Markets generally price in the impact of geopolitical events relatively quickly and then look past the short-run effects to focus on the future.1 Through World Wars, Cold Wars, and nuclear crises, the global economy has continued to grow and evolve. Markets respond accordingly.

The big question investors face today: Does the Iran conflict disrupt economic trends, delay economic activity, distract investors, or results in some combination thereof? Prior to the start of the conflict, the U.S. economy was on a rather healthy glidepath, having largely absorbed the tariff shock.2 The global economy’s temperature: not too hot, not too cold, probably just right.

There are, however, major geopolitical shifts at play and we look to Hamilton’s King George for some advice. Global relations increasingly resemble mercantilist systems of the past, where countries focused on improving economic strength through all manner of policy levers. At the same time, the unipolar peace dividend of the post-Cold War 1990s seems like a bygone era with rapid increases in military spending and the transition to a version of decentralized deterrence. That leaves investors to chart a path through a new world of geopolitical coordinates.

Key Takeaways

- The Iran conflict does not seem sufficient, at present, to disrupt major U.S. economic trends, but higher input costs could dampen consumer demand and corporate investment.

- Forecasts for earnings and economic growth have actually risen since the start of the Iran conflict, a notable divergence between fundamental expectations and market action.

- A rapid end to the military action could result in a relief rally, but given the uncertainty, strong secular themes with lower risk relative to the market (beta) and those that may be oversold seem attractive.

What Comes Next?

Blockade, perhaps. Negotiations on one week. Maybe negotiations off by the next week. While the diplomatic path remains uncertain, the physical degradation of Iran’s strategic assets provides a more objective baseline for expectations.

At the end of March, intelligence reports suggested that at least one-third of Iran’s missile stock and approximately 90% of its production capabilities had been destroyed.3 The final offensive operations that targeted Kharg Island and other strategic assets may have degraded that capability further. The Iranian regime’s ability to project force outside their borders is likely a shadow of what it was before Operation Epic Fury, putting the country’s position as a regional hegemon in question.4

Make no mistake, the military operation targeted Iran, but the strategic targets were Russia and China. After trying to pressure Russia to reach an agreement in Ukraine by reducing oil prices, the Trump administration pivoted by cutting off a primary supplier of drones and other weapons.5

The message to China was likely two-fold. Following Beijing’s decision to cut off critical minerals to the U.S. for a brief period last year, the Strait of Hormuz’s closure serves as a reminder that China also faces supply chain pressure points.6 The U.S. has underwritten freedom of navigation, critical to China’s energy supply since World War II, and that benefit is now at risk. Second, the U.S. wants China to stop supplying weapons to proxy states. This signaling, however, appears to have backfired, with China doubling down on military support for Iran and scheduling large scale military exercise in the South China Sea.7

By military standards, the operation seems successful, and the list of remaining strategic targets in Iran is probably quite short. In other words, the U.S. and Israel are looking to end the operation because there’s not much left to do, short of regime change.

