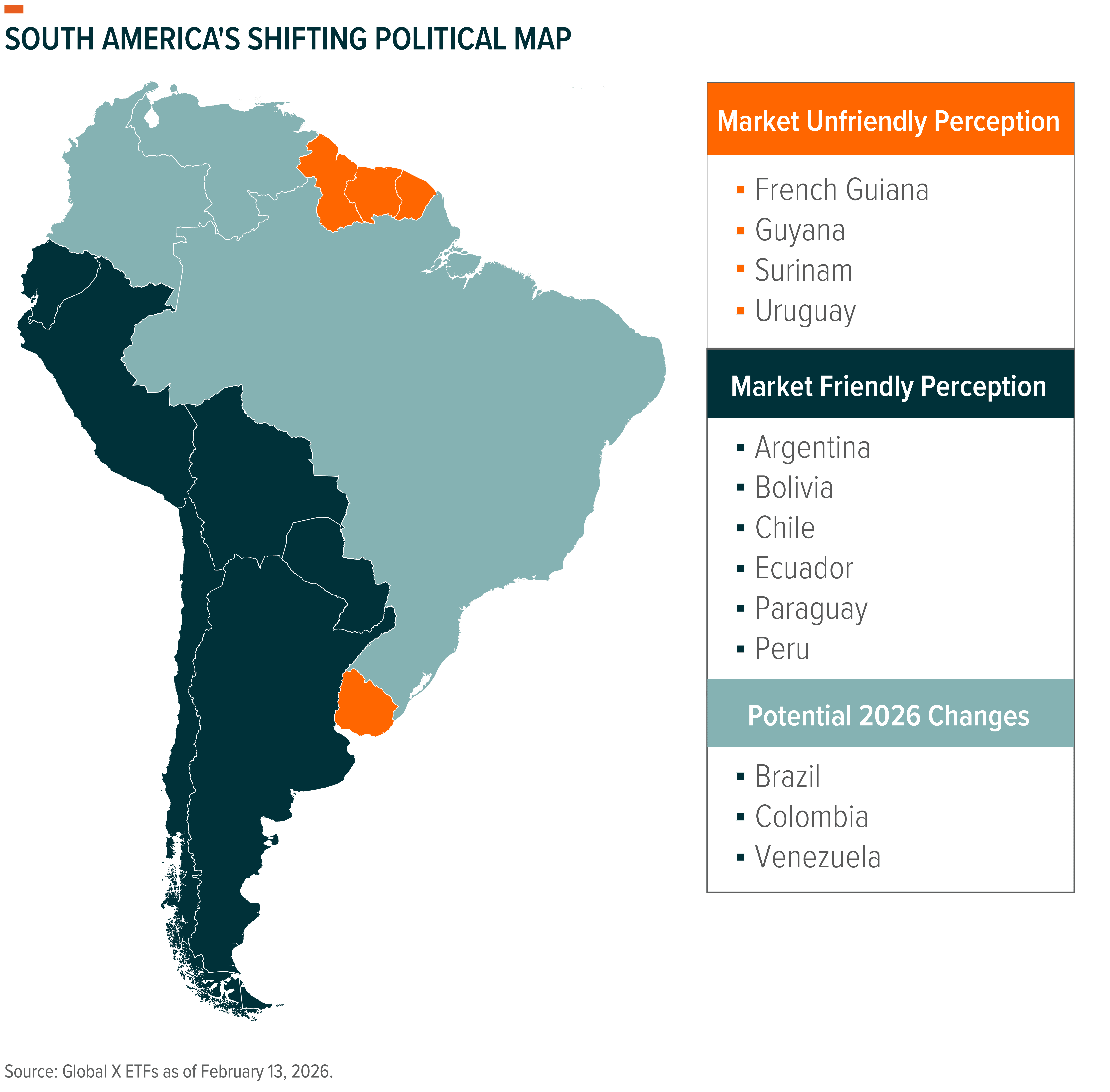

After years of fiscally unorthodox governance, the South American political pendulum has begun to swing towards the center and capital markets are taking notice. Politics are only the beginning, though. Combine potential 180 degree turns in fiscal oversight with single digit price-to-earnings multiples, a weaker U.S. dollar, and a diverse base of commodity exposures, and Latin America looks to be in a “sweet spot” for investment. From an allocator’s perspective, many portfolio managers are looking for ways to balance heavy exposures to U.S. and Asian Technology with cyclical plays on the market. South America checks that box.

