We recently returned from a due diligence trip to Delhi, Gurgaon, and Mumbai where we met with over 25 management teams and local consultants. We left more encouraged by the outlook ahead for Indian equities. Potential forthcoming progress on trade agreements, combined with below average investor positioning, could lay the groundwork for a significant catch-up opportunity.

Key Takeaways

- Structural Growth Story Appears Intact: We believe that India remains an attractive long-term standalone investment opportunity based on diversification benefits, structural growth advantages, and historically superior risk-adjusted return profiles.1

- Ready for the Turn: Corporates across most sectors appear to be in good shape with de-levered balance sheets, improving cash flows, and attractive return ratios. Regulations are also supporting growth and Ease of Doing Business metrics.

- Shifting Government Priorities: With a benign macro backdrop, the Indian Government is ready to support consumers and micro, small, and medium enterprises (MSMEs) to offset a growth drag from trade uncertainty.

A Structural Story Finally Cleared for Takeoff as Headwinds Turn to Tailwinds

In a recent blog post, we wrote about why we believe India merits consideration as a long-term standalone investment. Our argument was based on a combination of diversification benefits, structural growth advantages, and historically superior risk-adjusted returns. We believe the long-term thesis remains robust, but we see near-term opportunities, as well.

Sometimes extreme external pressures, like those India faces today, can create unique opportunities for a country to make large scale changes. In India’s case, the severe balance of payments crisis in 1991 led to a first round of liberalization. In 1998, India’s underground nuclear tests triggered sanctions, but the measures were eased later that year. This marked the beginning of a shift from sanctions-based responses to one of engagement and dialogue with a now strategically significant country. The current trade war creates another trigger for action, focused on further de-regulation and pro-growth government policies.

Taking a step back, a (1) benign macro backdrop (low inflation, rate cuts, significant foreign exchange (FX) coverage, consecutive positive monsoon seasons!), (2) significant improvements in the Ease of Doing Business (Goods and Services Tax cuts, Reserve Bank of India (RBI) easing measures, upcoming wage increases, deregulation, and digitization trends), (3) confirmation of a significant government capex pipeline, and (4) light investor positioning, set up an interesting entry opportunity. In turn, we believe India could be on the cusp of a significant catch-up opportunity to both global and Emerging Market performance.

- Light Foreign Portfolio Investment (FPI) Positioning: Over the past year, India’s weight in EM Funds compared to the benchmark weight has declined from an average overweight of ~2.5% to a neutral position, setting up a potential catch-up opportunity.

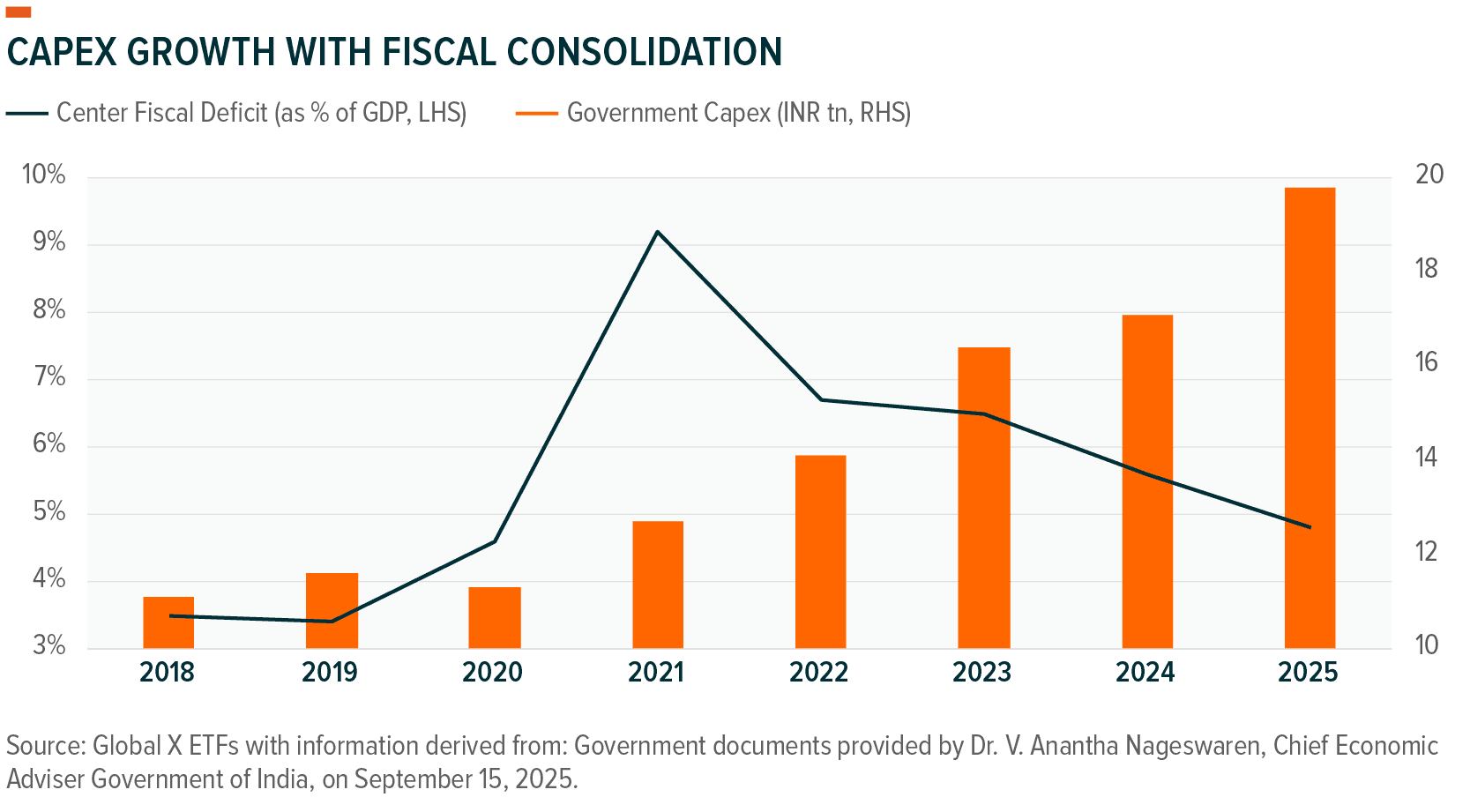

- Government Emphasis on Capex Remains: Public sector capex has increased roughly 2x between FY18-26.2 Dr. V. Anantha Nageswaran, the Chief Economic Adviser to the Government of India, told us that, “Continued emphasis on government capital expenditure to boost infrastructure” was listed as the top policy priority for the government. Importantly, India achieved fiscal consolidation (i.e., reduction in fiscal deficits) of more than 5% over the past five years, declining from a peak of -9.2% to reach a fiscal deficit of ~4% of GDP, despite the significant growth in government capex.

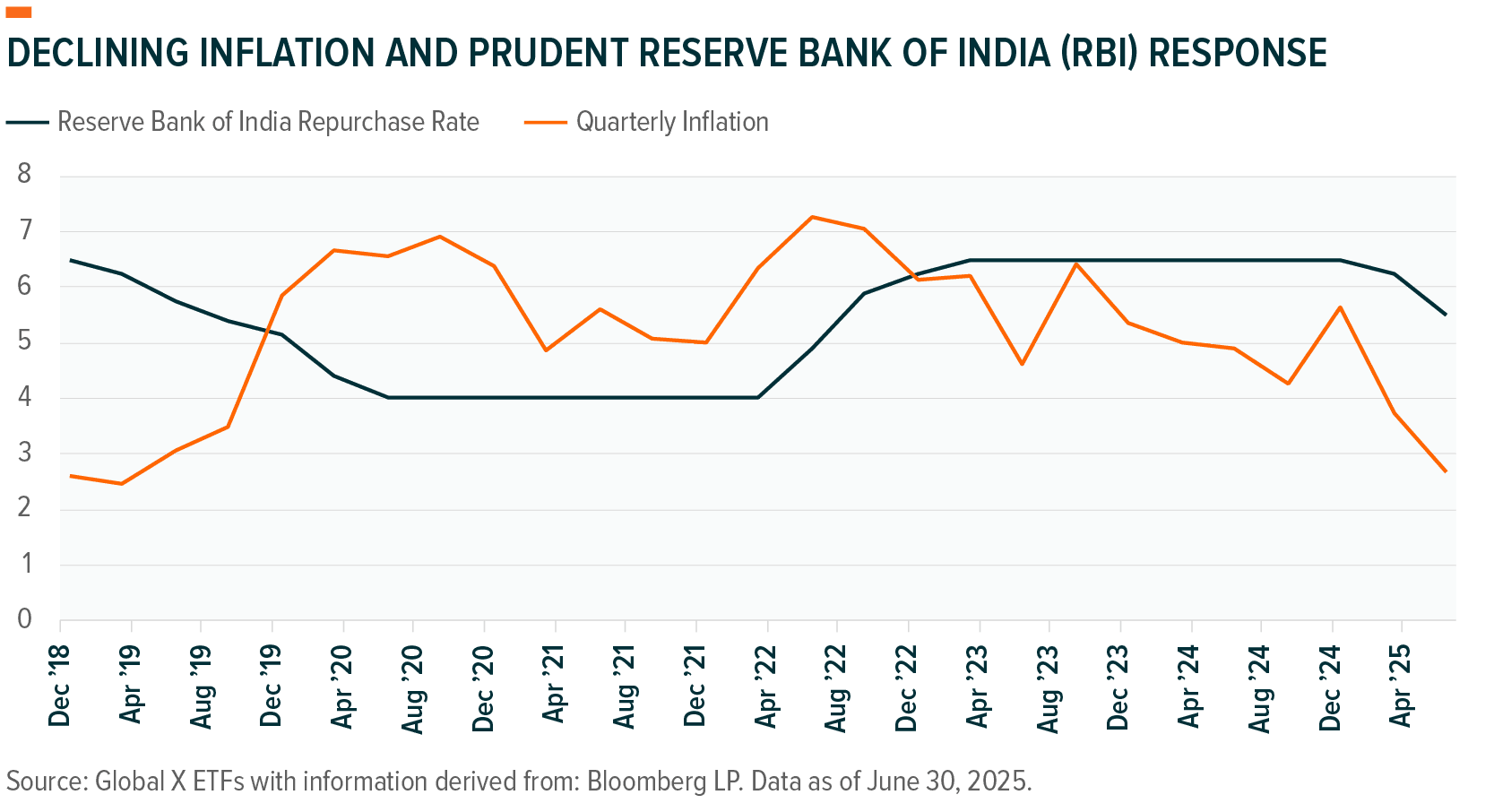

- Supportive Macro Trends: Consensus forecasts call for India’s current account deficit to be around 0.8% of GDP in FY2026, while FX reserves of USD695bn are near all-time highs and provide adequate import cover of ~11 months.3 Meanwhile, inflation is forecast to fall to ~2.8% in FY26, which has allowed the RBI to cut rates 100 basis points (bps), to 5.5%, over the first half of calendar 2025.4 In fact, July’s recent inflation print of 1.6% year over year was below that of even the U.S. and EU!5 Inflation benefited from the deflationary tailwinds of low energy prices (India imports nearly 90% of its oil requirements) and positive consecutive monsoon seasons (improved crop yields and limited food inflation).6 These drivers helped support rural livelihoods (~60% of the population), while increased reservoirs for hydroelectric power plants also tempered inflation expectations.7

