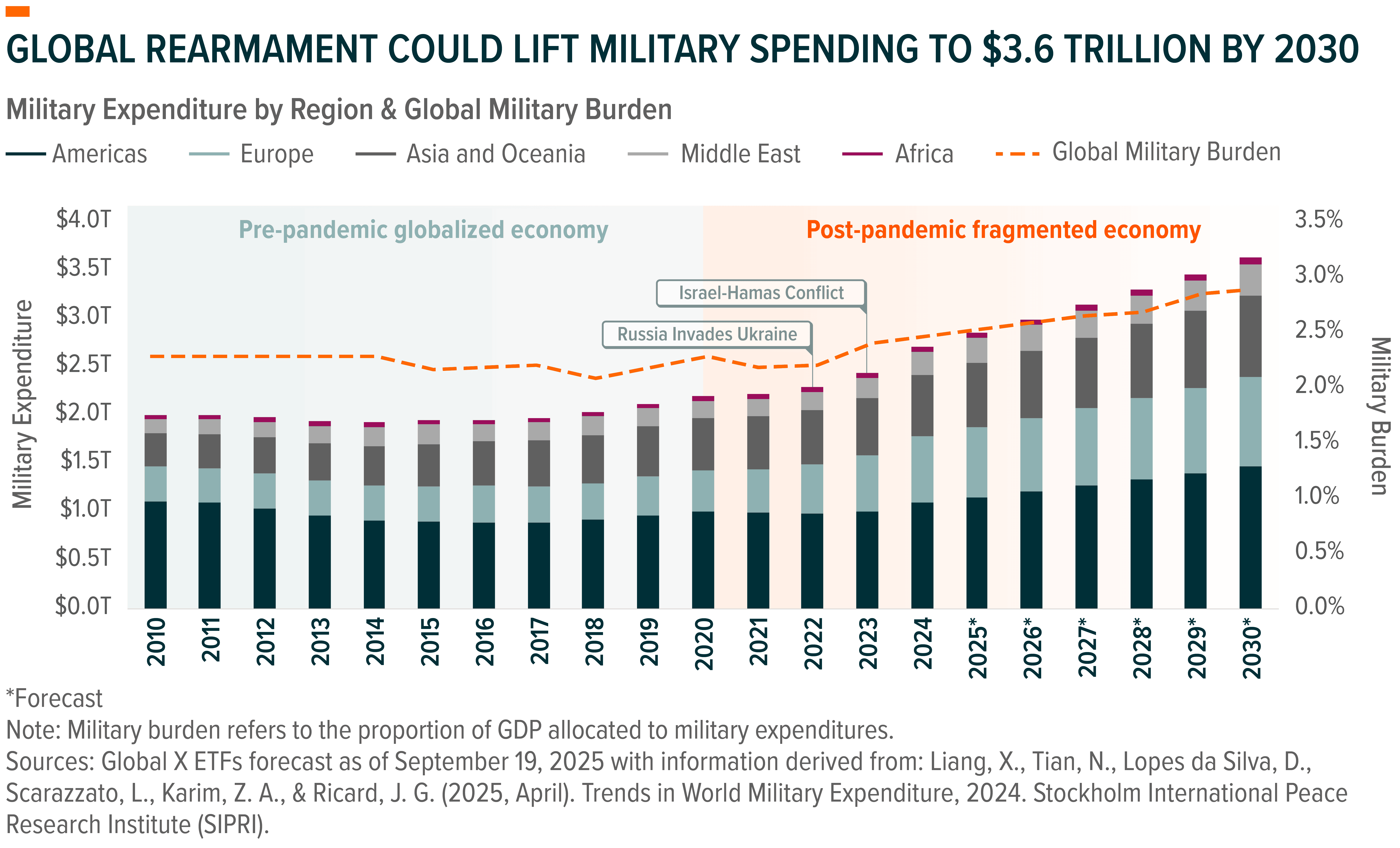

We believe volatility towards the end of 2025 has masked the underlying strength of the Defense Tech theme. Beneath the pullback, fundamentals have continued to improve, supported by expanding military budgets around the world, rising order books across major contractors, and modernization agendas as nations prepare for a more fragmented and technologically contested security environment. Global defense spending could surpass $3.6 trillion by 2030, nearly 33% above 2024 levels.1 Even as conflict headlines temporarily ease, structural geopolitical priorities across the United States, Europe, and Asia remain firmly in place, adding durability to the spending cycle.

