Round and round we go. While the military operation in Iran, February’s weak jobs report, downside revisions to growth, and the recent software selloff all warrant detailed attention, they also provide an opportunity to examine a broader context of the circular logic currently running through the market. Stress-testing prevailing wisdom is usually a healthy practice anyway, and that’s especially true when arguments resting on soft assumptions become more of a distortion than a prudent decision-making tool for investors.

In this piece, we examine three narratives and their possible logical fallacies that make this environment particularly complex. The first is relatively noisy macro data creating a loop of interpretations regarding the economic cycle and the potential interest-rate path.1 Second, the equity rotation into traditionally cyclical stocks coincides with mounting fears about tech’s long-term growth trajectory, a narrative that ignores the fact that these cyclicals require AI adoption to thrive.2 Further amplifying that concern is a potential link between investment in AI and possible accounting issues, which we believe is a thin argument given the strong fundamentals of the hyperscalers and enterprises leading the way.3

Key Takeaways

- A first-half rate cut remains on the table given increased economic and geopolitical risks, but the other side of the story is that economic conditions remain generally constructive with healthy year-over-year growth and slowing inflation.

- The market rotation into cyclicals is backed by fundamentals, but AI and automation technologies are likely critical to meeting mounting expectations.

- Fears over the circular nature of AI investment appear to be overdone and seem to ignore the rapid growth and adoption of the technology.

Macro Merry-Go-Round

Recent macro data has not painted a clear picture. Some evidence points to a slowing economy with higher inflation, fueling a stagflation narrative; yet the same data could be interpreted in the opposite direction: a precursor to accelerating growth and price stabilization.4 Falling back on Occam’s razor, the simplest explanation is usually the best, we continue to believe the data show that the economy is healthy and do not subscribe to fearmongering.

Three main culprits distorted recent data releases. First, the government shutdown and the decline in public funding slowed GDP growth, a drag that should reverse. Second, a backlog of delayed economic reports forced comparisons across different time periods, an issue that is slowly resolving. Third, distortions from the pandemic, yes from 2020, remain issues, particularly regarding employment.

