Interest in Southeast Asia continues to increase amid shifting global supply chains, elevated geopolitical risks in China, and disinflationary trends. Within this context, Vietnam stands out as a leader in reform and industrial dynamism, while ASEAN (Association of Southeast Asian Nations) offers breadth, scale, and macro resilience.

Vietnam: Structural Reforms with Trade Tailwinds

- Trade Deals: Vietnam’s recent agreement with the U.S., imposing a 20% tariff on domestic exports (down from a proposed 46%) and removing tariffs on U.S. imports, offers clarity for investors. The deal includes a 40% levy on “transshipped” goods, underscoring U.S. efforts to curb Chinese circumvention via Vietnam.1 While details are pending, we think this marks a net-positive for long-term positioning and sets a potential template for other ASEAN trade negotiations.

- Friendshoring: Vietnam continues to benefit from friendshoring trends, with foreign direct investment (FDI) rising 8.1% year over year in the first half of 2025.2 Manufacturing hubs have expanded across electronics, semiconductors, and garments, supported by bilateral trade clarity. U.S. firms are increasing supply chain exposure to Vietnam to mitigate concentration risk in China.

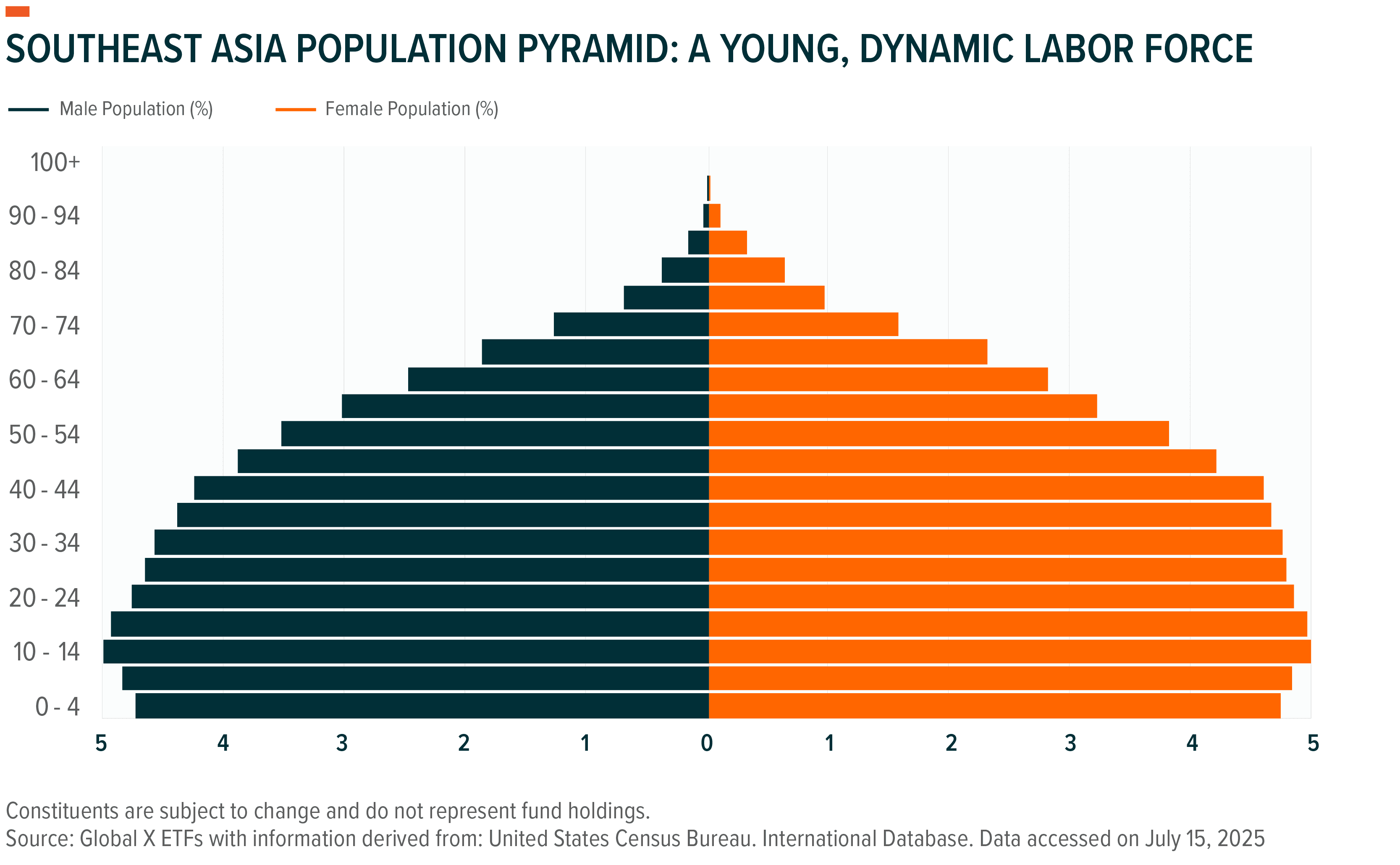

- Demographics: With a median age of 32 and over 70% of the population in working age, Vietnam offers a dynamic labor force.3,4 Urbanization is accelerating, with a 3% compound annual growth rate (CAGR) in urban population growth fueling housing, infrastructure, and consumer demand while also historically leading to productivity gains.5

- Structural Growth: The Vietnamese government is executing its most sweeping reforms since Doi Moi. Resolution 68 shifts the economic model toward private sector-led growth, streamlines bureaucracy through ministerial consolidation, and introduces R&D tax incentives (200% deduction).6 These changes are aimed at reducing the size of government, improving the ease of doing business, and supporting capital formation in industrials, banks, and consumer sectors.

- Catalysts: Vietnam remains on the FTSE Russell watchlist for potential reclassification to secondary Emerging Market (EM) status. An upgrade could attract roughly $6 billion in index-driven flows.7

ASEAN: Long-Term Diversified Growth

- Trade Deals: ASEAN countries have either reached a trade deal with the U.S. or have been subject to the baseline tariff rate, adding the policy certainty required for corporates to restart investment.

- Friendshoring: ASEAN has become a magnet for supply chain relocation. Indonesia and Malaysia are expanding semiconductor capacity, while Singapore and Thailand are consolidating regional tech and logistics roles. FDI into the region surpassed $235 billion in 2024, an all-time high.8

- Growth: ASEAN’s GDP is projected to grow 4.7% in 2025, driven by domestic consumption and infrastructure expansion.9 Indonesia’s interest rate cuts and Thailand’s $29 billion transport upgrade are examples of counter-cyclical fiscal support.

- Valuations: After the region saw significant outflows post-U.S. election, ASEAN ex-Singapore/Indonesia is trading near historical troughs relative to broader EM.10 Multiples remain compressed, offering potential asymmetric upside if positioning normalizes.

- Diversification: ASEAN economies are at varying stages of development and policy cycles. This heterogeneity offers natural diversification across growth drivers—energy in Malaysia, tourism in the Philippines, and logistics in Thailand.

- Catalysts: Macroeconomic stabilization, progress in bilateral trade talks, and improving fund flows could lift investor sentiment. Structural reforms in individual markets—such as digitalization in Indonesia or tax policy shifts in Thailand—enhance long-term visibility.

Category:International Access

Topics: