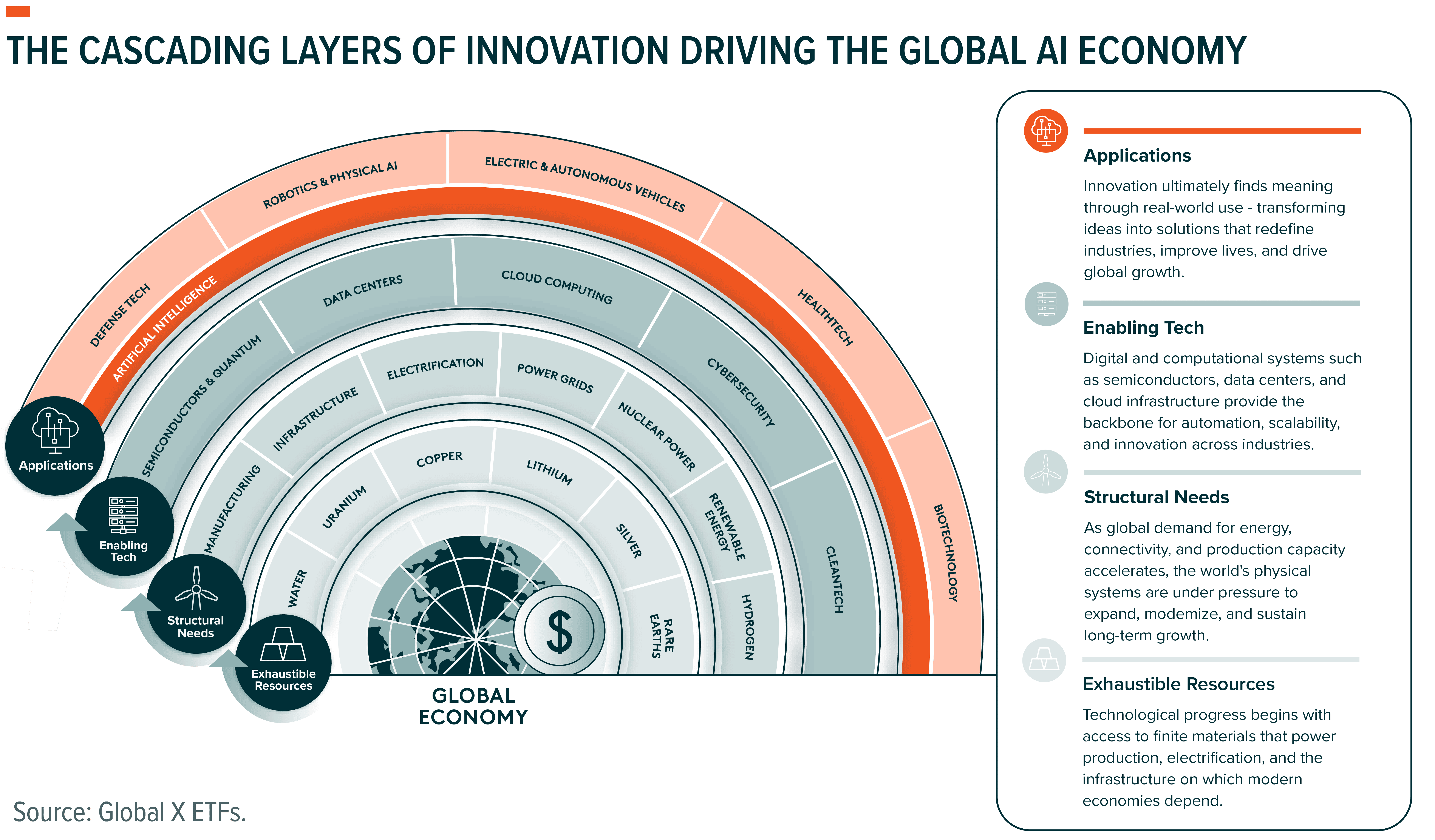

Artificial Intelligence (AI) is rapidly establishing itself as the defining economic layer of the post-internet era. The internet created a $16 trillion digital economy over the past three decades, about 15% of global GDP.1 In our view, AI is the only technology capable of doubling or even tripling that share in the decades ahead. Unlike earlier cycles, AI converts information into decisions and actions, allowing productivity to scale independently of labor. As chatbots amplify knowledge work, AI agents automate end-to-end tasks, and robots begin to complement human labor in physical and repetitive roles, a much larger share of the global economy becomes computable.

Early productivity gains from AI are already emerging but translating them into broad earnings growth and sustained economic output will require massive investment across a deep set of interlocking systems. On the technology side, algorithms, semiconductors, data centers and cloud infrastructure, as well as software are all essential to developing and embedding intelligence into everyday workflows. In parallel, energy, grid infrastructure, materials are essential to build and operate the physical backbone of AI. Understanding how these layers interact is critical for identifying where durable opportunities may emerge.

AI’s growth is also self-reinforcing. More compute drives higher power demand, which requires new infrastructure, enabling larger models and richer applications that push compute needs even further. In this piece, we explore eight themes investors can use to capture the multi-trillion-dollar AI supercycle and highlight the Global X ETFs positioned across this rapidly expanding ecosystem.

Key Takeaways

- AI Becomes a Distinct Economic Layer: As AI permeates industries, it is evolving from a tech trend into an economic system defined by its own enablers and adopters. Exposure across the stack is increasingly critical for investors.

- AI Anchored by Computing Infrastructure: Semiconductors and data centers are emerging as the critical leverage points of the physical backbone of the AI economy.

- AI Requires Vast Infrastructure and Exhaustible Resources: Electrification, nuclear power, and infrastructure development will be foundational to AI’s long-term scalability.

- AI Accelerates New Applications: Cloud computing, robotics, and cybersecurity stand to benefit as AI adoption broadens and applications scale.

The Multi-Trillion-Dollar Intelligence Age Has Just Begun

AI may be one of the most profound technologies ever created for two main reasons. First, AI scales intelligence and decision-making beyond the limits of human labor. Second, AI builds on and spreads through existing digital foundations such as the internet, cloud computing, and smartphones, accelerating its global diffusion.

Together, these two factors can lead to a productivity supercycle that enables economies to take on larger challenges, automate complex work, and unlock new avenues of disruptive growth. Over the next few decades, the companies at the center of this transformation could drive a multi-trillion-dollar expansion in the digital economy that expands global GDP.

For investors, this means opportunities and risks. Below, we outline key themes and allocation frameworks to help them navigate and capitalize on AI’s disruptive force.

1. Artificial Intelligence & Technology: Targeting AI’s Enablers and Adopters

AI is beginning to function like an economic sector of its own. It has a distinct capital expenditure (CapEx) cycle, a dedicated supply chain, and a growing base of revenue-generating use cases. In the next several years, the interaction between capital investment and AI-led monetization will determine how quickly this sector forms and how broadly it scales across the economy.

