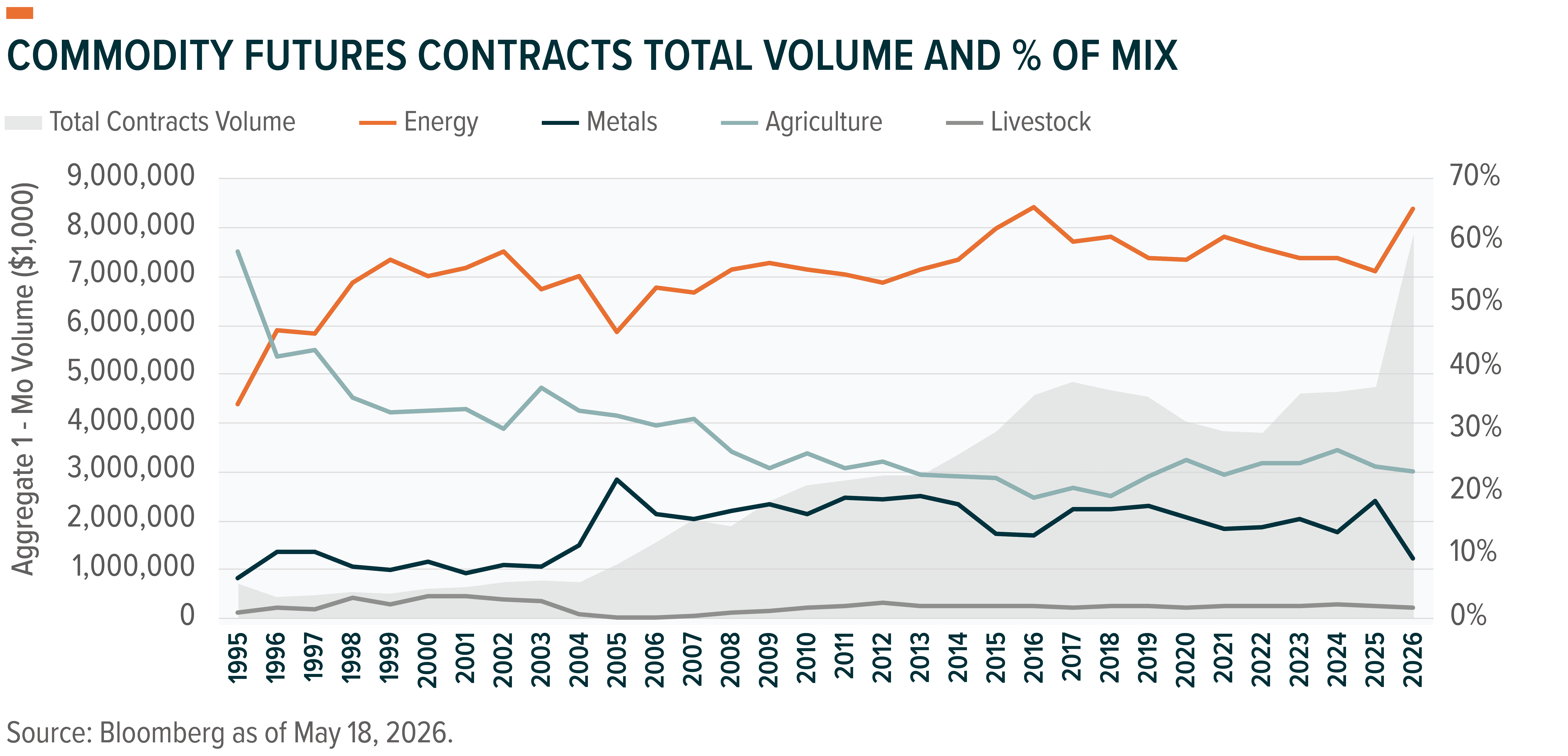

Taken together, securing essential inputs has become even more difficult exactly when demand to support the AI and tech buildout is surging. The massive data centers under construction require significant resources, from construction materials to copper wires for networking and power, to water for cooling. Unsurprisingly, trading in futures contracts across multiple commodities is on the rise, particularly energy and metals.

