For much of the last three years, the U.S. manufacturing story was easier to believe structurally than cyclically. Reshoring, automation, electrification, and defense modernization all pointed to a larger domestic industrial base, but the near-term data remained uneven.

In 2026, that gap is closing, with industrial production trending positive, the Institute for Supply Management’s (ISM) Manufacturing PMI (Purchasing Manager’s Index) holding in expansion for five straight months, and policy-sensitive sectors like steel showing early evidence of import substitution.1 The manufacturing pipeline also remains substantial, led by semiconductors, pharmaceuticals, electrical equipment, and defense, creating a long runway for the domestic capacity buildout.

A full ramp-up will take time, but the direction of travel has turned. In our view, investing around the bottlenecks of American manufacturing may be a credible way to capture structural growth over the next several years, particularly across industrial automation, connectivity, power, infrastructure, and materials.

Key Takeaways

- We believe U.S. manufacturing is entering a cyclical upturn, with industrial production and the manufacturing PMI both improving.

- U.S. reshoring is backed by structural demand from industries and supply chains linked to data center components, electrification, semiconductors, and defense modernization.

- Owning themes that align with what could be a sustained trend in domestic production—including Infrastructure Development, Robotics and Automation, Connectivity, and Electrification—provides pathways to capture potential growth over the long term.

Domestic Manufacturing Signals Trend Positive in 2026

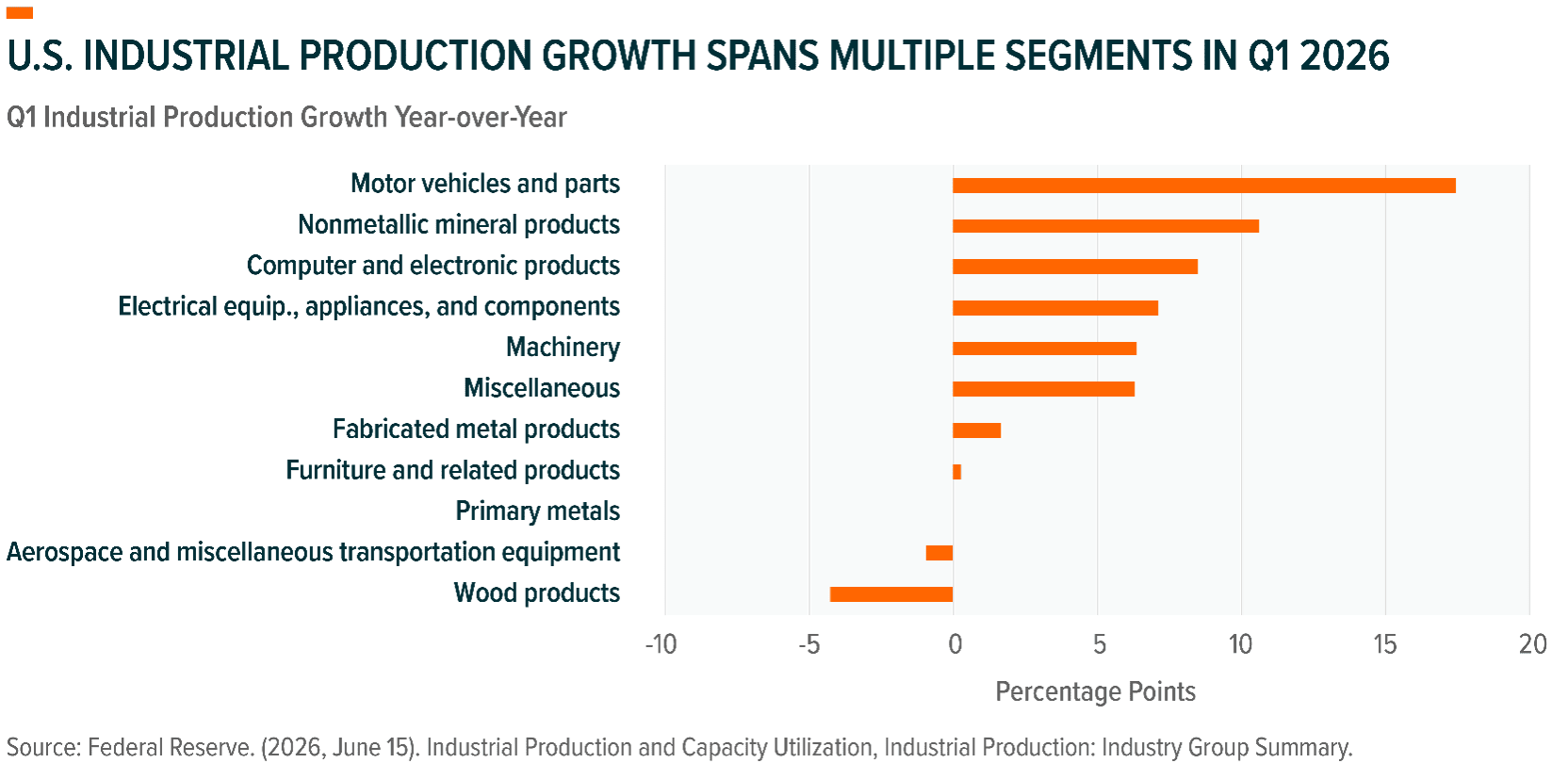

Hard economic data shows that the reshoring story, long viewed with skepticism, may finally be gaining operational traction. U.S. industrial production grew at a 2.1% annualized rate in Q1 2026 with 0.9% month-over-month growth in April and another 0.1% expansion in May.2 Durable manufacturing output, a cleaner production-side signal, rose 4.8% annualized in Q1, 1.1% in April, and another 0.8% in May, maintaining broad strength across computer and electronic products, electrical equipment, motor vehicles and parts, and machinery.3

