The video gaming industry is often dismissed as a niche investment category, but its scale tells a different story. In 2024, global spending on video games reached nearly $180 billion, exceeding the combined total spent on professional sports.1,2 Nearly five years after the COVID boom, we believe the sector deserves renewed attention as it approaches a critical inflection point.

A wave of major game launches is energizing demand, and a new console upgrade cycle is emerging as new titles push the limits of existing hardware. AI is transforming gameplay and development, boosting player engagement while helping game publishers and studios accelerate production and improve margins. Receding regulatory headwinds in key markets like China are also fueling momentum for publishers and hardware makers. With these forces in play, the global gamer base is expected to surpass 3 billion by 2029, a 17% increase from 2024.3

We expect advances in hardware, networks, and gaming applications, along with emerging paradigms like social and cloud gaming, to continue to fuel the industry’s growth flywheel. Considering these dynamics, we believe the Video Games theme presents a favorably priced, under-the-radar opportunity for investors to consider. And in our view, the Global X Video Games & Esports ETF (HERO) can offer investors targeted exposure to some of fastest growing and dynamic subsegments of this market.

Key Takeaways

- We expect new platforms, AI integration, lower access costs, and renewed momentum in Asia as regulations ease can help drive global games revenue growth in the coming years.

- New releases are creating strong momentum for top game publishers, with player engagement and spending on the rise. High anticipation for upcoming titles suggests further growth potential.

- Generative AI is reshaping and expanding the gaming industry by reducing development times and costs while improving game quality. Major publishers and platforms that enable AI-driven development are among the key beneficiaries.

Gaming is a Massive Global Market with Robust Runway for Growth

The global video gaming market grew to $178 billion in 2024, surpassing professional sports, with forecasts suggesting it could grow another 11.5% to exceed $198 billion by 2027.4,5 The scale and the diversity of the market are unparalleled within the entertainment industry. The emergence of new technological tools, such as AI, is creating more opportunities for the industry to reinvest and innovate, particularly to accelerate game development, reduce costs, boost engagement, and improve advertising targeting. Similarly, the rise in newer business models, such as subscription-based gaming, as well as newer platforms like mobile and cloud gaming are lowering barriers to entry and broadening access. Notably, cloud gaming is expected to grow at a 25% compounded annual growth rate (CAGR), reaching over $25 billion by 2029.6

Social gaming is another subsegment displaying impressive growth. Roblox, which generates more than $4 billion in annualized revenues, has grown revenues at an impressive 29% year-over-year (YoY) rate, as shown by the company’s most recent earnings release. User engagement remains robust too, with average daily active users climbing 26% YoY to 97.8 million and hours spent on the platform growing 30% YoY.7 These metrics highlight strong success of social gaming and user-generated content, a subsegment in the gaming space that is becoming increasingly popular with younger games, and a trend likely to accelerate with new on-device AI capabilities.

Regional Dynamics Are Contributing to Gaming’s Success

After decades of gradual progress, gaming has gone mainstream in the U.S. Roughly 213 million people play video games for at least 1 hour each week in the U.S. The average gamer spends 12.8 hours gaming per week, a number that is growing quickly as gaming evolves beyond younger generations. In 2004, just 17% of Americans aged 50 and older played video games; by 2024, that figure had risen to 29%.8

Similar trends are playing out in markets like China and Japan. In China, regulators—who once threatened aggressive restrictions on gaming time for young gamers—have taken a more relaxed stance toward gaming policies, supporting sustained growth. Investments in cloud gaming, 5G adoption, and AI-infused functionality are likely to keep growth elevated. In 2024, China’s gaming market grew nearly 7.5% YoY to over $44.8 billion, driven by the release of hit games like Justice Mobile from NetEase and continued momentum of Tencent’s Honor of Kings.9

One of the largest gaming companies in Japan, Konami Group, reported fiscal year (FY) 2025 revenue and profit growth of 17% YoY and 26% YoY, respectively, driven by strength across key titles in its Digital Entertainment business and sales of new console game releases.10 Gaming revenue in Japan is forecast to grow by another 6.22% in 2025 to reach US$50.94 billion, particularly driven by new hardware releases such as the Switch 2 by Nintendo.11

Regionally diverse growth drivers—from relaxed regulation in China to rising engagement among older U.S. gamers—underscore the cultural, policy, and market nuances shaping the gaming ecosystem. Rather than converging globally, demand is evolving along distinct paths. This complexity supports the theme’s durability, as we believe gaming’s next phase will be defined not just by innovation, but by its integration across geographies, age groups, and platforms.

