Michelle Cluver

Michelle Cluver Rohan Reddy

Rohan ReddyFixed income as either a security blanket or provider of higher income looks a little thin in early 2020. Following their downward trajectory over the last 30 years, U.S. Treasury yields are near historic lows. Where to find yield and portfolio diversifiers is one of the most pressing questions facing investors in this later-cycle market environment. It’s a particularly important question as the effects of population aging take hold. But there’s income out there, including through equity income solutions. This whitepaper explores different ways to find yield and provides suggestions on how to balance risks when seeking such yield instruments.

Contours of the Fixed Income Performance Landscape Shift in 2019

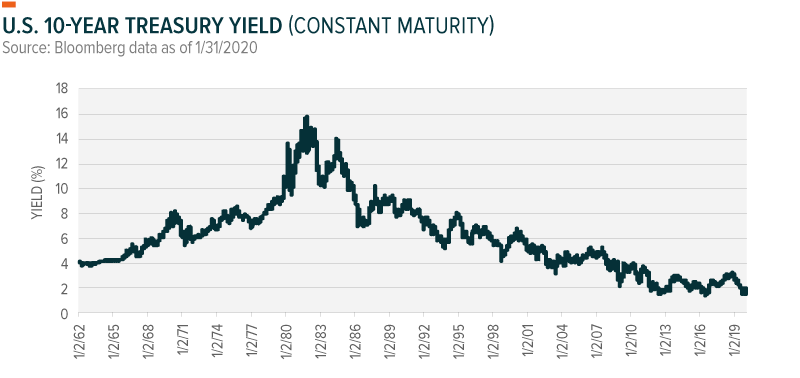

Continuing its 30-year trajectory, the yield on traditional fixed income securities declined significantly in 2019. In mid-November 2018, the yield on the Bloomberg Barclay U.S. Aggregate Bond Index rose to 3.59%. Today, it’s around 2.6%, only marginally higher than the yield on the S&P 500 Index. However, price is inversely related to the yields currently available in the market, so as yields declined in 2019, fixed income generally performed well.

As an example, consider a 10-year Treasury bond purchased at the beginning of October 2018 and held for one year. Yield started at 3.05% and declined to 1.68% by the end of the holding period. At that point, the security traded at a 30% premium to par value, assuming purchase at par value.

How Low Can Yields Go? The Search for Yield Gets Complicated

Historically, the answer to this question was easy: 0%. But now the presence of negative yields makes it more difficult to answer that question. Low yields are a challenge in the U.S., but numerous developed markets currently having sub-zero yields compound the problem because positive yields on U.S. Treasuries look that much more enticing. And the resulting global demand for U.S. debt puts even more downward pressure on yields.

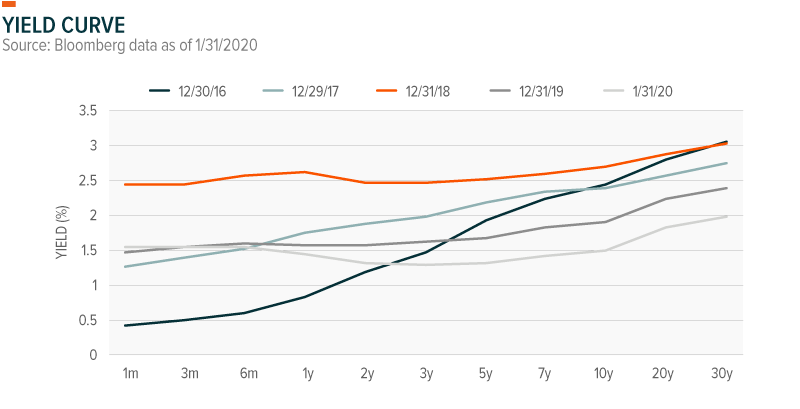

Over the last few years, the yield curve has flattened. The lack of term premium that has resulted could send yield seekers to different fixed income segments like Corporates, or even further down the capital structure to High Yield or Preferreds.