The end-use signal is also improving, with business equipment, transit equipment, defense and space equipment, construction supplies, and materials pointing to firmer demand across markets tied to capital expenditure (CapEx) investment and industrial buildout.4

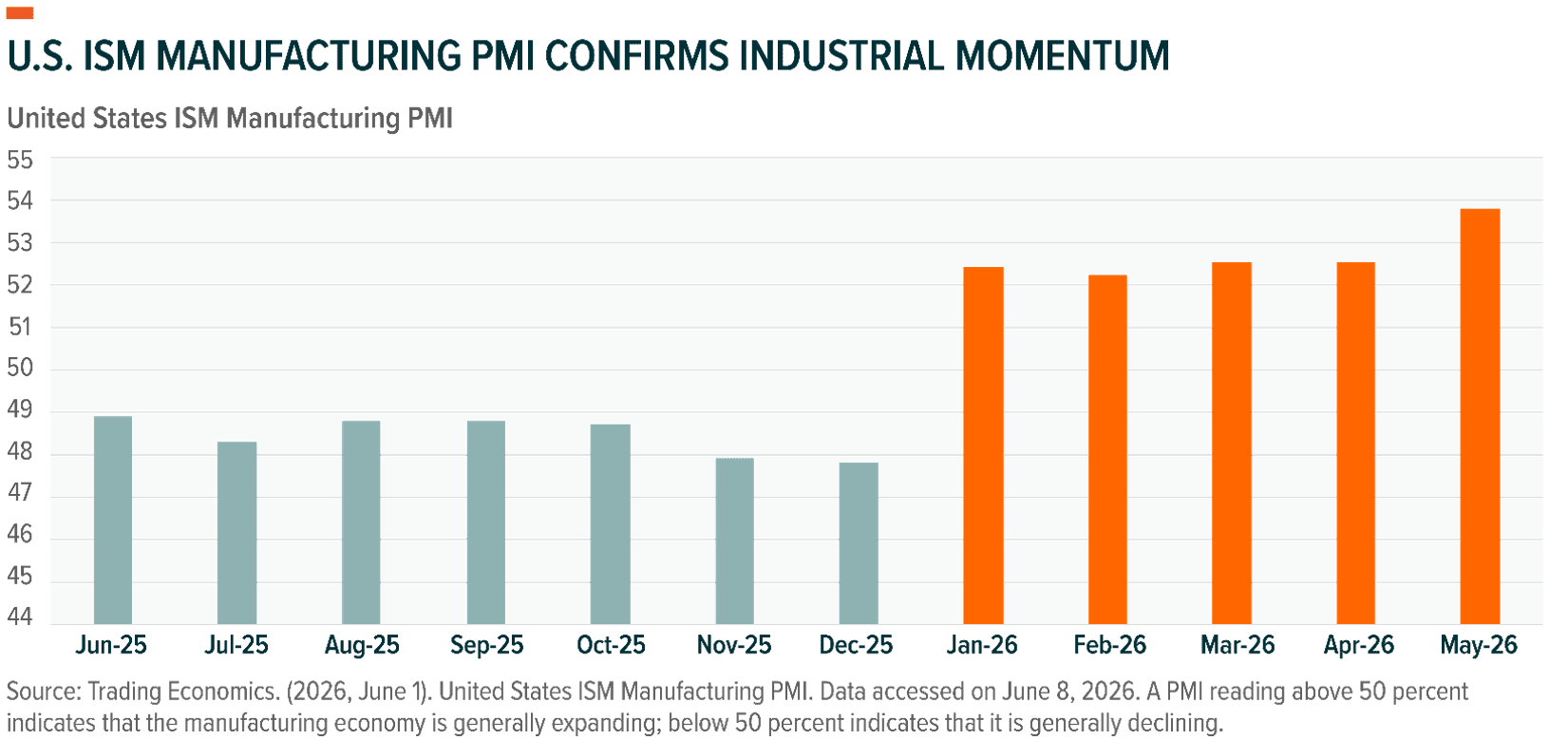

Survey data point in the same direction. ISM’s Manufacturing PMI rose to 54.0 in May from 52.7 in April, marking the sector’s fifth consecutive month of expansion after a 10-month contraction in 2025.5 The internals were also constructive, with New Orders strengthening, Production remaining in expansion, Backlogs rising, and customer inventories remaining tight, which is a condition ISM typically views as supportive for future production.6 S&P Global’s U.S. Manufacturing PMI confirmed the trend, rising to 55.1 in May from 54.5 in April, though some of the strength appears tied to stockpiling.7