Improvement in Ease of Doing Business and the Rebirth of the Indian Consumer

In nearly every meeting, the key theme that stood out was the clear shift in policies to support consumers. After several years of limited or targeted support, the government is finally stepping up to bolster domestic consumption. While India’s Chief Economic Adviser foresees a growth drag of around 0.5% per annum to GDP from trade and tariff headwinds, consumption focused policy changes could more than offset the trade impact, while also supporting a premiumization trend for corporates.8

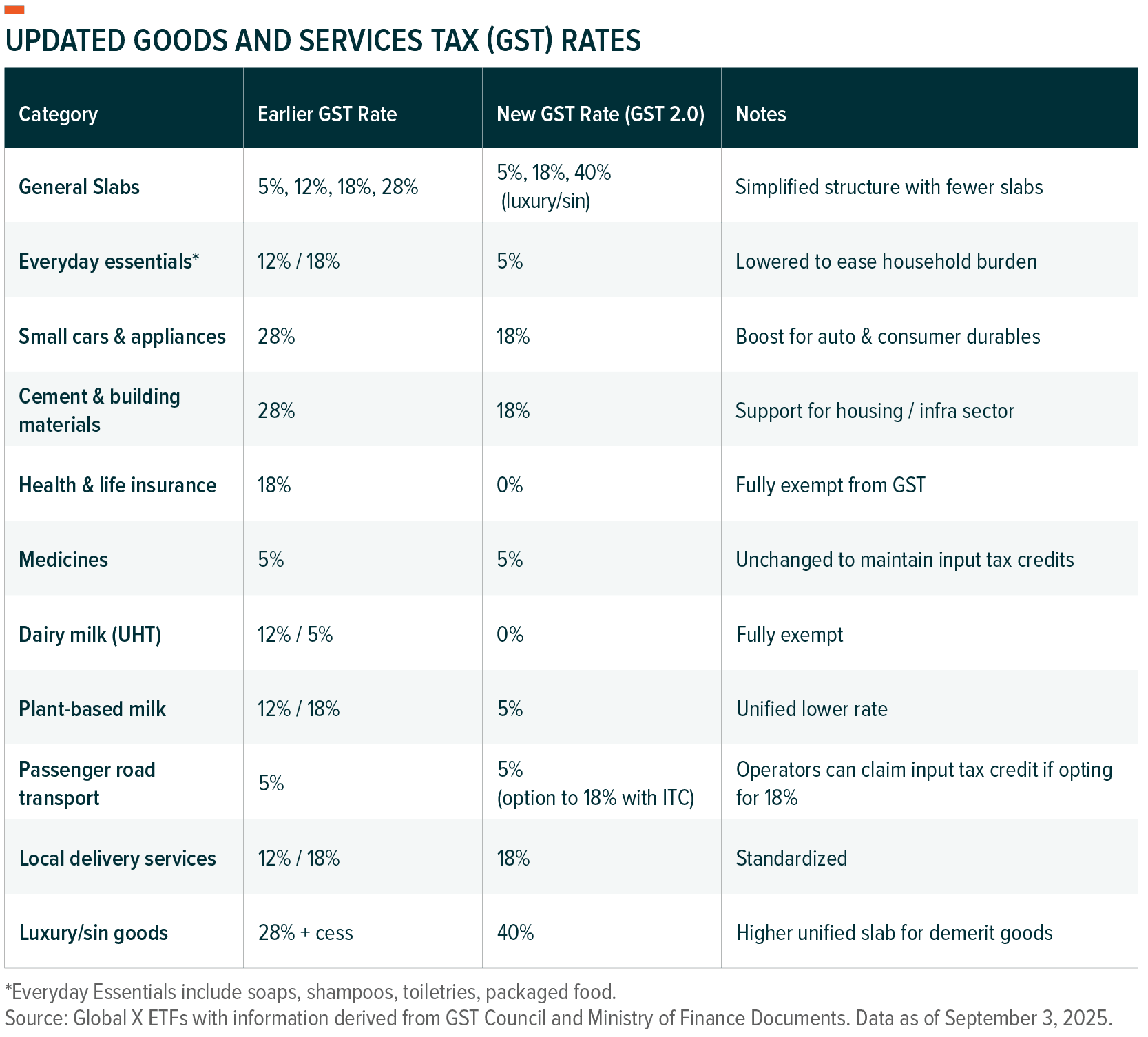

- GST 2.0 Tax Cuts: A new, simplified tax structure (going from four different rates for Goods and Services Tax to two) went into effect on September 22, 2025 ahead of the festive season (Diwali / Navratri). These changes should help reduce the tax burden on households, encourage consumption, and stimulate economic growth. In addition, the government is simplifying filing through technology while empowering MSMEs and manufacturers by fixing inverted duty structures and simpler rates to support the Make in India program.9