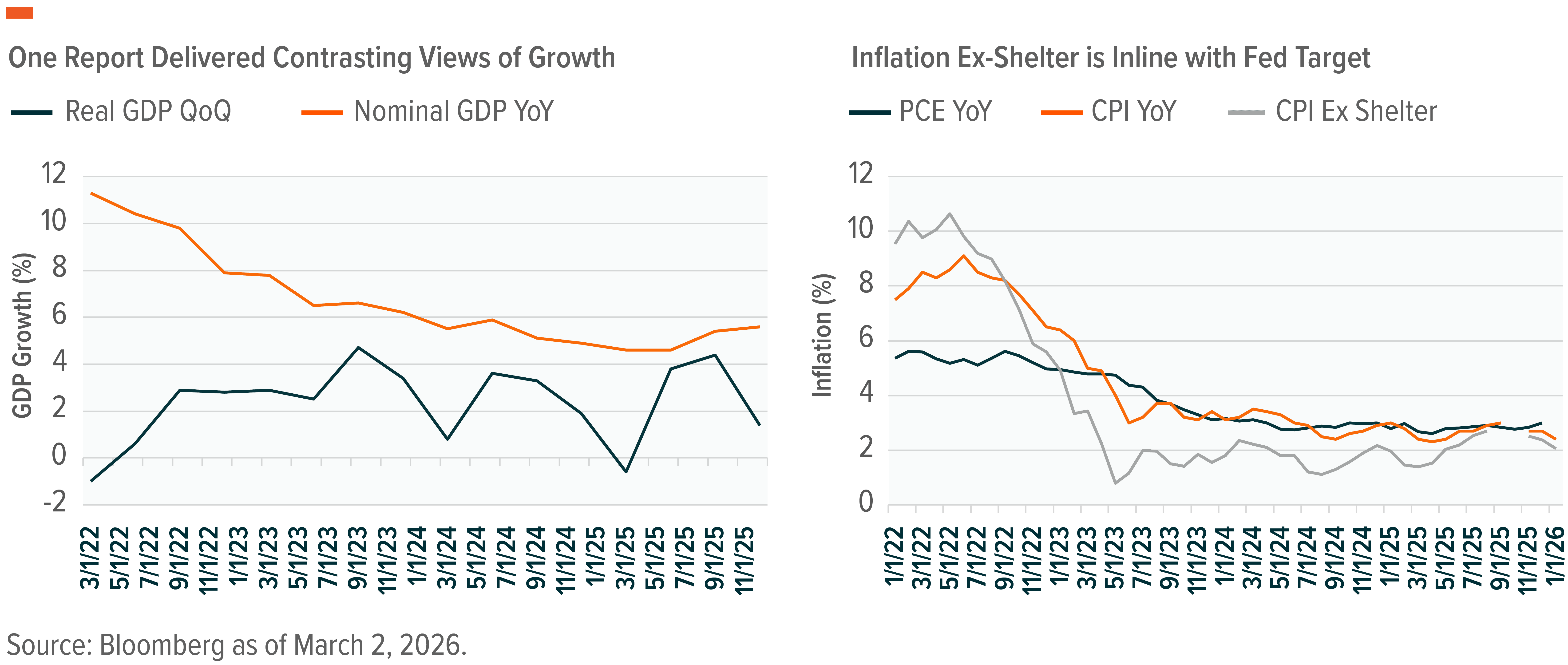

Quarter-over-quarter GDP growth was revised down from 1.4% to 0.7% for Q4 and meaningfully below consensus expectations for 2.0%.5 The miss was largely due to the falloff in government spending and exports; meanwhile, real consumption and investment were up 2.0% and 3.3%, respectively. On the inflation front, the Fed’s preferred metric, the PCE price index, came in higher than expected at 2.8% for January.6 The biggest drivers of inflation remain shelter and utility costs, which potentially hints at stagflation.

Interpreted through a different lens, there’s an argument that economic growth accelerated in Q4. Year-over-year, nominal growth was 5.4%, and a modest improvement on Q3’s 5.4%.7 Consumption expanded at 5.0% and nonresidential investment was up 7.9%, a good sign for continued mid-cycle expansion. The February CPI data also tells a different story; the headline number was 2.5%, but excluding shelter, consumer inflation was 2.1% almost spot on the Fed’s target.8 Together, these results reflect an economy growing at a reasonable rate with stable prices.

The irony is that both interpretations would dictate the Fed stands pat. In a low-growth/high-inflation scenario, the Fed should be concerned about price stability. In a high-growth/low-inflation scenario, there’s no reason to lower rates further. Currently, there is only a single rate priced into the market by December 2026.9