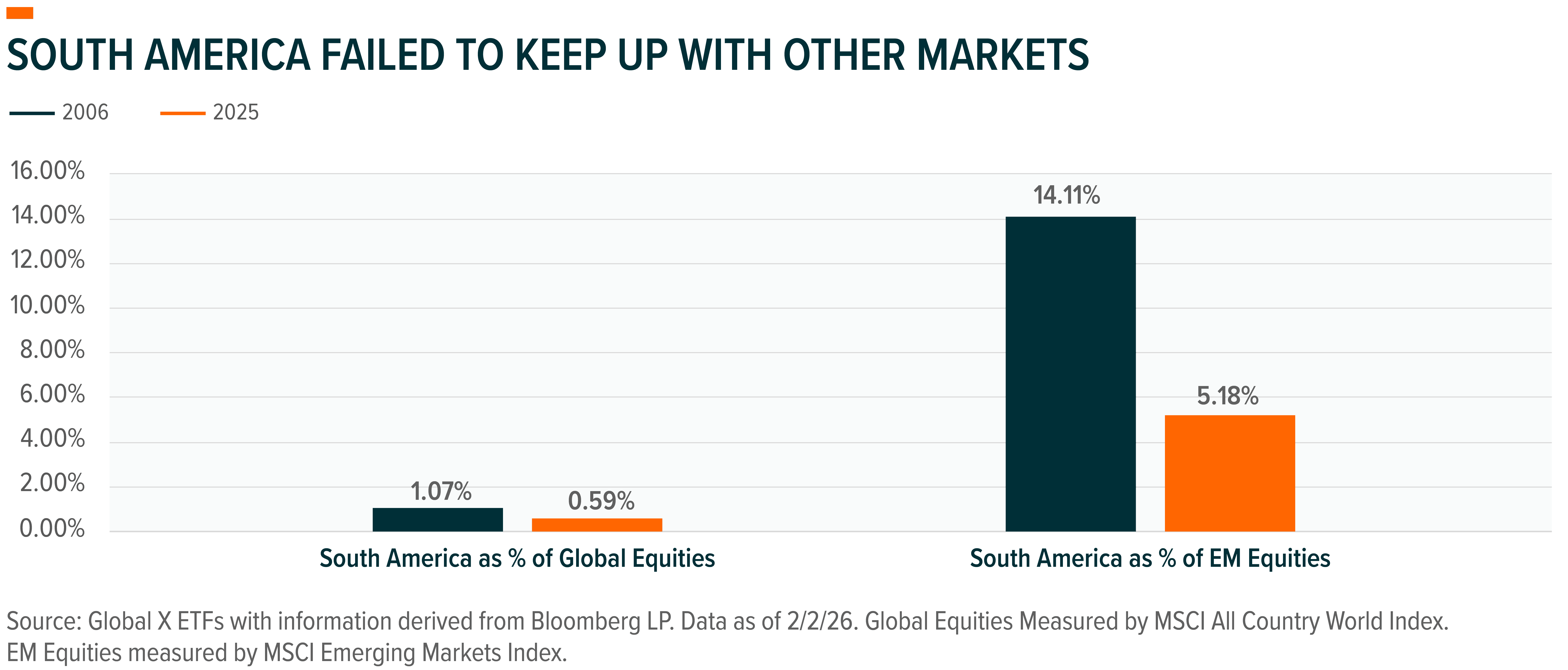

Historically, investors called South America the continent of tomorrow, with its wealth of natural resources and favorable demographics providing a promising backdrop for economic growth. However, “tomorrow” continuously remained a day away, as political mismanagement often got in the way. Politics can have an outsized influence on a company’s prospects, altering factors such as the cost of capital, growth, and currency volatility. These top-down factors can help explain South America’s equity market underperformance over the past two decades, with macro headwinds outweighing the continent’s natural competitive advantages. The political backdrop is now changing. Argentina led the way in late 2023, and we see the possibility for similar political shifts coming in Colombia and Brazil later this year. We believe a more market friendly political environment, coupled with the continent’s commodity exposure and easier monetary policy, position South American equities well in 2026 and beyond.