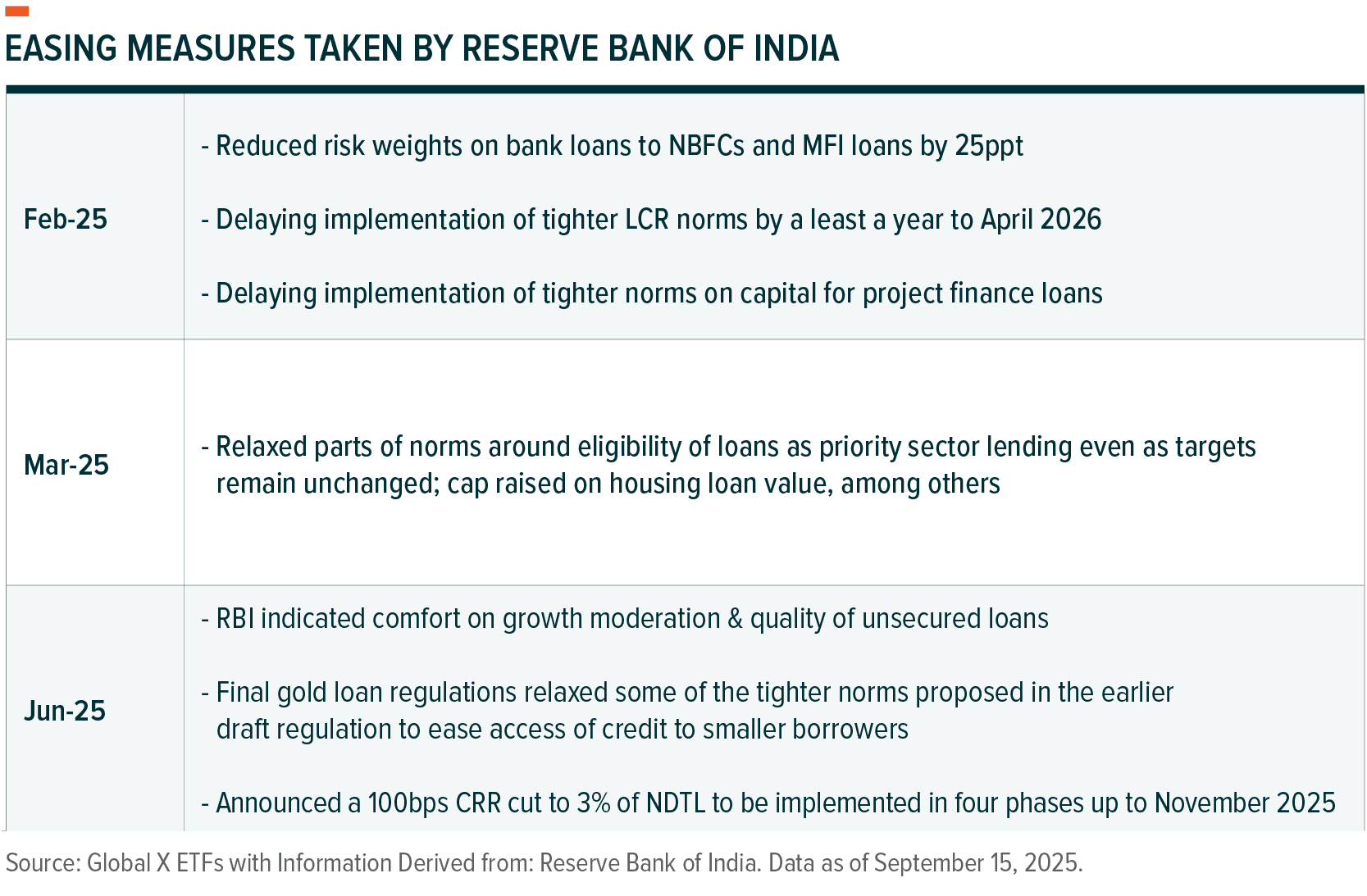

- RBI’s Shift to a Pro-Growth Stance: The RBI has shifted to a more pro-growth stance since Sanjay Malhotra took office as RBI Governor in December 2024. The table above shows several of the easing measures taken by the RBI this year.

- Deregulation & Reforms: In addition to meaningful tax changes, the government is also implementing reforms across various sectors to increase exports, improve tax collection efficiency, expedite logistics gains, improve labor participation, and drive India’s green transition.