Fundamentally, the AI sector is led by two complementary groups of companies: enablers and adopters. Enablers develop the technologies that make AI possible – such as algorithms, advanced semiconductors, high-performance computing systems, and cloud-based infrastructure. Adopters integrate AI into existing products and services to improve productivity, enhance capabilities, and create new commercial models. The progress of the AI sector depends on both, as enablers expand capacity and lower costs, while adopters validate real demand.

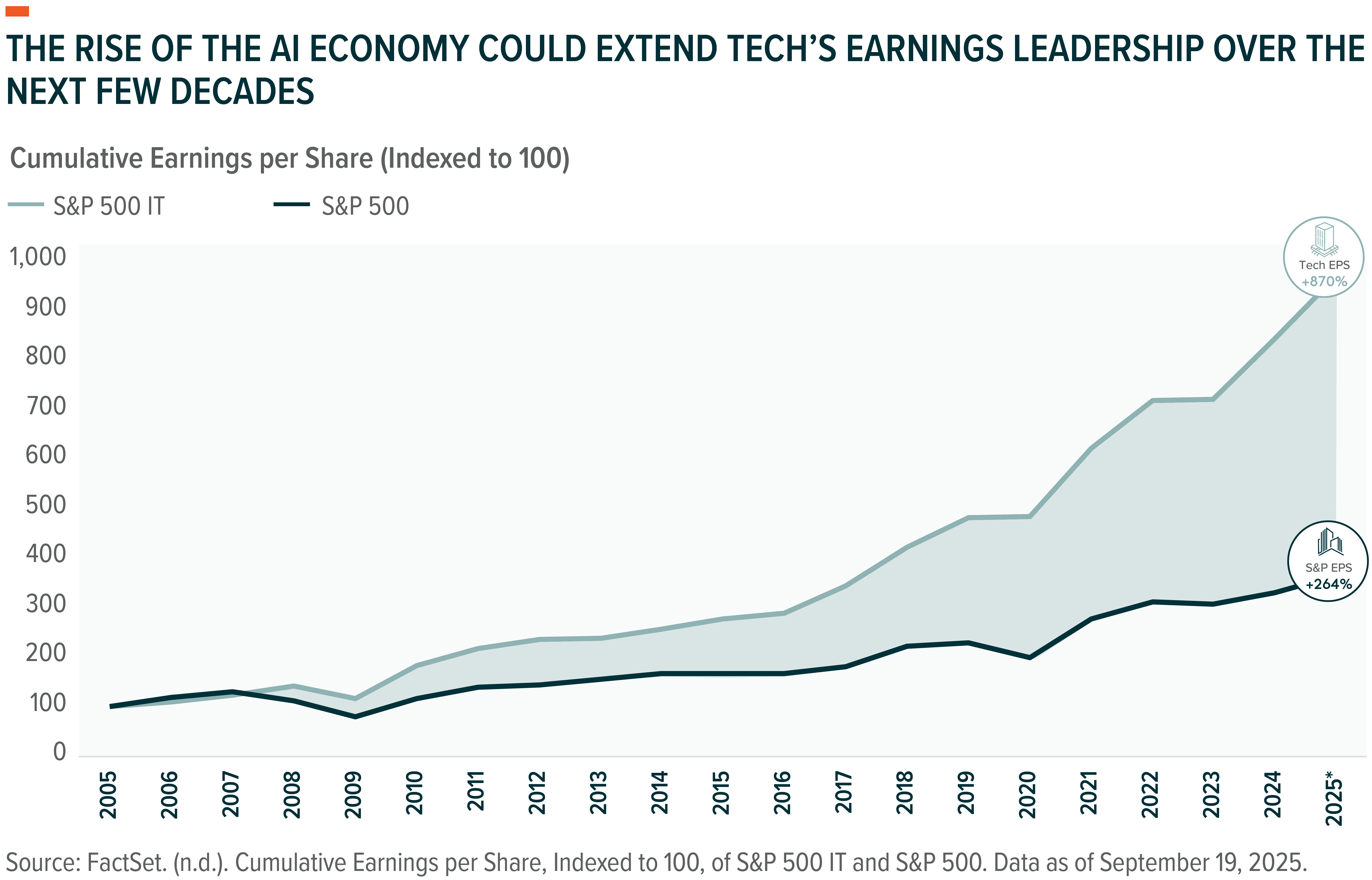

This dynamic is the foundation of the Hyperscaler-led investment cycle, where over $350 billion of AI-linked CapEx is expected this year and as much as $450 billion in 2026.2 These outlays are anchored by multiyear cloud infrastructure backlogs, digital advertising revenue, subscription services, and other businesses that provide evidence of monetization. As these firms reinvest cash flow into AI infrastructure, the cost of delivering AI falls, which further expands adoption and creates monetizable opportunities. This investment and monetization flywheel is likely to keep extending tech earnings, which have compounded four times faster than the broader market over the past two decades.3

Importantly, AI leadership extends beyond just tech companies. Early adopters in financial services, healthcare, communications, industrials, and consumer services are already using AI to enhance core operations. These firms help validate the commercial potential of AI, expanding share while also receiving AI’s productivity lift. Their adoption informs new layers of infrastructure investment by enablers, which in turn supports the next wave of enterprise integration.

For investors, exposure to the AI sector requires exposure to companies that enable AI and the companies that adopt and commercialize it. The Global X Artificial Intelligence and Technology ETF (AIQ) seeks to provide access to this full value chain. The fund seeks to target companies involved in AI algorithms and software platforms, AI as a service, and the hardware that enables AI deployment. It also includes companies that are integrating AI into their own products and services.

Notably, the approach is sector agnostic and aims to capture both established leaders and emerging innovators that may benefit from AI, both within and outside of technology. AIQ also seeks to cap individual holdings at 3%, limiting concentration at the top while overweighting the long tail of AI. In our view, this breadth is important because AI disruption will not follow a linear path, and competitive positions can shift as new models emerge, cost curves decline, and monetization patterns strengthen.

With a diversified and global thematic approach that spans enablers and adopters, AIQ can potentially position investors for the earnings expansion that typically defines the early years of a new technology-led paradigm shift.