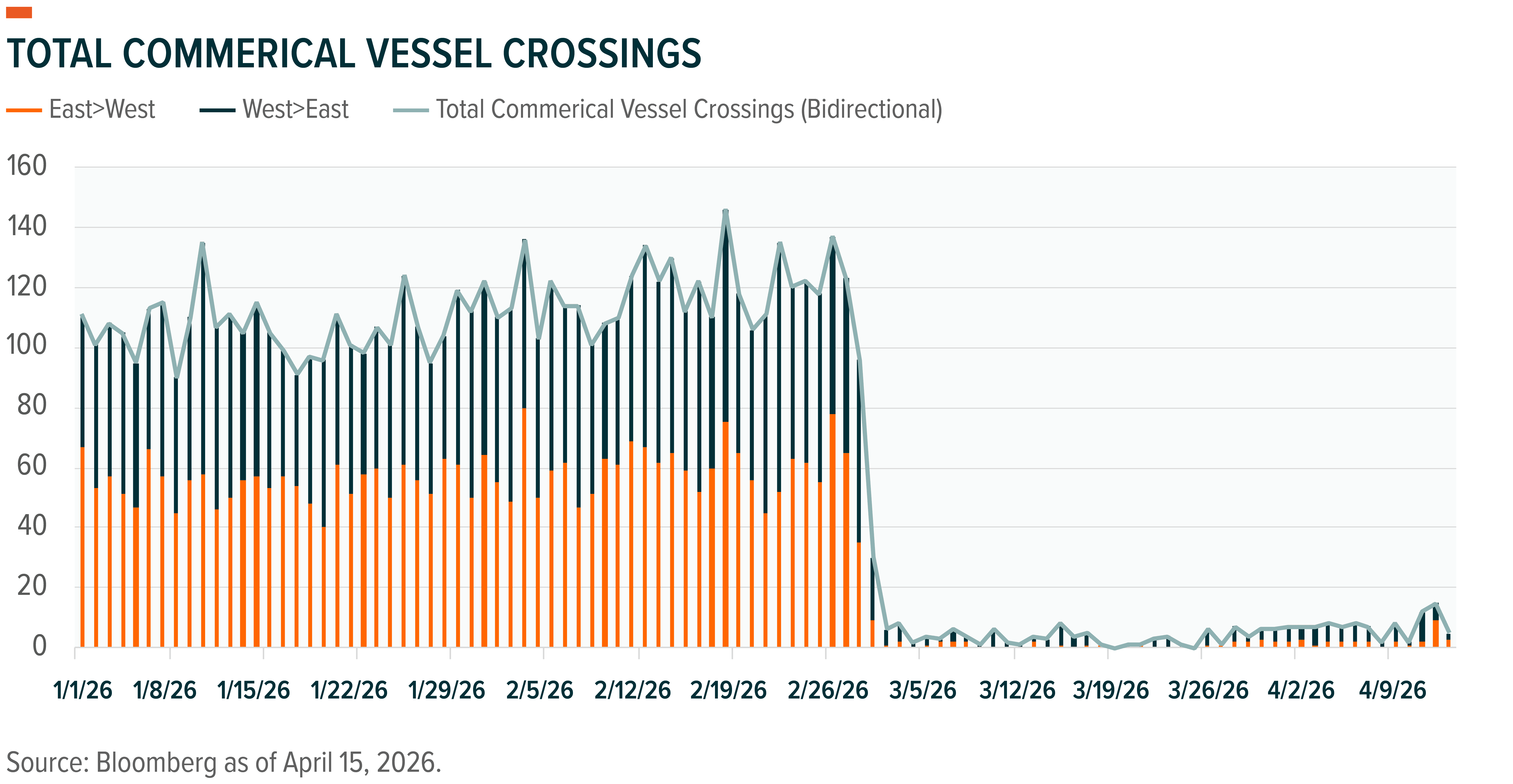

The question is whether the U.S. can find an exit that looks like a strategic victory. Iran remains reasonably intransigent in communications, vowing to outlast President Trump. Iran’s proposed 10-point plan may be a way for everyone to save face, but the public terms are far from an ideal endgame for the U.S.8 Meanwhile, Iran temporarily opened then closed the Strait as negotiations progress. Shipping has been just 10% of the normal traffic levels, meaning only a fraction of the $2 billion in daily oil flow is making it to the global market.9 There are of course other resources being constrained as well.

The challenge of reaching a lasting ceasefire is complicated by the competing factions within Iran. With the theocracy and Iranian Republican Guard (IRGC) weakened by the loss of top officials, the political class has gained power to negotiate with external parties, but it lacks a unified voice. While the theocracy likely controls the foreign ministry and the IRGC still controls the domestic economy, politicos are trying to improve their positions through foreign negotiations.

In addition, Iran has structured its military into 31 autonomous combatant commands, intending to achieve deterrence through redundancy.10 As a result, it is difficult to know who is firing missiles at neighboring countries and imposing a blockade of the Strait.

Global powers have always pushed their limits, but real shifts in the geopolitical order are rare, and the U.S. remains the only country capable of global force projection. While the conflict is likely nearing an end, a strategic victory may prove elusive if Iran can monetize control of Strait and China proceeds with its wargame.