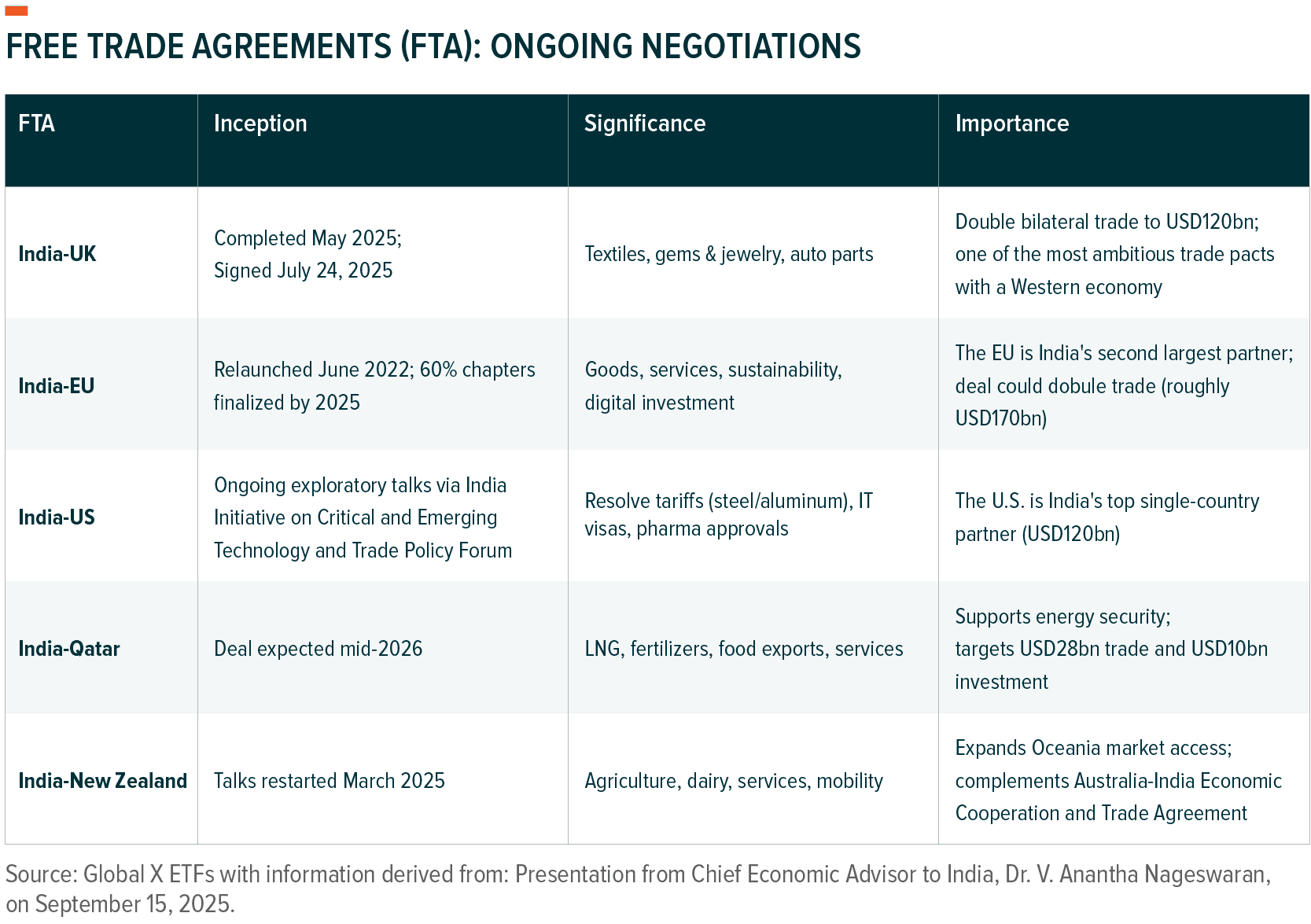

- Diversifying Trade: Though we expect symbiotic deals with the U.S. and Europe, the government has a clear mandate to diversify exports by fast tracking trade agreements in Asia, Africa, and Latin America. We also note the recent agreement India signed with the UK.

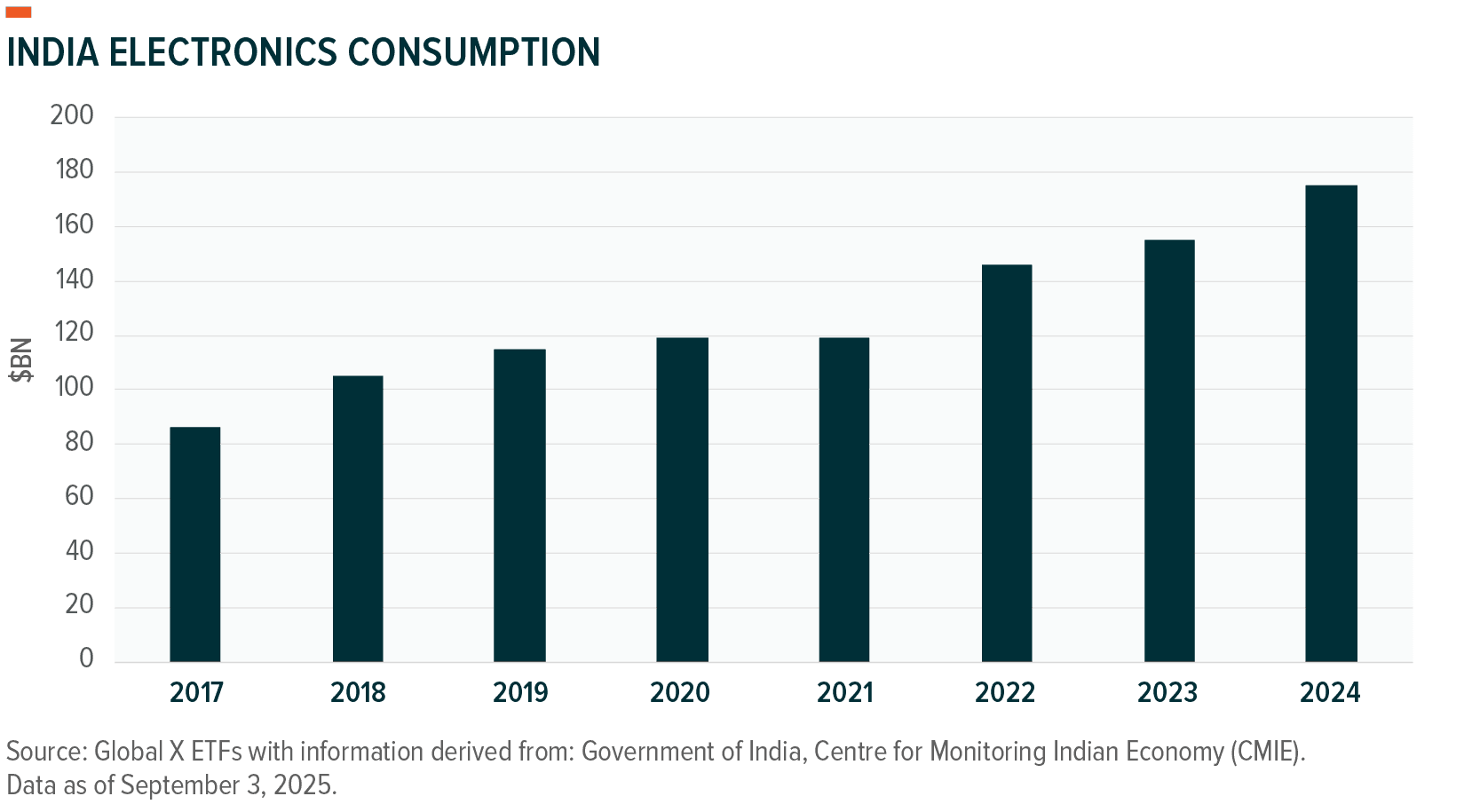

- Digitization Trend: Demand for electronics is growing, led by increasing disposable income, digital adoption, and the government’s digitization push.