At the same time, the center of gravity in defense is shifting from hardware to software. AI-enabled systems, drones, and digital command networks are moving from experimentation into deployment, reshaping industry economics and widening margin profiles. With fundamentals firm and modernization still in early stages, we believe Defense Tech enters 2026 with a constructive setup.

Key Takeaways

- Defense Tech fundamentals remain strong, with expanding order books pointing to sustained momentum into 2026.

- Modernization is accelerating, with AI, autonomy, and software-defined systems moving into deployment and expanding earnings power for Defense Tech leaders.

- A structural shift toward software-driven, higher-margin business models could reshape defense fundamentals, moving the sector closer to a tech-like profile.

Geopolitics and Macro Drove the Reset, Not Fundamentals

The Defense Tech theme retraced roughly 15% from its October highs.2 In our view, this was driven by two factors: markets reacting to a potential Ukraine peace agreement and renewed uncertainty with interest rates heading into 2026. Neither development should alter the structural drivers shaping global defense spending or the multi-year modernization cycle already underway.

While market behavior still tends to frame Defense Tech through the lens of headline intensity, we believe that can undermine the central reality that global defense spending is broad-based, durable, and increasingly tied to long-cycle modernization rather than episodic conflicts. These priorities will likely continue regardless of near-term geopolitical de-escalation and are central to long term peace.

Dynamic Geopolitical Backdrop Has Extended the Defense Spending Cycle

Geopolitics has been a key factor in influencing defense budgets and market perception. In late 2025, the backdrop may be far less conflict-led than it was a few years back. But it may be shortsighted to interpret this easing in conflict-related headlines as a structural turning point for the Defense Tech theme. In our view, the ongoing broad-based rearmament cycle could drive ~5% growth in defense spending in 2026, boosted by emerging geopolitical realities and power dynamics. Total spend could surpass $3.6 trillion by 2030.3

Specifically in Europe, even if the Ukraine peace deal advances, the region’s strategic trajectory when it comes to defense remains unchanged. Years of underinvestment have created capability gaps across air and missile defense, artillery, ammunition, drones, and technologies of strategic importance such as AI and Quantum — areas explicitly recognized and codified in the EU’s Readiness 2030 plan.4

Europe is also reinforcing this direction with capital. As the United States gradually steps back from underwriting Europe’s security, regional governments are preparing to allocate nearly €800 billion toward defense by 2030.5 EU-wide defense spending is already set to reach 2.1% of GDP in 2025, up from 1.6% in 2023.6 NATO’s guidance, adopted in June 2025, to target 5% of GDP by 2035 further reinforces and advances that commitment.7 This momentum is reflected in contractors like Rheinmetall forecasting a fivefold increase in revenue by 2030.8

Asia presents a similar picture of long-cycle escalation. Rising tensions around China and Taiwan have re-entered focus following recent diplomatic exchanges between Japanese leadership, Beijing, and Washington.9 Major powers are expected to continue to seek deterrence and technological parity across domains, suggesting that regional budgets are likely to remain elevated well into the next decade.

From India to South Korea to Central America, regional power dynamics continue to add more tailwinds to the overall defense spending story. In our view, these realities extend the durability of the global defense spending cycle, and even if headline conflicts moderate, incremental funding is still required to fill capability gaps, rebuild industrial capacity, and adapt to a more fragmented geopolitical order.

Technology Is Expanding Defense Tech’s Earnings Power

The earnings profile of Defense Tech continues to diverge from legacy contractors. For Q3 of 2025, Defense Tech companies delivered 29% year-over-year (YoY) earnings per share (EPS) growth, nearly twice the earnings growth of the S&P 500.10 Higher volumes, improved pricing, and accelerating demand for AI, autonomy, and digital command systems are some of the secular drivers of this growth.