2. AI Semiconductors: Leaning into the Picks and Shovels

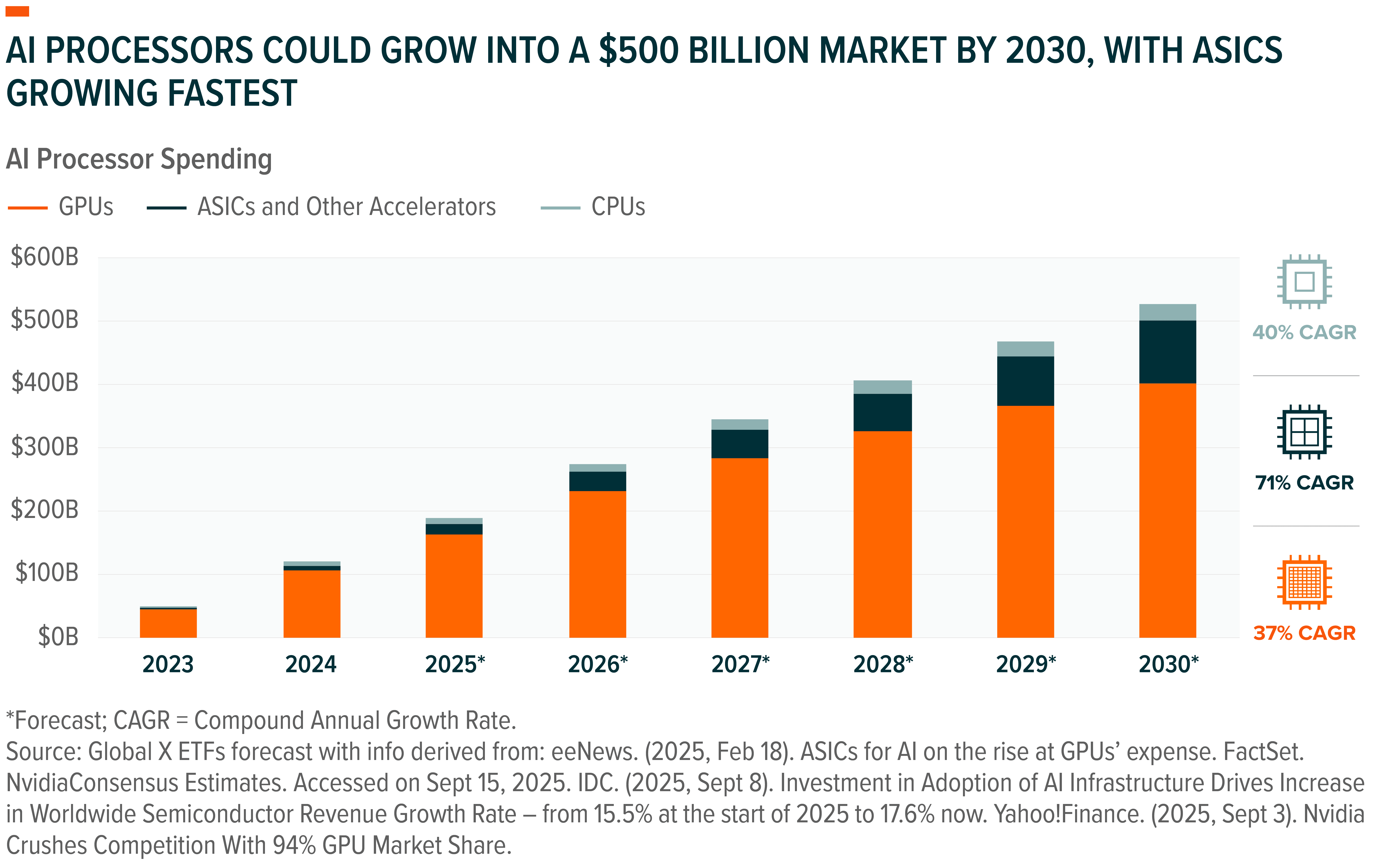

AI’s foundation rests on advanced semiconductors built for high-intensity compute. From training large models to running inference at scale, semiconductor innovation remains the backbone of the AI economy and the center of what is shaping up to be one of the largest capital investment cycles in history.

In 2025, nearly $200 billion could be spent on AI processors, more than twenty times the 2020 level.4 That market could exceed $500 billion by 2030, expanding far faster than the broader semiconductor sector.5 A second force reshaping the landscape is the surge in inference-driven workloads, which is accelerating the need for chips optimized for efficiency Beyond processors, hardware such as high-bandwidth memory, high-speed interconnects, and advanced cooling systems are also essential to sustain AI workloads. Total AI infrastructure spending could exceed $5 trillion by 2030, with AI semiconductors potentially capturing nearly 60% of that outlay.6

Demand for AI semiconductors is also moving beyond the data center. Robots, autonomous vehicles, drones, and next-generation consumer devices are beginning to widen the addressable market for AI semiconductors. As demand from these diverse end markets matures, the global semiconductor industry is likely to split into two halves – a high-performance tier tied to next-generation compute and a volume tier increasingly defined by commoditization.

For investors, this transformation presents an opportunity to lean into the hardware innovation underpinning AI. The Global X AI Semiconductor & Quantum ETF (CHPX) seeks to target the companies enabling this next-generation compute layer. The fund focuses on companies deriving at least fifty percent of their revenue from advanced AI processors, high-performance memory, interconnect technologies, and emerging quantum hardware – segments most directly exposed to AI and compute acceleration.

In our view, this revenue-led purity threshold and thematic first approach stand apart from traditional semiconductor strategies, which often dilute exposure by overweighting cyclical or commoditized segments CHPX seeks to provide focused access to the companies supplying the compute backbone of AI’s long-term expansion, a landscape that will continue to evolve as new challenges in AI computing drive further waves of innovation.

3. Data Centers & Digital Infrastructure: Enabling AI’s Physical Backbone

Data centers are emerging to become the toll booths of the AI economy. As AI applications scale, demand for compute, storage, and connectivity is likely to continue to grow, positioning data centers as the the core hubs for AI computing and data storage.

Today, most compute is still consumed by AI training. That balance could likely shift quickly toward inference, the real-time execution of models at scale. By 2030, inference could represent roughly 80% of total compute demand, up from about 20% today.7 This shift will reshape how capacity is built and managed, with a greater emphasis on efficiency and on distributing compute closer to end users to tackle latency. At this stage of the cycle, independent data centers operators are well placed to help the broader economy scale AI.