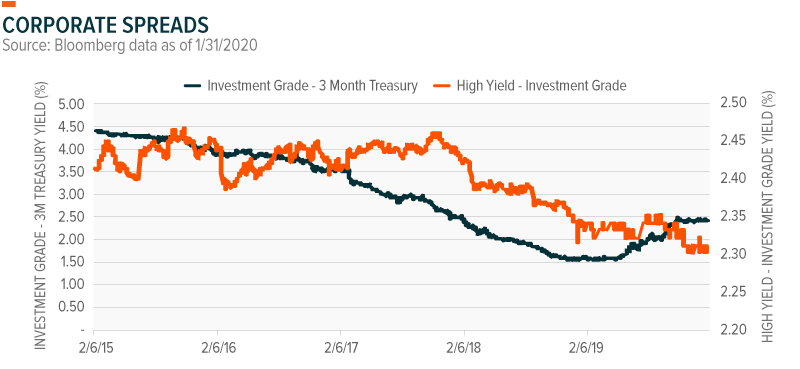

Corporate and country spreads relative to U.S. Treasuries are two areas where 0% should remain a solid floor. Still, the tightness in corporate spreads dampens potential risk-adjusted returns for Investment Grade and High Yield. Investment Grade and High Yield Corporate spreads are up slightly since Q2 2019. However, the spread between High Yield and Investment Grade Corporates continues to trend lower.

In the ETF markets, investors returned to High Yield bond funds in 2019 after a year of net redemptions in 2018. And they were rewarded for taking on additional credit risk. Corporate earning strength could lead to continued outperformance for High Yield in 2020. In our view, earnings per share (EPS) growth could slow year over year, but still be strong in terms of absolute levels.

Demographic Shift Underway: Population Aging Has Implications

The aging population makes the income theme all the more important. By 2035, Americans over the age of 65 will exceed the number of children in the country for the first time ever. Complicating matters is that more than a third of private sector workers do not have access to a workplace retirement plan.1

In our annual 2019 PR Survey, 70% of affluent investors cited retirement planning as a primary investment goal, easily making it the most important financial goal for wealthier investors. But it was also the goal these investors were least confident in achieving. Just 65% of survey participants said they were confident in their ability to meet their retirement goals. Still, over 60% of them said that they expected to retire in less than five years.

The disconnect between the population demographics and confidence to live comfortably in retirement means income generation strategies will be critical. Conventional investments like fixed income are an option, but as we’ll see below, there are potentially better strategies for the older demographic.

Is Fixed Income Still a Portfolio Diversifier? Not As Much As It Used to Be

Low rates create challenges for equities and fixed income. With the 10-year U.S. Treasury yield at 1.66%, financial markets are pricing in the U.S. economy having a natural growth rate below 2% for the next 10 years. This suggests that fixed income investors are currently positioned for an extended period of slow growth. However, equity markets continue to reach all-time highs, which means they’re not pricing in a decade of economic growth below 2%. The disconnect between the two means some period of adjustment is likely.2

This sets the stage for a potential breakdown in the historical relationship between equity and fixed income. Traditionally, fixed income responds to economic factors differently than equities, and thus brings diversification potential to a portfolio. But investors are in a tricky spot with fixed income today. The Federal Reserve (Fed) reduced short-term interest rates three times in 2019. Fed Chairman Jerome Powell also indicated that there would be a higher bar for future easing. So that leaves the market with super-low rates again, in a potentially slowing economy that saw the most predictive segment of the yield curve flash warning signals. The inversion of the 10-year/2-year spread in 2019 got the market’s attention and put recession risk squarely on the table.

We do not expect a recession in the next 12 months. However, a risk is that a recession becomes a self-fulfilling prophecy. To this point, consumers have done their part to help the economy. But if slowdown chatter grows louder and consumers curb their spending, then the math is simple: firms make less, invest less in their business, hire less or downsize. Small business sentiment and small business sales expectations, which, respectively, measure confidence and hiring, are two areas likely to shed light on any forthcoming recession.

So, the Fed’s on hold and, for its next act, a cut is more likely than a hike. But the driver of that cut would likely be heightened macroeconomic concerns. Not surprisingly, lower economic growth and profits are bad for equities. For fixed income, that scenario is more mixed; investors seek Treasuries and other risk-off assets, as riskier fixed income segments show a higher correlation with equities during market turmoil.