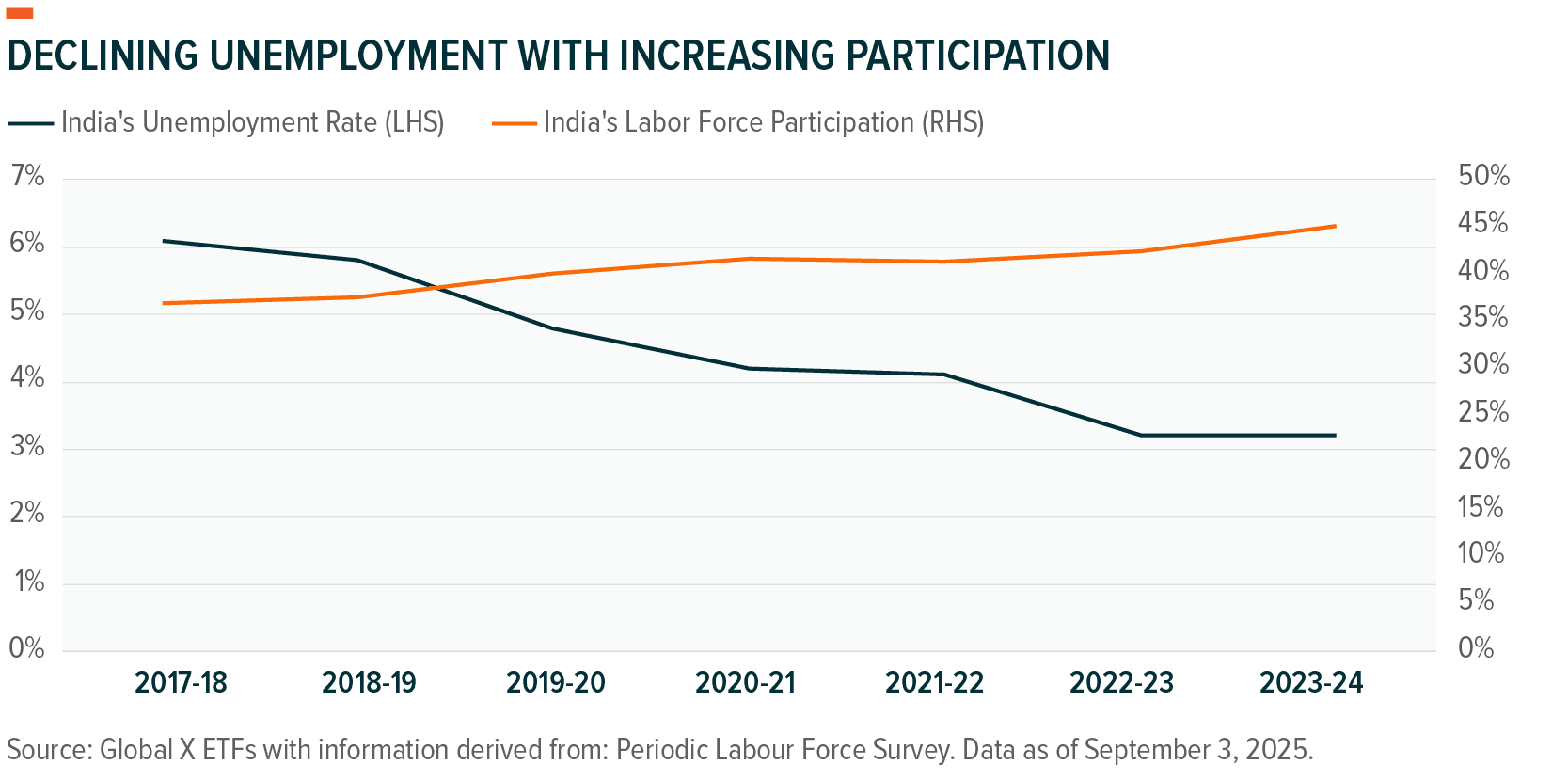

- Wage Hikes and Job Growth: Given the young and growing population, the government has maintained job upskilling as a key priority to raise income levels and living standards. In January, the Central Pay Commissions (CPC) recommended several changes that could see ~30-40mn employees benefit from salary increases, with some as high as 30-35%, driving a potential USD50bn boost in consumption with implementation possible as early as 2026.10

- Benefits of the Monsoon Season: The rural economy is seeing improvement after two successive good monsoon seasons. Above average rainfall has supported higher kharif sowing, led to comfortable buffer stocks, and better prospects for agriculture, which should help maintain food inflation at lower levels.

- Stronger Consumers and Runway for Growth: From discussions with retailers, we expect store additions to remain strong, overall, along with sustained same-store-sales (SSS) growth. Platforms such as Eternal (Zomato; food delivery and reservations), Swiggy (online food ordering and delivery), and Nykaa (cosmetics) should benefit from both more users and increasing frequency. Furthermore, we see scope for improving take rates and rising ad income to support margin expansion on scale efficiencies at these three companies.