A Robust New Release Slate and New Hardware Launches Are Catalyzing Growth

Major new releases like Call of Duty: Black Ops 6, and Helldivers II have helped top game publishers boost engagement in 2025. A gaming subtheme performing especially well is sports, including the EA Sports College Football 25 title. FY2025, which ended in March 2025, was a record year for Electronic Arts (EA) with net bookings totaling $7.35 billion, driven by over $1 billion in net bookings for the EA American football franchise. EA expects the momentum to carry into FY 2026, with bookings projected at $7.6–8.0 billion, ahead of analyst expectations.12

Another title where anticipation remains high is the Grand Theft Auto VI, which after repeated delays is now expected to be brought to market by Take Two Interactive in May 2026. The game’s trailer shattered records with 475+ million views in its first 24 hours.13 For context, the game’s current version, the GTA 5 generated over $8 billion in global revenue, making it the highest-grossing single entertainment product in history—across games, movies, books, and music.14

Helped by new releases potentially triggering hardware upgrades, the console market is projected to grow 20.9% through 2027, sharply outpacing mobile and PC.15 A hardware refresh cycle is on tap for 2025 and 2026, with Sony and Nintendo making early moves. Thanks to a strong lineup of exclusive titles, Sony had shipped 77.8 million PlayStation 5 units as of March 31, 2025, closely aligning with the PlayStation 4’s performance at a similar stage in its lifecycle.16 Nintendo’s Switch 2 sold more than 3.5 million units in the first four days following its recent June 2025 launch, putting the company on path to realizing its goal of selling 15 million units for FY 2026.17

Historically, hardware sales are a leading indicator of software and platform success. A substantial install base attracts developers and encourages increased software sales, which are typically more profitable than hardware, and overall platform growth. For instance, Sony sold over 160 million PlayStation 2 units, with software sales exceeding 1.5 billion units, while Nintendo sold 101.62 million Wii units and roughly 922 million software units.18,19

AI Integration Creates Growth Opportunities Across the Industry

Generative AI is beginning to transform game development, testing, and gameplay by reducing costs and dramatically shortening development times—by over 20x in some instances.20 The efficiencies that generative AI offers not only expands the gaming industry’s total addressable market but also lowers barriers to entry and can broaden the investment universe.

Key beneficiaries include major publishers like Take-Two Interactive and Ubisoft. Their scale, access to user data, and live-ops expertise offer competitive advantages, enabling reinvestment to preserve their market leadership. Smaller game publishers and studios could also benefit as they can launch new games, titles, and upgrades with much lower development costs as AI based coding assistants and creative generators help with productivity.

Also in line to benefit are game engines like Unity, distributors such as Xbox and PlayStation, and social platforms like Roblox. They may be more insulated from downside risks coming from AI enabled disruption and are well-positioned as gatekeepers enabling access to AI tools for developers.