Beyond the Gold Metal Jacket

Commodity scarcity and intensified trading could raise the possibility of securing physical commodities at the national level. While the private sector and individual investors face storage constraints, governments have capabilities otherwise unavailable. For example, in 1975, as a response to the 1973–1974 oil embargo,8 the U.S. government created the Strategic Petroleum Reserve, which sits within the Department of Energy. Thirty-one other International Energy Agency member countries maintain similar mechanisms for energy reserves.9

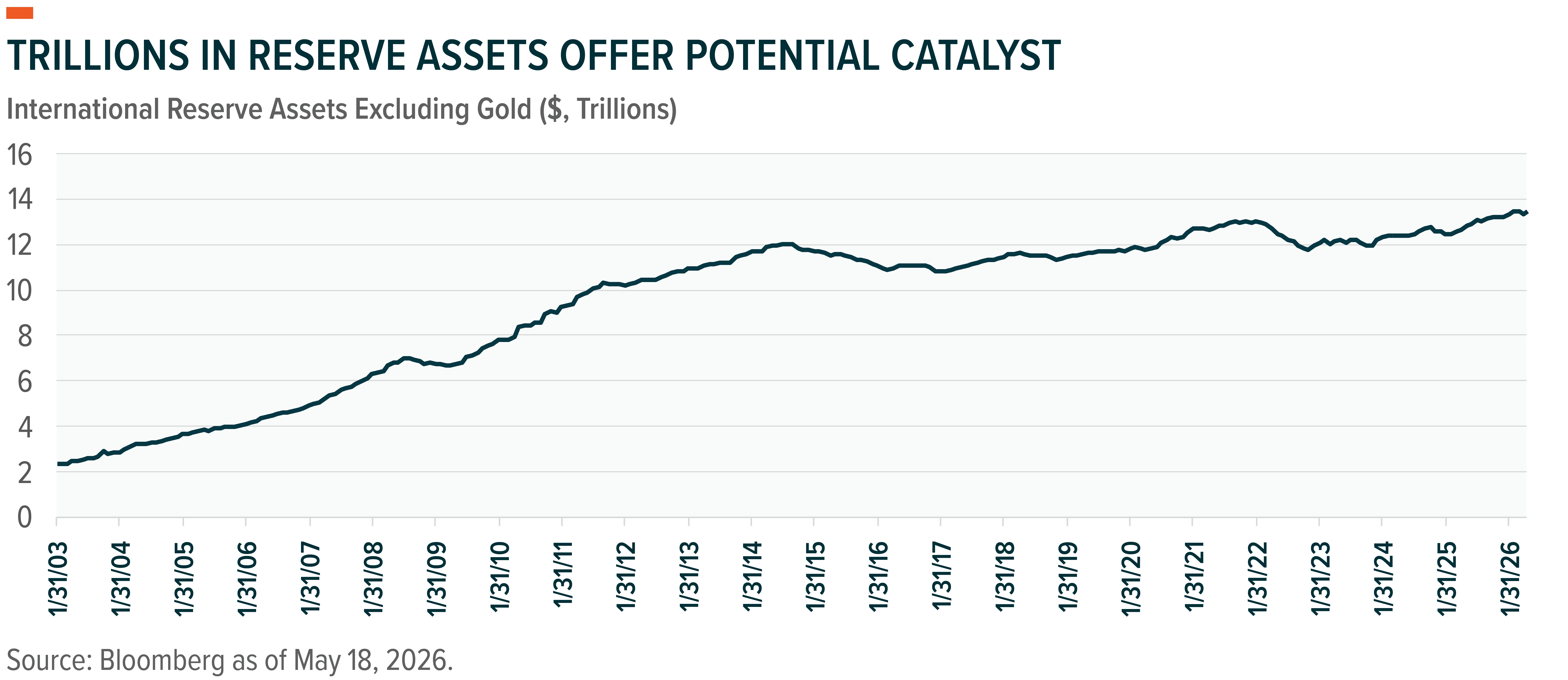

The appetite for hard assets is evident on sovereign balance sheets. Reserves excluding gold have now reached $13.4 trillion, up from $11.7 trillion in December 2019.10 Central banks have also diversified their holdings away from the U.S. dollar and Treasury debt, now owning an estimated 36,000–40,000 tons of gold valued around $4.5 trillion.11

Last year, central bank gold buying spurred a momentum trade as investors looked to diversify outside the U.S. In retrospect, the U.S. economy seems relatively well positioned, and questions about the relative value of buying or holding gold have emerged after the record price increase.12 With gold facing this scrutiny, the critical need to secure industrial metals and rare earths creates an opportunity.