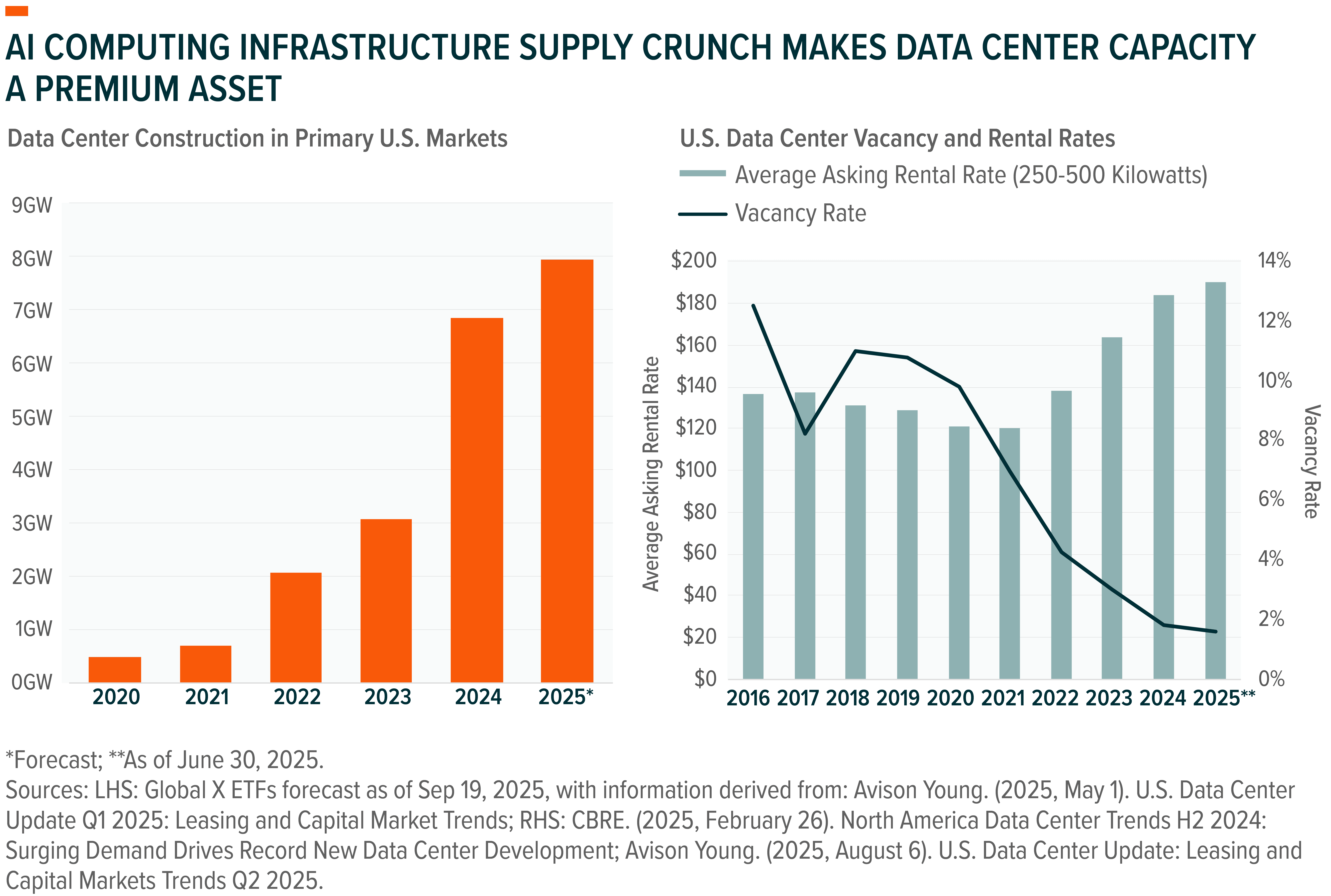

These trends are already reshaping data center economics. Across major U.S. markets, capacity remains tight, vacancy rates are at or near record lows, and access to power has become a gating factor for new development.8 As a result, data center REITs are experiencing some of the strongest rental environments in their history, with long-term leases renewing at higher rates and new builds often pre-leased before construction begins.9 Operators with established footprints, secured power contracts, and scalable land banks are in a position to command premium pricing and sustain growth as demand continues to outpace supply.

A parallel force reshaping data center economics is the surge in data generation driven by AI. Each AI query generates new information that must be stored, retrieved, and processed, and these demands multiply as models become more complex. The shift will accelerate further as autonomous AI agents interact with one another, producing far larger data volumes to complete tasks. This dynamic increases the burden on storage and memory systems across the stack.

The Global X Data Center & Digital Infrastructure ETF (DTCR) seeks to target companies positioned to benefit from rising demand for data processing, storage, and network connectivity as AI adoption accelerates. The fund focuses on the full digital infrastructure value chain, including data center and cell tower operators that build, own, and manage the physical and cloud assets enabling global data transmission and compute.

DTCR focuses on pure-play operators and takes a geographically agnostic approach. By emphasizing the infrastructure layer of the AI ecosystem, the fund seeks to provide exposure to the multi-year buildout of digital capacity required to support AI’s rapid growth.

AI Requires Energy and Enabling Infrastructure

AI has tech colliding with the real world, requiring rapid growth of exhaustible resources needed to keep AI functioning. From an investment standpoint, we believe this creates lasting opportunities for the Electrification and Infrastructure Development themes.

