Energy has always been the foundation of modern civilization, but rarely has it mattered more than it does today. In 2025, the world consumed over 636 exajoules of energy, a figure that has grown by more than 60% since 2000, and one that could climb another 15% through 2035.1,2 Electricity, the fastest-growing component of that demand, is at the center of an accelerating collision: the rise of artificial intelligence, the electrification of power grids, and the reordering of global trade are placing unprecedented demands on supply chains already strained by geopolitical fragmentation and strategic vulnerabilities.

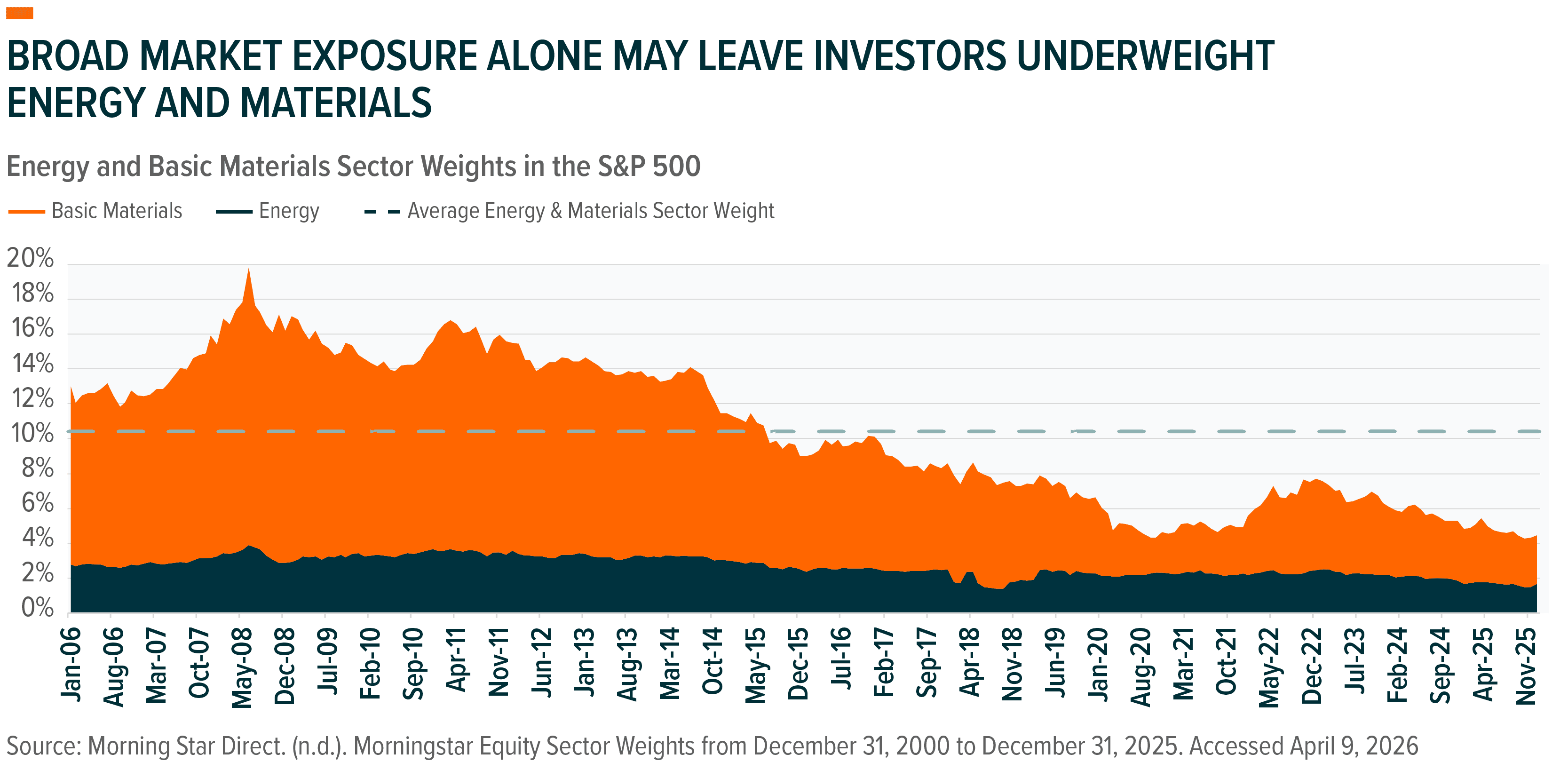

Despite its foundational importance, the combined weight of the energy and materials sectors today represents less than 5% of the S&P 500 index, which is a stock market index that tracks the performance of 500 of the largest publicly traded companies in the United States. This is roughly half their historic average and less than a quarter of their peak allocation in 2008.3 We believe this weighting undersells their significant importance to the global economy and runs the risk of underinvestment across energy infrastructure and material supply chains. The consequences of such trends can span decades, as new mines can take over 15 years to develop, while insufficient investment in energy infrastructure can undermine energy security.4 A course correction appears underway, and we believe it will require sustained public and private investment across the full energy supply chain.

The supply shocks of the 2020s, Russia's invasion of Ukraine, the COVID-19 pandemic, and Iran's 2026 closure of the Strait of Hormuz exposed the fragility of energy systems built for efficiency rather than resilience. Countries dependent on a narrow set of energy suppliers or fuels proved most vulnerable when supply chains were disrupted. The reverberations of those events continue to reshape how nations think about energy, prompting a fundamental shift in capital allocation that prioritized security of supply, diversity of fuel sources, and the resilience of critical infrastructure. We believe that shift is structural, not cyclical, and that it will be a defining driver of energy investment for decades to come.

Opportunities across electrification, energy infrastructure, alternative power, and critical materials are converging into what we believe is a multi-decade supercycle. At the same time, geopolitical risks, energy security, and resource nationalism are emerging to the forefront as matters of national security. Against this backdrop, we believe the case for investment across the entire energy supply chain is no longer optional, but imperative. In this piece, we explore the four categories that investors can use to capture the global supercycle and highlight the Global X ETFs positioned across each segment.

Key Takeaways

- Electrification: Surging demand for electricity, driven by artificial intelligence (AI), electric vehicles (EVs), and industrial growth, is creating investment opportunities across U.S. utilities, grid infrastructure, and the power system supporting them.

- Energy Infrastructure: North America has emerged as the world's most reliable energy supplier, underpinned by abundant reserves, integrated pipeline networks, and rapidly growing liquefied natural gas (LNG) export capacity. We see compelling opportunities across midstream infrastructure and natural gas firms positioned to meet sustained global demand.

- Alternative Power: Nuclear, solar, wind, and hydrogen represent a broad and growing range of power sources that can add meaningful capacity to the global electricity system. The scale of demand ahead means the buildout of alternative power infrastructure presents compelling opportunities across the energy mix.

- Critical Materials: Every pathway to meeting the world's growing electricity needs depends on the same physical inputs. Lithium, copper, and rare earth elements are among the most indispensable, underpinning everything from EV batteries and grid-scale storage to transmission infrastructure and clean energy equipment.

Electrification: The Foundation of the Modern Energy System

Demand for electricity grew much faster than overall energy consumption in 2025, as the proliferation of AI data centers, EVs, and expanding industrial activity pushed power consumption to higher levels.5 By 2040, the world could require an additional 12,200 terawatt hours (TWh) of electricity, which is nearly equivalent to the current annual power consumption of the United States and China combined.6

Nearly $15 trillion in investment could be required for power generation and grid infrastructure through 2035 to meet the growing demand.7 The scale of the grid infrastructure buildout is likely to include a diverse range of power sources, with renewables, fossil fuels, nuclear, and energy storage all expected to play a meaningful role in meeting the world's growing electricity needs.

