Rohan Reddy

Rohan ReddyAfter a volatile Q4 in which MLPs were pushed down due to aggressive tax-loss selling, global growth concerns, falling oil prices, and weak equity market conditions, MLPs have enjoyed a strong recovery in early 2019. In this quarter’s MLP insights, we touch on some of the important developments happening in the MLP space, including:

- Incentive Distribution Rights (IDR) restructurings – the main alternative to C-Corp conversions

- The shifting investor base of MLPs and C-Corps

- Active vs. Passive MLP Investment Approaches

IDR restructurings – the main alternative to C-Corp conversions

2018 will be remembered as a pivotal year for the MLP structure. A variety of factors led to a host of once bellwether MLPs exploring, and in many cases converting to the more traditional C-Corp structure. Those electing to continue using the MLP structure still implemented substantial changes, including strengthening their balance sheets through distribution cuts, reducing distribution growth, and/or restructuring IDRs. In short, it was a year of substantial changes for an asset class that ought to be anything but fast-moving.

Despite the heightened activity in 2018, we believe the market is likely near the tail end of the mass C-Corp conversions. After the spike in conversions last year, midstream infrastructure is currently split 55%/45% in market cap between the C-Corp structure and MLPs. For remaining MLPs, the pervasive retail base, shareholder tax implications of a conversion, and a cautious approach to corporate taxes, means it may still make sense for many to remain in the MLP structure. Yet while not all MLPs will become C-Corps, the old model of coupling an income-oriented Limited Partner (LP) with a more growth-oriented C-Corp General Partner (GP) has lost its appeal among investors, who now seem to prefer structural simplicity over complexity.

As such, many remaining MLPs are moving to eliminate the incentive distribution rights (IDR) payments paid to their general partners – an under-the-radar trend within the midstream space that we consider the ‘plan B’ to a full-on C-Corp conversion.

Originally, IDRs were used to incentivize rapid growth and to divert volatile incremental cash flows to the GPs, while keeping more stable ones for the LPs. Yet as MLPs grew and more and more incremental cash flow went to the GPs, IDRs came to represent a significant handcuff on an MLP’s ability to fund their growth. These payments, coupled with high debt levels and low equity valuations, forced many MLPs to restructure their IDRs to free up cash flow to fund growth capex or reduce leverage.

