On June 24th, 2026, we listed the Global X Adaptive Risk Managed Yield ETF (RMHY) on the NYSE Arca. RMHY is the newest addition to Global X’s fixed-income lineup that is designed to provide exposure to high yield corporate bonds while incorporating a rules-based risk management overlay. Under normal market conditions, the fund is invested in high yield bonds. When market signals indicate elevated risk, the strategy reallocates to short-duration U.S. Treasuries, seeking to reduce downside risk during periods of market stress.

Key Takeaways

- The Global X Adaptive Risk Managed Yield ETF (RMHY) seeks to track the Adaptive Wealth Strategies Risk Managed Yield Index, which allocates between U.S. high yield corporate bonds and short-duration U.S. Treasury bills based on market conditions.

- The Adaptive Wealth Strategies Risk Managed Yield Index uses Moving Average Convergence Divergence (MACD) and the Cboe Volatility Index (VIX) as technical indicators to determine whether the index should be positioned in high yield bonds or Treasuries.

- High yield bonds should be the strategy's primary source of income and return potential. The Treasury allocation is intended to help manage downside risk during periods of elevated market stress.

RMHY Aims to Combine High Yield Bond Exposure with a Rules-Based Risk Management Overlay

Most investors access high yield bonds through broad strategies that remain fully invested regardless of market conditions, leaving them exposed to the full impact of periods when credit spreads widen and risk assets come under pressure. Alternatively, investors must try to actively manage their high yield bond exposure and buy or sell their positions as conditions change.

The Global X Adaptive Risk Managed Yield ETF (RMHY) is a passive index strategy that seeks to provide a more risk-aware approach to high yield investing. It endeavors to do so by seeking to track the Adaptive Wealth Strategies Risk Managed Yield Index, which employs a rules-based mechanism to reallocate entirely from the Solactive USD High Yield Corporates Total Market Index to the Solactive 1-3 month US T-Bill Index when equity market volatility is high and the high yield bond market is displaying signs of weakness.