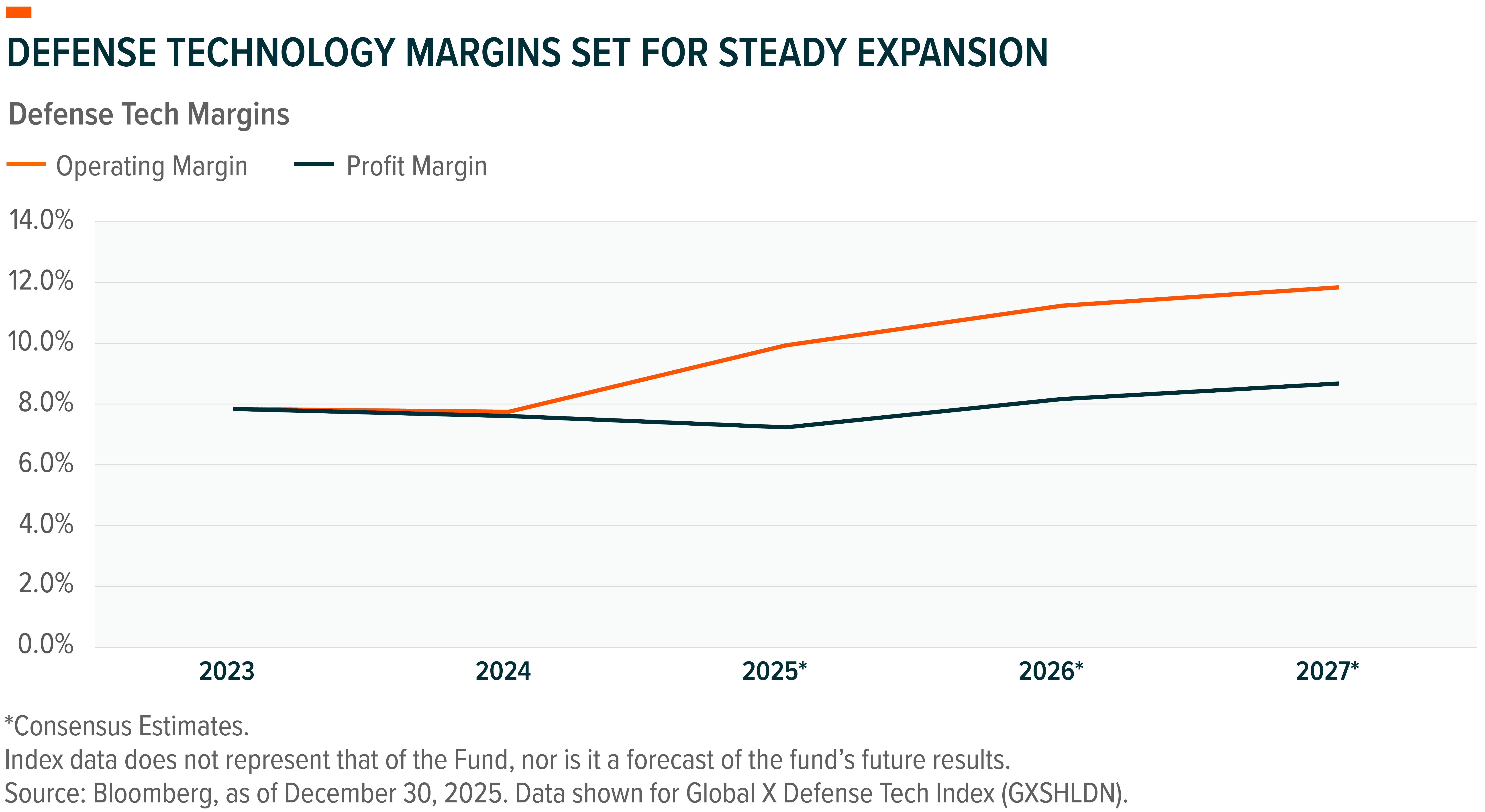

Margin expansion expectations reinforce this shift. Defense Tech operating margins are forecast to expand over 230 basis points (bps) in 2025, with another 120-bps gain expected in 2026.11 The expected gains reflect software-driven business models that differ fundamentally from traditional defense, as digital platforms generally carry structurally higher margins, long-lived contracts, and stronger pricing leverage.