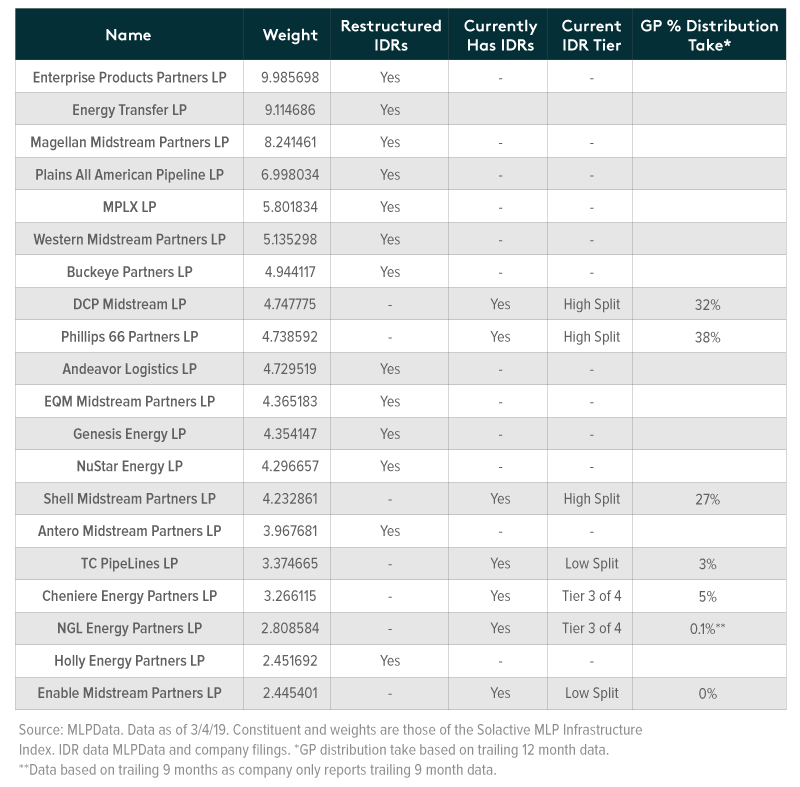

Q1 2019 may represent the apex of such restructurings. In February alone, there were three transactions to eliminate IDRs, with EQM Midstream Partners (EQM), PBF Logistics (PBFX), and Summit Midstream Partners (SMLP) each reaching new agreements with their GPs. Currently, just 26% of constituents in the Solactive MLP Infrastructure Index by weight have IDRs.1 Half of those MLPs still with IDRs are at the highest tier of splitting cash flows with their GP, meaning pressure to eliminate these IDRs remains prevalent.

As the midstream space continues to evolve, we believe that two distinct forms of energy infrastructure entities will exist: 1) Energy Infrastructure Corporations (EICs) that are structured like typical C-Corp corporations; and 2) streamlined midstream MLPs that do not have publicly traded GPs or IDRs tagged onto them. We believe this should make for a healthier growth story for both entities and allow for a cleaner due diligence process for prospective investors.

The shifting investor base of MLPs and C-Corps

One of the ramifications of an industry split between the C-Corp and MLP structures is that each entity type will attract different investor bases. MLP ownership is typically dominated by retail audiences and buyside firms with dedicated MLP strategies due to the attractiveness of high yields and the fact that many institutions are unable to buy MLPs for legal, regulatory, or investment mandate constraints. Foreign investors too, often see limited benefits to MLP investing due to the lack of taxable benefits afforded to US investors. Also restrictive is MLP exclusion from broad market indexes like the S&P 500, which may negatively affect MLPs as the investment landscape continues to shift towards passive investing.

The C-Corp structure avoids many of these structural issues that pertain to MLPs- a key argument for why MLPs should considering converting. This generally means that C-Corps should expect to see greater ownership from institutions, passive fund managers, and foreign firms.

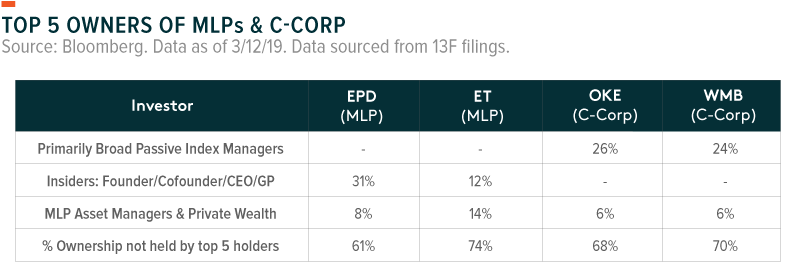

Given that we are a few quarters removed from a few major C-Corp conversions, we looked into how the ownership of these newly minted C-Corps compares to similar MLPs.

Combing through 13F filings, the largest C-Corp conversions in the past couple years, Oneok Inc (OKE) and Williams Cos (WMB) have clearly been affected by passive index flows, given that they are now eligible for broad index inclusion. The three largest holders of both these companies are Vanguard, BlackRock, & State Street, all of whom run among the largest index funds in the world.

By comparison, the two largest MLPs, Enterprise Product Partners (EPD) and Energy Transfer LP (ET), continue to show investor bases similar to historic MLP ownership. Investors are largely comprised of MLP Asset Managers and Private Wealth firms which cater to retail clients, and insiders that consist of founders, CEOs and affiliated companies.

In the table below, we compile and categorize the ownership data on the top 5 owners of each MLPs & C-Corp.

The base that remains largely elusive to the broader energy infrastructure complex has been generalist investors. While there has been some pickup in allocations from mutual funds with broader investment mandates and certain hedge funds, that group has not moved into the space en masse.