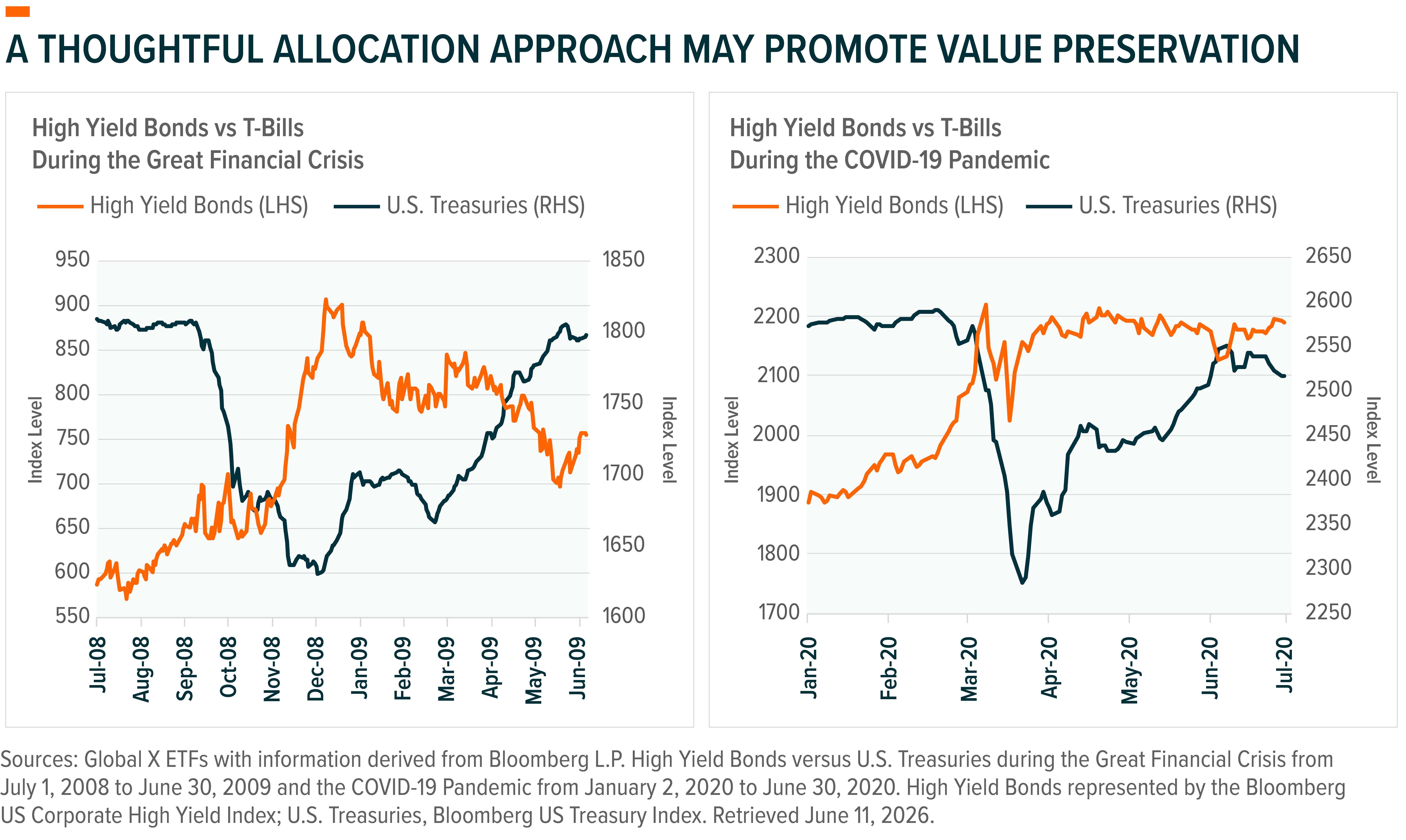

Looking at some of the most significant periods of stress in the credit markets over the last two decades, the potential value of incorporating a risk management overlay such as this becomes apparent. While high yield bonds have historically generated attractive income and total return potential over time, periods of severe market disruption have also been responsible for a disproportionate share of the asset class's downside participation. Given this understanding, RMHY seeks to remain invested in high yield bonds when conditions are supportive, but incorporates a rules-based process that is designed to respond when certain risks become elevated.

Index returns are for illustrative purposes only and do not represent actual Fund performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