You’ll Be Back

Despite everything, the U.S. economy may be well positioned to take all this geopolitical turmoil in stride. The economy was pretty strong to start the year, and as we expected, growth expectations were revised higher for a third straight year.11

That said, job growth is anemic. Inflation remains a little above the post-2000 trend.12 Markets have pushed out the next Fed cut to mid-2027. Delinquencies are rising. Cracks are showing in private markets. Yet, nominal year-over-year growth was healthy at the end of 2025, driven by continued consumption and corporate investment.13

Inflation concerns have dominated the headlines since the Iran conflict began. Higher energy prices may push costs higher, but inflationary pressure in the latest reports has been pretty muted.14 Perhaps the bigger risk is demand destruction, whereby growth slows due to reduced consumer spending in areas ex-energy or companies cut back on capital expenditure.

Another risk is that companies maintain their current investment levels but reallocate from projects that boost return on investment towards projects focused on resilience. For example, companies may shift resources from automation projects that improve margins to supply chain diversification to protect against further shocks. Communication throughout the current earnings season may provide insight into these trends.

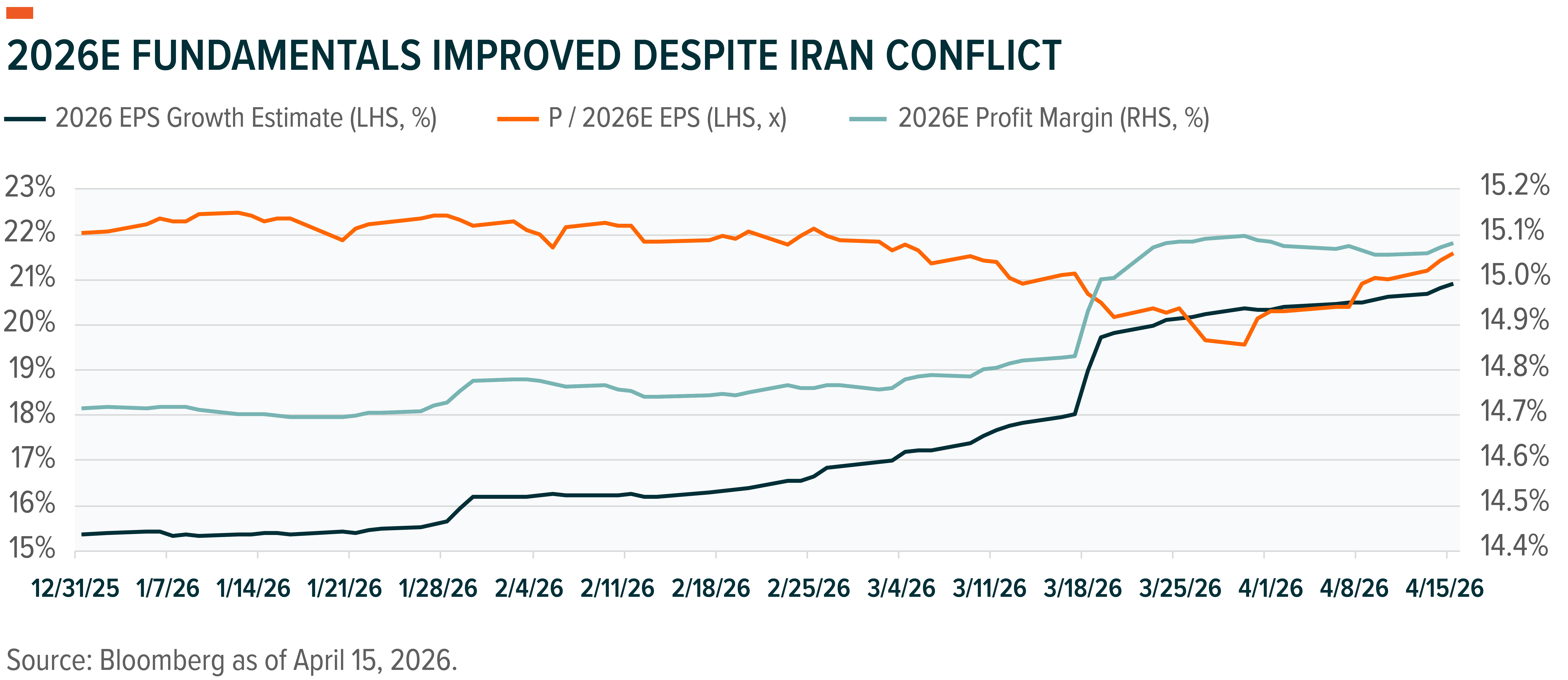

While the impact of the Iran conflict is starting to show in the latest economic data, forward expectations remain reasonably optimistic, and reasonably may be an understatement.