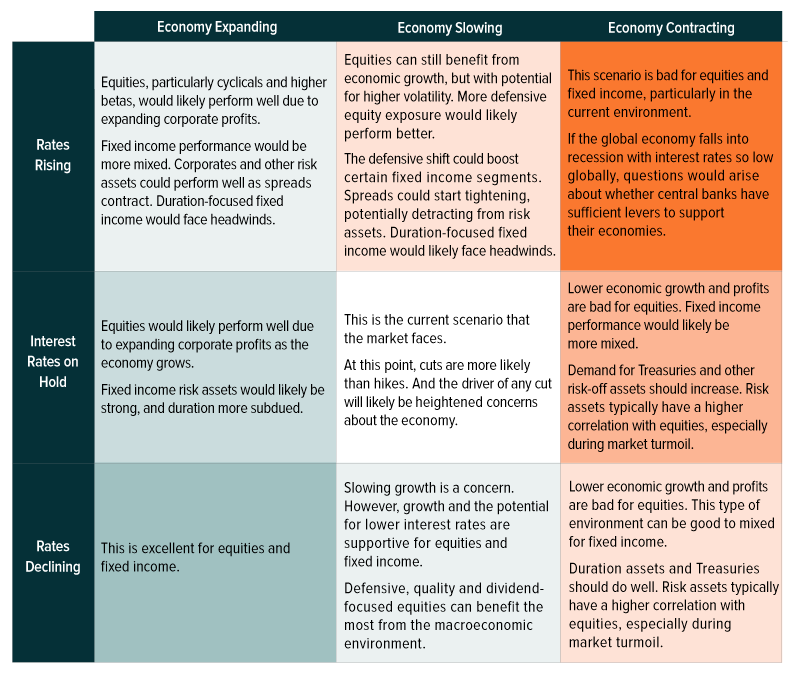

The table below outlines how equities and fixed income typically respond in different interest rate environments, and which segments of each perform well.

Equity Income Presents Opportunities

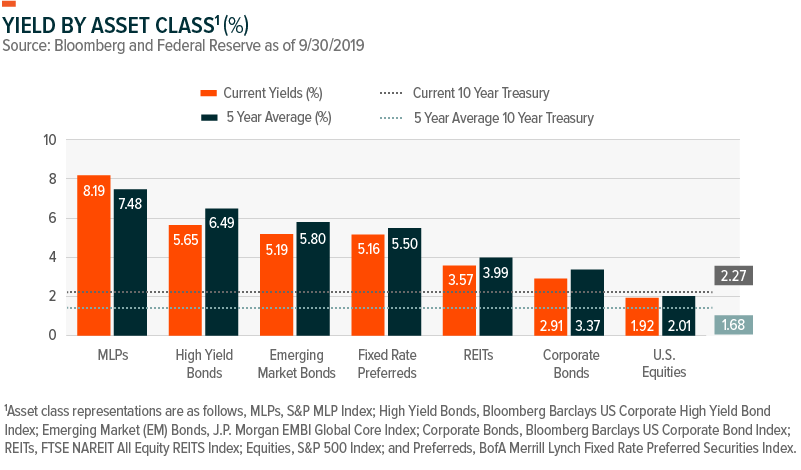

Without much yield available from traditional fixed income securities, a natural shift would be to explore equity income solutions. As the chart below shows, certain high-yielding equity income strategies continue to show a reasonably high correlation to interest rates, including Utilities and Real Estate, the bond proxy sectors. Other strategies, including covered calls, provide exposure that is independent of interest rates.

Below we provide more detail on the different equity income areas.

MLPs

Master Limited Partnerships (MLPs) are one of the historically highest-yielding equity income products available, and currently trade with a higher yield than they were a year ago. MLPs are a unique hybrid legal structure that combines the tax benefits of a private partnership with the liquidity of a publicly traded company. Similar to a Real Estate Investment Trust (REIT), MLPs pay mandatory regular dividends.

For more information on MLPs, please refer to our most recent MLP Insights and MLP Monthly Report.