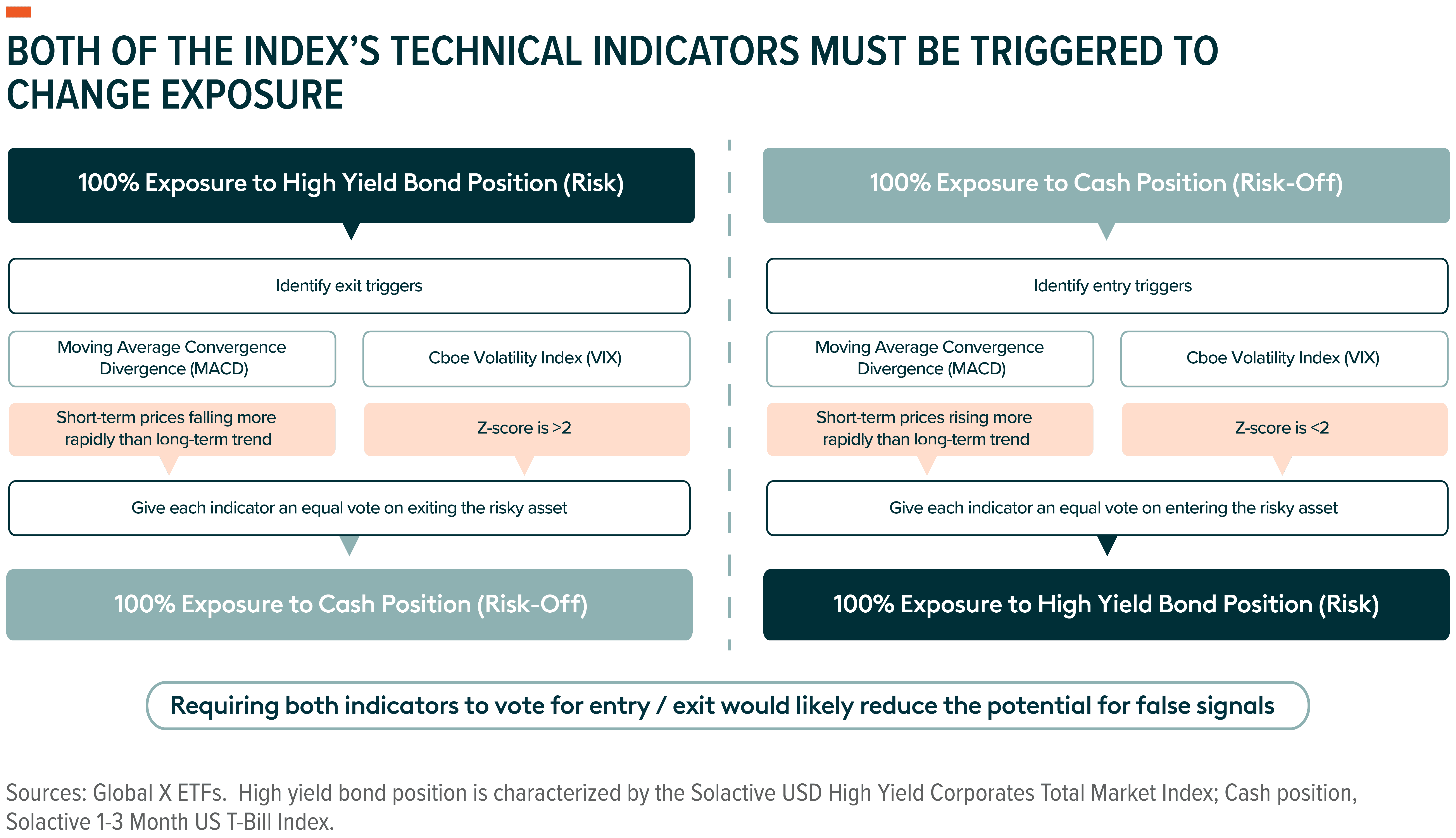

RMHY’s Index Utilizes a Two-Pronged Signaling Mechanism to Assess Market Conditions

Moving Average Convergence Divergence (MACD) and the Cboe Volatility Index (VIX) are two of the most commonly utilized technical indicators on the market. Investors use them to help guide trade timing and provide logic behind the decision to invest or divest in specific positions.

The MACD is a momentum indicator that evaluates the direction and strength of recent price trends and is commonly used by investors to identify potential buy and sell signals. It measures the difference between an instrument’s 12-day and 26-day exponential moving averages; changes in that relationship may indicate shifts in market momentum. The VIX is often referred to as the market’s “fear gauge” because it measures investor expectations for near-term market volatility. It does so by calculating the market’s 30-day forward implied volatility using prices of S&P 500® index options.

Importantly, the Adaptive Wealth Strategies Risk Managed Yield Index does not respond to either signal in isolation. The strategy reallocates from high yield bonds to short-duration Treasury bills only when both indicators simultaneously point to elevated market risk. Further, the strategy will only reallocate to high yield bonds from short-duration Treasury bills when the same indicators point to less market risk. This dual-signal approach is intended to reduce the likelihood of reacting to temporary market noise while reserving defensive positioning for periods when market conditions are deteriorating more meaningfully.

For the MACD signal to trigger high yield market exit, the Solactive USD High Yield Corporates Total Market Index must exhibit weakening momentum, with its 12-day exponential moving average declining relative to its 26-day exponential moving average to a degree that results in a z-score that is below -1.00. The VIX signal, meanwhile, is triggered when implied equity market volatility rises meaningfully above its historical norm, with a z-score greater than 2.00. A z-score measures how many standard deviations a value is above or below its historical average. In the case of the VIX, a reading more than two standard deviations above its historical mean suggests a period of elevated market uncertainty and heightened risk aversion. By requiring triggers from both indicators, the strategy seeks to distinguish between temporary market noise and more meaningful deterioration in market conditions.

Taken together, these indicators account for both backward-looking and forward-looking market conditions, evaluating recent momentum for high yield bonds in conjunction with near-term expectations for equity market volatility. In combination, they have the potential to detect material market correction events and the index adjusts accordingly.