A scenario exists where central banks could redeploy their balance sheets away from stores of value like gold toward commodities with greater economic utility. Such a shift would represent a sea change, but there is precedent.13 The U.S. holds critical materials in its National Defense Stockpile.14 China maintains extensive reserves of industrial minerals like zinc, cobalt, copper, and rare earths.15 Japan, South Korea, and India maintain modest stockpiles of specific materials, while Europe and Australia are in the process of establishing national reserves.16 This could create a tailwind for commodities beyond market forces.

How I Learned to Stop Worrying and Love Commodities

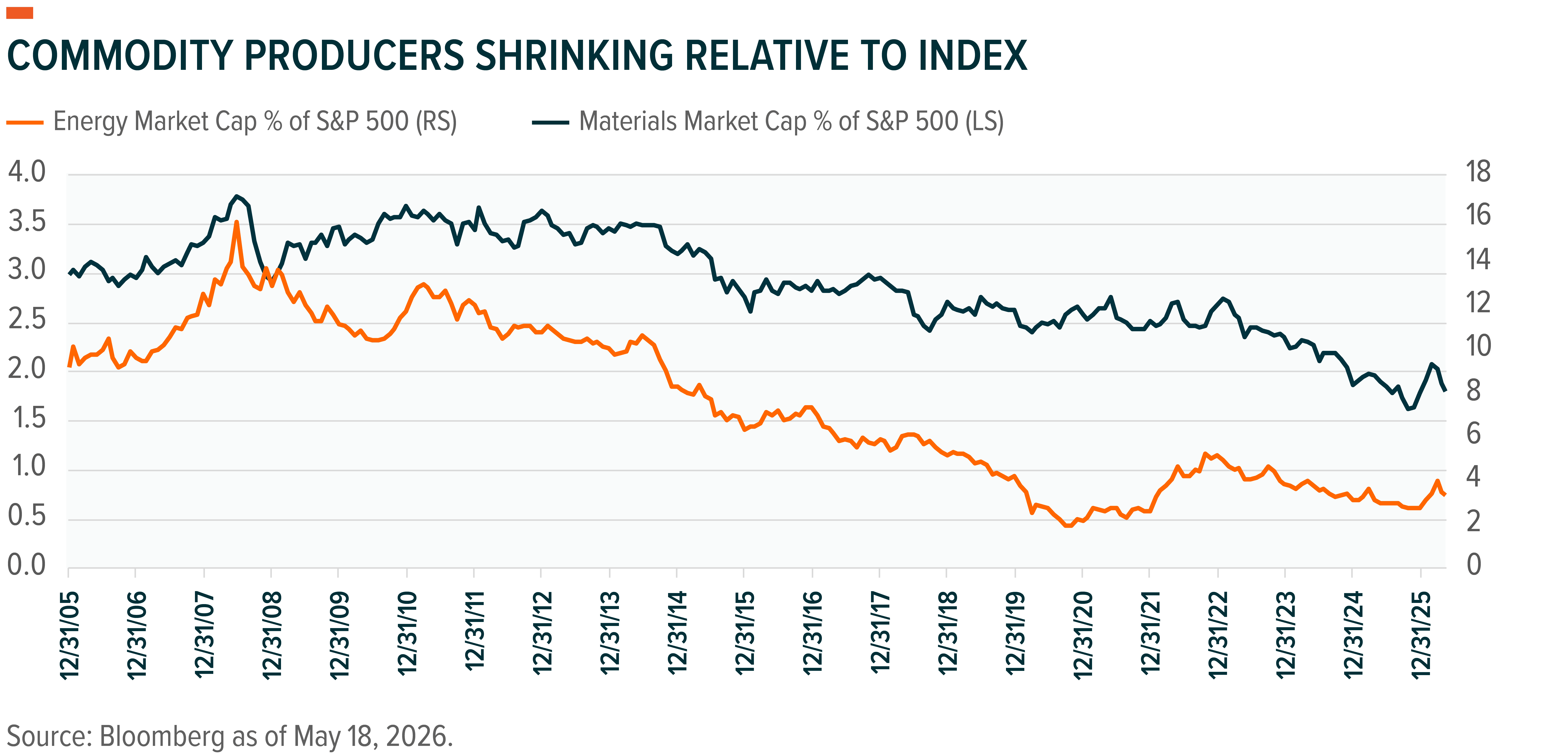

Commodity producers may be positioned for improved growth and profitability in the coming years, but portfolio positioning remains light. While commodity transaction volume has moved higher, ownership has not extended to commodity companies. The materials sector’s share of S&P 500 market cap has declined from a peak of 3.8% in 2008 to just 1.8% today, while the energy sector has declined from 16% to 3%.17 The rapid market cap growth of mega-cap tech is partly to blame.

But a powerful shift in the commodity complex is underway. Given the recent events with Iran and the resulting oil bottleneck, the energy sector is up 23% year-to-date. Materials is the third best-performing sector, gaining almost 13%. Industrials, which has exposure to chemical manufacturing, is up 11%.18 The market seems to be reevaluating the value proposition behind these businesses as expectations for margins and growth reach record levels. Materials companies are expected to grow earnings 54% by the end of 2027. Margins are forecast to improve from 10% in 2025 to 13%.19

We believe the secular demand for resources amid the rapid expansion of digital and traditional infrastructure and grid electrification will help power the next commodity cycle. The introduction or expansion of national resource reserves could add further fuel to this trend, potentially unlocking significant investment and acquisition activity.