We believe that the entrance of these generalist investors into the C-Corp names could drive a meaningful wedge in the valuations of C-Corps versus MLPs. The fact that this has not yet happened, is likely contributing to the stagnating number of C-Corp conversions recently. Until there is further evidence of valuation expansion, we expect there will be less desire among MLP management teams to rush into a C-Corp conversion.

Active vs. Passive MLP Investment Approaches

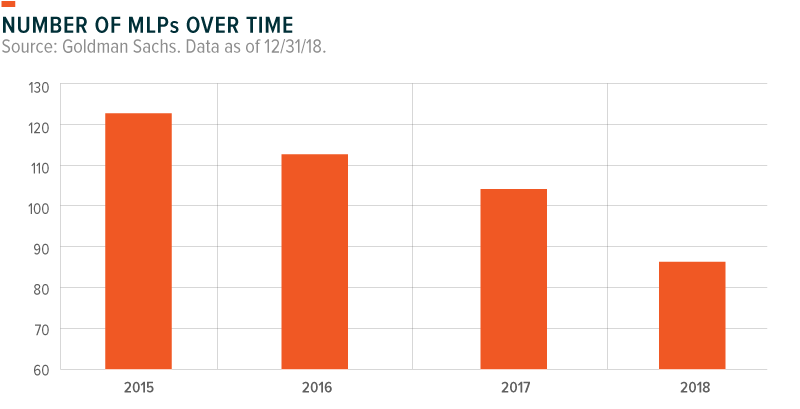

This leads us into the final part of our analysis, in which we delve into the active vs. passive nature of the newly developing energy infrastructure world. We previously evaluated active vs. passive MLP investing a couple years ago, but the topic has been generating more buzz recently as the magnitude of C-Corp conversions has left a narrowing opportunity set for MLP managers.

At a high level, the consolidating universe would suggest that alpha would be more difficult to generate with fewer MLPs. The Fundamental Law of Active Management, developed by Richard Grinold, attributes an active manager’s excess returns per unit of risk to their skill level, investment constraints, and the size of the investment opportunity set. This means that all else equal, if the number of investment opportunities in the manager’s universe begins to fall, a manager’s ability to generate excess risk-adjusted returns above a benchmark will fall. The formula to this theory is described below:

Information Ratio = Information Coefficient (skill level) * √breadth * Transfer Coefficient (TC)2

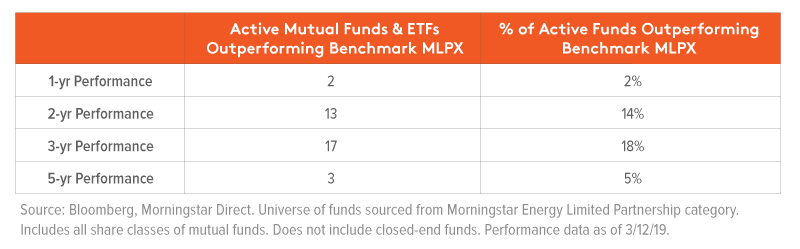

Simplifications of MLP family complexes, C-Corp conversions, and mergers are all tightening the size of investable universe, which inhibits a manager’s ability to outperform according to Grinhold’s theory. As shown in the table below, active managers have had a difficult time outperforming, both in today’s changing environment, as well as over longer time frames.

In short, active energy infrastructure managers have historically failed to consistently deliver alpha, and the consolidating universe only seems to exacerbate those challenges. We believe this should be a strong consideration when evaluating active vs. passive fund options. The possibility of taking on a manager’s ability to outperform and its higher fees may not be worth the risk given today’s consolidating environment and a weak historical track record.

Related ETFs:

MLPA: The Global X MLP ETF invests in some of the largest, most liquid midstream Master Limited Partnerships (MLPs).

MLPX: The Global X MLP & Energy Infrastructure ETF is a tax-efficient vehicle for gaining access to MLPs and similar entities, such as the General Partners of MLPs and energy infrastructure corporations.

Please click the fund names above for current fund holdings. Holdings are subject to change.

Definitions:

Alpha: Alpha is defined as the excess return of a fund relative to a benchmark index.