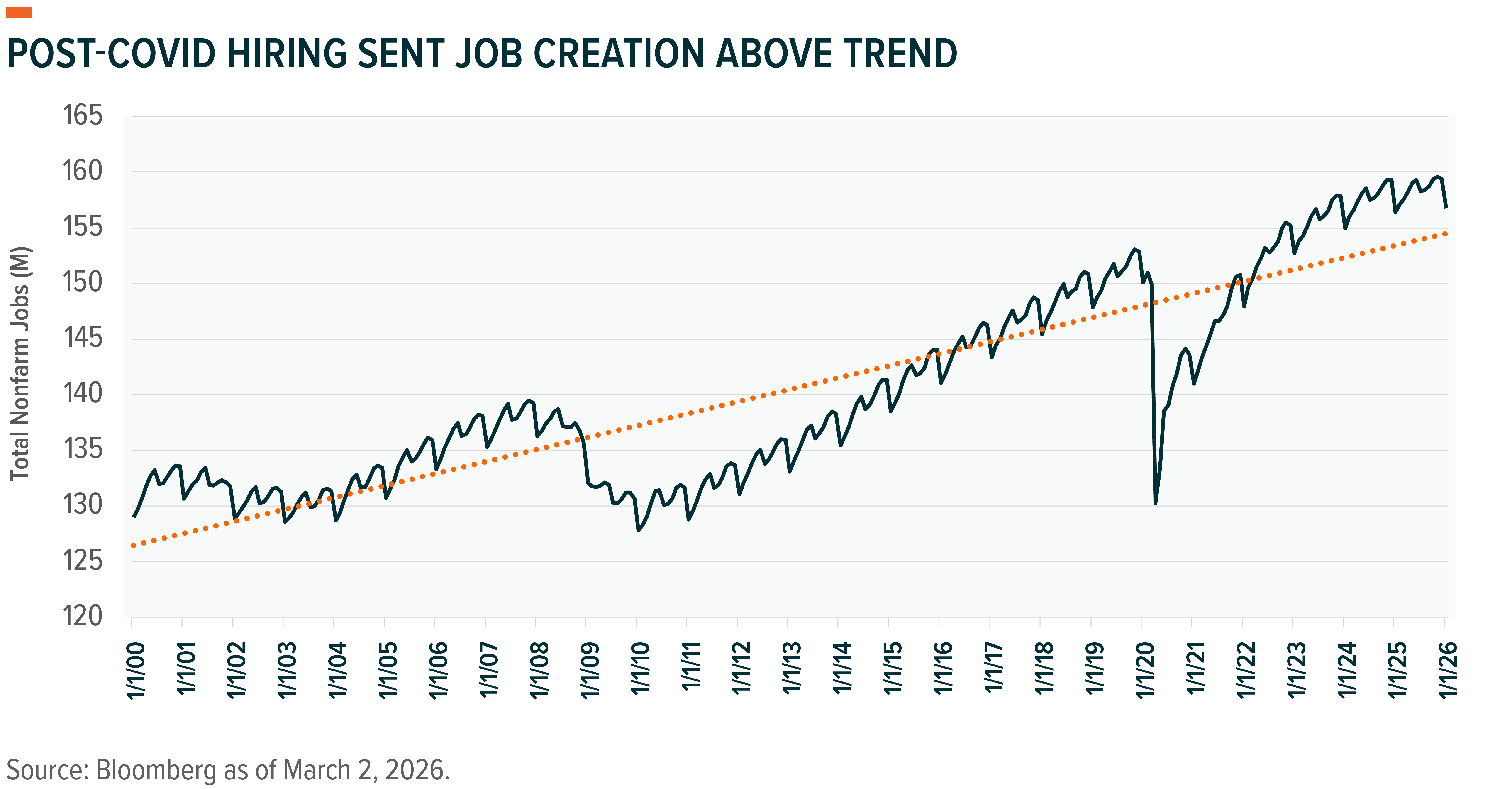

The labor market may be a swaying factor, potentially giving the Fed cover to lower rates. Job growth has been below trend for months, averaging 15,000 per month in 2025 compared to 90,000 going back to 2000.10 That trend might seem problematic, but it’s not that bad given COVID-era distortions. The economy shed jobs at the fastest rate ever during the pandemic shutdown, only to add them back at the fastest pace ever over the subsequent 18 months. The result was above-trend job creation.

The current job weakness is more likely about rightsizing back to trend rather than downsizing, though the February jobs report was much weaker than expected. While a large labor strike in healthcare and extreme winter weather distorted the data, almost every category shed jobs, including transportation, manufacturing, construction, information, and business services.11 With the CPI excluding shelter at the Fed target, the Fed has cover for a cut sooner than expected.

Another complication is the military operation in Iran, which introduces the risk of an oil supply shock. Since the conflict began, oil prices are up more than 30%.12 An increase of that magnitude risks transitory inflation and possibly keeps the Fed on hold, but there’s more to the story. Employment tends to take a hit when oil prices rise sharply, notably 20% or more in a month.13 Higher energy costs also present a headwind to growth with less disposable income for consumption and added uncertainty impeding corporate investment. The incremental risk to both labor and growth may well offset inflationary pressures, putting the Fed in position to act.

