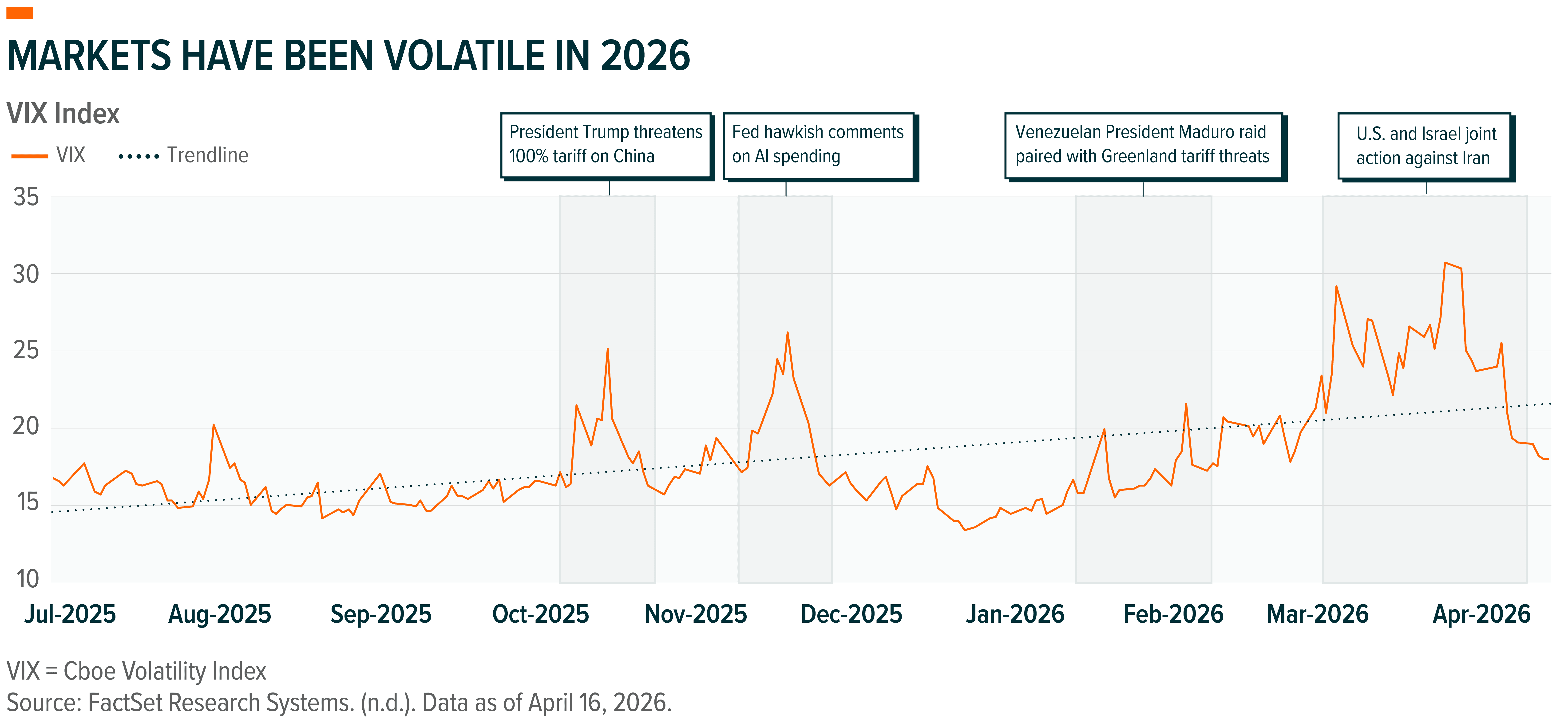

Equity markets have entered a more volatile stretch in 2026, with a growing list of risks for investors to navigate. These include the possibility of a prolonged Iran conflict, higher energy prices feeding back into inflation, a Federal Reserve (Fed) that may stay restrictive for longer, policy uncertainty ahead of the U.S. midterms, and emerging stress in parts of the credit market. That backdrop, combined with a quiet rotation away from mega-cap leadership and toward other areas of the market, is adding another layer of uncertainty.

We do not see this environment as a reason to step away from equities. The fundamental backdrop remains constructive, supported by earnings growth, healthy margins, and ongoing structural tailwinds such as AI. Instead, we think investors may benefit from broadening how they express equity and growth exposure, adding sources of return less reliant on narrow market leadership.

That is where selective thematic exposure can play a role. We believe themes tied to non-discretionary demand, policy support, and strategic relevance can complement existing portfolios and help improve resilience within equities. This piece outlines why some themes may hold up better during periods of volatility and highlights four thematic opportunities we favor for 2026 and beyond.