U.S. Electrification: Powering the Next Era of American Growth

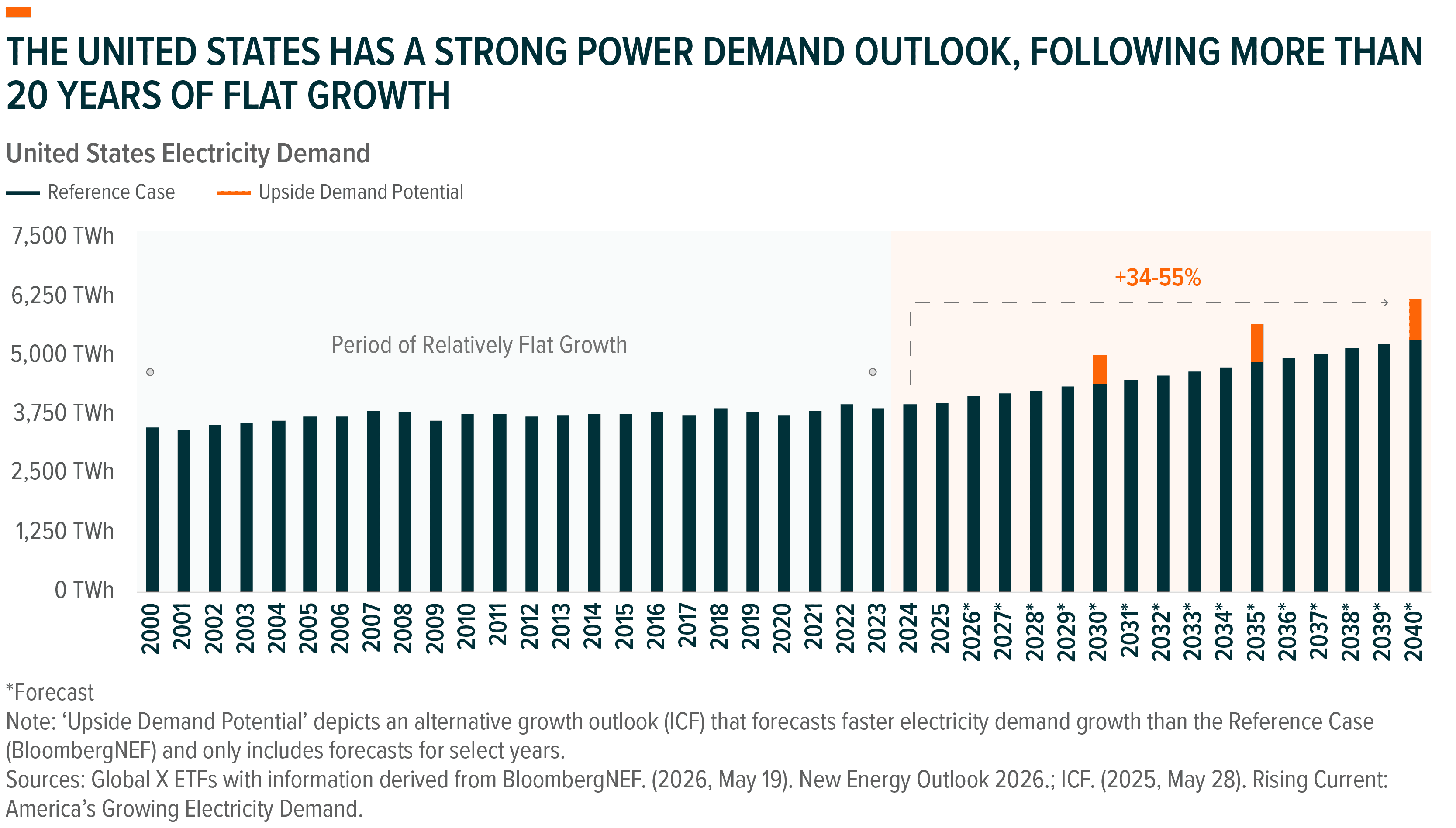

After two decades of near-flat growth, U.S. electricity demand is forecast to increase by as much as 50% between 2024 and 2040, driven by AI data centers, manufacturing, and electric vehicles.8,9 Data centers alone could account for 9% to 17% of U.S. electricity consumption by 2030, which would be an increase from just 4-5% in 2025.10 Compounding the challenge, much of the country’s power grid was built decades ago, with 70% of transmission lines and large transformers at least 25 years old.11 This means that utilities must simultaneously expand capacity to meet surging demand and replace infrastructure that was built in a different era of power consumption.

The electric utilities responsible for keeping up with rising demand are already responding at scale. Dominion Energy, the power utility serving Virginia's data center corridor – the densest concentration of data centers in the world – has committed $65 billion through 2030 to expand its transmission infrastructure, add new power generation, and build out energy storage capacity.12 Southern Company, which provides power to much of the southern United States, plans to spend $81 billion to meet surging regional demand.13 In early 2026, Duke Energy, which services pockets throughout the eastern United States, raised its spending plan by 18% to $103 billion through 2031.14 In total, U.S. utilities plan to spend at least $1.4 trillion between 2025 and 2030, and that figure is likely to increase as capital expenditure plans continue to grow.15

The Global X U.S. Electrification ETF (ZAP) is designed to capture this opportunity across two interconnected parts of the U.S. power system. The first is the utilities themselves, including both conventional electricity providers that form the backbone of America's existing power supply as well as alternative electricity providers supplementing the grid with new sources of power. The second is the grid infrastructure and smart grid technology companies that are building and modernizing the physical grid. This includes components such as transmission lines, substations, transformers, and power management systems that carry electricity from where it is produced to where it is needed. To be included, companies must generate at least 50% of their revenues from U.S. electricity markets, ensuring the fund remains tightly focused on the domestic buildout.

Energy Infrastructure: The Backbone of Global Energy Supply

Oil, natural gas, refined fuels, and the infrastructure that processes them remains the bedrock of global energy. Conventional fuels continue to supply most of the world's energy needs, and global demand for them continues to rise as economies grow, nations industrialize, and power needs multiply. Within this landscape, North America plays a critical role in meeting global energy demand. The United States and Canada are among the world's largest energy producers, underpinned by abundant reserves, integrated pipeline networks, extensive storage capacity, and rapidly expanding liquefied natural gas (LNG) export capacity. As energy needs grow and nations look to geopolitically stable regions for secure supply, North American energy infrastructure is increasingly well-positioned to meet those needs.