Cyclical Rotation Built on Secular Growth

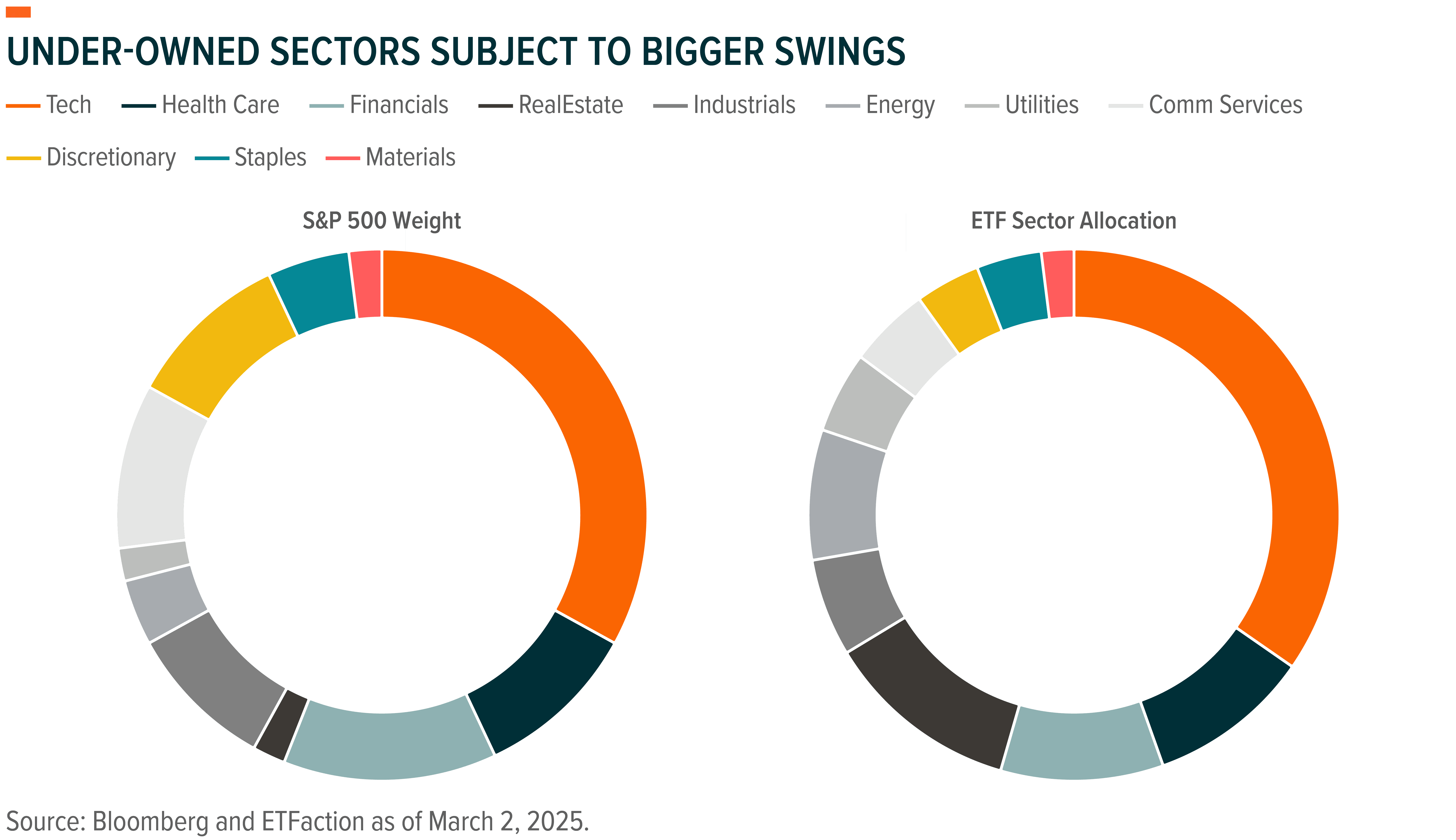

Perhaps the most significant trend in equities so far this year is the rotation driving wide dispersion between leaders and laggards despite relative calm at the index level. It does not take much to move the needle on under-owned sectors, especially those with lower index weight. Based on ETF sector ownership relative to the S&P 500 weighting, tech and healthcare remain over-owned relative to other sectors.14