Consensus expectations for 2026 S&P 500 EPS growth were 16% at the start of the year.15 At mid-April, they were revised up to 21%. Profit margin forecasts were bumped up from 14% to 15%, despite potentially higher input costs from elevated energy prices.16 During the conflict’s first six weeks, markets dropped by as much as 8%, and realized volatility jumped from 13 to 18.17 The S&P 500 recovered those losses and moved to all-time highs, but volatile price action has followed headlines rather than upward trending expectations.

The schism between headline volatility and consensus expectations is somewhat confusing. Either markets should just look past the conflict and embrace the optimistic forecasts, or expectations are not being revised fast enough to reflect the challenges companies face. EPS growth of 22% would be the best since 2018, excluding the 2021 post-pandemic recovery, and only the seventh time that profit growth has exceeded 20% since 1991.18 Most of the other instances followed recessions. So, it would seem there is a combination of exceptional resilience and profitability being priced into markets.

It’s possible that inflation might not pass through to earnings in any meaningful way. In 2022, companies faced almost 20% inflation, and in 2025, they dealt with the prospect of higher tariffs.19 In both cases, they reaffirmed guidance, met expectations, and hit near-record profit margins. The accelerated inflation tied to slightly higher energy prices the past few weeks does not seem like a major risk factor going into earnings.