North American Energy Infrastructure: Moving Energy to Where It's Needed

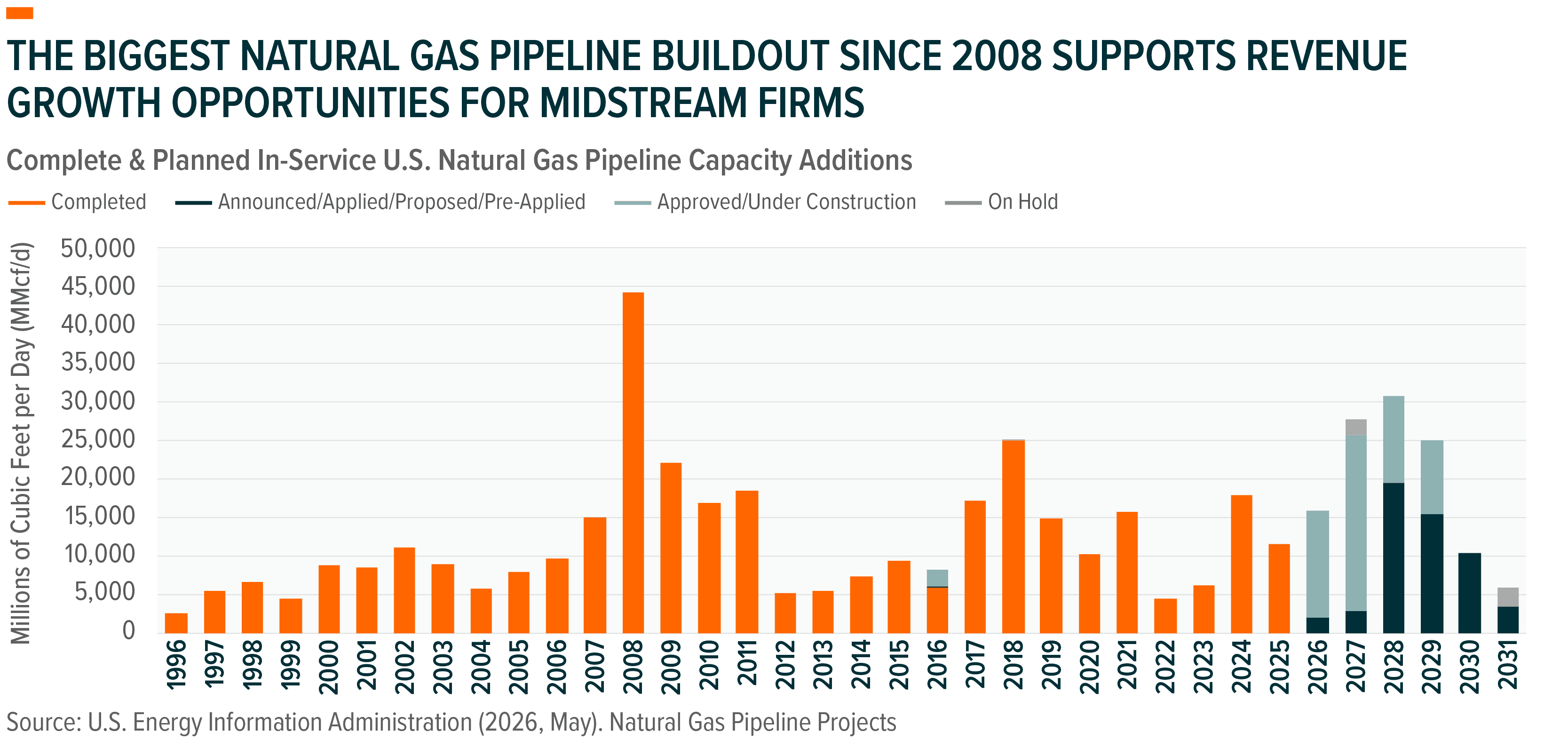

Before oil or gas reaches a power plant, a factory, or a home, it must be extracted, processed, transported, and stored. That physical journey is the domain of midstream energy infrastructure: the pipelines, processing facilities, storage terminals, and export facilities that form the backbone of the North American energy supply chain. Midstream companies typically operate these assets under long-term contracts, charging fees for the volumes that flow through their networks, meaning their revenues are driven more by throughput volumes flowing through their networks than by the price of oil or gas. The North American midstream network is among the most extensive and well-integrated in the world, connecting the continent's resource-rich production basins to consumers and export markets. As global demand for reliable energy supplies has intensified, accelerated by the supply disruptions of the 2020s, the strategic importance of that network has grown considerably.

Crises like the War in Iran left much of the world increasingly energy insecure, with calls for Canadian and American energy exports to fill the void. U.S. crude exports spiked to their two strongest months ever in April and May of 2026, with as many as 5.48 million barrels per day of oil trade rerouting away from the Strait of Hormuz and toward North American shores, underscoring the scale of demand.16 Furthermore, lasting physical and reputational damage to Middle Eastern supplies may have conferred a permanent geopolitical risk premium on trade throughout the region, solidifying the case for U.S. and Canadian energy exports.

Investors can access this opportunity through two complementary funds. The Global X MLP ETF (MLPA) invests exclusively in master limited partnerships (MLPs), publicly traded partnerships, predominantly in midstream energy infrastructure. These are publicly traded partnerships that distribute most of their recurring cash flows to investors, after paying operating, interest, and capital expenses required to maintain their existing asset base. By investing purely in MLPs, MLPA is a targeted choice for investors seeking regular income distributions. The Global X MLP & Energy Infrastructure ETF (MLPX) broadens that exposure by investing in both MLPs and traditional energy infrastructure corporations across the United States and Canada, a wider universe that balances income potential with greater exposure to the capital appreciation that accompanies midstream expansion. Together, the two funds offer investors a choice: pure MLP exposure, or broader infrastructure exposure that balances distributions with capital appreciation potential.