Key Takeaways

- Politics, commodity exposure, and monetary policy are drawing eyes and capital to South America.

- Argentina has set an example yet still trades at extreme discounts to the rest of EM.

- Colombia and Brazil stand out as two opportunities to follow Argentina’s lead.

Argentina: A Roadmap for Economic Reform

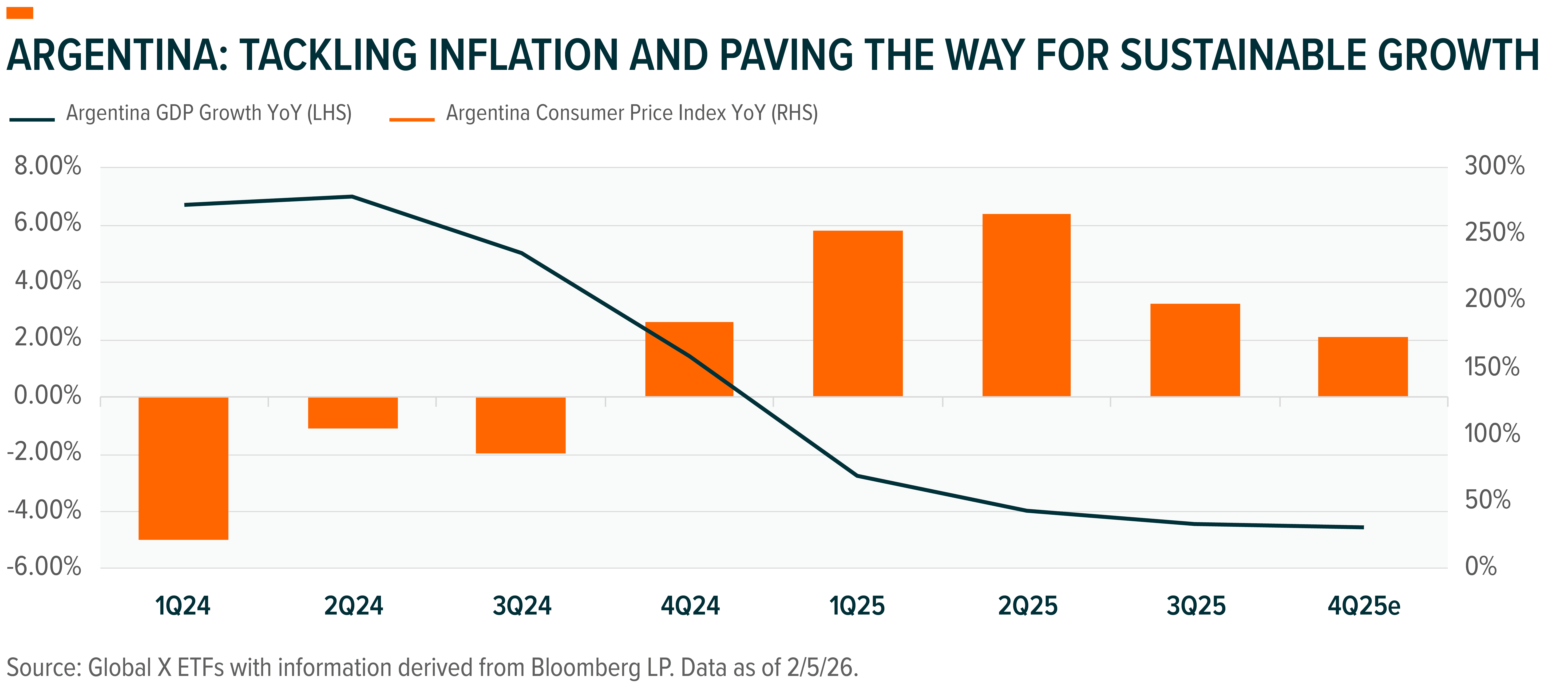

Argentina is in the midst of one of the most dramatic economic turnarounds in market history. Economically unorthodox governments have long plagued the Argentine investment thesis, evidenced by years of stagnating growth, hyperinflation, and five sovereign defaults since 1980. At the turn of the 19th century, Argentina and the United States shared similar GDP per capita. Today that number favors the U.S. by over 600%.1 However, after years of economic stagnation, Argentine voters appeared ready for change, electing market-friendly candidate Javier Milei by a wide margin in 2023. President Milei has executed on his orthodox economic agenda, aggressively cutting spending, loosening currency controls, and improving the ease of doing business. Inflation has fallen from 289% to 31% today, GDP growth has swung from under -2% in 2023 to over +4% in 2025, poverty levels have dropped, and the country appears open for business with the U.S., China, and Europe.2 Milei’s October 2025 decisive midterm victory reinforced investor confidence and expanded his ability to deliver market friendly structural reforms. Equities recently traded at roughly 8x forward earnings, well below regional peers, potentially leaving room for multiple expansion as fundamentals strengthen.3 We see parallels to Brazil in 1995: inflation is cooling, reforms are gaining traction, and markets are awakening after years of dysfunction.

Colombia: The Next Argentina?

Though we believe Argentina is still in early innings, Colombia just started the game. Colombian equities may present a rough parallel to what we’ve been monitoring in Argentina. Valuations remain deeply discounted, reflecting years of policy uncertainty and perceived mismanagement, yet the upcoming May Presidential election could mark a turning point. A market friendly political shift could unlock investment, stabilize fiscal policy, and reignite growth. Early polls signal a wide array of potential outcomes; however, we see a clear path back to a more market friendly government, which we view as key to raising the country’s economic prospects and unlocking growth. Moreover, Colombia stands to benefit indirectly from potential regime change in Venezuela, with improved trade, migration normalization, and regional sentiment offering potential tailwinds.