Palantir’s fundamentals put this growth into perspective. The company’s revenues grew 63% YoY for the quarter of Q3 2025, with operating margins remaining over 40%, highlighting the scale benefits of software.12 In our view, software still represents a small fraction of total global defense spend, suggesting considerable untapped growth ahead.

Earnings visibility has also improved. Backlogs across major global defense contractors sit at multi-year highs, in some cases representing more than two years of forward revenue.13 This dynamic improves cash-flow visibility and predictability relative to other cyclical industries and sets a firm floor under the growth outlook.

Defense Valuations Reflect a Techno-Industrial Future

AI, software, drones, and autonomous systems are reshaping the defense landscape. As these technologies scale, the sector’s fundamentals are beginning to resemble those of technology businesses rather than traditional industrials. This evolution also has likely direct implications for how the market values defense companies.

For decades, legacy defense contractors commanded disciplined, cash-flow–anchored valuations, shaped by predictable but limited growth.14 The emergence of dual-use, software-heavy platforms is breaking that pattern. Expanding budgets for tech are spurring growth, while recurring contracts, higher-margin digital systems, and faster product cycles are pushing the sector toward tech-style valuations.

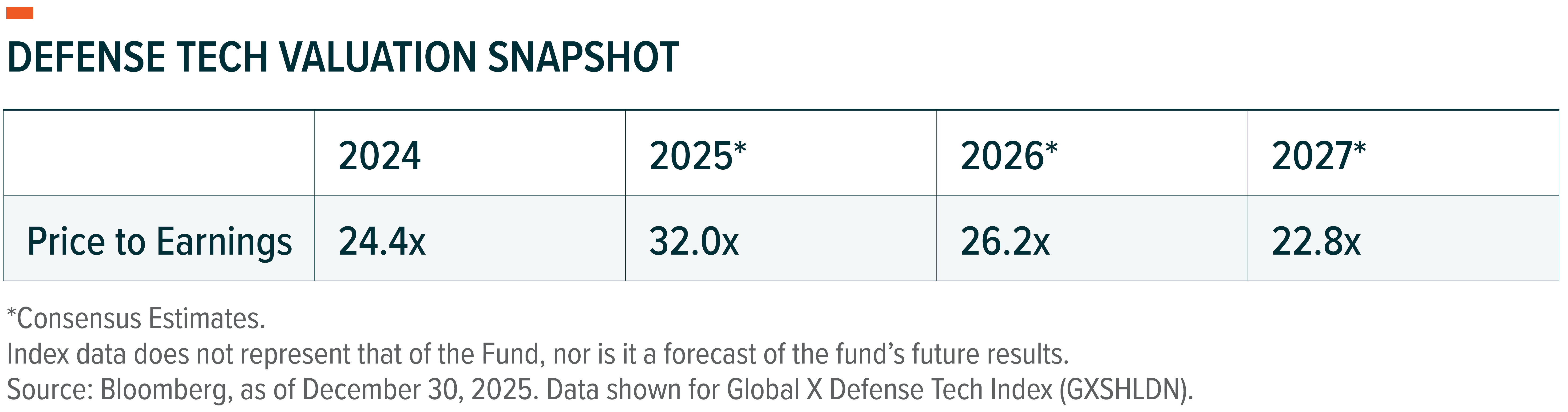

Despite the run-up YTD, as of December 30, 2025, the defense tech sector is valued at just over 26x 2026 earnings and 22x 2027 earnings. We expect EPS growth to remain strong, boosted by a continued mix shift toward high-margin software and digital systems.

Conclusion: Defense Tech Set Up Appears Constructive for Next Few Years

Global defense transformation is not driven by any single conflict, but by a broad rearmament cycle aimed at meeting future threats and the need for modern, tech-focused solutions. Major militaries are directing capital toward closing capability gaps, strengthening deterrence, and building resilient techno-industrial capacity for a more multipolar world. We believe these priorities create a strong foundation for the Defense Tech theme. With fundamentals firm and valuations more attractive, we believe the theme is well positioned as militaries enter a long modernization cycle.

Related ETFs

SHLD – Global X Defense Tech ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.