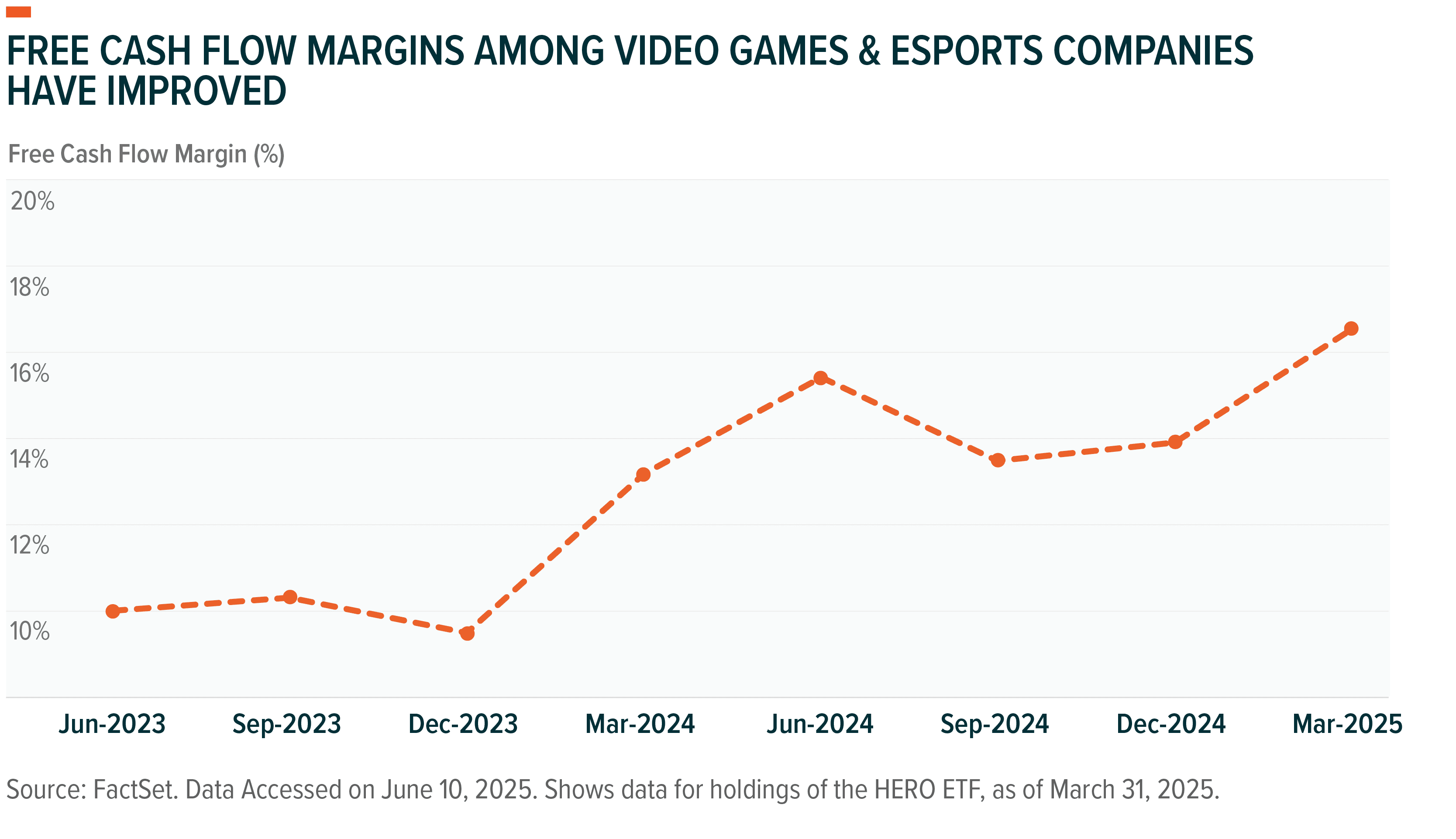

Gaming Fundamentals Have Strengthened

Companies across the Video Game & Esports theme boast attractive free cash flow margins and offer strong expected earnings growth. Notably, many leading players used the post-COVID market reset to streamline operations by reducing excess, cutting costs, and unlocking efficiencies through AI-driven tools. As a result, we believe the sector is entering its next growth phase on a stronger financial footing, with leaner cost structures and improved scalability.

In parallel, business model innovation has added structural strength to the theme. A key shift is the growing adoption of Gaming-as-a-Service (GaaS) business models, which enables developers to monetize long after a game’s release through subscription fees, in-game purchases, and ongoing content updates. Unlike traditional one-time game purchases, GaaS enables vendors to grow revenues more nimbly and consistently, even during periods of declining console and new title sales. It also helps game developers to maintain pricing power and supports margin stability.

Leading gaming companies have also expanded net bookings while containing production costs, largely by securing incremental spending on existing offerings. For example, Take-Two Interactive’s net bookings rose to $5.65 billion in FY 2025 from $3.55 billion in FY 2021, predominantly due to recurrent consumer spending.21 Similarly, Roblox's bookings climbed to $1.2 billion in Q1 2025, up from $774 million in Q1 2023.22 In our view, this level of monetization efficiency remains underappreciated by the market.

Lastly, gaming has historically demonstrated low sensitivity to economic cycles, with consumers maintaining spending even during slowdowns, which in our view positions the sector as a potential buffer in volatile markets. 23

HERO Is Strategically Aligned to Capture Video Games & Esports’ Long-Term Growth Potential

We believe that the Global X Video Games & Esports ETF (HERO) is well-positioned to capture the upside of rising gaming spend, engagement, and monetization. In summary, HERO seeks:

- Pureplay Exposure: HERO is a passively managed fund tracking an index that requires constituents to generate at least 50% of their revenue from video game and esports-related activities. Eligible companies include those that develop or publish video games, stream or distribute gaming and/or esport content, operate and/or own competitive esports leagues or teams, or produce gaming hardware, including augmented reality (AR) and virtual reality (VR) devices.

- Global Diversification: While the fund itself is non-diversified, HERO offers broad geographic diversification by including industry leaders from established and rapidly growing markets, including China, Japan, and other parts of Asia, in addition to the United States.

Conclusion: Video Gaming Industry Appears to Be At a Key Inflection Point

We believe the gaming industry is well positioned for continued momentum, even amid a broader economic slowdown. As consumers trim discretionary spending, digital entertainment remains a sticky and affordable outlet. Meanwhile, the resurgence of key markets like China and Japan appears sustainable in our view and generally underappreciated by investors. Looking ahead, gaming companies are likely to further harness AI to accelerate development cycles, deepen engagement, and refine advertising strategies, which should help catalyze growth and sustain margin improvements throughout this decade. HERO seeks to provide targeted access to the structural shifts shaping the Video Games & Esports theme, while maintaining global diversification in an effort to capture growth across key markets.

Related ETFs

HERO - Global X Video Games & Esports ETF

Click the fund name above to view current performance and holdings. Companies discussed may or may not be holdings of the fund. Holdings are subject to change. Current and future holdings are subject to risk.