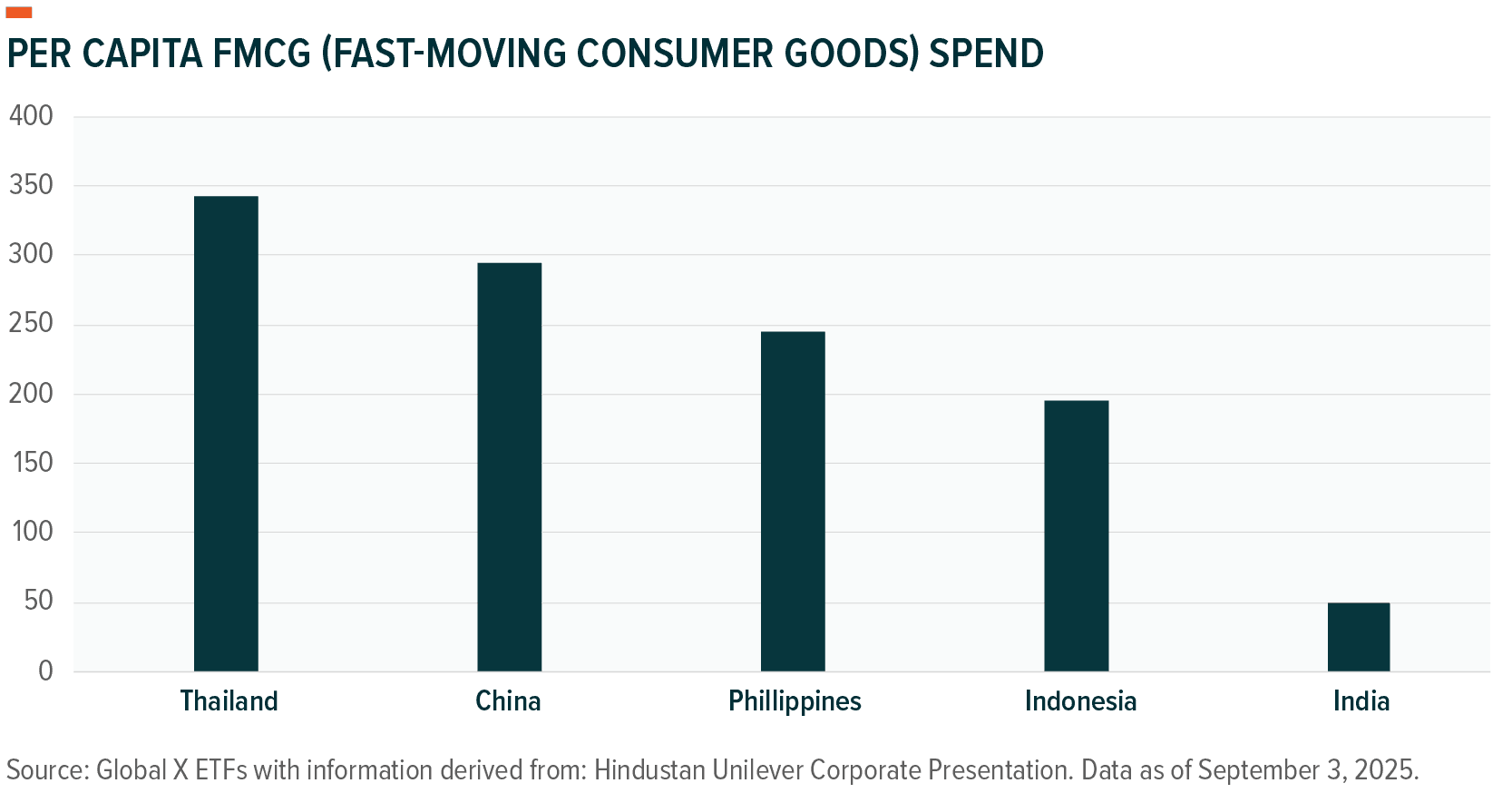

- Premiumization – Consumers Want More: Favorable demographics, rising disposable incomes, and digital improvements already started a meaningful premiumization trend in India. Now, with the addition of significant consumer support via tax cuts, we see increasing scope for the trend to accelerate. Areas such as travel and hospitality have seen strong momentum over the last three years, reflecting increased willingness to spend more on higher quality experiences and products. Benchmarking India to other peers in areas such as aviation gives a potential glimpse of the opportunity ahead for players such as IndiGo Airlines. India is the third largest aviation market by passenger volume (behind the U.S. and China), yet still only represents around 4% of global traffic versus roughly 18% of the global population.11

Takeaways From the Ground

- Other Key Policy Priorities for the Government: Our visit left us with a clear sense of India’s urgency to continue boosting private investment, enhancing manufacturing capacity by strengthening the MSME sector, and furthering systematic deregulation (Ease of Doing Business 2.0).

- Quick Commerce: The story is no longer just about the platforms. In fact, most companies are leveraging QC logistics and capabilities to rapidly launch, test, and tailor new products to specific regional needs. This is changing how companies test products, allowing for greater premiumization opportunities.

