Artificial Intelligence

AI Infrastructure Deals Are Getting Bigger and More Frequent

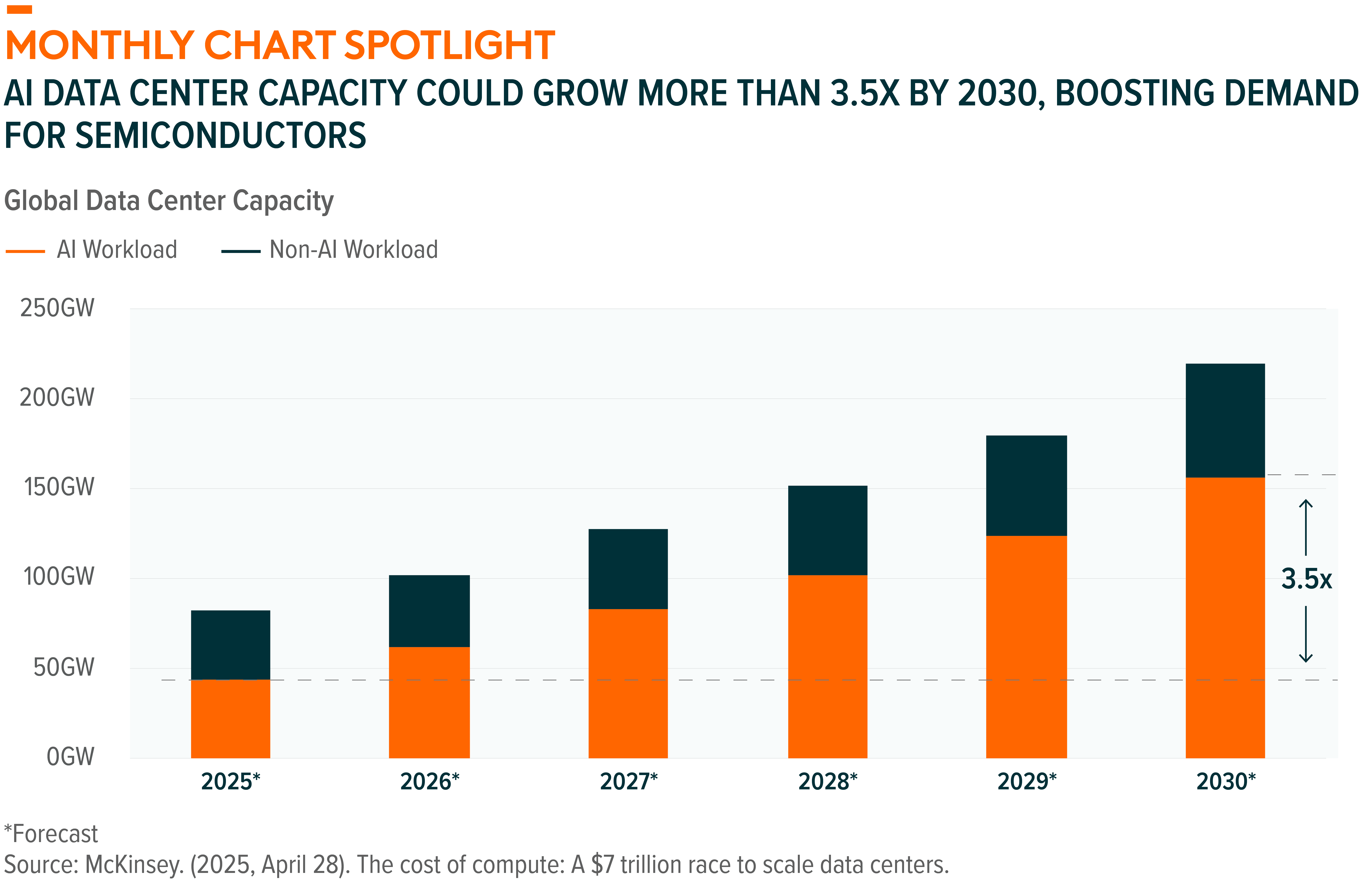

OpenAI and Nvidia inked a landmark deal under which OpenAI will deploy at least 10 gigawatts (GW) of Nvidia systems for its next-gen AI infrastructure. Nvidia will progressively invest up to $100 billion as each gigawatt is built.1 OpenAI also struck a multiyear deal with Advanced Micro Devices (AMD) to supply up to 6 GW of its MI450 graphics processing units (GPUs), with an option for OpenAI to acquire a roughly 10 % stake in AMD via warrants tied to milestones.2 CoreWeave expanded its infrastructure agreement with OpenAI by an additional $6.5 billion, bringing the total value of their relationship to about $22.4 billion across several contract rounds.3 CoreWeave also secured a $14.2 billion AI infrastructure contract with Meta through December 2031, further cementing its role as a GPU cloud operator.4 Collectively, these deals underline how AI leaders are locking in large-scale compute capacity and securing diversified hardware and cloud partnerships to scale ever faster.

![]()

Defense Technology

Palantir Secures Major UK Defense Contract to Power AI-Driven Operations

The UK Ministry of Defence agreed to a £750 million contract with Palantir to integrate AI systems across its armed forces. It’s part of a broader partnership valued at up to £1.5 billion over several years, through which Palantir will invest in UK defense innovation and establish London as its European defense hub. The initiative will fuse data across the UK’s military systems—covering logistics, personnel readiness, maintenance schedules, and real-time battlefield awareness—to give commanders a unified, intelligence-driven operational view. The agreement extends Palantir’s existing presence beyond the Royal Navy’s Project Kraken into the Army, Air Force, and broader UK defense ecosystem.5 Broadly, the move illustrates how AI and data analytics are rapidly becoming central to military operations, not just in intelligence but across logistics, readiness, and command. Also, the UK’s embrace of such cutting-edge systems signals its intent to become a leading NATO force in advanced defense technologies.