Key Takeaways

- We believe elevated volatility is reinforcing the case for broadening equity exposure, not stepping away from it.

- Thematic investing is not solely about growth; the right themes can complement existing growth allocations by adding potentially more resilient sources of return within equities.

- Theme selection matters. We favor four themes where demand is durable, visible, and less sensitive to near-term macro swings.

Market Volatility Meets Strong Fundamentals in 2026

2026 has already reminded investors that bull markets do not move in straight lines. Volatility has returned as markets digest a growing list of macro and geopolitical risks, including a prolonged Iran conflict and renewed oil shocks, inflation reaccelerating through energy, a Fed that may be slower to ease rates than investors had hoped, rising political uncertainty ahead of the U.S. midterms, and broader concerns around credit conditions and AI capital expenditure (CapEx).

That said, volatility alone does not imply a deterioration in the underlying equity story. We believe the fundamental backdrop remains solid. The S&P 500® entered 2026 with strong momentum and is expected to grow earnings by over 17% this year, with margins near record highs.1 At forward earnings multiple of ~20x, valuations appear reasonable, especially with structural trends like AI unfolding.2 Higher energy prices could pressure estimates at the margin, but we believe the broader earnings trajectory still points to a healthy corporate backdrop and continued economic growth.

Rather than materially reducing equity exposure, one approach could be to seek more balance within equities themselves. In uncertain markets, investors often look to traditional defensive tools such as cash or short-duration fixed income. While those allocations can help manage risk, they may also limit participation if the earnings backdrop stays constructive.

This is where thematic investing can play an important role. Themes are often thought of as targeted growth exposures and tactical allocation tools, but the right ones can also serve as complementary building blocks within portfolios – providing potentially differentiated sources of return that may be underrepresented in broad indices. Done well, thematic investing provides focused exposure to structural shifts and economic trends whose demand drivers are less dependent on the next quarter’s move in the S&P 500® or Nasdaq-100®.

Where Thematic Resilience Comes From

One reason some themes can hold up better during volatile periods is that their demand drivers are often non-discretionary. Defense procurement is government-mandated and supported by long-duration contracts. Water infrastructure spending is regulated and essential. Healthcare demand is shaped by demographics, not sentiment. Power and electrification are tied to policy and grid constraints. When equity markets broadly reprice risk, those underlying demand curves do not necessarily move with them. That disconnect between market sentiment and underlying demand is what gives some themes resilience.

Second, themes tend to be structurally under-owned relative to where the capital eventually flows. By design, they often sit in sectors that make up a small fraction of major indices. Defense and aerospace, for example, represent less than 2.5% of the S&P 500® – and similar underweights exist across energy, water, cybersecurity, and other themes.3 When volatility triggers a rotation out of crowded positions, under-owned themes with real fundamentals may become destinations for institutional capital.

Third, some themes are supported by unusually strong earnings visibility. In many cases, the market is no longer underwriting these themes on distant optionality alone. The path from innovation to monetization has shortened, and demand is increasingly visible in revenue, backlog, CapEx plans, and earnings revisions. In AI-linked infrastructure, for example, demand is often already visible in CapEx plans, capacity commitments, and backlog, before financials reflect it. That matters in volatile markets, when investors become less willing to pay for narratives that sit far out in the future and more willing to own exposures where the fundamental case is already being validated in real time.

In some cases, volatility can also reinforce the theme itself. Geopolitical stress can pull forward defense spending. Energy insecurity can accelerate investment in power infrastructure. Industrial disruption can strengthen the case for domestic capacity and automation. In those instances, volatility is not just a headwind to work through, but it can become part of the demand signal.

That said, themes are not immune to drawdowns. Volatility can still compress multiples, particularly when macro factors such as interest-rate expectations shift and investors reassess terminal values. But unless the macro shock permanently changes the lifecycle of the theme, that repricing can create opportunity rather than invalidate the thesis. That is why theme selection matters as much as thematic conviction.

Demand-Resilient Themes We Like for the Years Ahead

1. Defense Tech & Cybersecurity

Defense has traditionally been viewed as one of the more stable areas of the economy, supported by government budgets, strategic priorities, and long-cycle contracts. That stability now sits against an even more favorable backdrop. As geopolitical tensions rise and military spending growth broadens, global defense expenditures are projected to surpass $4 trillion by 2030, up from an estimated $2.9 trillion in 2025.4 U.S. defense spending alone could top $1.5 trillion in fiscal 2027, years ahead of earlier expectations.5

What we believe makes the Defense Tech theme especially compelling, in addition to the spending growth, is the structural shift underneath it. The economics of modern warfare are changing. Relatively inexpensive offensive systems, such as drones, are increasingly forcing the use of much more expensive defensive interceptors and response systems. That imbalance is accelerating replenishment cycles across missile defense, munitions, drones, and surveillance, creating more durable tailwinds for the sector.