A Risk Managed Approach May Help Investors Maintain High Yield Bond Exposure

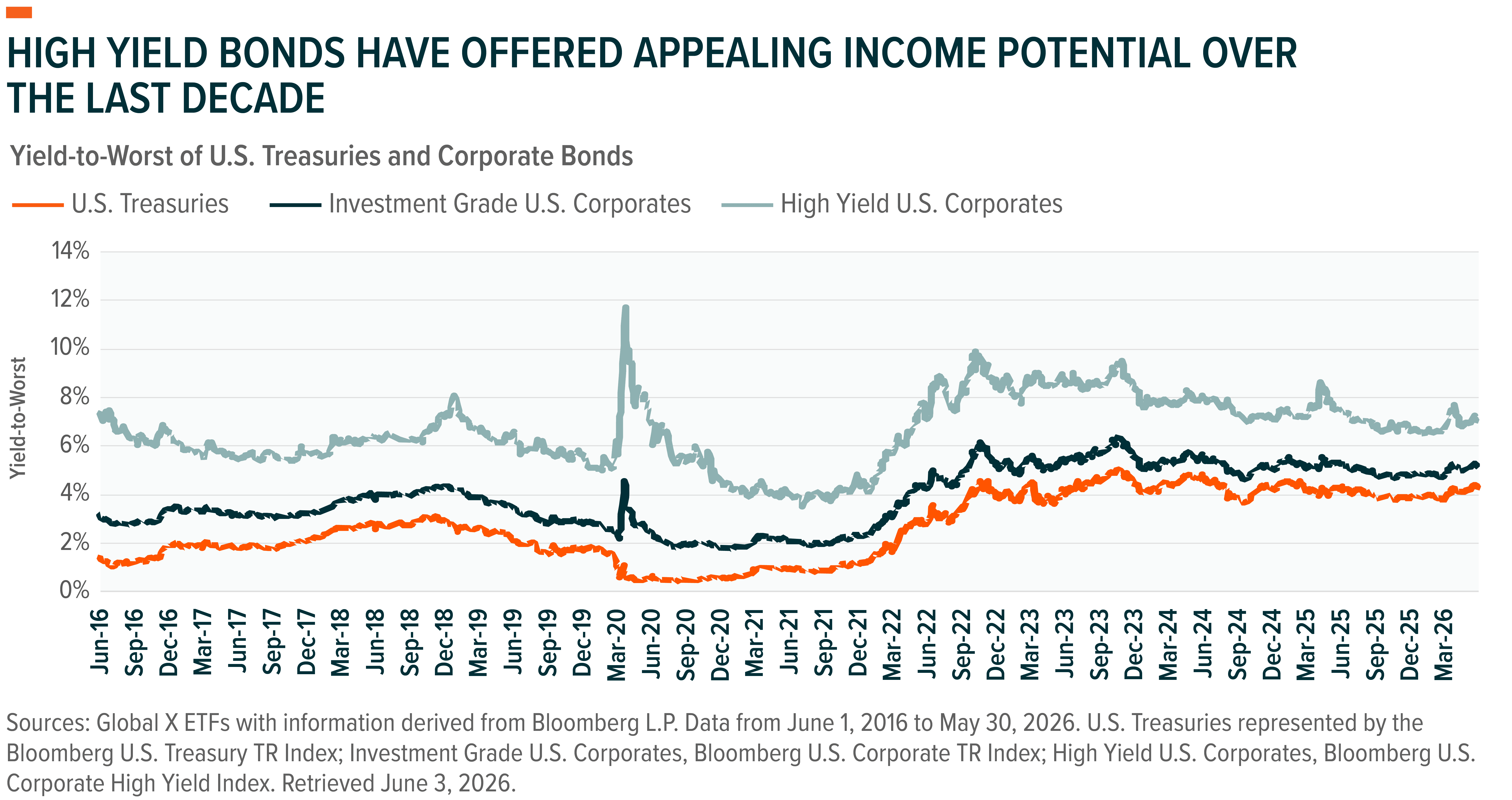

High yield bonds have historically occupied a unique position within fixed income portfolios, combining attractive income potential with potential diversification benefits and opportunities for capital appreciation. They also generally offer meaningfully higher coupons relative to investment-grade corporate bonds and U.S Treasury instruments, which is the case because they reside further out across the credit spectrum. One way to evaluate that opportunity is through yield to worst, a commonly used measure of the yield available from a bond under a conservative set of assumptions. As shown below, high yield bonds have historically offered meaningfully higher yield-to-worst levels than investment-grade corporate bonds and U.S. Treasuries, helping support their appeal among income-oriented investors.

Past performance is not a guarantee of future results.