Covered Calls

Covered calls have been a great way to generate income in a rangebound market. A covered call sells the upside potential and receives a premium. The premium becomes the income that the product generates. When volatility rises, the premium received rises to compensate for the higher level of volatility.

In a market trading within a reasonably tight range, covered calls benefit from receiving the premium income and potentially a small improvement in the underlying equities (or other) while not having the underlying called.

In a rising market, covered calls underperform the overall market due to the underlying being called. This affects the total return, not the income produced by the product.

In a declining market, covered calls provide a small buffer of protection because they receive the premium income.

For more information on covered calls, refer to our more in-depth explanation of covered calls.

Preferreds

Preferred equity has characteristics of both equity and fixed income. Within the capital structure, preferreds are above common equity and below bond holders. Holders of preferred equity receive dividend income ahead of common equity owners. While this protects the income component of preferreds, they don’t have the same price return potential as common equity. Preferreds have historically offered high yields compared to more traditional fixed income instruments. In addition, the yield from preferred stocks may be treated as qualified dividend income (QDI) rather than as ordinary income, resulting in favorable taxation.

For more information on preferreds, please refer to our Preferred Report.

High-Yielding Equities

High dividend stocks are a popular strategy for investors across the age demographic with income goals. Many high dividend stocks tend to have a value tilt because of their high-yielding nature. These stocks typically present yield and capital appreciation opportunities but generally lag the broader market, particularly within a growth focused rally.

High dividend equities are typically a core part of asset allocation within income models because of their many uses. Stocks in this area are overweight sectors like Utilities and Real Estate and underweight Technology. The value tilt can also lead to market cap drifts toward smaller and mid-cap stocks to generate higher yields, but the investors can manage these characteristics.

For more information on high-yielding assets, please see our Income Monitor.

Quality Dividends

Quality dividends are sometimes nicknamed the blue-chip dividend strategy because these companies are seen as being higher quality and more financially stable than other dividend-paying stocks. Blue chips are often name brand stocks investors are familiar with and hold onto for longer periods than other stocks. The defensive characteristics of these stocks make them more likely to maintain their dividends across varied economic environments, compared to other types of dividend stocks.

The tradeoff is the yield tends to be lower than their high dividend counterparts. However, their attractive financial profile often makes them a core strategic holding for long-term investors with income needs. The quality dividend space tends to lean more toward sectors like Consumer Staples, which have a longer track record of paying dividends.

For more information, please see our primer on dividend strategies.

REITs

Real Estate Investment Trusts (REITs) are a traditional, high income equity investment focused on the real estate sector. Under U.S. tax law, REITs must distribute 90% of their income to their shareholders, making them popular with income-focused investors. REITs in the U.S. get a lot of attention, but there is also a growing segment of international REITs in this low interest rate environment.

There are two classes of REITs: Equity REITs and Mortgage REITs. Equity REITs are focused on managing properties in different sub-segments of the real estate market, such as Warehouses, Industrial Properties, Hotels and Retail. Mortgage REITs invest in mortgages and are typically higher yielding than Equity REITs because of the leverage they use to take advantage of their mortgage portfolios.

To read more about REITs, see our explainer.

Holistic Approach to the Search for Higher Yields

Attaining a high yield is important. However, we believe the approach is important too. In our view, it is essential to take a holistic approach that considers the sustainability of that yield and the investment from a total return perspective.

Equity income solutions can fall into similar sectors and segments of the market, and thus may be affected by similar economic and market factors. When developing an equity income portfolio, diversification across equity income strategies is critical. It’s just as critical to round out the exposure with positions that can provide total return in environments where value and dividend exposure is out of favor. In line with this, we advocate incorporating sector and industry exposures that are systematically lacking within traditional equity income portfolios.

Conclusion

Traditional fixed income segments aren’t what they used to be from a yield perspective because market dynamics have pushed yields historically low. And that is an issue that we expect to become more pronounced as increasingly large swaths of the population enter their retirement years. We believe equity income solutions can be portfolio diversifiers, particularly those that are independent of interest rates. For yield in this environment, we encourage investors to think beyond the norm.