U.S. Natural Gas: Capturing the Global LNG Trade Amidst Rewiring Supply Chains

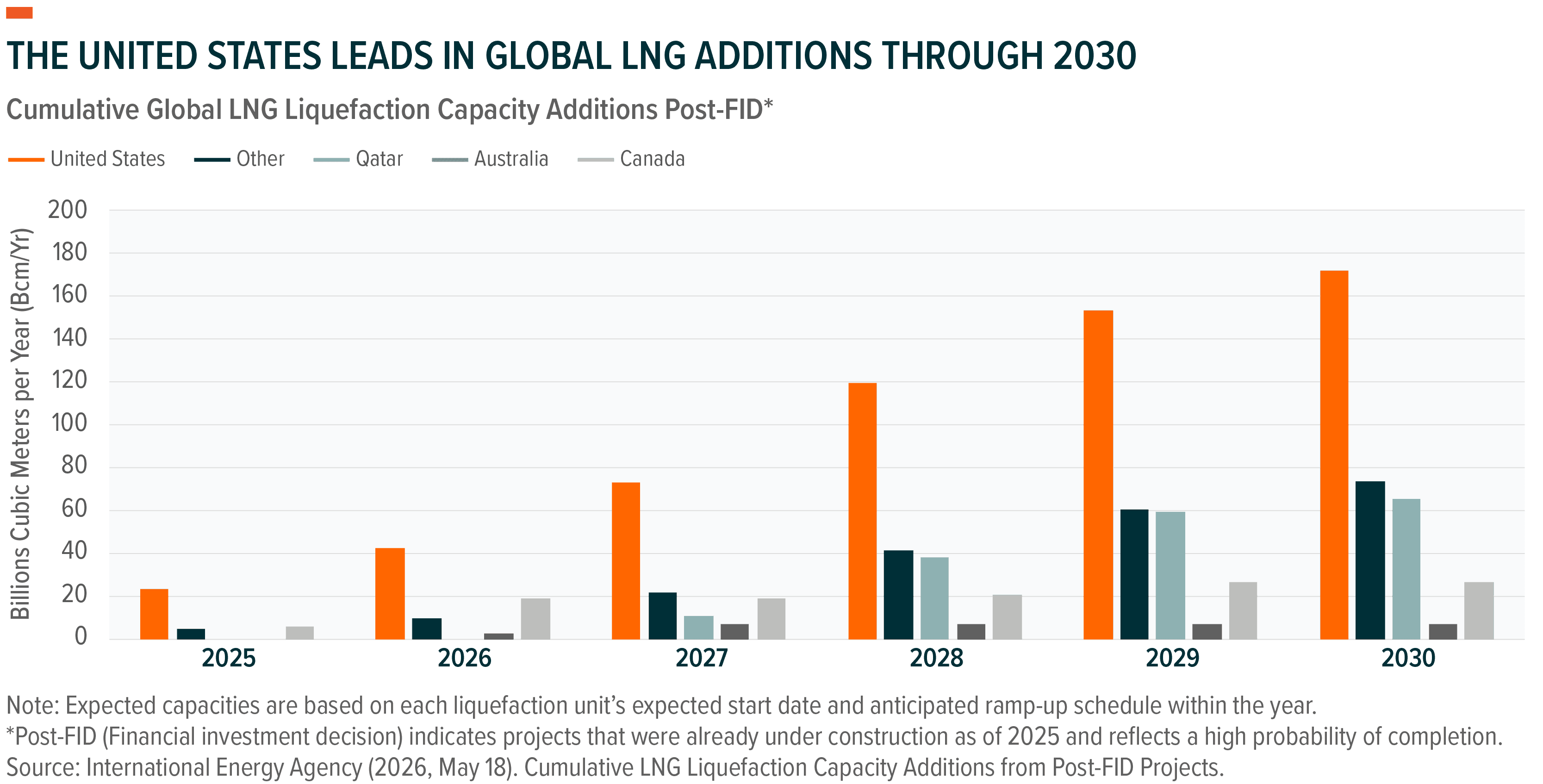

Natural gas plays a critical role in the global energy mix, responsible for 22% of worldwide power generation and serving as a primary source of heating, power generation, and critical industrial feedstock across the world.17 Liquefied natural gas, or LNG, is natural gas that has been cooled to its liquid state for transport, allowing it to reach international markets that are not connected by pipeline. As competition for reliable LNG supply has intensified, the United States has emerged as the world's leading exporter, a position it has held in nearly every year since 2022.18 The U.S. remains on track to nearly double its LNG export capacity by the end of the decade, with nearly 13.9 billion cubic feet per day of new capacity expected online by 2029, comprising just under half of all new supply additions globally.19

At the same time, LNG supply chains are adapting to the changing geopolitical landscape. Iran's 2026 attack on the world's largest LNG facility at Ras Laffan highlighted the importance of reliable LNG supply. The disruption temporarily removed roughly 17% of the LNG export capacity of Qatar, the world's second-largest exporter, underscoring the concentration of global energy supply.20 With new LNG export facilities requiring billions of dollars in investment and as long as five years to construct, lost capacity is not easily replaced.21 As a result, buyers may place greater emphasis on supply security when negotiating future contracts, leaning increasingly on the U.S. as the world’s largest source of new capacity.

Consequently, we believe U.S. natural gas production and export infrastructure plays an increasingly important role in global energy markets. The Global X U.S. Natural Gas ETF (LNGX) provides exposure to the full U.S. natural gas value chain, from the upstream producers extracting gas from America’s prolific basins to the midstream pipelines, processing facilities, and export terminals that feed domestic consumers and international markets. For investors, LNGX offers a way to participate in what we believe is a structural growth opportunity for the U.S. natural gas industry.

Alternative Energy: Beyond Conventional Power Sources

The world's growing electricity needs cannot be met by any single source. Alternative sources of power such as nuclear, renewables, energy storage, and hydrogen are among the expanding scope of solutions that can add meaningful power capacity, reduce reliance on imported fuels, and help nations build more resilient power grids. Almost every country on earth has the potential to generate more electricity from alternative sources than it currently consumes.22 Additionally, in just four years since the 2022 energy crisis, many of these technologies have become substantially cheaper and more readily deployable.23

The development timelines for many alternative power technologies compare favorably to conventional energy projects. For example, a 1 gigawatt (GW) solar installation can be built in roughly one to two years, versus three to four years for an equivalent gas plant.24 The development speed and scalability could make several alternative power resources a near-term solution to the world’s growing energy needs, as well as a long-term structural story.

Nuclear Power: Reliable, Around-the-Clock Electricity with a Minimal Physical Footprint

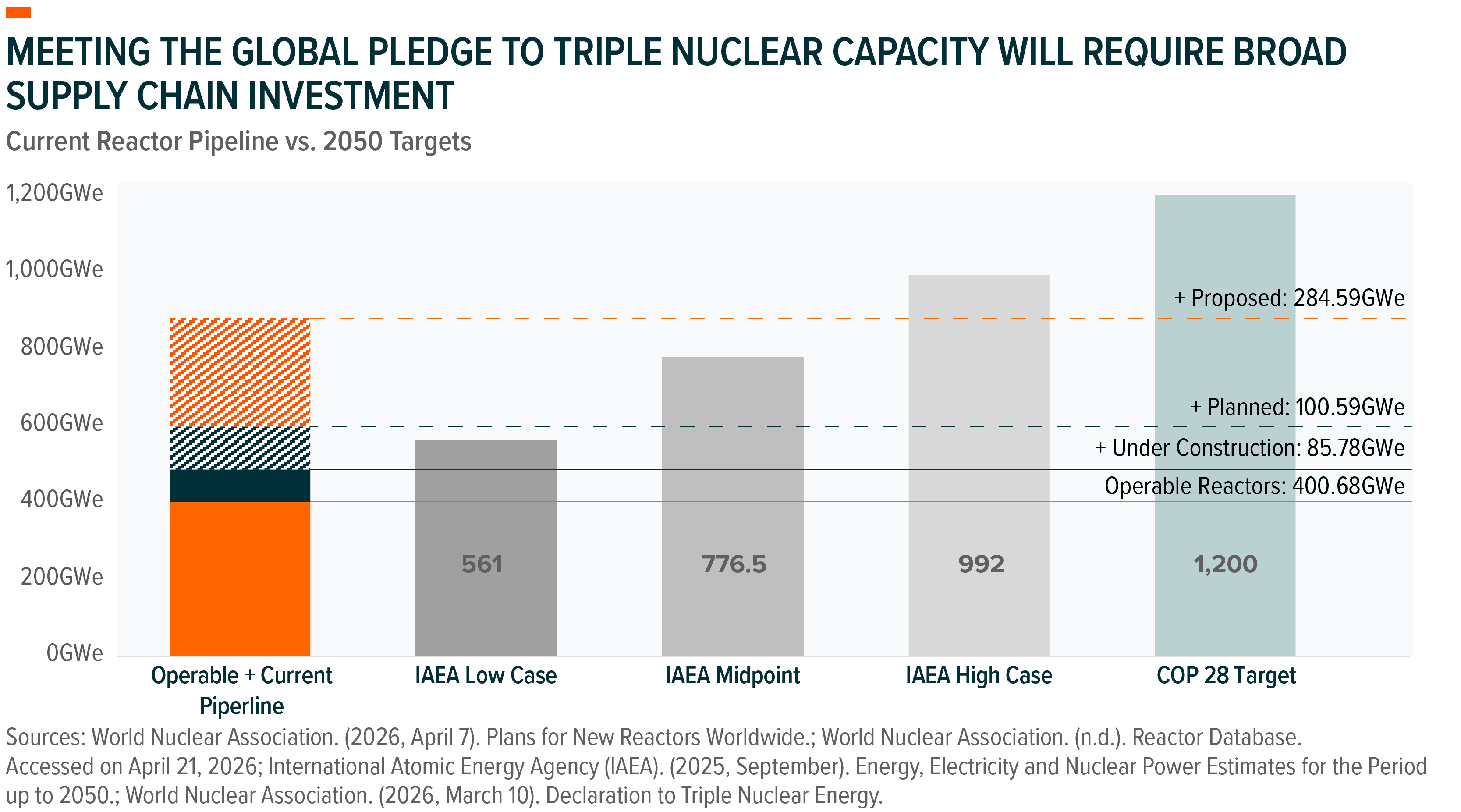

Nuclear power, which accounts for roughly 9% of global electricity generation, is one of the few energy sources capable of providing continuous, around-the-clock power, on a reliable basis.25 Nuclear reactors are fueled by uranium and, once built, can operate for decades with proper maintenance.26 Combined with low lifecycle carbon emissions, these characteristics have sparked a renewed interest in nuclear power as countries seek reliable sources of electricity. That interest is reflected in growing policy support, with 42 countries endorsing a pledge to triple global nuclear generation capacity by 2050.27