4. Electrification: Powering AI

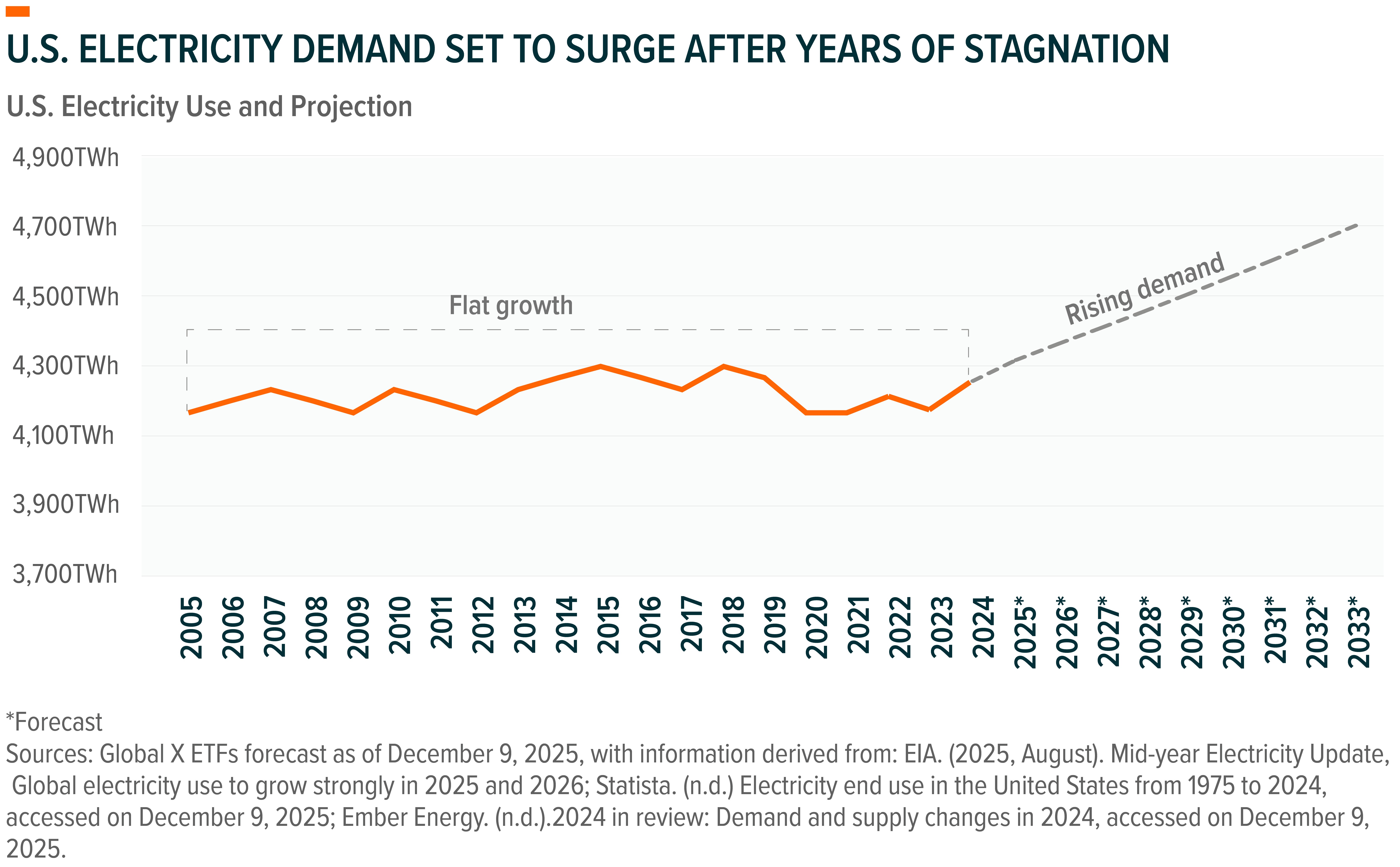

AI needs electricity, and a lot of it. Training foundational model like OpenAI’s GPT-4 required roughly 50 gigawatt hours (GWh) of electricity, the equivalent of powering 6,000 U.S. homes for an entire year and about fifty times more than it took to train GPT-3.10 As AI adoption accelerates, U.S. data centers could consume up to 12% of the nation’s total electricity by 2030, up from about 4% today.11

Even rapid efficiency gains won’t come close to offsetting the surge in electricity demand. Chips are getting better and algorithms more optimized, but these improvements are dwarfed by the scale of new compute requirements. The real drivers of demand are expanding AI workloads, increasingly data-rich models, and the emergence of giga-scale data center facilities to be built around millions of accelerators with power requirements that can reach as much as 5GW per site.12 As these deployments scale, the industry’s aggregate power needs rise far faster than efficiency can reduce them.

The state of the power grid is another hurdle. Largely built in the 80s and the 90s, the grid is due for an upgrade. Interconnection queues stretching multiple years, limited transmission capacity, and an aging network built for a pre-AI world all constrain how quickly new load can come online.13 At the same time, AI data centers require uninterrupted 24/7 power, placing unprecedented pressure on utilities and generation resources. These constraints have major implications for grid infrastructure, utilities, and energy production mix. Natural gas and renewables will play roles in meeting base and peak demand, while nuclear energy stands out as a stable, long-term, zero-emission source for continuous high-load AI operations. Policymakers are already revisiting advanced nuclear technologies, small modular reactors, and uranium supply chains to prepare for this demand curve.

The Global X U.S. Electrification ETF (ZAP) seeks to capture the companies positioned at the center of this emerging energy cycle. The fund focuses on pure-play conventional and alternative U.S. power producers as well as smart-grid infrastructure operators deriving at least half of their revenues domestically. These companies are integral to expanding generation capacity, modernizing grid systems, and enabling the reliable high-voltage networks required for AI’s growth.

As AI pushes electricity demand into a multi-decade upward trajectory, the electrification value chain may become one of the most important – and underestimated – enablers of the AI economy. ZAP provides a way to target this foundational layer as power availability becomes a defining competitive advantage for the digital era.