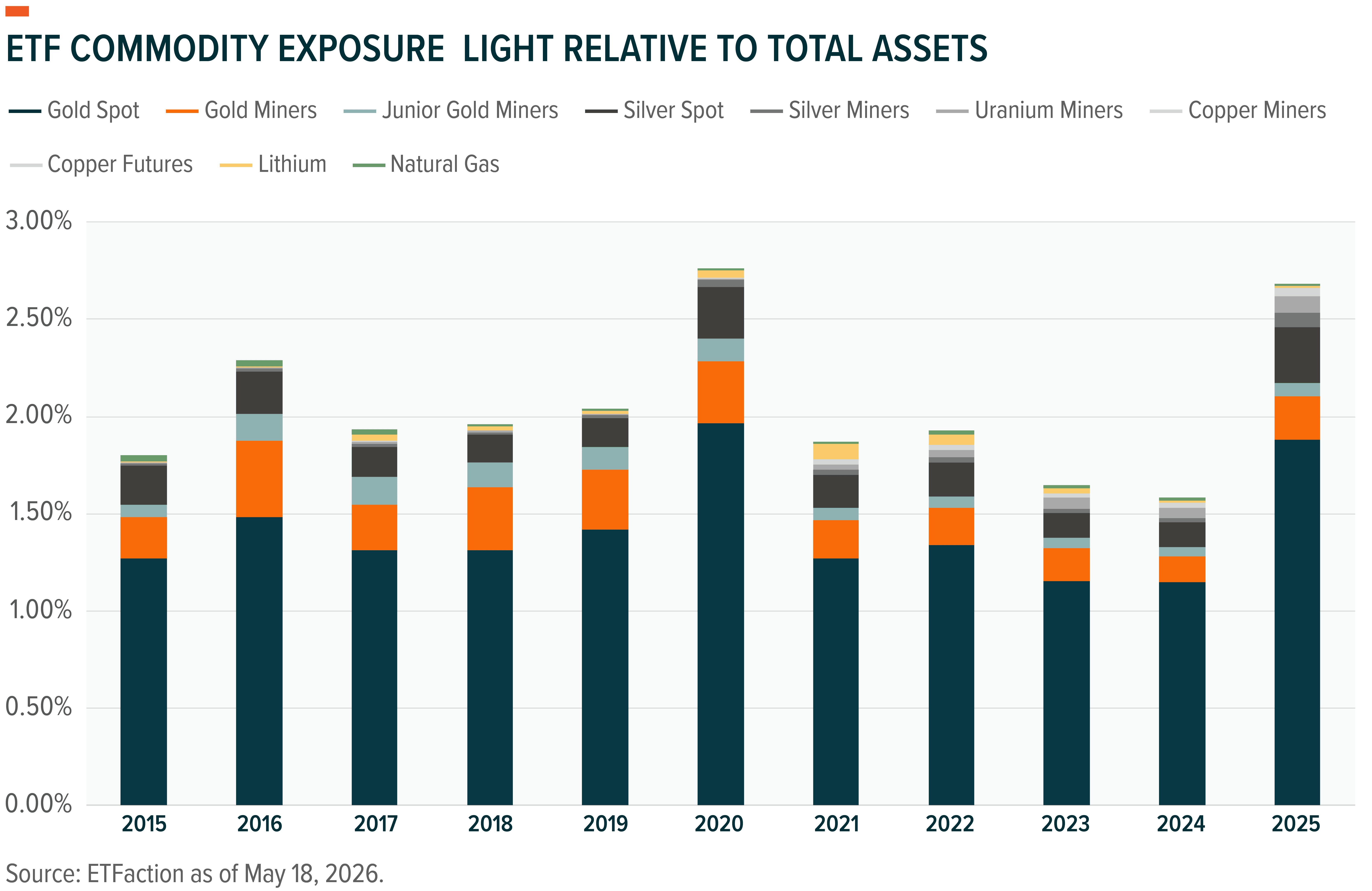

The strategic benefits of increasing commodity exposure within a portfolio are gaining credibility. According to a CFA Institute study, a 10% allocation to commodities can help lower portfolio volatility with only a minimal drag on returns.20 The study came to this conclusion by replacing 10% of the equity basket in a 60/40 allocation with a broad-based commodity index. Current allocation to commodities and commodities producers is nowhere near those levels. Historically, commodities have represented 2% to 3% of assets based on Morningstar classifications.21

ETF ownership, which includes exposure to commodity producers and commodities directly, reflects a similar pattern with much of asset base skewed to gold. Producers of industrial metals like copper and lithium remain relatively under-owned.22

Both broad-based and more targeted exposure to the commodity complex may make strategic sense, depending on specific portfolio objectives. For more targeted exposure, three distinct strategies offer compelling entry points: industrial metals, rare earths and critical minerals, and energy.

Industrial metals cover a broad range of materials, including copper, aluminum, lead, iron and steel, nickel, and others. Though sometimes viewed as a precious metal, silver is the world’s most conductive substance, making it a key input in high-end electrical processes. Silver has been in a structural deficit for five years with a shortfall of 800 million ounces annually.23 Copper, the second most conductive metal, also faces a shortfall after a mudslide at the Grasberg mine in Indonesia is expected to remove more supply from the market than the world's third-largest mine produces in a year.24 Copper has numerous use cases, including the internal wiring in data centers and reinforcing a stretched electrical grid.