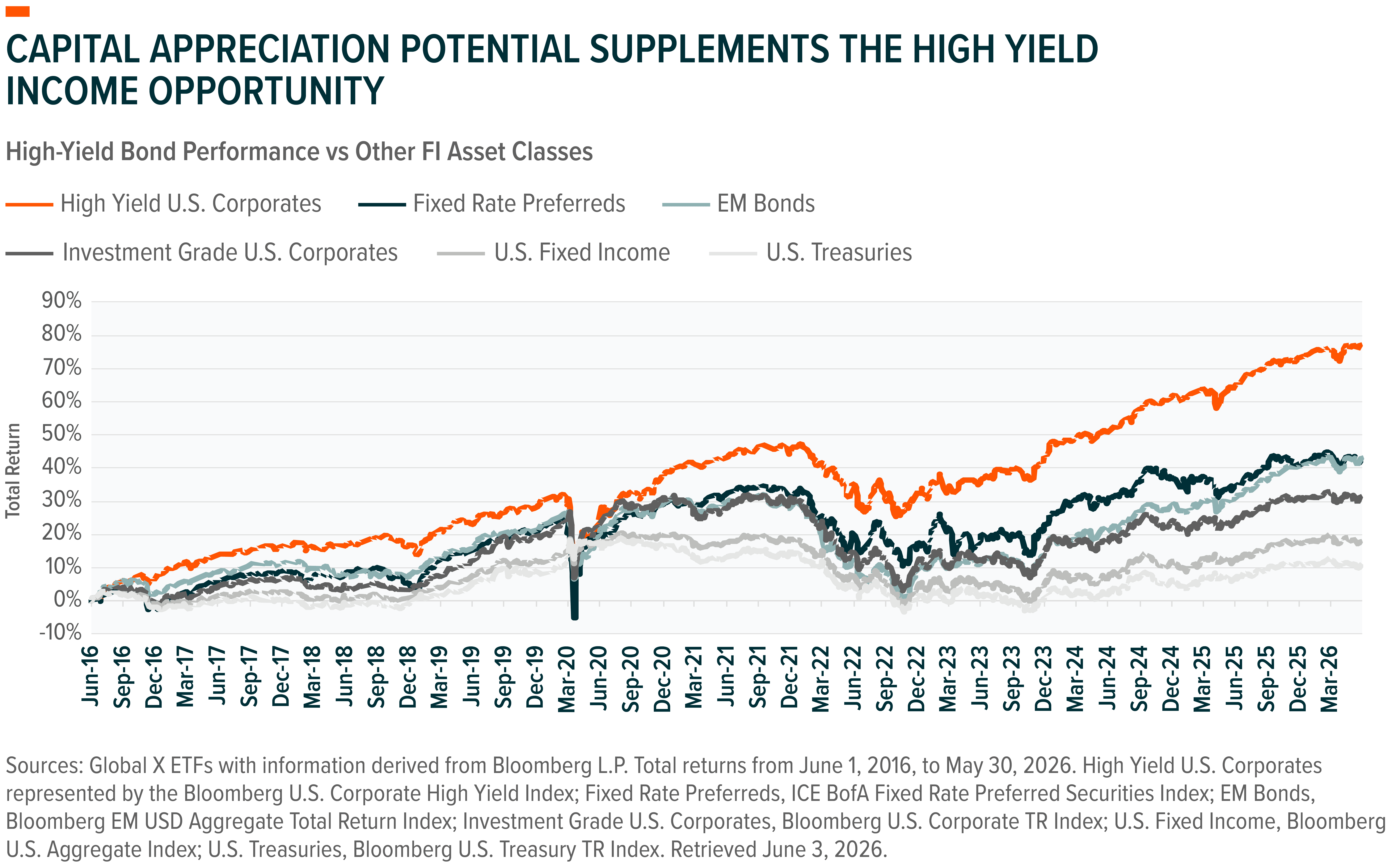

Capital appreciation potential should not be ignored, however. The chart below shows that, relative to other fixed-income instruments, high yield bonds have notably outperformed over the last decade, as market conditions have improved and credit spreads have tightened.

Index returns are for illustrative purposes only and do not represent actual Fund performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Looking forward, as spreads remain historically tight, having a contingency in place to potentially address a risk-off environment might be deemed appealing. One of the obstacles that has likely prevented investors from confidently committing to high yield issuances in the past is the potential nature of their tail-risk events, when credit comes under fire owing to broad economic contractions, liquidity shocks, or other market disruptions. By actively addressing these concerns through the passive utilization of a rules-based mechanism that will reallocate to more of a risk-off portfolio, investors may not only recognize a potentially less volatile high yield experience, they may also be able to drastically improve long term total returns by failing to realize the losses that come about with those events.

Conclusion: RMHY Seeks to Instill Confidence for Sustainable High Yield Bond Commitments

Virtually every asset class comes with a measure of tail risk. For high yield bonds, those periods can be particularly challenging, as market stress, widening credit spreads, and deteriorating economic conditions potentially result in significant drawdowns that weigh on long-term outcomes.

Yet despite these risks, high yield bonds have remained a compelling allocation for many investors because of the yield, return potential, and diversification they can provide within a broader portfolio. The challenge is often not whether investors recognize the value of the asset class, but whether they can maintain exposure through periods of heightened uncertainty.

The Global X Adaptive Risk Managed Yield ETF (RMHY) is designed to address this challenge, giving investors the ability to remain invested in high yield bonds while employing a simple allocation mechanism to attempt to curtail loss potential when market risk is elevated. By seeking to reduce the severity of the episodes that have historically done the most damage to long-term compounded returns, RMHY aims to make high yield bond exposure not just a compelling short-term income trade, but a more sustainable fixture of a thoughtfully constructed portfolio.

RMHY – Global X Adaptive Risk Managed Yield ETF (RMHY)

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.