Cybersecurity is an important extension of this dynamic. Though often grouped with higher-growth areas of tech, cyber demand increasingly looks like a non-discretionary layer of modern defense. Governments are stepping up investment, while enterprises have little room to reduce spending in a worsening threat environment. The recurring revenue nature of the business makes that demand especially durable.

Related ETFs:

2. Aging Population

Demand drivers for Aging Population are demographic rather than economic cycles and are tied to non-discretionary healthcare spending, which helps sustain the investment case intact even during periods of market uncertainty. Americans aged 65 and older already account for nearly 18% of the U.S. population, or just over 61 million people, and that cohort continues to expand.6 Globally, population aged 65 and older is expected to expand nearly three times faster than younger cohorts.7

Importantly, this is not just a story of population growth, but of spending intensity. As these cohorts age into more procedure-heavy years, demand shifts toward higher-cost areas such as cardiovascular care, orthopedics, and long-term care. That progression is already visible in the data, with individuals aged 55 and older accounting for 57% of total U.S. healthcare spending in 2023 despite representing only 30% of the population.8

That combination of rising spending intensity and system-level demand is increasingly translating into durable and visible revenue streams across the healthcare ecosystem. Innovation is also expanding the opportunity set, from orthopedic procedures like hip and knee replacements to chronic disease treatments like GLP-1s that are extending patient lifespans and increasing lifetime care needs. At the same time, demand for senior housing and long-term care facilities continues to grow, with occupancy increasing and pricing power improving. Those dynamics give the theme unusually high demand visibility at a time when investors could look to pay more for earnings durability and less for cyclical sensitivity. Valuations also look supportive, with the broader healthcare sector still trading at a discount to the S&P 500® despite improving fundamentals.9

Related ETFs:

3. U.S. Electrification

The Electrification theme stands out because it pairs a traditionally defensive segment of the market – utilities – with what we believe is one of the strongest long-term growth opportunities in U.S. equities: power generation, grid modernization, and transmission buildout.

More importantly, the fundamental backdrop is solid. After two decades of near-flat growth, U.S. electricity demand is forecast to rise by nearly 50% between 2024 and 2040, driven by AI data centers, manufacturing, and electric vehicles.10 According to the U.S. Department of Energy, data centers could consume as much as 17% of U.S. electricity by 2030, up from 4.4% in 2023.11 At the same time, industrial electricity consumption was forecast to grow 2% in 2025 and 3.5% in 2026, reinforcing that this is not a single-source demand story.12

The capital commitment behind this theme also helps make it structurally resilient. U.S. utilities plan to spend $197 billion in 2026 in CapEx, with investments between 2025 and 2030 expected to reach $1.4 trillion – twice what was invested over the prior ten years.13 Nearly half of transmission assets are at least 20 years old.14 Replacement and modernization are operational necessities with regulatory backstops.

Related ETFs:

4. Data Centers & Digital Infrastructure

The Data Center theme, dominated by Real Estate Investment Trusts, represents a core infrastructure layer of the digital economy and, increasingly, AI. Leading operators lease capacity to hyperscalers and large enterprises under long-term contracts that are getting longer, in some cases extending beyond ten years as landlords prioritize large AI-oriented tenants.15 In a volatile market, that revenue visibility with cash-flows backed by contractual obligations, can be a meaningful source of resilience.

At the same time, supply remains exceptionally tight. North America’s vacancy rate is near record lows of under 1.5%, and nearly 90% of new capacity under construction is already pre-committed.16,17

We believe that combination of long-duration contracts, structural undersupply, and AI-driven demand gives the theme unusually strong earnings visibility and pricing support, making it less sensitive to near-term market sentiment.

Related ETFs:

Conclusion: When Volatility Rises, Theme Selection Matters

Choppy markets tend to shift investor focus from concentration toward balance. We think the themes most likely to hold up are the ones backed by non-discretionary demand, policy support, and visible capital cycles. That is why we continue to favor areas like defense, aging, electrification, and digital infrastructure in 2026 and the years ahead.

For investors already positioned in growth-oriented areas of the market, these themes can serve as complementary exposures – helping broaden return drivers and potentially improving resilience without stepping away from equities.