Brazil: Monetary Policy, Politics, and Commodities

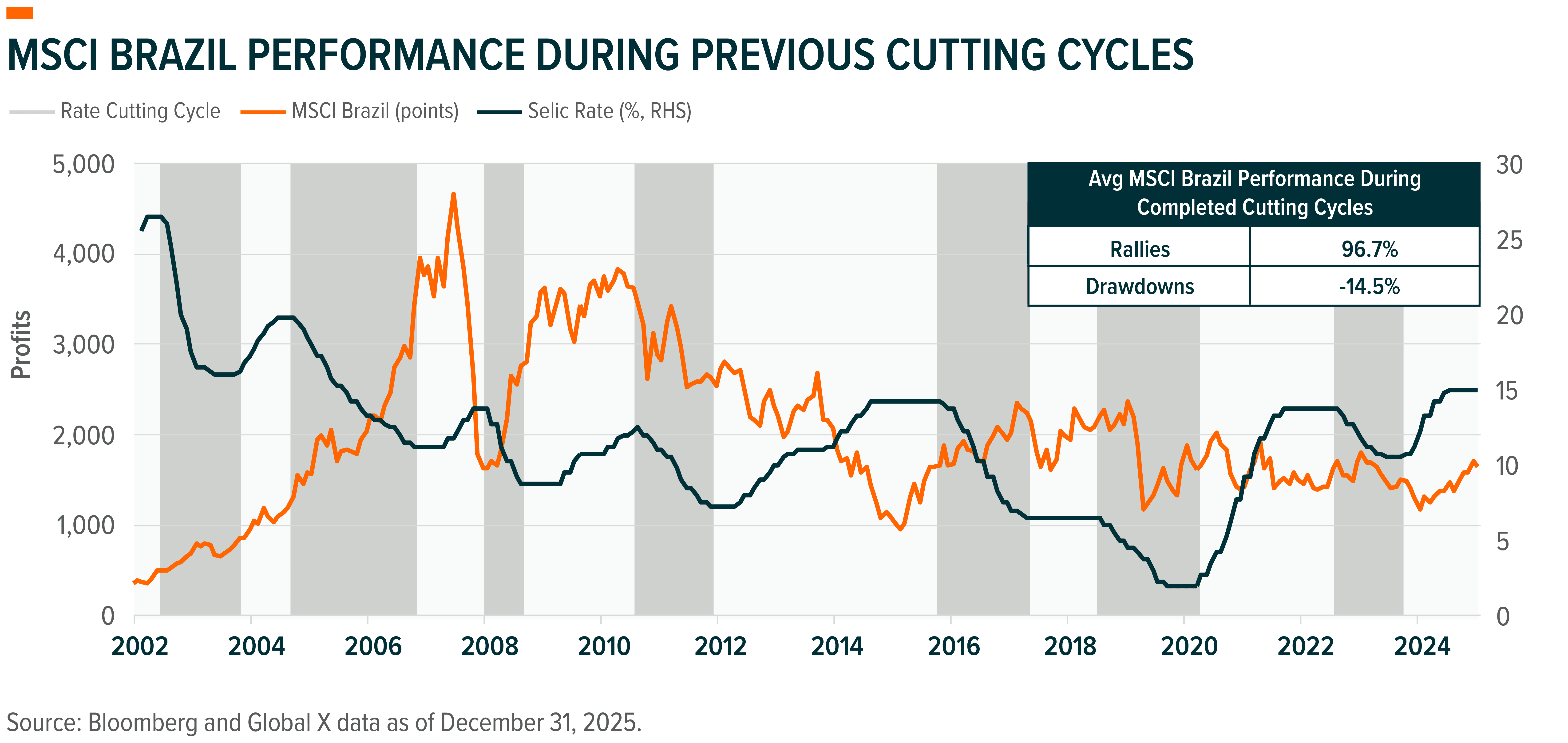

Brazil goes into 2026 with two key performance drivers: interest rates and politics. In terms of monetary policy, Brazil’s key rate began 2026 at 15%. With inflation around 5%, that translates into one of the highest real interest rates in the world, which should support a powerful carry trade and buoy the Brazilian real (BRL).4 We expect rate cuts beginning in the first quarter of 2026, which would likely act as a powerful standalone force for Brazilian equities. The prevalence of floating rate debt in Brazil means lower interest rates should reduce net interest expenses for corporations and lift earnings (before we would expect to see other positive effects in the form of improved asset quality, more loan growth, more capex, and growth!).

Looking at the past seven completed rate cutting cycles in Brazil, the average MSCI Brazil Index (Net) rally stood at roughly +95% (cumulative), where the average drawdown was around -15% (cumulative).5 We like this risk reward set-up. Looking further out, Brazil hosts Presidential elections in October of 2026. The incumbent is expected to run for his fourth term in office and, if elected, would be 81 by the start of his new term. He has recently faced multiple health challenges and a high rejection rate. Noticing a pattern of Senate and Congressional elections moving towards the center-right, we believe that there is a legitimate opportunity for a market friendly, fiscally responsible candidate to step into the presidency.