5. Infrastructure Development: Building AI’s Foundation

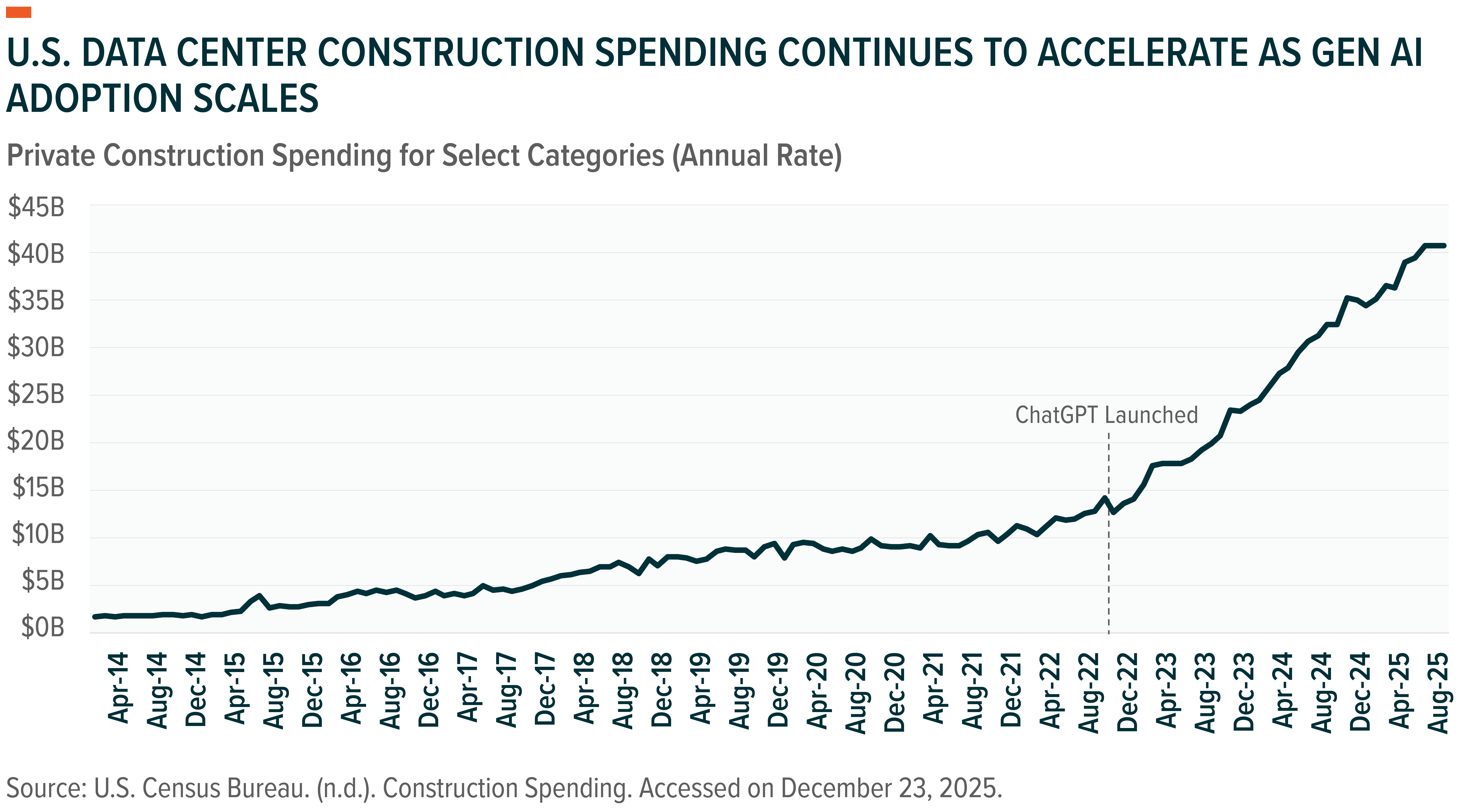

AI’s infrastructure demands are triggering one of the largest physical buildouts in decades. Power plants, grid infrastructure, semiconductor factories, and data centers all require extensive, long-lead construction, and the scale of these projects is accelerating as AI moves from experimentation to industrial deployment.

The opportunity is especially pronounced in the United States. In 2025 alone, a handful of U.S. tech leaders could spend nearly $350 billion on AI data center expansions.14 Some of that spend is moving offshore, but a meaningful share is being directed into domestic tech corridors like Arizona, Texas, and Virginia. Roughly 20% of a data center’s cost is tied to construction, which aligns with the $40 billion annualized run rate now flowing into that segment.15 Parallelly, these regions are becoming epicenters of high-voltage grid expansion, substation upgrades, and high-capacity transmission lines built to sustain 24/7 power loads from AI clusters.

This physical buildout extends beyond data centers. Encouraged by national incentives and supply chain realignment, semiconductor producers are reshoring operations to secure critical chip production on U.S. soil. At the same time, utilities could deploy nearly $1 trillion in cumulative CapEx by 2029 to modernize grids and expand generation capacity.16 Together, these investments create a durable tailwind for construction, engineering, and materials companies at the foundation of the AI economy.

The Global X U.S. Infrastructure Development ETF (PAVE) seeks to capture companies central to this buildout – spanning construction and engineering services, raw materials, infrastructure products and equipment, and industrial transportation that derive a majority of their revenues from the United States. As AI drives sustained demand for complex, capital-intensive projects, PAVE provides exposure to the beneficiaries of one of the most significant infrastructure cycles in modern U.S. history.

AI Accelerates the Application Ecosystem

Once the enabling infrastructure is ready, a wave of new applications is likely to drive the third phase of AI’s growth. Limited visibility into what that future looks like is a challenge for investors, but we believe the parts of the economy that are already coming into focus present opportunities.

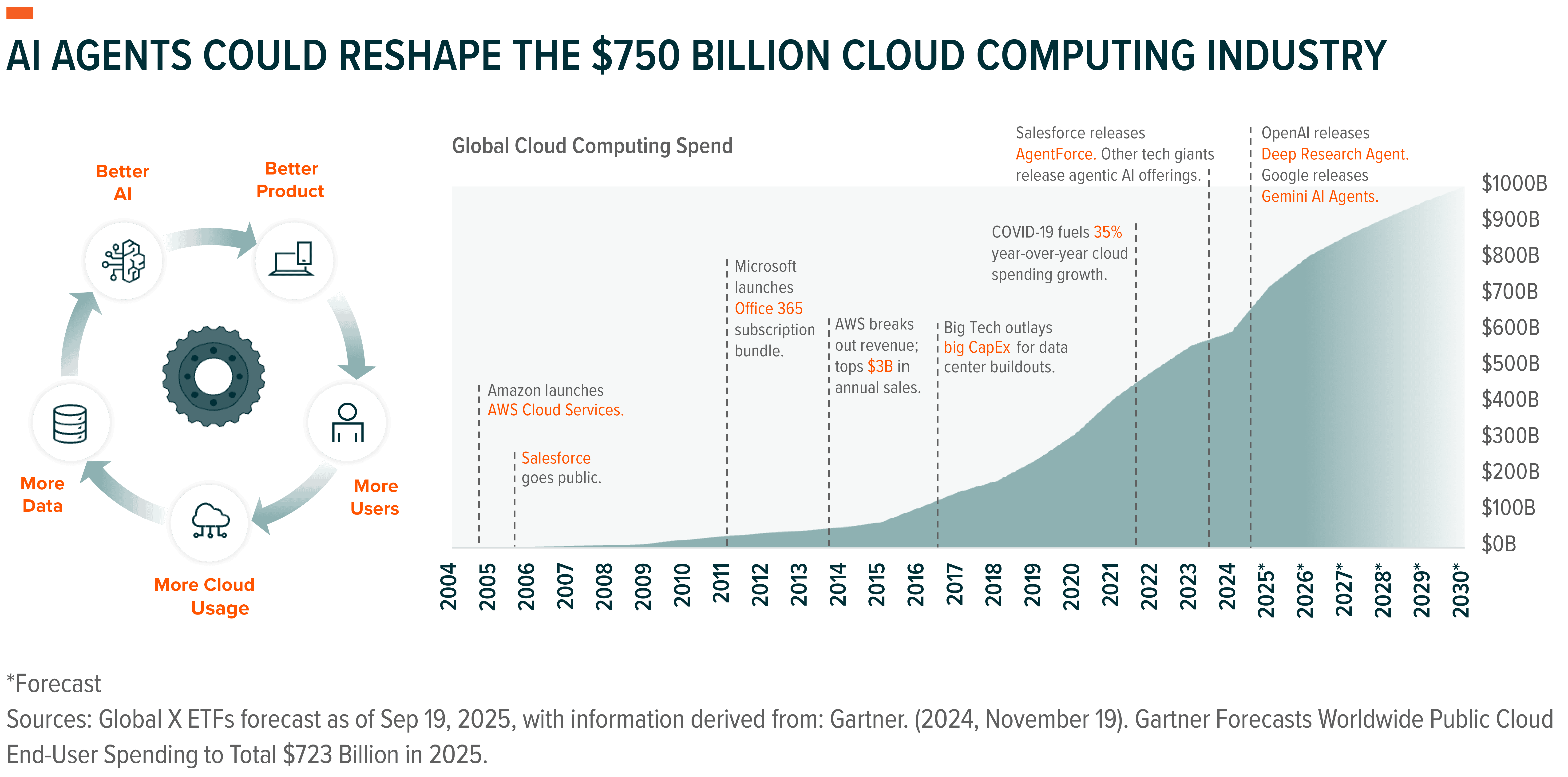

6. Cloud Computing: AI’s Operating System

Cloud infrastructure is becoming the distribution layer for artificial intelligence. Every major model, agent, and application runs on cloud infrastructure. Embedding AI into software requires tight integration with existing IT systems, most of which now run on public and private clouds. As businesses infuse AI across their operations, they depend on cloud providers for the compute, storage, and data management they cannot build in-house. For cloud leaders, this opportunity is already a multi-billion-dollar business.17

Another major opportunity is the extraordinary amount of data AI produces. As agents interact with tools, they are likely to create constant feedback loops and new information streams. This data must be stored, retrieved, and processed, and cloud providers can monetize each step. Cloud operators with global footprints are likely to benefit as “data gravity” pulls more AI workloads closer to where the data lives, further compounding layers of monetization.