The rotation is not a typical factor swap from growth or momentum to value or quality; rather, it’s a reduction in tech and communication services for traditionally cyclical sectors like industrials and materials.15 Ironically, these forces are inextricably intertwined, with success in traditionally stodgy cyclicals increasingly predicated on successful deployment of leading-edge technology.

The selloff in tech, software in particular, is tied to fears over AI disruption that may or may not be warranted. Putting that aside, the rotation into cyclicals is more challenging to explain. Investors are either looking past risks of stagflation and deceleration by opting for sectors that traditionally do well in early- and mid-cycle economies, or they are following the fundamentals. The latter seems the most plausible, even if only at a subconscious level.

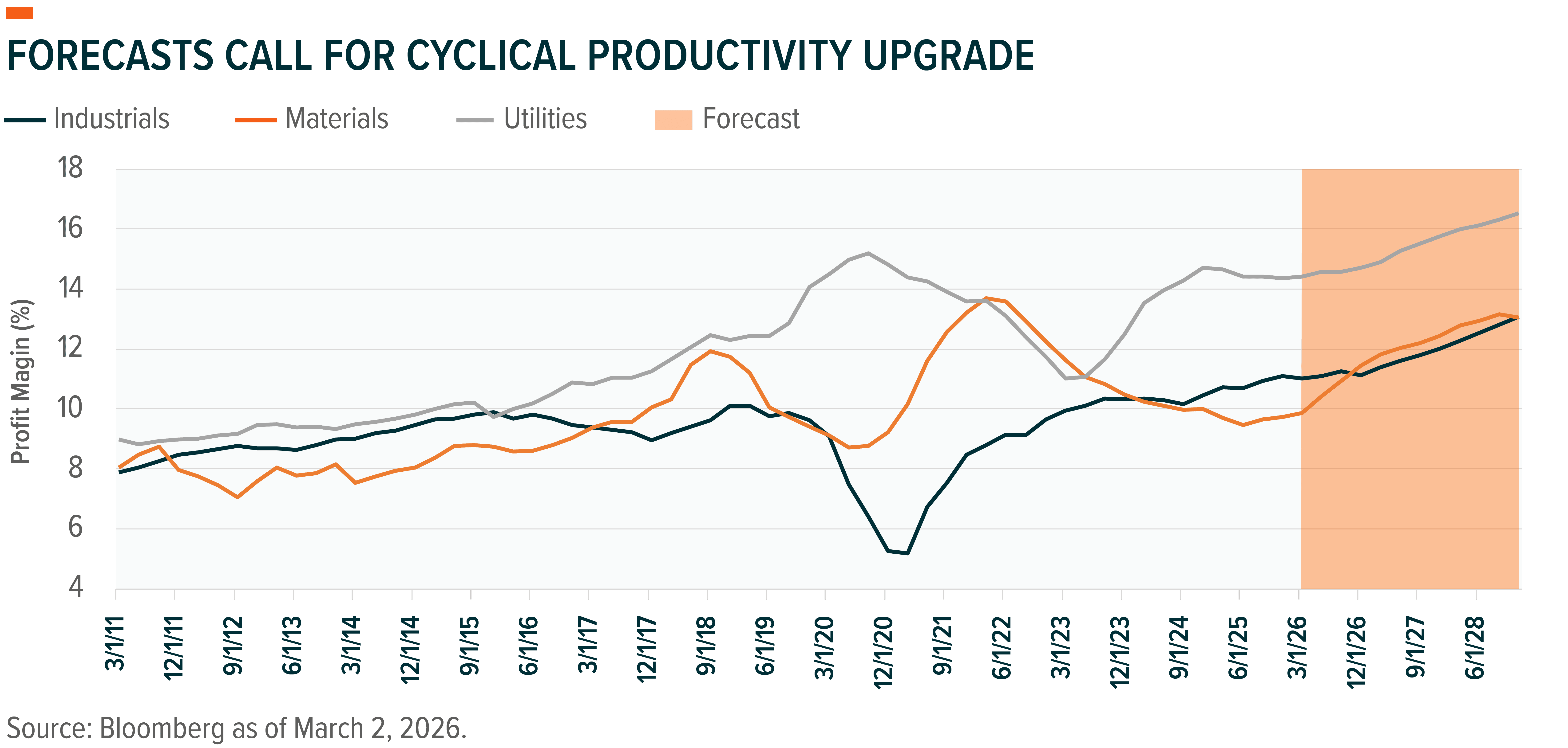

Revenue growth and profit margins for cyclical sectors like industrials and materials are forecast to improve meaningfully over the next three years. Even utilities are garnering attention. The expected growth rates for these sectors are now 2% to 3% higher for the next three years.16 Simultaneously, expectations for profit margin improvement are rising to new all-time highs.