Rare earths and critical minerals have garnered significant attention of late, especially given China’s threat to cut off the U.S. supply. The 17 distinct elements that comprise rare earth materials are not heavily traded, but there is strong demand across numerous sectors, from computing to clean energy.25 The most effective way for most investors to gain exposure may be through producers.

Lithium, which is not a rare earth, is a critical material that should benefit from energy constraints on the AI buildout.26 Once viewed as a corollary for the growth of electric vehicles, high-end batteries are important to data centers, which must maintain consistent energy loads. Supply constraints are accelerating globally, underscored by Zimbabwe, the largest producer in Africa, banning the export of raw concentrate. The ban effectively removes 10% of the global mine supply.27 Similar to lithium, the adoption of hydrogen cell technology could increase as well over time.

Finally, the Iran conflict has exposed deep risks in the global energy market. With energy supply chains attempting rapid restructuring to address the Strait closure, U.S energy assets may be well positioned to capture market share over time. At a minimum, those assets offer a degree of energy security for the U.S. economy and defense industrial base. Hard assets like energy pipelines and transfer do not offer direct commodity exposure, but they are an adjacent asset that should have less cyclicality based on the structure of long-term contracts. U.S. energy exporters, particularly within the liquified natural gas (LNG) space, also seem well positioned to gain market share.