Leading software vendors are positioned to capture early AI-driven earnings growth through their established distribution networks and access to privileged enterprise data. Agentic AI models rely on deep integration with systems of record, which strengthens the position of incumbent cloud-native software providers.

New revenue models are already emerging, including subscriptions for AI agents, metered billing for inference actions, and usage-based pricing tied to outcomes rather than compute hours. These dynamics could help expand today’s roughly $700 billion cloud computing market to well over $1 trillion by 2030.18 Additional upside is possible if agentic workloads mature into a mainstream enterprise computing layer through the 2030s.

The Global X Cloud Computing ETF (CLOU) can be a potential tool for investors to capture the opportunity AI creates for the cloud computing ecosystem. The fund seeks to provide exposure to pure-play cloud software providers and hyperscale operators deriving the majority of their revenues from cloud services. As the cloud becomes the operating system of the AI economy, CLOU offers access to the businesses well placed to capture the next decade of AI-driven enterprise growth.

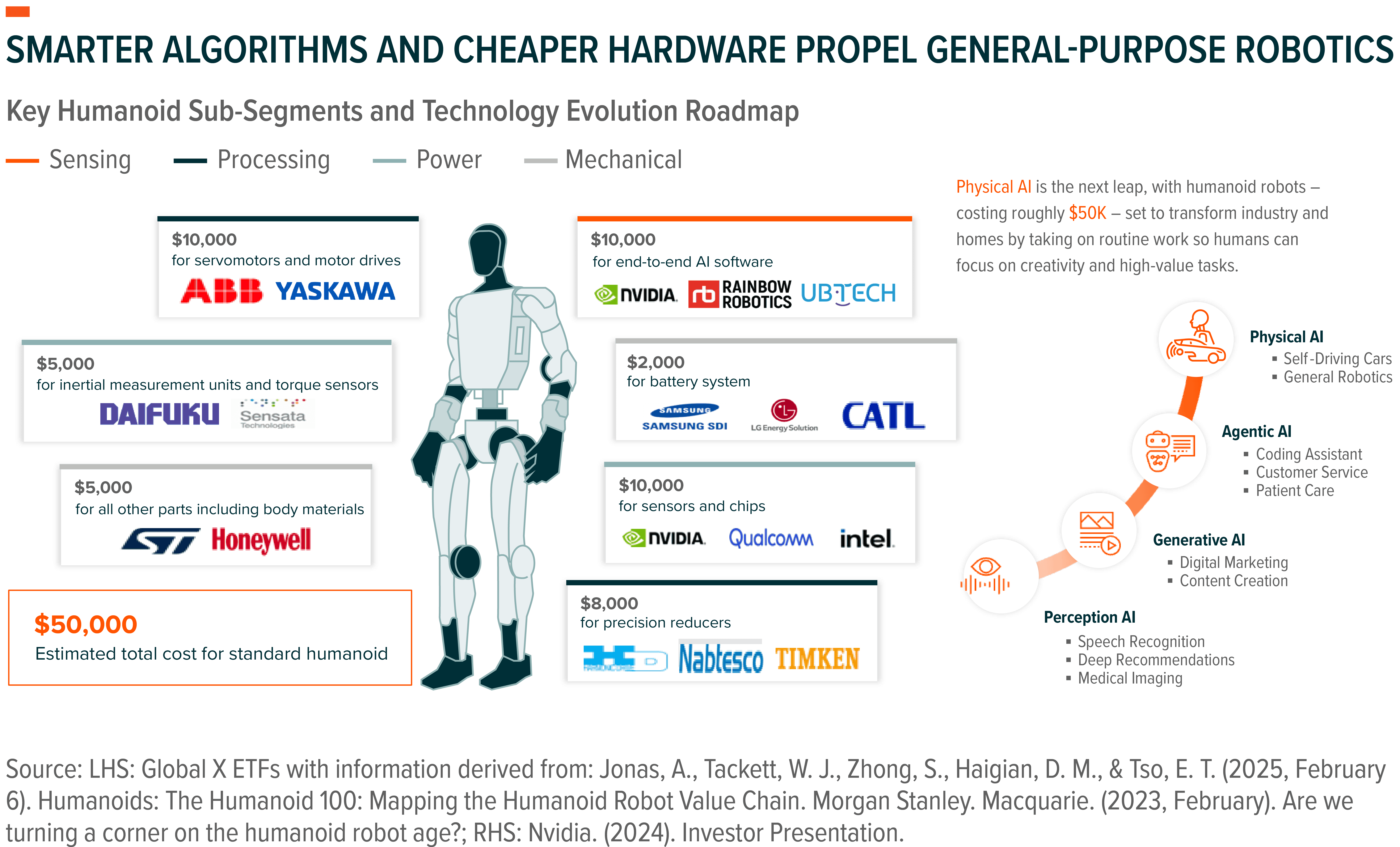

7. Robotics: Bringing AI to the Physical World

AI’s next big frontier is the physical world. Robotics represents AI brought to life through intelligent systems that can sense, decide, and act. For years, robotics innovation was limited because software took time to evolve, but recently, falling compute costs and more efficient AI hardware are expected to push robots beyond controlled environments into broader commercial and consumer applications.

Autonomous vehicles are an early example of this technology gradually advancing towards commercial scale. In the United States, self-driving taxis could surpass tens of millions of rides per week by the end of the decade, up from roughly 250,000 today, powered by robotic systems that process vast streams of sensor data in real time.19 The underlying technologies, such as sensor fusion, local processing, and real-time optimization, are transferrable across sectors.

Industrial robotics remains the largest and most established physical AI segment today with nearly four million systems already deployed worldwide.20 AI upgrades are likely to push these machines beyond repetitive, structured tasks, enabling them to navigate variability, accelerating factory automation and strategic reshoring. Similarly, services robotics is also set to expand meaningfully as AI improves perception, precision, and adaptability. In healthcare, robotic-assisted surgery is scaling as models enhance training and real-time decision support. Logistics networks are deploying fleets of drones and delivery robots to strengthen last-mile efficiency. In defense, physical AI is improving resilience across surveillance and support functions while reducing exposure for human troops.