- Don’t Just Take Our Word For It: We were also pleased to see S&P announce a sovereign upgrade to BBB Stable (from BBB-) in August, while Morningstar DBRS upgraded the country’s rating from BBB (low) to BBB due to an improved macroeconomic outlook, stronger reforms, and fiscal resilience.12,13

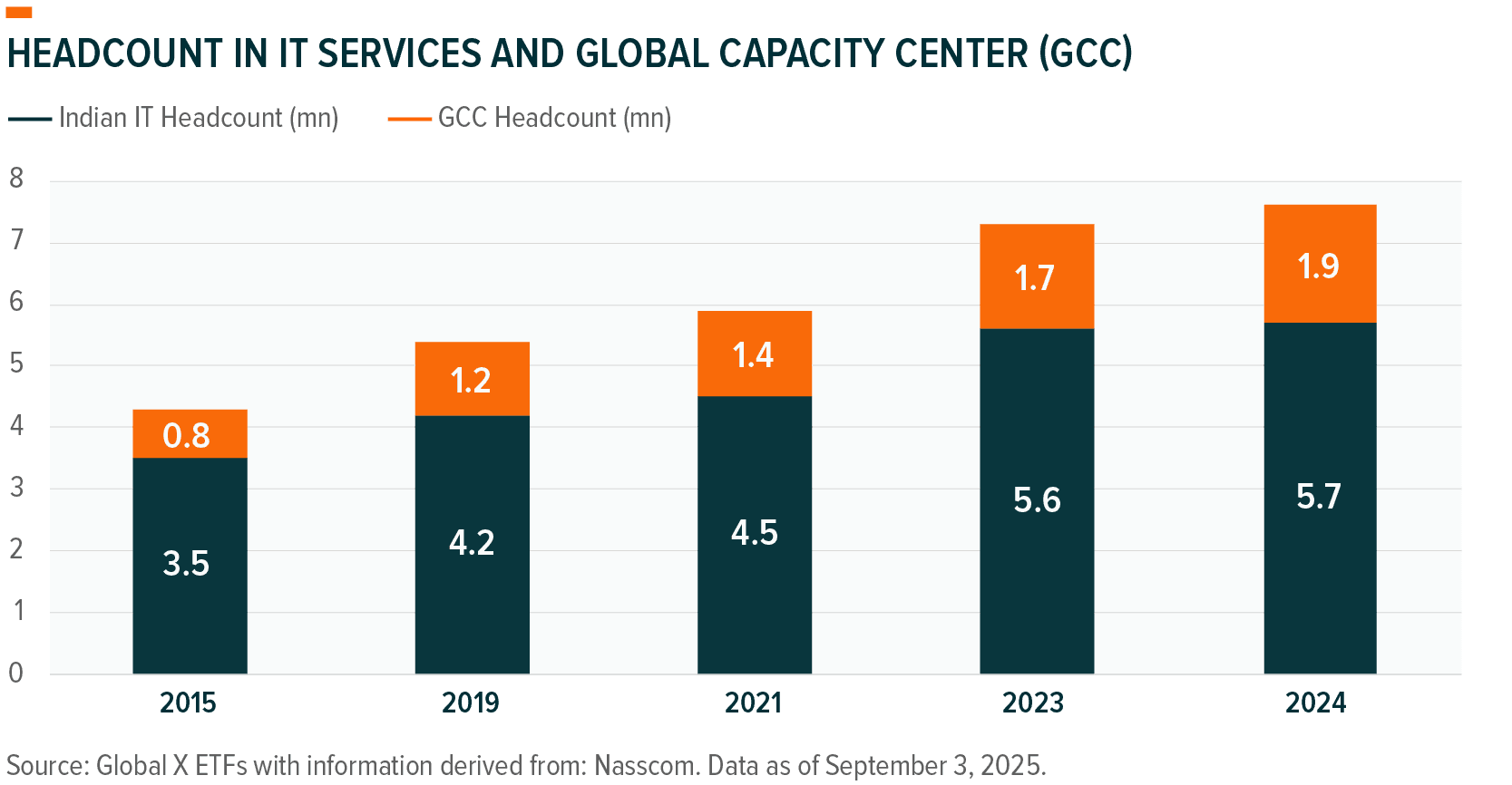

- IT Services: Although the new $100,000 fee for U.S. H-1B visa applicants will be a headwind, the move could also accelerate offshoring trends to India, which would help nearshoring and automation domestically, while also potentially reducing “brain drain” as fewer Indian students and professionals go abroad. Finally, this shift could drive higher IT wages in India and further support urban consumption.

Meeting Highlights

- InterGlobe Aviation: The Company operates IndiGo, which is the first successful low-cost airline operator in the country. Instead of competing directly with other large carriers, IndiGo is focused on converting a growing share of the existing ~7bn domestic train passengers every year. A clear beneficiary of consumers’ growing preference for premiumization, the company recently launched a new loyalty program as well as code share with most leading global airlines. Furthermore, as it adds larger planes, IndiGo is widening its reach (i.e. distance traveled), expanding its total addressable market to more leisure travelers. With over 900 planes in the pipeline and a recent upgrade from Moody’s to Investment Grade, IndiGo presents an interesting opportunity for investors to tap shifting consumer habits and preferences.

- KFin Technologies: KFin operates as a RTA (registrar & transfer agent) and has grown to be a leading Indian FinTech platform. The Company has become the backbone of many asset managers, issuers, pension funds, and wealth platforms and has been a clear beneficiary from the growth in the domestic asset management industry, as well as ongoing financialization trends in the country. KFin is also growing its international footprint, while adding new financial verticals such as fund administration, pensions, and alternative investments. The company enjoys strong operating leverage with high client stickiness due to switching complexity and costs.

Conclusion

Fiscal second-quarter GDP came in as a positive surprise to markets at 7.8%, and the combination of carryforward momentum with prospects for a strong festive season suggests growth will remain strong.14 This would support India’s growth differential versus peers, as well as our longer-term investment thesis that India will maintain a higher growth differential versus the rest of the word for longer. Manufacturing and services are starting to climb, while consumption and investment should continue to anchor growth into yearend. The government has proven itself by achieving fiscal deficit targets, supporting credibility and providing comfort that their recent push to support consumers can potentially help drive a market re-rating. Should domestic demand strengthen with every quarter and the government continue to improve the ease of doing business (e.g. deregulation and digitization) like we expect, we see India being able to achieve its medium-term $10tn GDP target.