![]()

Robotics & Artificial Intelligence

Industrial Robotic Stock Has Increased Worldwide

Global industrial robot installations totaled approximately 542,000 units in 2024, more than doubling over the past decade. Asia led the charge, representing 74% of all new deployments, while Europe and the Americas followed with 16% and 9%, respectively. China alone installed 295,000 robots—about 54% of the global total—and, for the first time, domestic manufacturers surpassed foreign suppliers in their home market. The global stock of industrial robots now tops 4.66 million units, up roughly 9% year-over-year (YoY). Installations are forecast to grow another 6% in 2025 and exceed 700,000 annually by 2028, underscoring automation’s relentless advancement.6 Driving this momentum are smarter, more adaptable robots powered by AI, falling deployment costs amid rising labor expenses, and a global push toward reshoring and supply chain resilience.

![]()

Data Centers & Digital Infrastructure

U.S. Data Center Build Hits an All-Time High

Construction spending on U.S. data centers reached a record $40 billion at a seasonally adjusted annual rate in June 2025, a roughly 30% YoY jump following the 50% YoY increase in 2024.7 The boom is fueled by accelerating demand from generative AI and machine learning workloads, which are straining power grids and compute infrastructure. Massive investments by Big Tech hyperscalers such as Microsoft, Amazon, Google, and Meta are responsible for much of this growth. For example, in September, Microsoft announced a $3.3 billion plan to build a hyperscale AI data center campus in Wisconsin, with an additional $4 billion committed over the next three years.8 All told, hyperscalers’ capital expenditures are forecast to reach nearly $400 billion in 2025, with much of it directed towards data centers.9 The scale of this construction boom highlights how intense the AI race has become. It’s not just about better models; it’s also about owning the physical infrastructure to train and deploy them.

![]()

HealthTech

Digital Health Platforms Move Into Men’s Hormonal Care With New Testosterone Treatments

Leading telehealth platform Hims & Hers launched a range of personalized low-testosterone treatments for men. The company now offers tailored doses of compounded enclomiphene, a medication that naturally boosts testosterone production without compromising fertility. It also offers a combination therapy pairing enclomiphene with tadalafil for men experiencing hormonal and sexual symptoms. Beginning in 2026, Hims will add Kyzatrex, a U.S. Food and Drug Administration (FDA)-approved oral testosterone therapy offered exclusively through its platform in partnership with Marius Pharmaceuticals, a significant step toward needle-free, accessible care. The company also plans to introduce injectable options for users seeking more traditional delivery methods. All treatments begin with at-home diagnostic testing, enabling customers to complete evaluation, lab work, and prescription entirely online within days.10 This launch reflects Hims’ broader strategy to expand beyond telemedicine into comprehensive digital healthcare, positioning it as a key player in the fast-growing digital health and men’s wellness market.

![]()

Hydrogen

Investment in the Maturing Hydrogen Industry Soars

Global investment in green hydrogen has surpassed $110 billion, as of September 2025, backing over 500 projects already operating, under construction, or past the final investment decision stage. Committed production capacity now exceeds 6 million tonnes per year, with 1 million already operational. The broader pipeline suggests potential for 9–14 million tonnes by 2030. China leads with $33 billion in committed investments, followed by North America at $23 billion. Europe ranks third at $19 billion, though it is forecast to account for nearly two-thirds of global hydrogen demand by 2030. Amid this growth, about 50 weaker projects have been cancelled over the past 18 months, signaling an industry shifting from early enthusiasm toward execution.11 While some projects may not reach final development stages, the robust pipeline and advancement of more than 500 projects point to the growing opportunities within the hydrogen industry.

![]()

KEEP UP WITH THE LATEST RESEARCH FROM GLOBAL X

To learn more about the disruptive themes changing our world, read the latest research from Global X, including:

- Introducing CHPX: The Case AI Semiconductors & Quantum Computing

- The Next Big Theme: September 2025

- Inflection Points: No Reservations, Just Valuations

- The Next Big Theme: August 2025

- Investing in AI: Why Data Centers? Why DTCR?

ETF HOLDINGS AND PERFORMANCE

To see individual ETF holdings and current performance across the Global X Thematic Suite, including information on the indexes shown, click these links:

- Disruptive Technology: Artificial Intelligence & Technology ETF (AIQ), Blockchain ETF (BKCH), Robotics & Artificial Intelligence ETF (BOTZ), Cybersecurity ETF (BUG), Cloud Computing ETF (CLOU), Autonomous & Electric Vehicles ETF (DRIV), Data Center & Digital Infrastructure ETF (DTCR), FinTech ETF (FINX), Video Games & Esports ETF (HERO), Lithium and Battery Tech ETF (LIT), Defense Tech ETF (SHLD), Internet of Things ETF (SNSR), Social Media ETF (SOCL), U.S. Electrification ETF (ZAP)

- Consumer Economy: Millennial Consumer ETF (MILN), E-Commerce ETF (EBIZ), Genomics & Biotechnology ETF (GNOM), Aging Population ETF (AGNG), HealthTech ETF (HEAL)

- Infrastructure & Environment: U.S. Infrastructure Development ETF (PAVE), CleanTech ETF (CTEC), Renewable Energy Producers (RNRG), Clean Water ETF (AQWA), Hydrogen ETF (HYDR), AgTech & Food Innovation ETF (KROP), Infrastructure Development ex-U.S. ETF (IPAV)

- Digital Assets: Blockchain & Bitcoin Strategy ETF (BITS), Bitcoin Trend Strategy ETF (BTRN)

- Multi-Theme: Dorsey Wright Thematic ETF (GXDW)