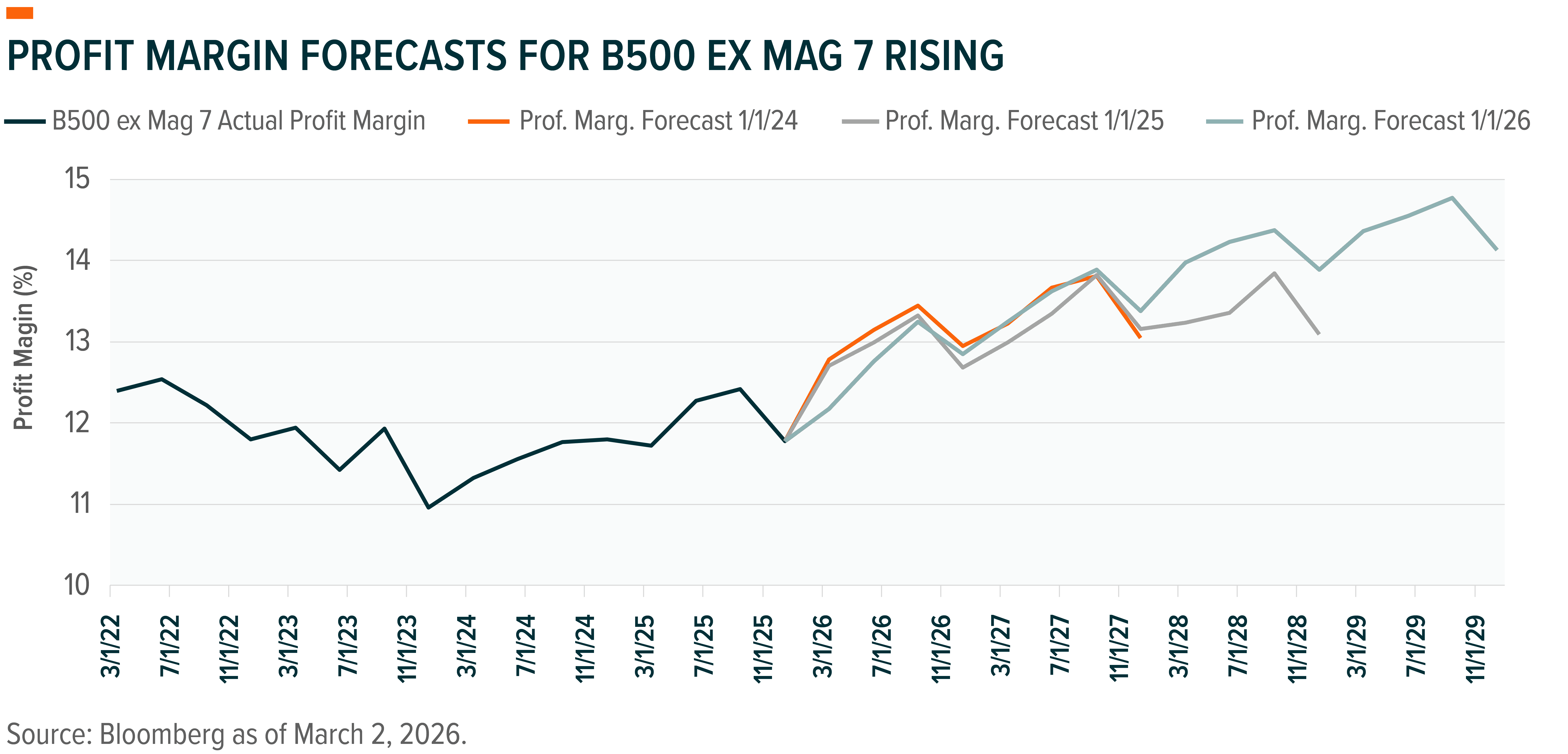

This is the economic broadening we have been talking about for the past two years. The critical caveat is that more companies will become more productive by adopting automation and AI. Selling off the very technology critical to productivity improvements in other industries ignores the co-dependency. Profit margin forecasts for the Bloomberg 500 excluding the Magnificent 7 jumped from 2025 to 2026 as more analysts started incorporating AI-driven efficiencies.17 For cyclicals to make good on those numbers, AI companies must deliver the goods.

AI Revolutions and Real Growth

Investment in the AI ecosystem remains a primary growth engine for the U.S. and the global economy. While the software sector may have fallen out of favor and faces revision to long-term growth expectations, massive capital expenditures continue to boost interconnected sectors like infrastructure, materials, and utilities. There is, however, concern that all the spending is a house of cards, akin to the circular nature of home financing that preceded the Global Financial Crisis in 2008.18 In our view, that comparison is apples to oranges.

The current anxiety stems from venture investment and vendor financing, both of which are legitimate, long-held, and widely used corporate strategies. While these strategies can introduce risk when used in the wrong context, the AI buildout does not appear to be one of them.

Venture investment risks arise when a company provides funds that cannot be met by growing cashflow.19 The main example now is Microsoft investing in OpenAI, which then purchases cloud services for the same amount in Microsoft’s Azure. In essence, Microsoft is providing services in exchange for equity. If OpenAI fails to generate revenue and profit that exceeds the investment, the investment becomes a loss. But if the pace of growth exceeds the investment within a reasonable time horizon, there should be a positive internal rate of return.

Vendor financing risks arise when a company offers a line of credit for its products.20 The company supplies the goods on credit to be paid in the future. At the consumer level, this practice is akin to a car loan or a short-term financing option like buy now, pay later (BNPL). It is also common practice in wholesaling, from consumer staples to heavy equipment, likely comprising more than 50% of B2B sales.21