The case for nuclear has strengthened considerably in recent years. Nations with significant nuclear capacity have arguably proven more resilient to oil and gas supply shocks than those primarily dependent on imported fuels. South Korea, shaken by its dependence on Middle Eastern energy exports amidst the Iran War, announced plans to expedite reactor restarts within weeks of the conflict's outbreak. 28 France, which generates over 70% of its electricity from nuclear, has remained largely insulated from the fossil fuel supply shocks that have destabilized other major economies.29 By Q2 2026, Japan had already restarted 15 of its 33 operable reactors following mandatory shutdowns in the aftermath of Fukushima, and seeks to double its nuclear output by 2040.30

Beyond energy security, nuclear power is attracting demand from new and powerful buyers. Microsoft, Google, and Amazon have all signed long-term agreements with nuclear utilities to supply power to data centers across the United States, underscoring nuclear's reliability and scalability.31 Governments have responded as well, with policy announcements supporting reactor life extensions, new constructions, and nuclear fuel enrichment flooding headlines. Looking ahead, small modular reactors (SMRs) represent a potential next frontier of nuclear innovation. Their modular, standardized designs could shorten deployment timelines and bring down cost curves, expanding nuclear's potential across data centers, industrial facilities, and remote power applications.

As countries seek reliable sources of electricity and invest in new grid capacity, opportunities are emerging across the nuclear ecosystem. The Global X Uranium ETF (URA) provides exposure across the full nuclear supply chain, from uranium miners and fuel suppliers to reactor manufacturers and companies developing advanced nuclear technologies, including small modular reactors (SMRs). URA offers a single point of access to the nuclear ecosystem at a moment of rising demand, global policy support, and technological innovation.

Renewable Energy Producers: Generating Power from Wind, Solar, and Beyond

Renewable energy producers are the utilities and independent power companies that own and operate wind power sites, solar power installations, and other renewable power assets. With these assets, they generate electricity and sell it to the grid or directly to corporate buyers. Renewables reached a landmark milestone in 2025, accounting for just over a third of global power generation and overtaking coal as the world’s largest source of electricity for the first time.32 Solar power installations alone covered 75% of all electricity demand growth last year, the largest annual increase ever recorded by any single power source outside of post-crisis recoveries.33,34

The outlook for renewables is supported by cost competitiveness, favorable government policies, and continued technological advancements. Corporate power purchase agreements are also a significant tailwind for many renewables developers and producers. Tech companies including Amazon, Meta, Microsoft and Alphabet have signed agreements totaling over 80 gigawatts of renewable energy in the United States alone.35 For example, Brookfield Renewable and Microsoft signed one of the largest single agreements, with the renewables developer providing 10.5 gigawatts of wind, and solar, and energy storage to the tech giant.36

Through 2040, solar power could make up 59% of net capacity additions, while wind and energy storage could make up an additional 18% and 19%, respectively.37 The Global X Renewable Energy Producers ETF (RNRG) provides exposure to the companies generating that power, targeting those that derive at least 50% of their revenues from wind, solar, and other renewable power resources worldwide.

.png)

ClimateTech: The Components at the Center of the Alternative Energy Buildout

ClimateTech companies manufacture the components and technologies that make renewable energy systems work, such as solar panels, inverters, wind turbines, energy storage batteries, fuel cells, and the smart grid technologies that can help manage and distribute power across increasingly complex electricity networks.

The scale of demand for these products is already substantial and growing. Battery energy storage systems were the fastest-growing power technology globally in 2025, with 108 gigawatts of new capacity added in a single year.38 Battery energy storage systems are an increasingly critical part of grids because they make renewables more reliable and dispatchable on demand.

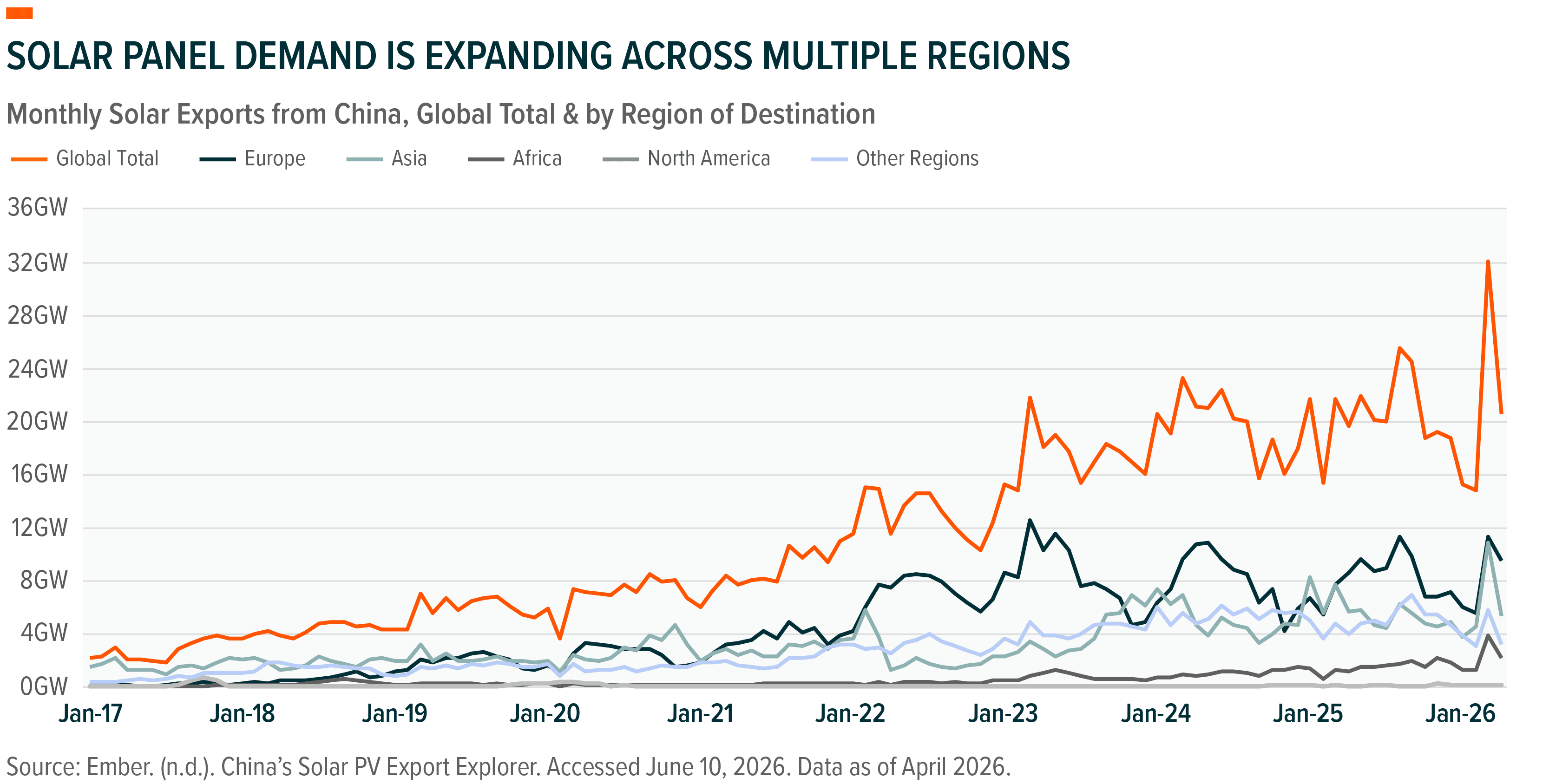

Additionally, solar component exports from China, the dominant global supplier, reached 68 gigawatts in March 2026 alone, more than double the prior month, with demand expanding rapidly across Europe, Asia, Latin America, and Africa.39 As the buildout of alternative power accelerates globally, the market for equipment will likely expand.