Andeans: The Die was Kast in December

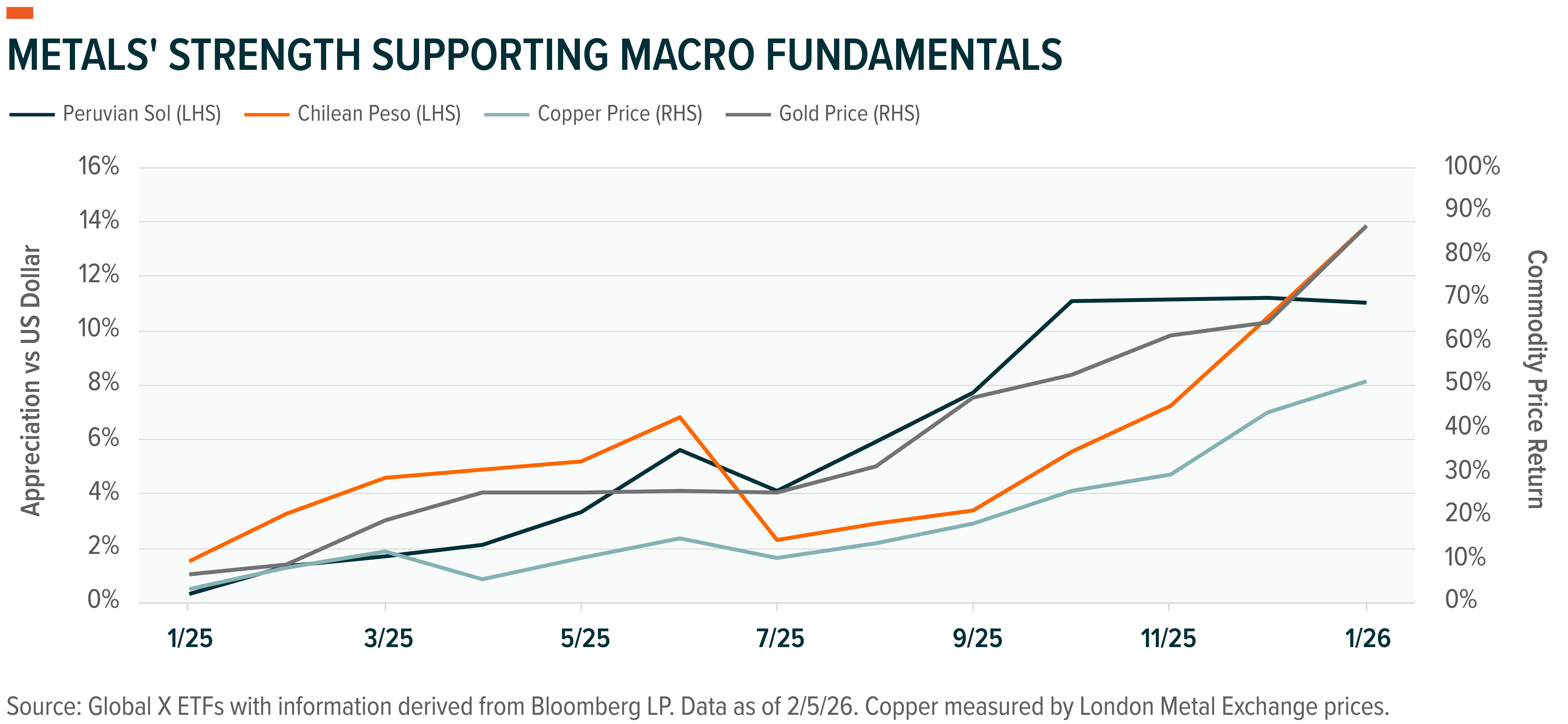

Chile was historically considered South America’s most stable economy, with the strength of its institutions and policy certainty providing the country with a structurally lower cost of capital than peers. However, after years of social unrest and radical constitutional reform proposals, this reputation has been dented, slowing growth and stifling investment in the copper-rich nation. But in December of 2025, Chileans elected Jose Antonio Kast by a wide margin after he campaigned on a platform of deregulation, tax cuts, and security. Looking ahead, we see plenty of room for new policies to be implemented to attract investment, especially considering Chile’s wealth of copper, lithium, and gold resources.

Peru’s economic prospects have been hampered by recurring political instability, with four Presidents over the past decade having been impeached. Despite this, the country’s vast wealth of natural resources, which include copper and gold, and its solid institutions, notably its central bank, have helped cushion the blow, with Peru witnessing some of the highest and most consistent growth in the region. We don’t necessarily forecast any substantial change to occur at the April election, but the creation of a second legislative body of congress could be a game changer, not only adding a second layer of checks and balances but also potentially ensuring increased political stability by raising the threshold for impeachment.

Conclusion: A New Market Friendly Era Could be in the Cards for South America

From Buenos Aires to Brasília, South America’s political pendulum appears to be swinging back toward market-friendly leadership. We expect future economic policy in South America to be better than the past, reducing the cost of capital, increasing investment, and having the potential to drive more sustainable growth ahead. A region-wide shift could create positive spillovers, as countries reinforce one another and power the next cycle for South America.