I Know Him

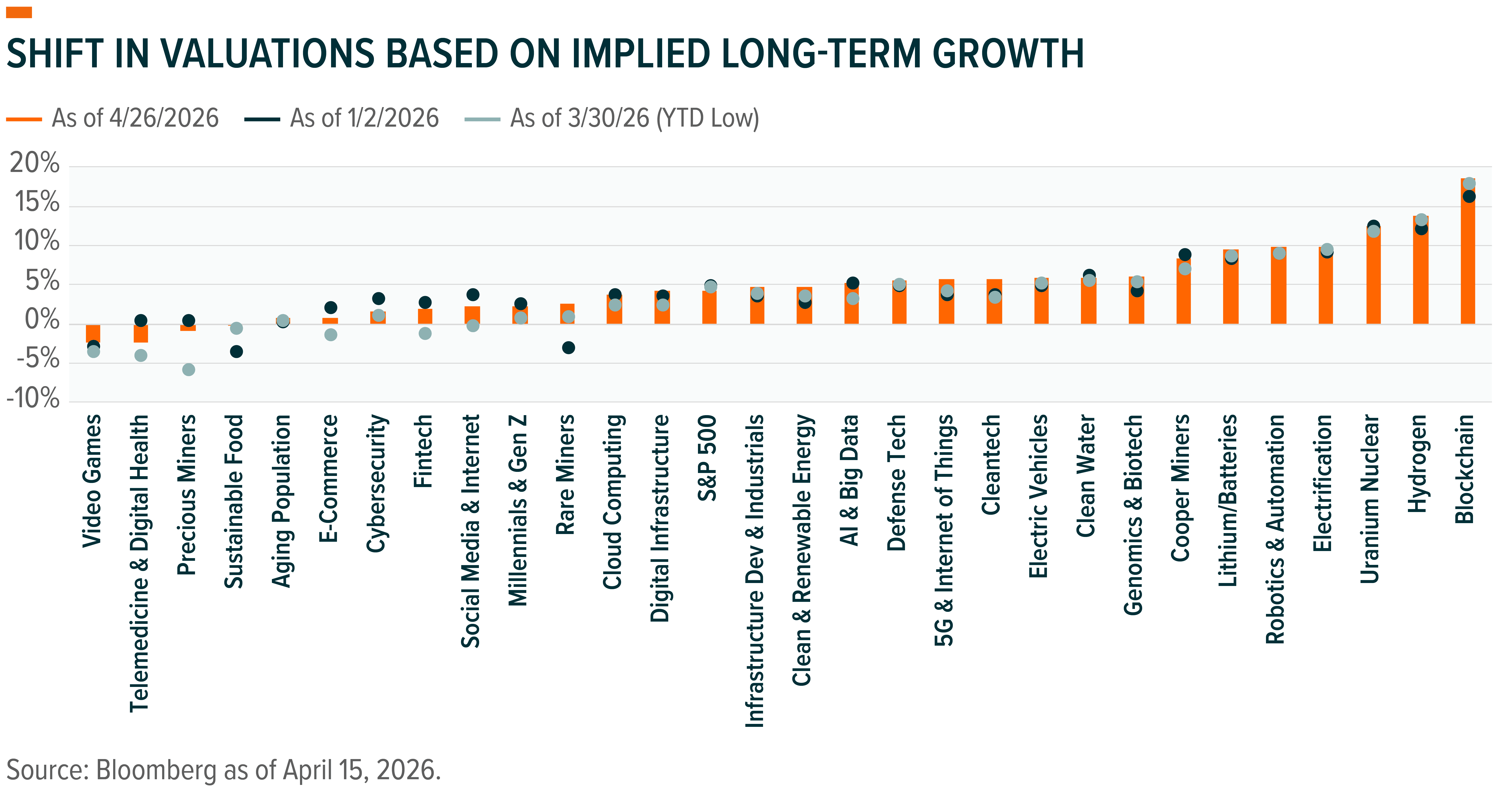

The volatility and risk of demand destruction aside, the market could move higher quickly. If there is a reasonable settlement and geopolitical tensions cool, the S&P 500 could easily move past 7,300, given multiples at the start of 2026 and current earnings forecasts.20 That said, this may be a time to get targeted with strategies.

Themes that have a strong secular tailwind but are typically less volatile than the market may provide market exposure while helping to manage day-to-day volatility. Defense tech is a prime example. Defense spending is usually consistent, and the associated companies are typically lower beta as a result.21 More recently, the fiscal year 2026 national defense budget, the first to hit $1 trillion, is a significant step change in spending, and that just may be the start.22 The White House is requesting $1.5 trillion for fiscal 2027, and with the Iran conflict and China’s saber-rattling, the likelihood of passage is higher. On top of that, the Iran conflict may well be funded by a $200 billion supplement, lifting next year’s defense budget to $1.7 trillion, which should help to drive revenues meaningfully higher.23

Data centers is another theme with strong secular tailwinds and reasonably stable cash flows that may help in volatile conditions. The recurring revenue business model creates relatively sticky cash flows, as moving data platforms can be costly and time-consuming.24 Further, storage and memory availability may be one of the major gating issues in the AI buildout.25 Current data center owners and operators already have compute, storage, and memory capabilities, and they may benefit from improved pricing power in the event of a shortfall.

The U.S. electrification theme also has a solid secular thesis, with companies that are typically lower beta than the market. Energy demand is increasing as AI and automation adoption presses forward, but the U.S. has underinvested in its grids and clean energy. In his State of the Union address, President Trump called on tech companies to meet their own power needs, which will likely be powered by nuclear and natural gas.26 Power providers and companies helping to support improvement in the energy grid are likely to stay very busy.

A second strategy worth considering involves themes that have sold off considerably and offer high growth potential at reasonable valuations. Cybersecurity is one such example.27 Newly released AI tools are changing the software calculus; as companies gain the ability to build customized software, the build-vs.-buy calculation shifts. Most firms, however, are unlikely to build their own cybersecurity software, which should keep many of the established providers profitable.

A tactical opportunity tied to U.S. energy assets may be available as well. Whether the Strait remains opens in the coming weeks or not, U.S. energy infrastructure and development are probably more valuable today than before the conflict. The risk to global supply chains has increased, and the U.S. is the largest exporter of oil and gas in the world.28 MLPs offer exposure to energy infrastructure with stable cash flows, while LNG exploration and export may be poised for accelerated growth.