The long-term demand picture is further supported by policy commitments. 139 countries, 333 cities, and over 1,200 companies, including Amazon, Meta, Microsoft, and Walmart, have pledged to reach net zero emissions, typically by 2050.40 The Global X ClimateTech ETF (CTEC) provides exposure to the manufacturers and technology developers supplying the components at the heart of the growing adoption of alternative electricity.

Hydrogen: A Versatile Fuel for the Next Generation of Power

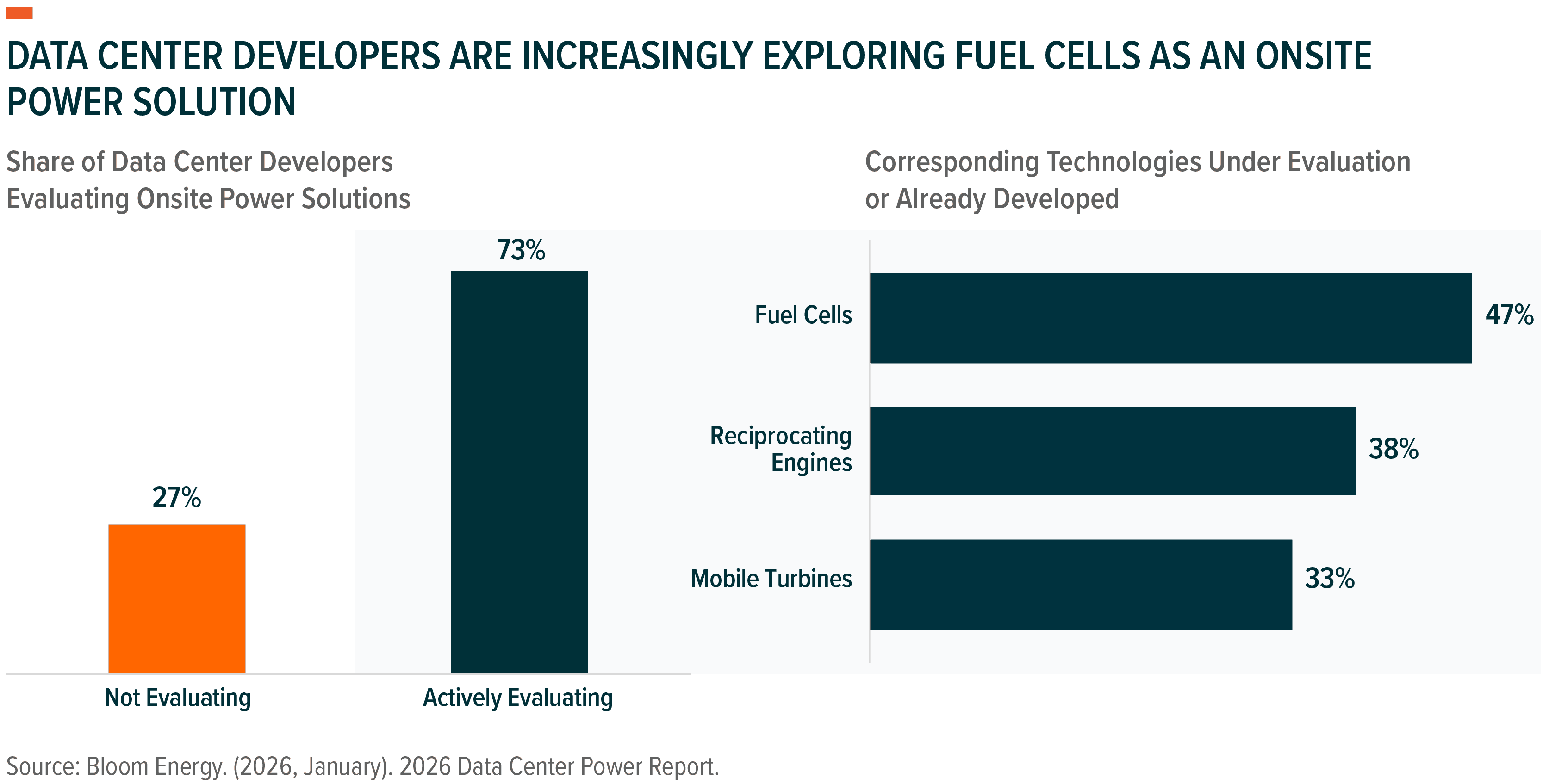

Hydrogen has a wide range of use cases, including for power generation and long-duration energy storage applications. For example, hydrogen fuel cells can serve as onsite power solutions. A fuel cell is a device that generates electricity through a chemical reaction hydrogen, can operate continuously, and can be deployed onsite in a matter of weeks rather than the months or years required for grid infrastructure. They can also run on a range of fuels, including hydrogen and natural gas.

That combination of speed and reliability is driving rapid adoption among data center operators seeking power solutions independent of the grid. A recent survey found that 73% of data center developers were actively evaluating onsite power solutions, with 47% of those considering fuel cells as their preferred option.41

Beyond its power applications, hydrogen's high energy density and adaptability gives it the potential to be used in other applications, including as a fuel for long-haul transport, in heating systems, and as a chemical feedstock for fertilizers, steel, and other materials. Current agreements span a wide range of industries looking to reduce reliance on conventional fuel supply chains, pointing to a hydrogen opportunity that extends well beyond any single use case.

The industry remains in the early stages of commercial adoption and costs are still elevated relative to conventional alternatives, but the pace of deployment is accelerating, and costs are expected to fall as the technology scales. The Global X Hydrogen ETF (HYDR) provides exposure to the full hydrogen value chain, from the companies producing hydrogen to the fuel cell producers converting it into power, as well as the companies positioned to benefit as the hydrogen industry matures.

Critical Materials: The Building Blocks of the Energy Supercycle

The technologies driving the energy supercycle – from power grids and energy storage to EVs and AI infrastructure – cannot be built, scaled, or sustained without a reliable supply of critical materials. These materials do not generate power or transmit electricity themselves, but they are the foundation beneath every electrification technology. Years of underinvestment in mining and processing capacity mean supply could struggle to keep pace in the coming years, creating new and urgent opportunities for the miners of these critical materials.

Lithium & Battery Tech: Enabling Electrification at Scale

Higher electricity demand and the electrification of transport are creating the need for batteries. The rise of renewable energy sources, whose output fluctuates with weather and daylight, is increasing the need for energy storage. The widespread adoption of EVs and surging demand for onsite power solutions from data centers are also creating new opportunities for battery systems and the materials that are critical to their operation.