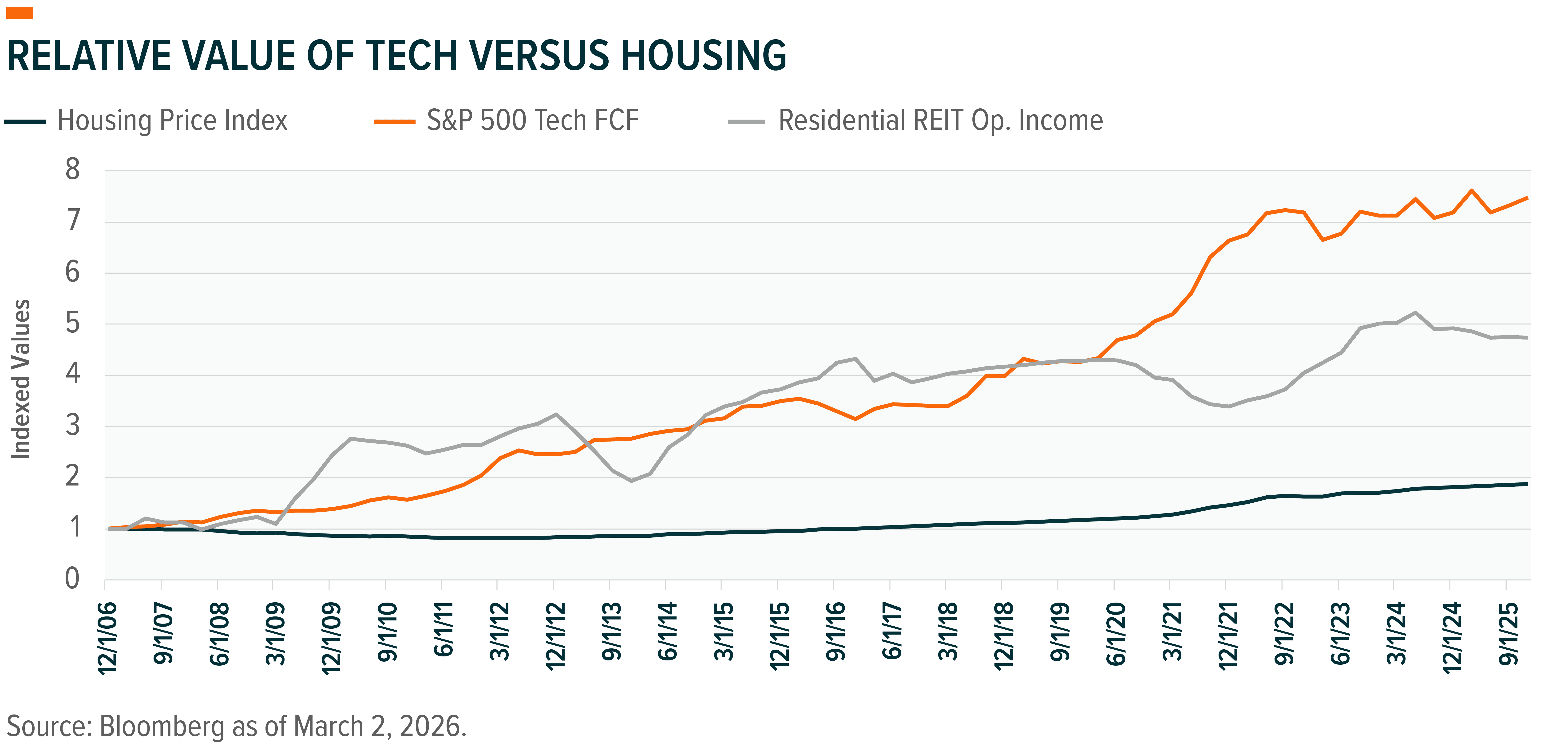

Financing only becomes a problem when the underlying asset fails to gain value or grow cash flow fast enough to justify the credit. That proved true in 2008 with housing, an asset that typically appreciates at a fairly slow rate. In contrast, investments in tech historically generate much more rapid cash flow growth.22 Providing equity or a line of credit to a company seeing brisk demand growth—which is the case with large language models and the data infrastructure needed to power them—is not necessarily a circular trap.

Straight Lining the Logic

We believe there is room to run in the economic broadening narrative that has supported cyclical themes like infrastructure, miners, and electrification. Their success remains contingent on the successful adoption and deployment of automation and AI technologies. For investors who may have missed earlier entry points into the AI and digital infrastructure trade, the recent selloff presents an opportunity to build exposure to AI software, cybersecurity, data centers, and alternative power sources such as uranium. The ongoing conflict in Iran also creates potential opportunities in defense technology, U.S. natural gas, and U.S. energy infrastructure.

Pairing the cyclical trade with continued exposure to AI growth seems like a reasonable way to navigate the market’s current distortions and straighten out the circular logic.