The Global X Robotics & Artificial Intelligence ETF (BOTZ) provides exposure to companies driving this physical AI transformation, including providers of industrial robotics, non-industrial robotics such as those in healthcare, drones and unmanned aerial vehicles (UAVs), and AI systems advancing physical robotics. The fund applies a high-purity screen, requiring constituents to derive at least 50% of their revenues from these subsegments to qualify for inclusion.

As the AI narrative broadens beyond a handful of large tech names, the fund could potentially be attractive to investors seeking exposure to AI’s impact outside traditional tech, given its focus on leaders in robotics and industrial automation, areas that are generally under-represented within the technology sector.

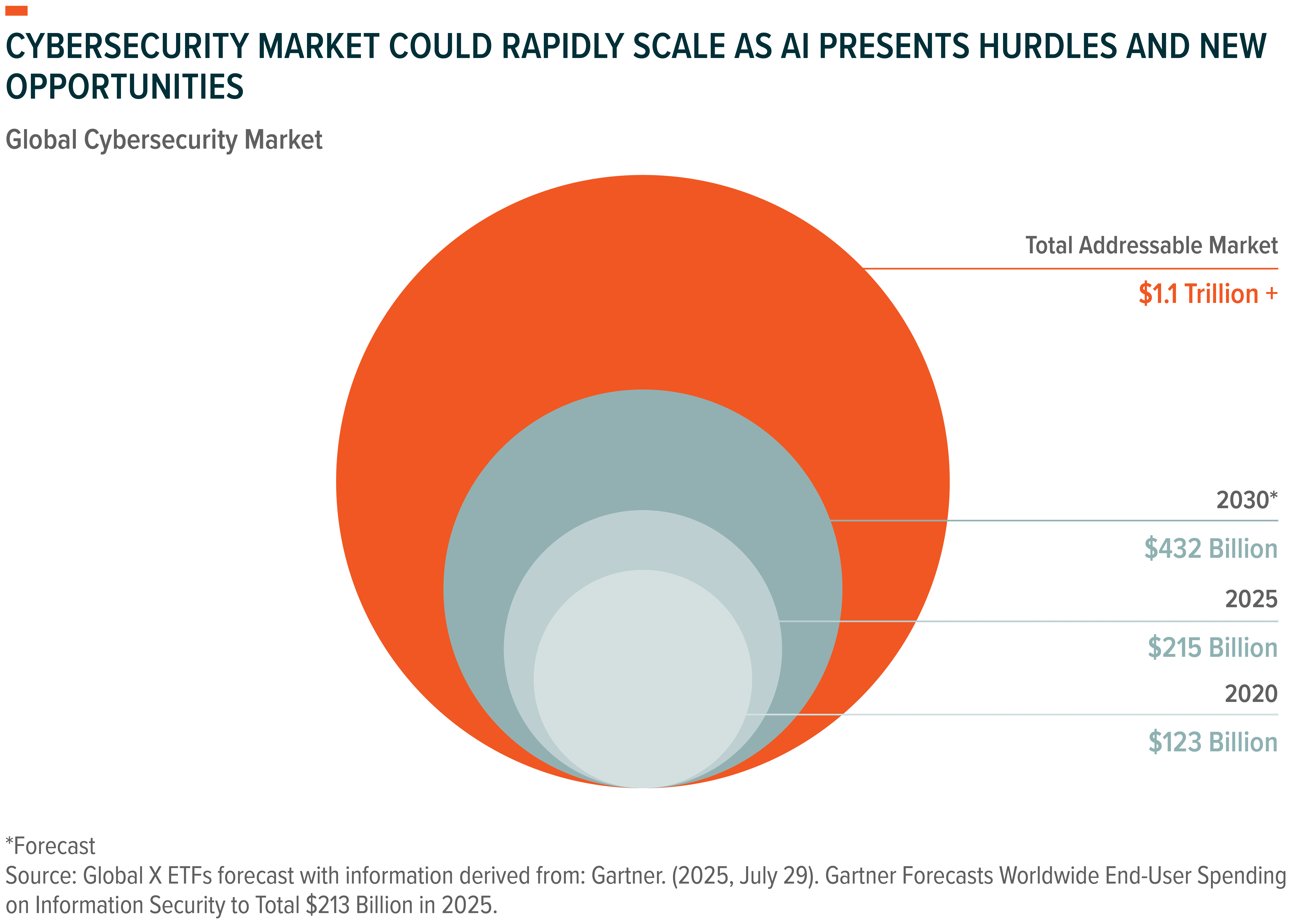

8. Cybersecurity: Securing the Intelligence Economy

As AI expands into critical infrastructure, factories, and cloud networks, cybersecurity becomes both more urgent and more complex. Each new intelligent system introduces additional data flows, endpoints, and attack surfaces. AI agents that can access enterprise systems amplify risks if left unsecured. Without robust security, the very tools designed to improve efficiency can become high-leverage vulnerabilities.

Leading cybersecurity firms are embedding AI directly into their detection and response workflows, creating autonomous security platforms capable of identifying and mitigating threats at machine speed.21 This shift positions cybersecurity as a foundational pillar of the AI economy, not a secondary layer. Combined with a worsening global threat environment, where attacks have risen nearly 49% year-over-year per organization, the result is powerful tailwinds for the sector.22 By 2030, cybersecurity spending could approach $432 billion annually, with an addressable market likely far larger as AI expands the attack surface.23

The Global X Cybersecurity ETF (BUG) provides exposure to companies building the next generation of security infrastructure including cloud security solutions, identity and access management platforms, network security systems, endpoint protection, and a range of other security infrastructure for traditional IT as well as AI applications. As AI expands across digital and physical domains, cybersecurity stands as a durable growth pillar – ensuring the intelligence economy can operate safely, reliably, and at scale.

Conclusion: AI-Led Transformation of the Economy Is a Mega Theme

Like electricity or the internet, AI is a general-purpose technology with the potential to reshape how the economy functions. From semiconductors and data centers to cloud, robotics, and cybersecurity, each layer of the stack contributes to a self-reinforcing cycle of innovation and productivity, which automates cognitive tasks and creates new markets like code generation or autonomous systems. As AI becomes the new utility of the digital age, we believe it is critical for investors to see it as an investable ecosystem and position across its interconnected opportunities.

Related ETFs

AIQ – Global X Artificial Intelligence & Technology ETF

CHPX – Global X AI Semiconductor & Quantum ETF

DTCR – Global X Data Center & Digital Infrastructure ETF

ZAP – Global X U.S. Electrification ETF

PAVE – Global X U.S. Infrastructure Development ETF

CLOU – Global X Cloud Computing ETF

BOTZ – Global X Robotics & Artificial Intelligence ETF

BUG – Global X Cybersecurity ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.