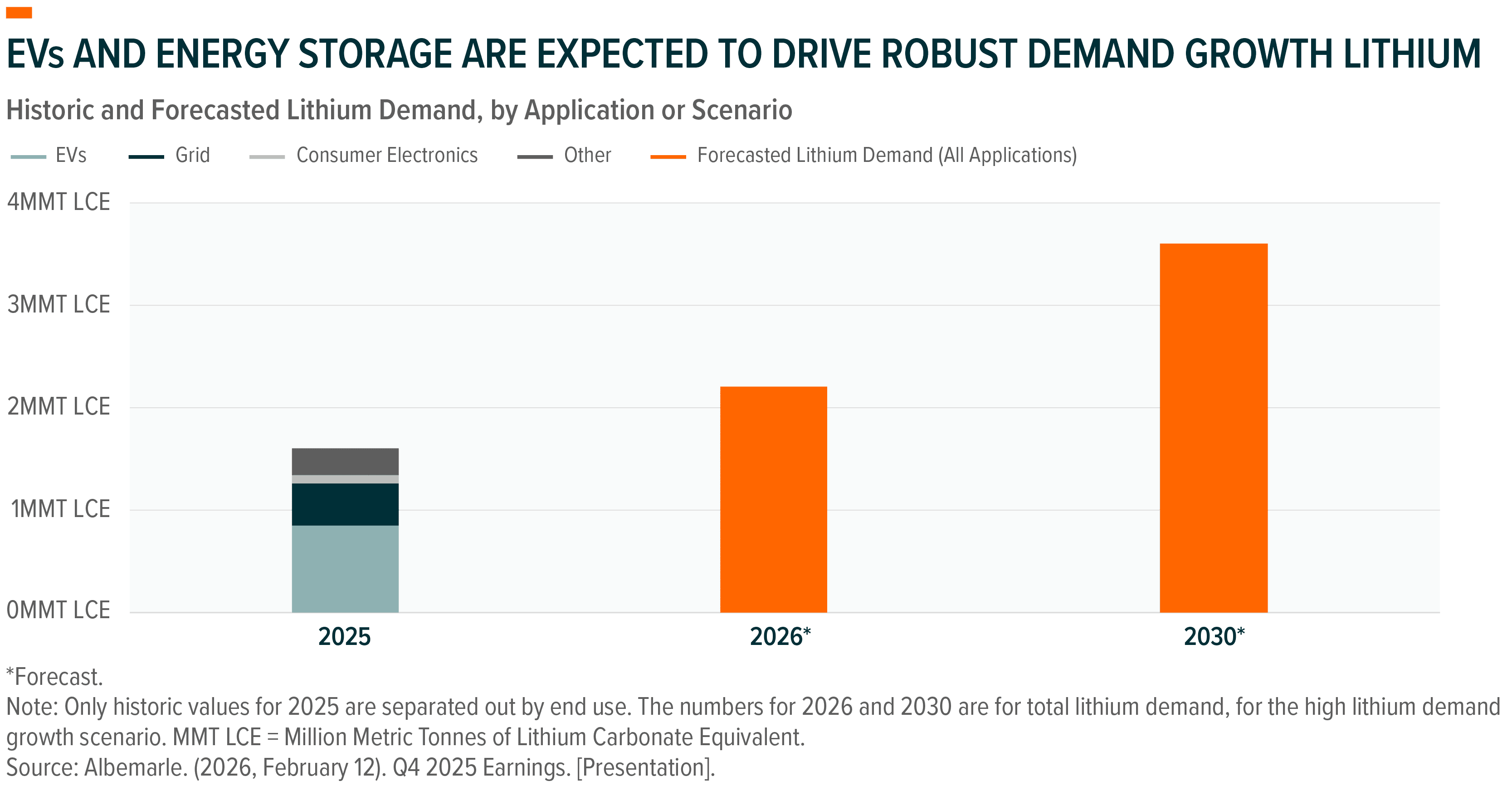

The shift from gasoline-powered vehicles to electric ones is one of the primary drivers of rising electricity consumption. Most EVs run on a lithium-ion battery, which is expected to remain the dominant EV battery chemistry for the foreseeable future, given its combination of energy density, cost, and scalability. Global EV sales grew 22% in 2025 to reach 21.4 million units, accounting for nearly one in four cars sold worldwide. By 2040, EV sales are forecast to surpass 78 million units or nearly 70% of global vehicle sales, pointing to sustained and growing lithium demand from the transportation sector alone.42

Energy storage is also emerging as an increasingly important driver of lithium demand. Utilities are deploying grid-scale battery systems to support grid reliability and integrate renewable energy sources, while data center operators and other large power consumers are investing in onsite battery systems to improve power resilience. Falling costs are accelerating adoption. Energy storage is forecast to decline from $107 per megawatt-hour in 2024 to $58 by 2035.43 Looking forward, battery energy storage demand for lithium is forecast to grow from 250,000 metric tons of lithium carbonate equivalent (LCE) in 2025 to more than one million metric tons LCE by 2030 – more than a fourfold increase in five years.44

Together, EVs and energy storage are expected to drive a near doubling of global lithium demand by the end of this decade – from 1.6 million metric tons LCE in 2025 to as much as 3.6 million metric tons LCE by 2030.45 The Global X ETF Lithium & Battery Tech ETF (LIT) seeks to capture this opportunity by providing exposure to companies across the lithium supply chain, including miners, processors, and battery manufacturers worldwide.

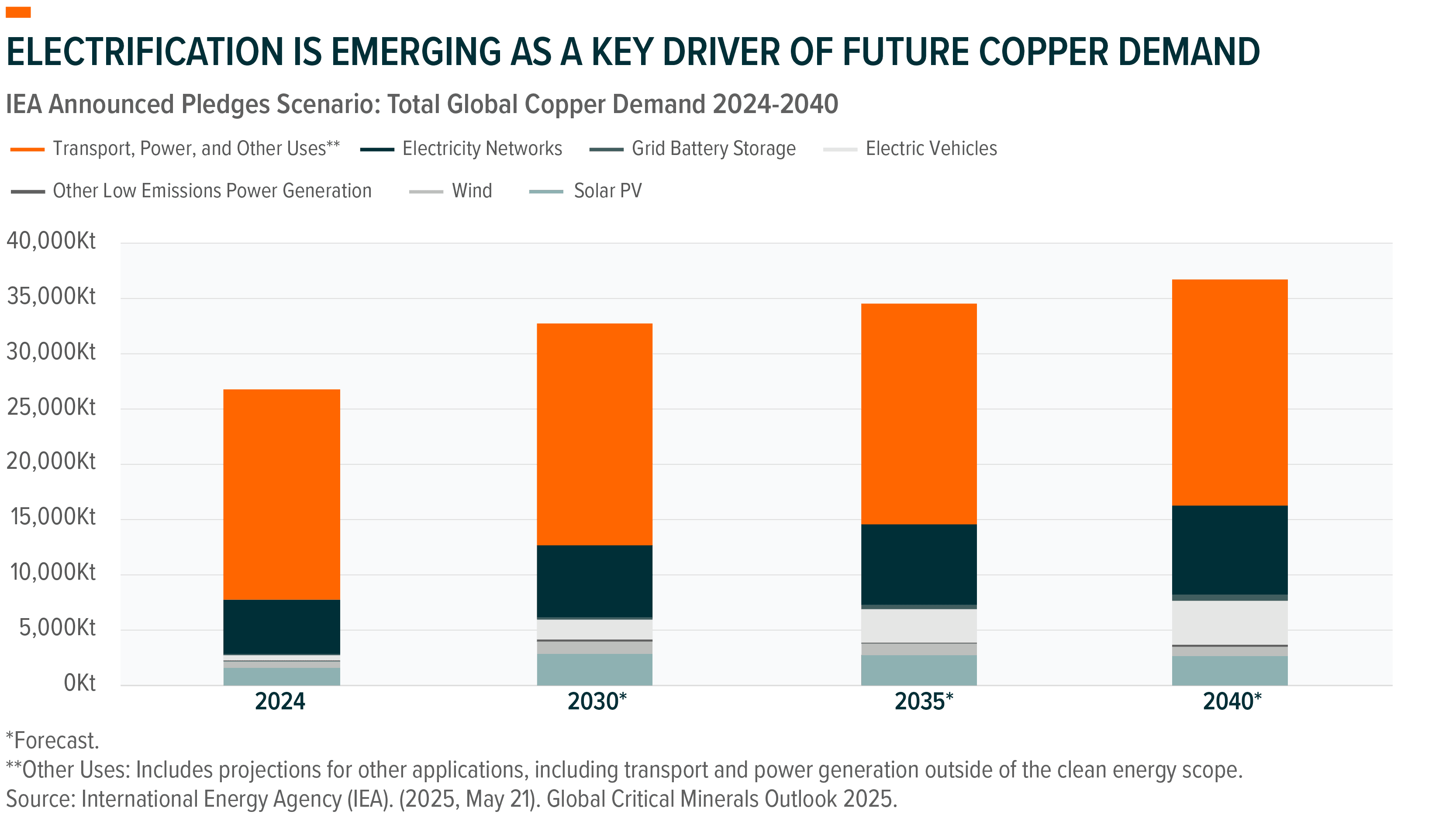

Copper Miners: The Veins of the Modern Economy

Copper plays a critical role in power grids, electric vehicles, data centers, and industrial infrastructure. Given its highly conductivity and corrosion-resistant properties, copper is likely to remain a key input across many of these technologies. As electricity demand grows and investment in energy infrastructure accelerates, demand for copper is expected to increase alongside it.