Policy-sensitive sectors add evidence of import substitution, a sign that domestic capacity is filling in to absorb demand. Steel imports fell 12.6% in 2025 following enacted tariff policy, while finished steel imports declined 17.1%. U.S. steel mill production has increased in 2026, suggesting that trade policy is beginning to affect domestic production in select markets.8

Skeptics point to weak manufacturing payrolls, with employment, although improving, still tracking lower over the past year.9 That critique has merit, but it may also understate a structural shift toward a more automated, capital-intensive model, where output and capacity matter more than headcount. Manufacturing capacity utilization was 75.8% in April, still 2.4 percentage points below its long-run average.10 These datapoints keep us from embracing the most aggressive “reshoring boom” narrative, but they do not undercut the groundwork taking shape for a real turn in domestic industrial activity.

The Structural Foundation Is Intact

The reshoring case firmly rests on capital that is already committed. Our analysis indicates that companies announced roughly $1.42 trillion in planned U.S. manufacturing investment between January 2025 and mid-March 2026, concentrated in strategically important industries and led by semiconductors and pharmaceuticals. This builds on nearly $769 billion in private investments committed towards reshoring of strategic industries under the Biden administration.11

In a world shaped by geopolitical fragmentation, tariff risk, supply chain bottlenecks, and U.S.–China competition, critical industries need more domestic redundancy, and that need extends well beyond semiconductors and pharmaceuticals. Grid equipment, transformers, aerospace components, defense systems, industrial automation, and advanced electronics all sit at the intersection of U.S. economic competitiveness, supply chain resilience, and national security.

Recent corporate commentary reinforces that view, providing more evidence of capital flows into domestic industrial capacity tied to strategic industries such as the data center buildout. In Q1 2026, Vertiv highlighted its efforts to expand domestic manufacturing capacity to meet rising demand for thermal management equipment.12 Power equipment maker GE Vernova is scaling domestic production for on-site generation. The company has installed more than 280 new machines across its U.S. gas power factories over the past 15 months and added roughly 1,800 U.S. production workers in 2025 and 2026.13 Industrial automation provider Rockwell Automation reported demand from warehouse automation, semiconductors, and energy in fiscal Q2 2026. To meet this demand, the company is advancing its roughly $2 billion U.S. manufacturing expansion to reduce tariff exposure and shorten lead times.14 Eaton is tracking a U.S. mega-project pipeline of nearly $3 trillion across 866 announced projects and is expanding U.S. production capacity to capture its share.15

Policy measures underpin the durability of the trend. The CHIPS Act of 2022 anchored semiconductor investment, and substantial incentives continue to roll out to support the production of strategic chips. Recent Defense Production Act authorities target domestic grid infrastructure and equipment, including transformers and related electrical equipment.16 Meanwhile, rebuilding depleted munitions inventories due to the Iran conflict is likely to require further expansion of the defense industrial base.17 The U.S. also recently committed $2 billion to seed domestic quantum computing production.18

Navigating the Reshoring Cycle Requires Mapping the Investable Stack

For investors, we believe the reshoring opportunity is less about owning manufacturers broadly and more about owning the bottlenecks that make domestic production possible. We believe the investable stack starts with infrastructure development, moves through automation and connectivity, and ultimately depends on power.

Infrastructure Developers: Building the Foundation for Reshoring

Before reshoring becomes a production story, it is a land, materials, engineering, and construction story. New capacity requires site preparation, roads, utilities, industrial buildings, equipment installation, and logistics, all of which drive construction spending through the infrastructure value chain. That backdrop creates potential opportunities across engineering and construction, raw materials, heavy equipment, and industrial transportation. Aging U.S. infrastructure, increasingly under stress and in need of broad modernization, adds another layer of tailwinds and extends the development pipeline.

Robotics, Automation, and Connectivity: Running Next-Gen Factories

The reshoring cycle has been concentrated in high-throughput, high-precision sectors like semiconductors, electronics, autos, and industrial equipment, where automation is the operating model rather than a productivity overlay. Higher U.S. labor costs, persistent skilled-labor shortages, and rising quality requirements all strengthen the case for robotics. The connectivity layer behind smart factories, including sensors and industrial software, stands to benefit alongside it.

Electrification: Powering Manufacturing

Reshoring arrives alongside AI data center expansion, electric vehicle adoption, and broader electrification, creating a new demand cycle for electricity after years of flat growth. Factories need reliable, affordable, and scalable power, potentially positioning the companies that expand and harden the grid, add generation, deploy storage, and improve load management to emerge as the cycle’s winners.

Conclusion: Early Throughput, Long Runway

The U.S. manufacturing story could be steadily shifting from one of future promise to actual throughput. The factories, incentives, and capital expenditure plans are largely in place, while early signals from industrial production, ISM data, and policy-sensitive sectors suggest output could scale quickly to meet rising demand. In our view, the opportunity for investors lies in the key enablers of that throughput: infrastructure development, advanced automation, and next-generation power infrastructure.