Historically, copper demand has been driven primarily by construction and industrial activity. Today, electrification has emerged as an increasingly important source of growth. Power grids require copious amounts of copper to transmit and distribute electricity, while electric vehicles use three to five times more copper than traditional internal combustion engine vehicles.46 At the same time, the rapid expansion of data centers and renewable energy infrastructure is creating an additional layer of demand.

Industry forecasts suggest global copper demand could rise from 26.7 million metric tons in 2024 to as much as 34.6 million metric tons by 2035.47 Supply, however, is unlikely to keep pace. New greenfield mines can take over a decade to develop, even as ore grades on existing mines are declining, and processing capacity remains constrained.48 Beyond these structural challenges, geopolitical factors that seek to secure domestic supply chains for critical minerals may further fragment copper supply.

For copper miners, that dynamic is significant: a sustained supply gap has the potential to support copper prices and producer margins for years to come. The Global X Copper Miners ETF (COPX) provides exposure to a broad range of copper mining companies, which include the largest global miners whose revenues and margins are most directly tied to the structural dynamics shaping the copper market.

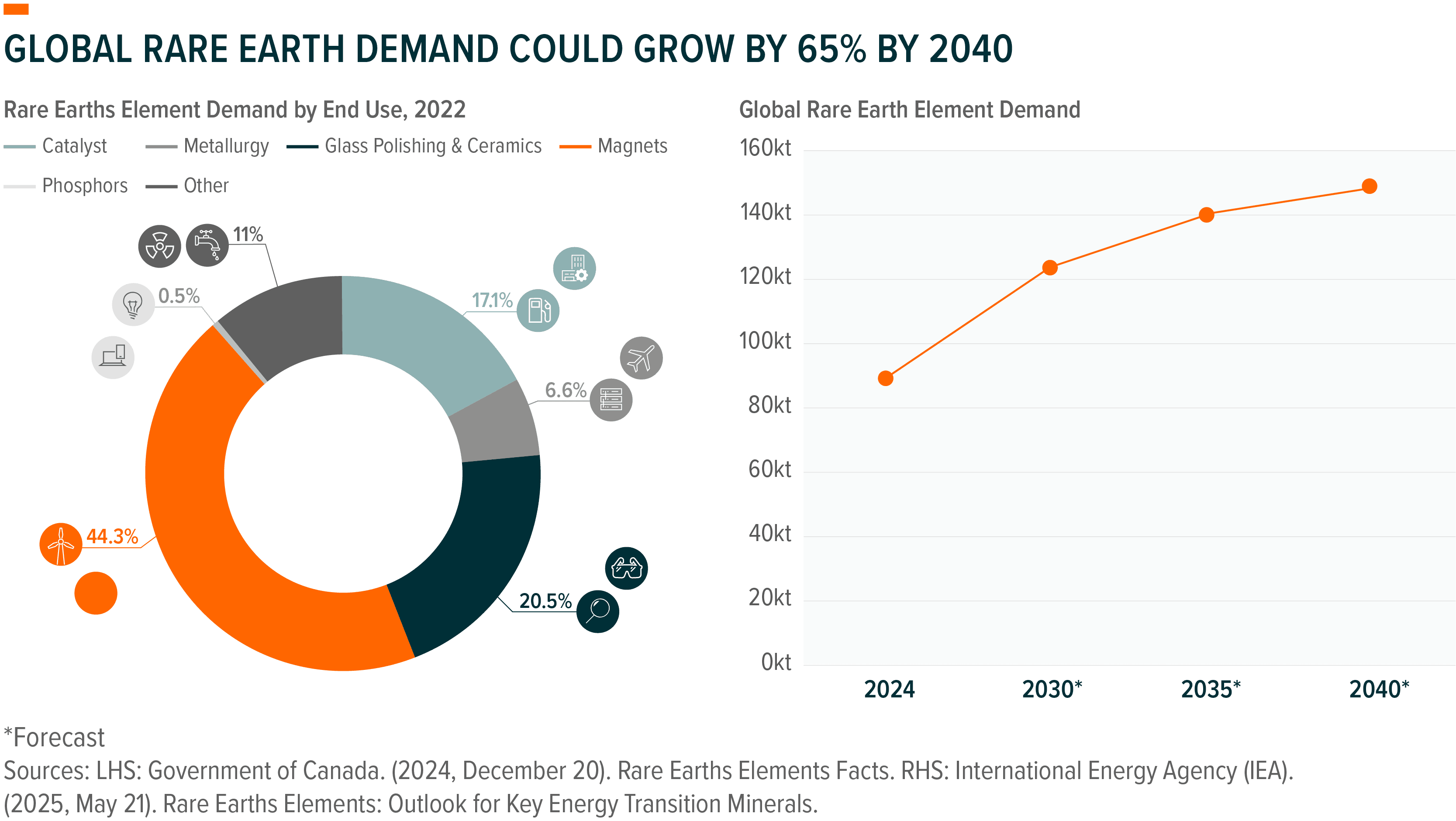

Rare Earths: The Hidden Inputs Powering the Modern Economy

Rare earth elements are a group of 17 metallic elements essential to the motors, magnets, and semiconductors that make clean energy technology work. For example, every EV on the road relies on rare earth magnets in its motor, while every wind turbine depends on them in its generator. As electrification accelerates and clean energy capacity expands, demand for rare earths is forecast to grow 65% by 2040.49

Despite being relatively abundant in the earth's crust, rare earths are difficult to refine. China controls nearly 90% of global refining capacity, giving it decisive leverage over a supply chain the world's clean energy buildout depends on.50 The U.S. and its allies are committing substantial capital to reduce that dependence and build domestic supply chains, with the Inflation Reduction Act alone earmarking over $40 billion for domestic EV and battery supply chains including rare earths.51 Additionally, the U.S. Department of Defense took a stake in MP Materials, the only company running a rare earth mine in the United States.52

The Global X Rare Earth & Critical Materials ETF (EART) provides exposure to the rare earth miners, processors, and critical materials suppliers positioned to benefit as that supply chain rebuild accelerates.

Conclusion

The forces reshaping the global energy system, surging power demand, the reordering of supply chains, the scaling of alternative power, and the critical materials underpinning it all, are structural, not cyclical. They are interdependent parts of the same supercycle, and no energy source is sufficient to carry the load alone. The investment required in both energy and materials to fuel global growth is immense, even as nations race to secure increasingly scarce sources of supply. For investors, the risk may be assuming that the strategic importance of energy and materials is reflected in their relatively small weight within broad market indexes. In a world increasingly defined by energy security, electrification, and resource competition, the sectors enabling those trends become difficult to ignore.

Related ETFs

COPX – Global X Copper Miners ETF

CTEC – Global X ClimateTech ETF

EART – Global X Rare Earth & Critical Materials ETF

LIT – Global X Lithium & Battery Tech ETF

LNGX – Global X U.S. Natural Gas ETF

MLPX – Global X MLP & Energy Infrastructure ETF

RNRG – Global X Renewable Energy Producers ETF

ZAP – Global X U.S. Electrification ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.